How (and When) to Pay Off Your Mortgage Early

When you take out a mortgage, especially one with a 30-year term, it can feel like you’ll never reach the finish line of owning your home “free and clear.” The good news is you can pay off your mortgage early. Doing so can save you money and give you peace of mind, but you should understand what happens when you pay off your mortgage and what trade-offs you could be making.

On this page

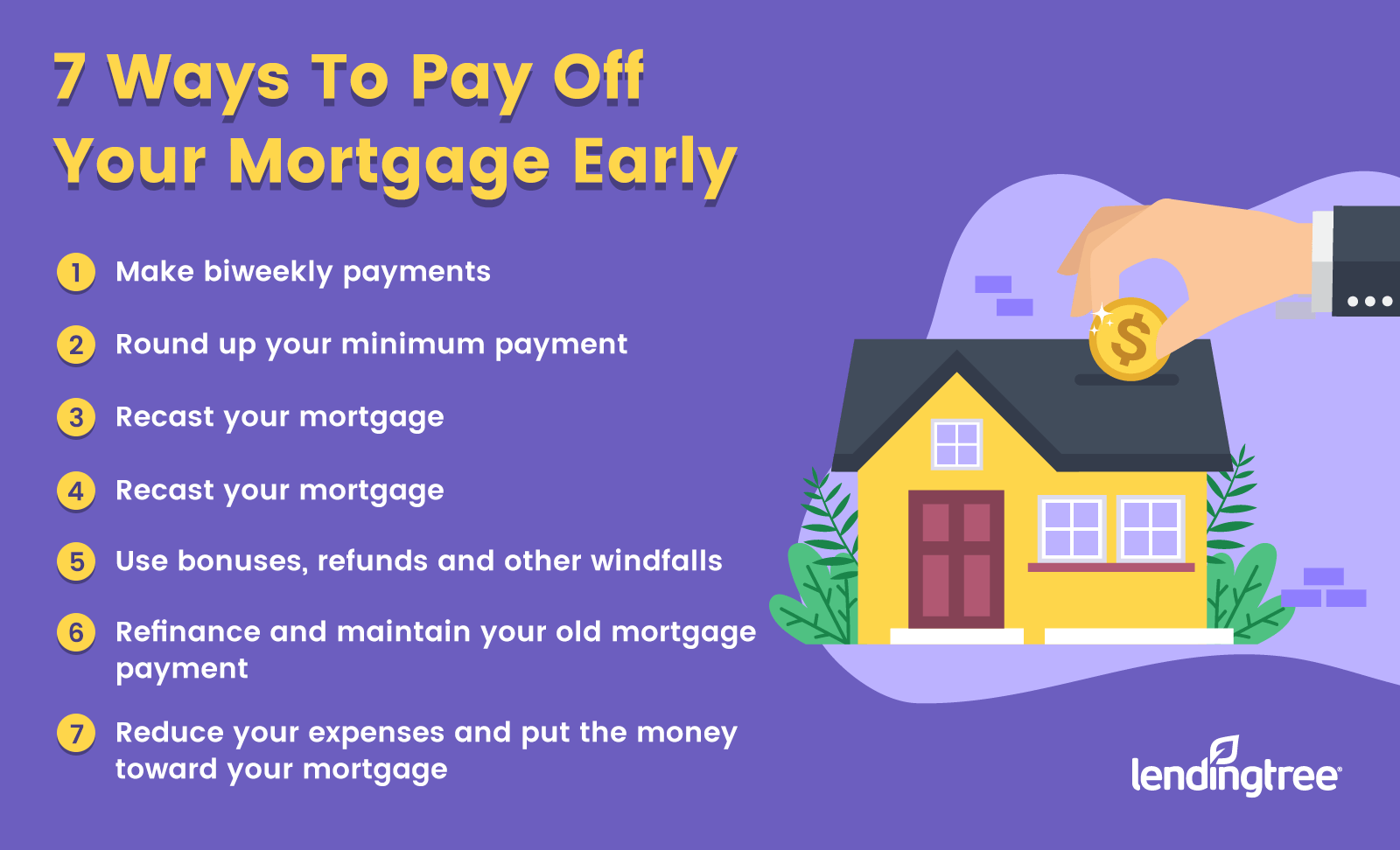

7 ways to pay off your mortgage early

- Make biweekly payments. Split your monthly mortgage payment in half and make biweekly payments instead. At the end of a calendar year, you would’ve made 26 half payments (since there are 52 weeks in a year) — which equals 13 full payments — instead of the 12 you’d normally make. You can shave about four years off of a 30-year loan term with this method. Remember to check with your mortgage company first, as some lenders impose penalties for making “extra” payments or paying off your mortgage early.

- Round up your minimum payment. Try rounding your minimum payment up to the next $100. For example, if you owe $1,015 on your mortgage each month, pay $1,100 instead. Even better, pay $1,200 monthly if you can comfortably afford it. Don’t forget to indicate to the lender that the extra amount should be applied to your principal balance (and if you run into any issues with payments being promptly and correctly credited to your account, know your rights as a borrower).

- Recast your mortgage. If you have a lump sum, such as $5,000 or $10,000, consider a mortgage recast. You’d pay the money to your lender to reduce your loan principal and recalculate your mortgage payments. Your term won’t change, but your new payments would be lower, giving you room to pay extra toward your principal as frequently as possible. A recast can be a good alternative to a refinance because you’ll pay fewer fees. A recast isn’t allowed for those with FHA or VA loans, but you can still get ahead by using your lump sum to make extra mortgage payments.

- Use bonuses, refunds and other windfalls. Whenever you get a bonus from work, an income tax refund or another financial windfall, put that extra money toward paying down your loan principal.

- Refinance and maintain your old mortgage payment. If you qualify for a mortgage refinance to get a loan with a lower refinance rate and monthly payment, keep making your original payments to pay off your mortgage faster. Refinancing may be more appealing to those borrowers with a higher mortgage rate, because the amount you stand to save will likely outweigh the costs and fees that come with a refinance.

- Make one extra payment each calendar year. You can also combine one or more of the methods above with making one additional payment each year. For example, if you pay biweekly, plus make an extra full payment, that’s 14 full payments you’d make each year.

- Reduce your expenses and put the money toward your mortgage. Depending on how quickly you want to pay off your mortgage, you may want to reduce small, recurring expenses or target the biggest ones in your budget. This could look like cutting down on dining out and canceling a few streaming subscriptions or downsizing your home — choose the lifestyle changes that will help you meet your financial and quality of life goals.

Should you pay off your mortgage faster?

It may seem like paying off your mortgage early is a no-brainer if you can afford to do it. But before you start aggressively paying down your principal, you should look at your overall financial picture and make sure it’s the best use of your extra money.

Reasons for paying off your mortgage early

- Getting rid of your biggest monthly payment. Your mortgage is likely the largest monthly expense you have. If you plan to stay in your home for the long haul, getting rid of your monthly mortgage payments sooner means you can unlock more disposable income to bulk up your savings or retirement funds, invest in stocks or cover other expenses with cash rather than credit.

- Reducing your foreclosure risk. There’s real security in owning a home free and clear. As long as you still owe a balance on your mortgage, there’s the possibility you could lose your home to foreclosure if you ever default on your payments. Although you’re still responsible for property taxes and homeowners insurance after your mortgage is paid off, knowing you no longer have a loan against your home can be a huge stress reliever.

- Saving money on interest. The more time you spend paying down your mortgage, the more you’ll pay in interest. For example, if you take out a $250,000 loan with a 5.75% interest rate and a 30-year term, you’ll pay a total of $275,215.57 in interest alone. That’s money you can’t put to work to meet other financial goals.

Reasons for not paying off your mortgage sooner

- Building an emergency fund. Paying extra on your mortgage isn’t wise if you don’t have an emergency fund set aside for when life dishes out the unexpected. Having at least three to six months’ worth of living expenses in an immediately accessible account will help you meet your needs in an emergency and make it possible to avoid taking on new debt when big expenses pop up.

- Losing a major tax incentive. One perk the IRS offers to those paying down a mortgage is the mortgage interest deduction, which allows you to deduct interest payments from your taxable income each year. If you’re not making mortgage payments, there won’t be interest to deduct, so it’s worth considering how your taxes will be impacted if you itemize your tax deductions.

- Falling short on retirement savings. If there’s room in your budget to boost your retirement savings, prioritize that first. This is especially important if your employer offers a matching contribution — that’s essentially free money that shouldn’t be left on the table.

Pros and cons of paying off a mortgage early

| Pros | Cons |

|---|---|

You'll build equity faster You'll pay less in interest over time You can reduce your long-term foreclosure risk You can free up more income for other goals | You'll take money away from other goals You could strain your monthly budget Your credit score can be negatively impacted by a closed account You'll lose the ability to deduct interest payments at tax time |

Should you invest instead of paying off your mortgage early?

If you’re trying to decide whether to budget extra money to pay off your mortgage early or invest the money instead, you really can — and should — run the numbers.

Generally, it’s going to make sense to attack your high-interest debt before investing. But, especially compared to credit card or personal loan debt, mortgages often aren’t high-interest. So while it may seem counterintuitive, in many cases you’re better off sticking with the scheduled mortgage payments and using your extra funds to invest. Use a home loan calculator to determine how much you’ll save in interest by paying off the mortgage early. Then, see how those savings stack up against the return you’re likely to make from investing.

For example, say you have a 30-year mortgage for $250,000 at a 6.5% interest rate. If you continued to pay your mortgage as scheduled, you would pay $318,861 in interest over the 30 years. If you put an additional $300 towards the mortgage each month, though, you would save $125,514 in interest and pay off the mortgage 10 years and four months earlier. Sounds hard to beat, right? But if you were to put $300 a month into an index fund for 30 years, you could expect to make more than $450,000.

Choosing your next steps

If you’ve decided that paying off your mortgage is the best option for you, your next step is to make sure there are no prepayment penalties included in your loan terms. You can find this information on Page 1 of your closing disclosure. Additionally, confirm that your lender is applying all extra payments toward your principal balance, not interest. You may have to make a request in writing or follow a special process when sending in extra principal payments. You’re getting rid of a huge monthly bill and building a substantial amount of home equity when paying off your mortgage early.

If, on the other hand, you decide to stick with your scheduled mortgage payments, make a concrete plan for how you’ll use the extra money that won’t be going toward the mortgage. It may be tempting to treat it like spending money, but bulking up retirement accounts, an emergency fund or long-term investments will likely better serve your financial goals.