When Is My First Mortgage Payment Due?

As a new homeowner, your first mortgage payment will typically come due on the first day of the second month after you closed on your home loan. If that sounds confusing, don’t worry — it’s fairly simple to calculate.

We’ll take you step by step through everything you need to know about when your first mortgage payment is due.

On this page

When is your first mortgage payment due after closing?

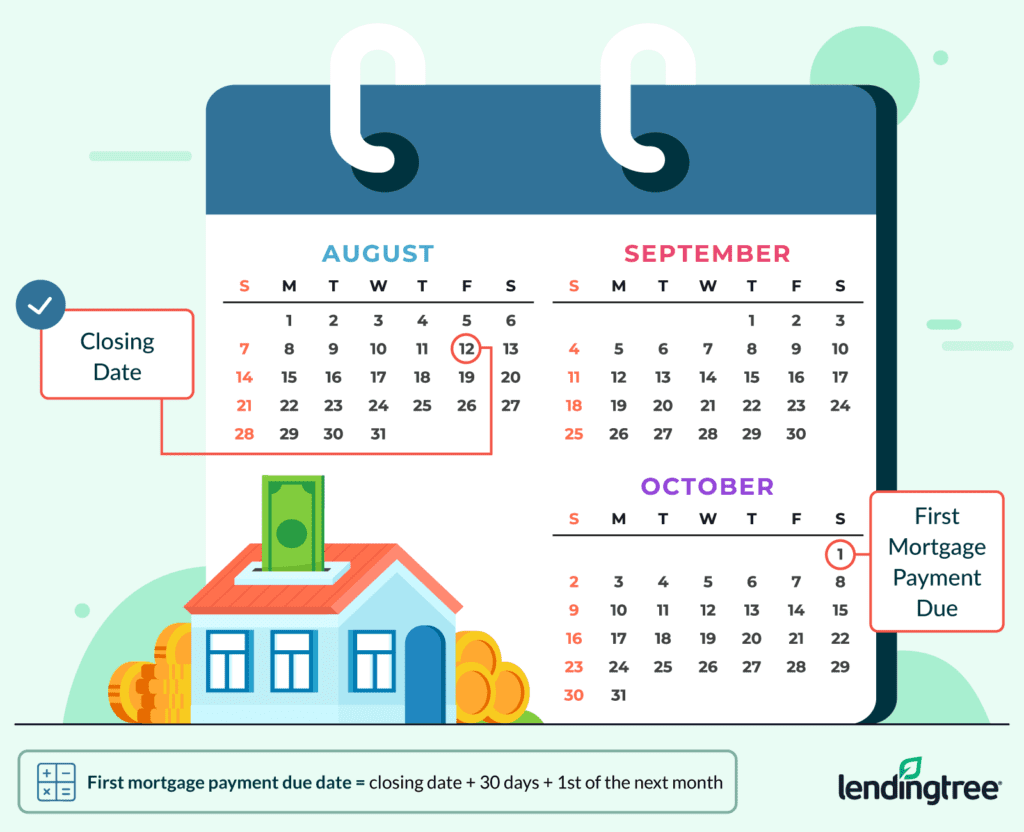

Your first mortgage payment is traditionally due on the first day of the second month after the mortgage loan closed. To calculate this date, simply add 30 days to your closing date and, from there, jump ahead to the first day of the next calendar month. For example, if you closed on your house on Aug. 12, you can expect your first mortgage payment to be due on Oct. 1.

Just make sure to check your closing documents, as this tradition isn’t set in stone — it’s just a guideline. The only way to know for sure what day your first payment is due is to look at your closing documents. Your first payment due date will be listed in your promissory note, along with other details like the time, place and amounts of your payments.

What is due before closing?

Since interest starts accruing the day you close, you’ll prepay some amount of prorated interest as part of your closing costs. Precisely how many days of interest that accounts for is determined by how many days you needed to “jump ahead” to reach the first day of the next calendar month. If you closed on Aug. 12, the interest for Aug. 12 through Aug. 31 will be prorated and prepaid as a part of your closing costs.

Your closing disclosure will list how much prepaid interest is included in your closing costs. Look for the section on Page 2 titled “Prepaids” under the heading “Other Costs.”

In our example, you would owe 19 days worth of interest to cover the time from Aug. 12 to 31.

Will my first payment be higher than usual?

Your first payment shouldn’t be significantly different from your future payments, since mortgages are amortized — meaning the total you need to pay is divided into equal payments over your loan term. However, amortization only applies to the principal and interest owed on your loan. Other parts of your monthly payments, like homeowners insurance and property taxes, can fluctuate from year to year.

Adjustable-rate mortgages (ARMs) are a notable exception to the general rule that your mortgage payments will remain the same over the life of your loan. If you have an ARM, once your loan’s initial fixed-rate period ends, your interest rate has the potential to rise or fall and change your monthly payment amount in response.

To be on the safe side, though, if you have an ARM you should expect for your payments to rise rather than fall. In fact, due to the complexities of the rules that govern ARMs, the deck is stacked against your payments dropping. When interest rates do fall, your payments may not actually drop by much — and even when interest rates aren’t on the rise, your payments could still increase.

What if my first mortgage payment is late?

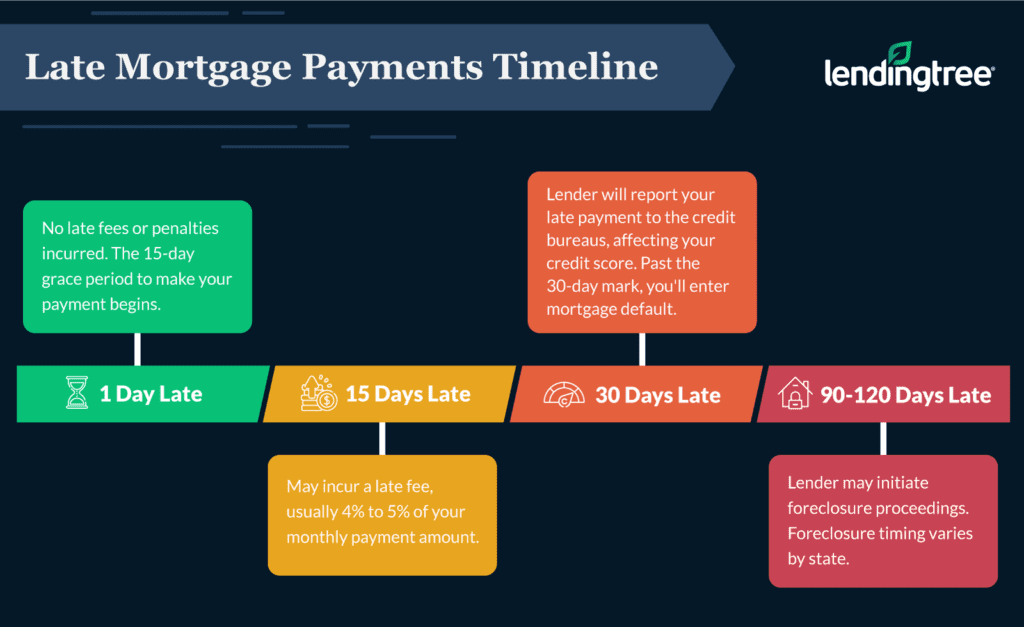

Most lenders offer a grace period on late mortgage payments — meaning that if you miss your due date, you won’t be penalized as long as you’re able to make that payment within a set period of time (usually 15 days). After the grace period ends, your mortgage payment is considered “late.”

If you aren’t sure whether your loan has a grace period, check your promissory note. It’ll list your grace period and any late fees you’ll owe if you don’t make the payment within that grace period. These fees aren’t cheap, and will typically run you around 4% to 5% of the total overdue balance.

If 30 days go by and you still haven’t made your payment, your loan will be considered delinquent and the missed payment will be reported to the credit bureaus. Your credit score will suffer, and that missed payment will remain on your credit report for up to three years.

Past the 30-day mark, you’ll enter mortgage default and, if three to six months pass, your lender will likely initiate the foreclosure process.

The takeaway here is to make on-time payments if you can — and, if you find that you can’t, reach out to your lender. Even if your payment is still outstanding long after the grace period has ended, your lender will likely work with you to find a solution. They may agree to waive late fees, not report the late payment to the credit bureaus or help you get on a repayment plan that works with your cash flow. And if the reason you’re struggling to make payments is a hardship that’s out of your control, such as being unexpectedly laid off, you may qualify to enter a mortgage forbearance or loan modification program.

What’s included in my first mortgage payment?

You probably already know that mortgage payments are made up of principal and interest. However, there are two additional things you need to understand about mortgages that will clarify why your first payment is scheduled the way it is and what it includes:

- You pay interest in arrears, meaning after it has accrued. The portion of your mortgage payment that goes toward interest is paying for the interest accrued during the previous month.

- You pay principal in advance. The portion of your monthly mortgage payment that goes toward the principal balance is paying for what you owe for the month ahead.

Therefore, your first mortgage payment will include interest owed 30 days “backwards” and principal owed 30 days “forwards.”

So, following our earlier example, an Aug. 12 closing date means your first payment is due Oct. 1. That first payment would include interest owed for Sept. 1 through Sept. 30, plus the principal payment owed for the month of October.

Interest starts accruing the day you close, and will continue accruing until you pay off the entire loan. The loan balance will slowly shrink as you pay it down, so each month you’ll pay more in principal and less in interest than you did the previous month.

A note on calculating mortgage payments

Our example didn’t include costs you may pay monthly beyond interest and principal. Typically, these costs include:

- Homeowners insurance

- Property taxes

- Mortgage insurance

- Homeowners association fees (if applicable)

If you’d like to calculate how much your subsequent mortgage payments will be including these types of costs, LendingTree’s home loan calculator allows you to enter these costs and will automatically add private mortgage insurance (PMI) if you indicate that you made less than a 20% down payment.

Closing date vs. due date: When is the best time to close on a house?

If you time your closing right, you can exercise a measure of control over how much prepaid interest you’ll pay, as well as how long you’ll have to gather yourself and your finances before making that first mortgage payment. That’s because your loan closing date has a direct relationship to your first mortgage payment’s due date, which in turn determines your prepaid interest cost. If you’re strategic, you can reduce how much cash you need to bring to the closing table or give yourself more time to prepare for that first mortgage payment.

There’s no single best time to close on a house — but if you know your priorities you can choose to close on a date that initiates a timeline that works well for you:

→ If you close at the beginning of the month, you’ll pay more in prepaid interest, but also have a relaxed timeline that gives you around 60 days between your closing and first payment due date.

→ If you close in the middle of the month, you’ll have around 45 days between closing and your first mortgage payment. You’ll have a still fairly relaxed timeline, however, as well as paying slightly less in interest.

→ If you close near the end of the month, you’ll have a more rapid timeline that gives you only around 30 days of reprieve between closing and making your first payment — but you’ll pay less in interest.