Personal Loans With No Credit Check in 2026

Fast funding options that skip a hard credit check

- No-credit-check loans skip hard credit pulls and rely on income or banking history instead.

- They can be expensive, with high fees or annual percentage rates (APRs).

- Paycheck advance and buy now, pay later (BNPL) apps are usually the cheapest option, but keeping up on payments can be hard due to weeks-long repayment terms.

What is a no-credit-check loan?

A no-credit-check loan is a loan that doesn’t require a hard credit check. Instead, the lender or company may do a soft credit pull and/or review your employment, income and banking history. Funding is usually fast, but rates and fees can be expensive. No-credit-check loans are designed for people with little credit, no credit or bad credit.

In this article, we’re examining three types of loans that typically don’t require a hard credit check:

A no-credit-check personal loan comes as a lump sum of cash and may fit if you need to borrow and need more than two weeks to repay.

A paycheck advance app lets you borrow from your next paycheck and may fit if you need a smaller loan and can pay it back in full when you get paid.

A BNPL app helps you split retail purchases into smaller payments and may fit if you need credit instead of cash.

We focused on products that typically avoid hard credit checks and compared them based on cost, speed, repayment structure and borrower risk. When possible, we favored options with lower fees, clearer qualification rules, payment flexibility and credit reporting features.

What to know before getting a no-credit-check loan

If you don’t have the credit for a personal loan, you’re not alone. Many people find themselves in a similar spot. These no-credit-check loans can help when you’re out of options, but it’s still important to understand how they work.

If you’re considering borrowing from a lender that skips a credit check, you should know that:

- Approval isn’t guaranteed. No-credit-check lenders still have eligibility requirements — they just don’t involve your credit score. The lender could deny you if you don’t have a positive bank account history, for instance.

- Rates and terms can be hard to manage. No-credit-check loans can come with very high APRs and fees. On a small loan, that might not add much to your total cost. But fast repayment schedules can still strain your budget and raise the risk of repeat borrowing.

- You might have more than one payment a month. Paycheck advance apps, BNPL and some high-interest installment loans require you to pay every two weeks or on your payday.

- Automatic payments are usually required. This can lead to overdraft fees, especially if you’re juggling multiple loans or apps.

- You might not qualify if you’re in the military. The Military Lending Act prohibits lenders from offering loans with an APR higher than 36% to active-duty military, their spouses and select family members.

Depending on why you need the money, you might be able to find financial relief without having to take out a loan.

- If you need cash to catch up on everyday bills, see if your provider (e.g. utility company, phone or internet service provider, etc.) has a financial hardship program.

- If you’re struggling with medical debt, contact the billing department and ask for a payment plan.

- If you’re a credit union member, find out if they have a small loan program.

Personal loans with no credit check

Personal loans with no credit check are expensive and small-dollar. They’re also known as high-interest installment loans. You get the money as a lump sum and pay it back monthly or on paydays, depending on the lender.

Impact on credit score: If the lender reports to the credit bureaus, it can help or hurt your credit score depending on whether you make on-time payments. If the lender doesn’t report payments, then it typically won’t have any impact on your credit.

| Lender | Why we like it | APR range | Loan terms | Loan amounts | |

|---|---|---|---|---|---|

| Bigger loans and longer terms | 160.00% – 195.00% | 9 – 18 months | $500 – $5,000 | |

| Small loans within minutes | Charges fees that vary by state | Up to 2 months | Typically up to $500, but varies by state |

Best for: Bigger loans and longer terms – OppLoans

APR range: 160.00% – 195.00%

Loan terms: 9 – 18 months

Loan amounts: $500 – $5,000

Speed of funding: As soon as the same business day

Pros

- Long 18-month loan term can make bigger loan payments easier to manage

- Can borrow up to $5,000

- Reports to all three credit bureaus

- Automatic payments aren’t required

Cons

- Rates are very high

- Longer loan term means more total interest

- Not available in all states

- Approval decision can take two to five days for some

When a lender offers a personal loan without a credit check, the terms typically aren’t in your favor. Loan amounts are small, and you usually only have a few weeks to a few months to pay back what you borrowed.

You could borrow up to $5,000 with the lending platform OppLoans, and you might get 9 to 18 months to pay it off. The longer your loan term, the lower your monthly payment, as you’ll have more time to spread your balance across.

A longer term can be easier on your monthly budget, but you’ll pay more in total interest. And considering OppLoans’ triple-digit rates, you could be looking at a hefty sum if it takes you a long time to pay.

You must meet the following eligibility requirements to get a no-credit-check loan from OppLoans:

- Be at least 18 years old

- Earn a minimum of $18,000 annually

- Have a checking or savings account

- Receive a regular source of income through direct deposit (Social Security and disability income counts)

- Live in an eligible state

Best for: Small loans within minutes – Possible Finance

APR range: Charges fees that vary by state

Loan terms: Up to 2 months

Loan amounts: Typically up to $500, but varies by state

Speed of funding: Within minutes when sent to a debit card

Pros

- Could get your money instantly

- Can push your payment due date out by 29 days for free

- Additional financial relief plan in case of unexpected hardship

- Reports to two of the three credit bureaus (TransUnion and Experian)

Cons

- Fees can be expensive

- Not available in all states

- Payments are based on your payday and require autopay

With Possible Finance, you could get your funds within minutes if you have them sent to your debit card.

Possible Finance works a little like a payday loan. Payments are automatically deducted from your linked bank account or debit card, and your due dates are based on when you get paid.

But unlike a payday loan, you can extend your payments up to 29 days. This can help you avoid overdraft fees or having to roll your loan into a new one.

Possible Finance charges fees that vary by state, and fees can be steep. In Delaware, for instance, Possible Finance charges $25 for each $100 you borrow. If you get a $500 loan, you’ll pay $125 in fees.

To get a personal loan with no credit check from Possible Finance, you’ll need to be at least 18 years old and have the following:

- U.S. phone number and internet access

- Social Security number and valid government-issued ID

- Checking account that’s compatible with Plaid, with at least three months of transaction history, recent income deposits and a positive balance

- Residence in an eligible state

Paycheck advance apps

A paycheck advance app lets you borrow money between paydays. Loans are usually smaller than personal loans and instead of interest, these apps charge fees. You will pay back all that you borrowed on your next payday.

Impact on credit score: Usually none, as paycheck apps don’t typically report payments to credit bureaus.

| App | Why we like it | Amounts available | Timeline for a free advance | Fee for expedited advance | Requires direct deposit to app account | |

|---|---|---|---|---|---|---|

| Fast free advances for established users | $20 – $500 | 24 hours or less | $2-$5 | Yes | ||

| Doesn’t require you to change your direct deposit | Up to $150 a day and $1,000 per pay period | 1-3 business days | $3.99 to $5.99, plus $1.99 on all transfers regardless of speed | No |

Best for: Fast free advances for established users – Chime

Amounts available: $20 – $500

Timeline for a free advance: 24 hours or less

Fee for expedited advance: $2-$5

Requires direct deposit to app account: Yes

Pros

- Can get a free advance within 24 hours, much faster than most apps

- Although switching your direct deposit to Chime is required, Chime accounts come with benefits you might not have at your current bank

- Comes with a free credit-building Chime Card along with a standard debit card

Cons

- Must get paycheck directly deposited into a Chime account to qualify

- Most new users only qualify for $50 to $100, though that amount can increase over time

- Have to wait one to two direct deposits before you’re eligible

- Not available in all states

To be eligible for MyPay, Chime’s paycheck advance feature, you’re required to switch your direct deposit from your current bank to Chime.

Although this might be a hard stop for some, Chime accounts are fee-free, have no minimum balance requirements and come with free overdraft protection up to $200. You can even build credit with a complimentary secured credit card (called the Chime Card).

You won’t be able to borrow right away. MyPay is only available after you’ve gotten one or two direct deposits into your Chime account. Once you’ve unlocked MyPay, you can borrow up to $500 from your paycheck, although loans start small (usually $50 to $100).

To qualify for Chime MyPay, you must set up an eligible direct deposit into a Chime account. To open a Chime account, you must:

- Be at least 18 years old

- Be a U.S. citizen or permanent resident

- Have a Social Security number

- Live in an eligible state

Best for: Not requiring you to change your direct deposit – EarnIn

Amounts available: Up to $150 a day and $1,000 per pay period

Timeline for a free advance: 1-3 business days

Fee for expedited advance: $3.99-$5.99, plus $1.99 on all transfers regardless of speed

Requires direct deposit to app account: No

Pros

- Don’t need to get your paychecks sent to an EarnIn account

- Large loan amounts

- Offers a free “Tip Yourself” benefit that can help you grow your savings

Cons

- All advances have a fee

- GPS tracking required if you don’t have a work email address

- Must get a regular paycheck and make at least $320 per pay period

EarnIn could be a good choice if you need to borrow from your paycheck, but you don’t want to change the bank you use for direct deposit.

EarnIn is an earned wage access (EWA) company, which means you’re borrowing from your paycheck as you earn it. To do that, EarnIn has to verify your employment. If you have a work email, that’s all you’ll need. If you don’t, you’ll have to enable GPS tracking in the app.

You can borrow up to $150 a day with EarnIn, but you’ll probably need to use the app responsibly for some time before you’re eligible for that much. EarnIn charges a $1.99 fee on every advance, and another $3.99 to $5.99 if you want your money in minutes instead of days.

Only workers who make at least $320 per pay period can use EarnIn. You must also:

- Be a U.S. resident and at least 18 years old

- Have a checking account

- Enable GPS or have an employer-provided email address

- Have a valid cell phone number and email address

- Have a consistent pay schedule

Buy now, pay later (BNPL) apps

You won’t get cash with buy now, pay later. Instead, BNPL helps you break retail purchases into smaller payments. The most popular payment plan requires four payments: one at the time of purchase and then three more payments, due every two weeks.

Impact on credit score: Varies, but most BNPL apps do not report payments to the credit bureaus on Pay in 4 plans (the most popular repayment option).

| App | Why we like it | APR range | Loan terms | Loan amounts | Fees | |

|---|---|---|---|---|---|---|

| No credit checks, even on monthly financing | 0% for Pay in 4 and Pay in 30 days 0%-35.99% for monthly financing | 6 weeks for Pay in 4 30 days for Pay in 30 days 6 to 24 months for monthly financing | No predetermined amount | $7 late payment fee on Pay in 4 Late fee varies for monthly financing | ||

| Can use it to pay some bills | 0% (charges fees instead) | 6 or 12 weeks | No predetermined amount | Origination fee $0 – $124 Late fee up to $7 Possible $2 payment rescheduling fee |

Best for: No credit checks, even on monthly financing – Klarna

APR range: 0% for Pay in 4 and Pay in 30 days; 0%-35.99% for monthly financing

Loan terms: 6 weeks for Pay in 4; 30 days for Pay in 30 days; 6 – 24 months for monthly financing

Loan amounts: No predetermined amount

Fees: $7 late payment fee on Pay in 4; Late fee varies for monthly financing

Pros

- No hard credit checks, ever

- Many 0% interest options

- Can be used at retailers that accept Visa

Cons

- Can’t use to pay utilities, rent or medical care

- Won’t know if you’re approved until checkout, which can be hard for planning

Some buy now, pay later apps run a hard credit hit if you want to pay by anything other than Pay in 4. Klarna only runs a soft credit check, no matter the payment plan you choose.

You can use Klarna at retailers that accept Visa, but you can’t use it to pay utility bills, rent or medical bills. Klarna makes more sense than an emergency loan if you need help breaking up a retail purchase.

To use Klarna, you must:

- Be at least 18 years old

- Be a resident of the U.S. or a U.S. territory

- Have a valid bank card or bank account

- Have a positive payment history

- Be able to receive texts

- Have a valid Social Security number (for the use of certain products)

Best for: Using BNPL to pay bills – Zip

APR range: 0% (charges fees instead)

Loan terms: 6 or 12 weeks

Loan amounts: No predetermined amount

Fees: Origination fee $0 - $124 ; Late fee up to $7; Possible $2 payment rescheduling fee

Pros

- Can use to pay some bills, which is unique for BNPL

- One free monthly payment due date extension per order

- Can use at most retailers that accept Visa

Cons

- Potential for expensive origination fee

- Won’t know if you’re approved until checkout, which can be hard for planning

- Fewer pay plans than some BNPL apps

Typically, you can use BNPL to pay only for items and, in some cases, services. With Zip, you can use BNPL to pay your bills for car insurance, electricity, cell phone, internet and more (depending on your provider). You can also push out your payment due date once per month, per order. This can help you avoid late fees and overdrafts.

Using Zip can be pricey. Both six-week and 12-week plans come with an origination fee, which varies from $0 - $124.

To use Zip, you must:

- Be at least 18 years old

- Live in the U.S. and have a valid U.S. residential address

- Have a U.S. credit or debit card that’s not from Capital One or Chase

- Have a valid cell phone number

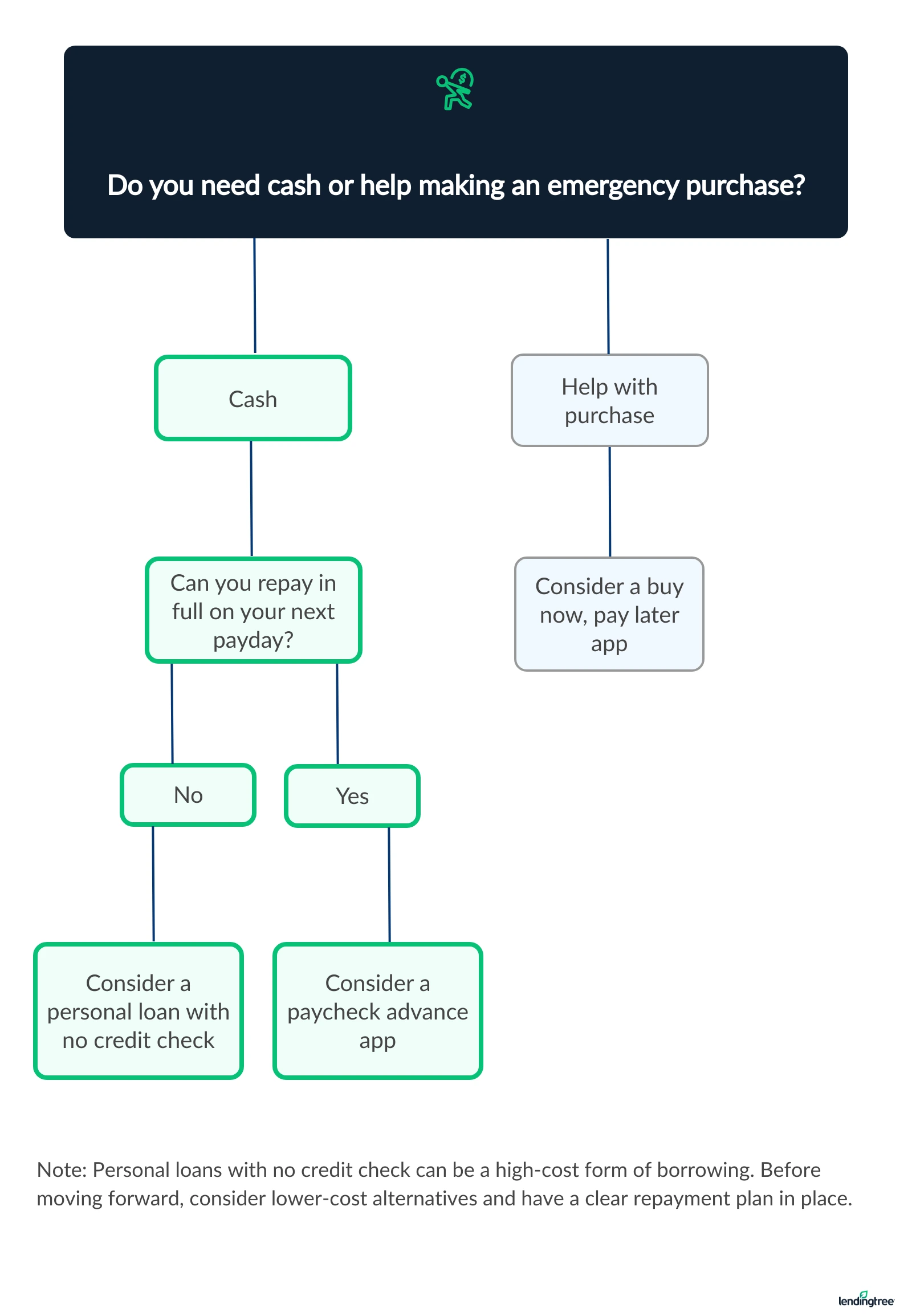

Which no-credit-check loan option makes sense?

It can be stressful figuring out what to do when you need money but don’t qualify for a standard personal loan. But between no-credit-check personal loans, paycheck advance apps and BNPL, you may still have options. The flowchart below will help get you started on choosing the best path for you.

Comparing costs between no-credit-check loans

To see how costs compare between no-credit-check personal loans, paycheck advance apps and BNPL, consider the following scenario.

Imagine that you wake up one morning to a flat tire. You need to get it fixed fast. Otherwise, you won’t make it to work. A replacement will cost you $150. Here’s how much each type of loan would cost you in the end.

| Option | Estimated payment | Down payment amount | Time to repay | Estimated total repayment |

|---|---|---|---|---|

| No-credit-check personal loan | $64 per month (160% APR) | $0 | 3 months | $192 |

| Paycheck advance app | $150 on next payday | $0 | 2 weeks | $150 |

| BNPL app | $38 every two weeks | $38 | 6 weeks | $150 |

Takeaways:

- The no-credit-check personal loan costs the most overall, but it gives you the most time to repay.

- Using a paycheck advance app or BNPL is free if you pay on time, but repayment terms are much shorter.

- BNPL requires a down payment, but personal loans and paycheck advance apps don’t.

Tips to get approved for a standard personal loan

Even if you have rocky credit, you might still qualify for a “standard” personal loan, or one that requires a credit check. Getting approved can be easier if you:

Apply with lenders that specialize in bad credit

Many personal loan lenders specialize in bad credit, and while they might require a hard credit check, some don’t have a formal score requirement to meet.

Offer collateral

Secured loans, or loans that require collateral, are typically easier to get approved for. Online lenders tend to use your car as collateral. Banks and credit unions usually use your savings or investment account.

Add a co-borrower

Getting a joint loan with a co-borrower can also help you qualify. A co-borrower is someone who is willing to take equal responsibility for the loan. They should have good to excellent credit. But late payments impact their credit as much as it will yours, so stay true to your word.

Use a loan marketplace

Every lender has its own way of calculating rates and eligibility. You could get denied by one company but approved by another. Using a loan marketplace like LendingTree lets you shop multiple lenders at once, increasing your chances of qualifying.

Want more details on how online loan marketplaces work?

Learn how to compare personal loan offers on LendingTree and what can affect rates and approval odds.

When banks compete, you win

You won’t find paycheck advance apps or BNPL with LendingTree, but we can help you find and compare personal loans, including ones that don’t require a credit check. Our network of expertly vetted lenders accepts good credit, bad credit and everything in between.

Tell us what you need

Take two minutes to tell us who you are and how much money you need. It’s free, simple and secure.

Shop your offers

LendingTree users with bad credit get four personal loan offers on average. Compare your offers side by side to get the best deal.

Get your money

Pick a lender and sign your loan paperwork. You could see money in your account in as soon as 24 hours.

No-credit-check loans to avoid

The no-credit-check loans showcased in this article aren’t the only ones out there, but they are among the safer options. The options below are riskier — avoid them if you can.

- A car title loan is a short-term loan that uses your car as collateral. If you don’t pay back your loan, the lender will repossess your car. Some secured personal loans also use your car as collateral, but car title loans come with shorter terms, higher rates and smaller loan amounts.

- With a pawn shop loan, you’ll offer a valuable piece of property to a pawnbroker. The pawnbroker then gives you a loan that’s much lower than what your item is worth. If you don’t pay back what you owe, the pawnbroker can sell your item.

- Payday loans come with high APRs, and you have to pay the loan in full by payday. If you can’t pay, you might have to take out another one to pay for the first. This can launch a cycle of debt. Some high-interest installment loans follow a similar model — always know how your loan works before accepting.

Final thoughts: Escaping the cycle of debt

As long as you understand the cost of borrowing and have a solid payoff plan, a no-credit-check loan can help if you’re in a true financial emergency.

But if you find yourself relying on expensive loans and apps to get by — or to cover debt you already have — you might be trapped in a debt cycle.

About four out of 10 people say they’ve been late on a BNPL payment, according to LendingTree’s buy now, pay later tracker. And remember, a $150 advance taken today may mean being $150 short on rent, groceries or gas next payday.

Here are some possible ways out if you’re feeling stuck.

Debt consolidation

If you’re having trouble juggling multiple credit card and personal loan payments, you might be a good candidate for a debt consolidation loan. Consolidating won’t change what you owe, but you’ll only have one bill to pay and you might qualify for a better interest rate.

Debt management plan

You may also find debt relief through a debt management plan (DMP). With this, you’ll work with a certified credit counselor to come up with a plan to get out of debt in three to five years, usually at a low cost. Most credit counseling agencies are nonprofit.

Bankruptcy

Bankruptcy is a valid option if you have more debt than you possibly can afford. Although there’s an unfair stigma surrounding bankruptcy, it can give you a fresh start if you really need it. Still, this is one of the most extreme acts you can take when it comes to personal finance. Bankruptcy will follow you for seven to 10 years.

What sets LendingTree content apart

Expert

Our personal loan writers and editors have 52 years of combined editorial experience and 42 years of combined personal finance experience.

Verified

100% of our content is reviewed by certified personal finance professionals and meets compliance and legal standards.

Trustworthy

We put your interests first. We’ll tell you about any loan drawbacks and be clear about when to consider alternatives.

Frequently asked questions

Yes, it’s possible to get a personal loan without a hard credit check. Instead, these lenders use a soft credit check (which won’t impact your credit score) and other information, like your bank account activity, to determine your eligibility.

OppLoans and Possible Finance offer personal loans with no hard credit pull, so they may be a good place to start. If you want to avoid a hard credit check, also consider paycheck advance apps or BNPL services.

Most personal loan lenders, however, will require a hard credit check when you apply. To minimize hard inquiries, you can use LendingTree to compare rates with a soft credit check first and then decide whether to move forward with a full application.

The safest types of no-credit-check loans are ones that you can use interest-free or for a low fee.

Most buy now, pay later apps let you split retail purchases into four interest-free payments. Paycheck advance apps also don’t typically charge interest. You could even get your money without a fee if you’re willing to wait a day or two.

The danger with these BNPL and paycheck advance apps isn’t necessarily their cost, it’s how easy they are to use. Without discipline, you could end up impulse buying or shorting your paycheck every week.

Most no-credit-check loans will not help you build credit. Usually, lenders that approve loans with just a soft credit hit do not report payments to the credit bureaus. There are some exceptions, though, including OppLoans and Possible Finance (although Possible Finance only reports to TransUnion and Experian).