How to Calculate Your Car Insurance Needs and Rate

Advertising Disclosures

Loading Disclosures…

If you want to calculate how much to pay for car insurance, you’ll first need to figure out how much car insurance you need. After that, you can look at average rates in your area and start collecting quotes.

How to calculate your car insurance needs

Start by calculating how much car insurance you need.

-

Liability insurance

is required by law in almost every state. The minimum requirements aren’t always enough.Liability insurance covers injuries and property damage you cause to others.

-

Full coverage — meaning both collision

and comprehensiveCollision covers damage to your car from a collision with another vehicle or object.coverage — is usually required for a car loan or lease, and can also be worth having even if you own the car outright.Comprehensive covers your car for theft and damage from non-collision causes, like fire, flood and vandalism.

-

Uninsured motorist

(UM) coverage and/or personal injury protectionUninsured motorist covers you and your passengers for injuries caused by a driver with no insurance. It’s required in about 20 states and optional everywhere else.(PIP) are legally required in some states. They can come in handy in states where they are optional.PIP covers injuries to you and your passengers, whether you or another driver causes the accident. It also covers lost wages and certain other expenses.

Out of all of these, liability and collision coverage usually add the most to your insurance rates.

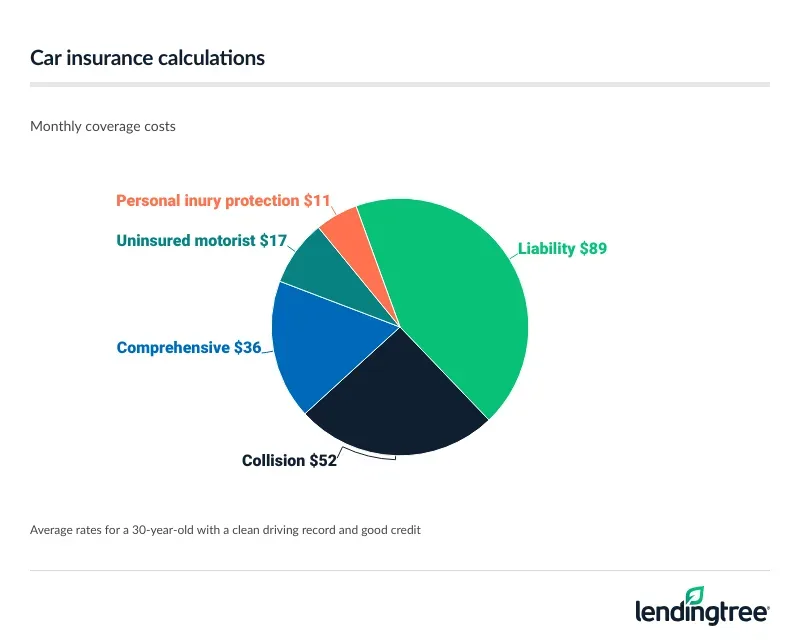

Car insurance average coverage costs

| Coverage | Monthly cost |

|---|---|

| Liability | $89 |

| Collision | $52 |

| Comprehensive | $36 |

| Uninsured motorist bodily injury | $17 |

| Personal injury protection | $11 |

Coverage costs vary and are based on factors like your location, driving record and vehicle. This makes it wise to compare car insurance quotes from a few companies to find the cheapest rate for you.

You can find the details in LendingTree’s guide to how much insurance you need, but here’s a rundown of how to calculate your car insurance requirements for each type of coverage.

How much liability car insurance do you need?

Beyond the basic minimum required by the state, you may want more liability coverage to protect your money and property in case you’re at fault in a major accident. Since you’re responsible for part of the damages above your liability limits, your savings or even your home could be at risk.

Add up the value of your savings and investment accounts, as well as any properties you own, and consider getting a policy with liability limits close to that total amount.

How much full coverage car insurance do you need?

Choosing high collision and comprehensive deductibles can help you save on full coverage.

Since your deductibles come out of your own pocket, you don’t want them to be too high. But for a typical driver with a clean record, just raising those deductibles from $500 to $1,000 would reduce your car insurance rate by about 10% or $216 a year.

Say your car lists for $3,500 in its current condition. If you have a $1,000 deductible, insurance won’t give you more than $2,500 for it. This is about the same as a few years of collision and comprehensive coverage.

How much do you need for other car insurance coverage?

You may be required to get uninsured motorist (UM), personal injury protection (PIP) and/or medical payments

- UM coverage costs an average of $17 a month for bodily injuries (UMBI). In most states, you can also get coverage for property damage (UMPD), including your vehicle, for about $5 more.

- PIP is required by law in about a dozen no-fault insurance states, and it’s optional in many others. It costs an average of $11 a month.

- MedPay adds an average of $7 a month to a typical car insurance bill. It’s usually optional in states that don’t have PIP. In some states, you can choose between MedPay and PIP.

Health insurance also covers car accident injuries, but most health plans make you pay a deductible and coinsurance. UM, PIP and/or MedPay protect you from out-of-pocket costs like these.

How to estimate your car insurance costs

Car insurance quotes are free rate estimates from insurance companies. You don’t have to buy insurance from an agent who gives you one.

Each company uses a different formula to calculate your car insurance rate. Some may give you a bigger discount for being a good driver. Others may have a smaller increase after a ticket or accident.

Comparing quotes from different companies helps you find the cheapest rate for your situation.

How much should I pay for car insurance?

A typical adult driver pays an average of $177 a month for full coverage, before discounts. Minimum coverage policies cost an average of $68 a month.

However, prices vary by location. For example, full coverage costs an average of $280 a month in Nevada, but just $101 a month in Vermont.

Estimated car insurance costs by state

| State | Monthly full coverage | Monthly liability |

|---|---|---|

| Alabama | $153 | $59 |

| Alaska | $135 | $48 |

| Arizona | $201 | $82 |

| Arkansas | $197 | $59 |

| California | $182 | $69 |

| Colorado | $238 | $78 |

| Connecticut | $265 | $128 |

| Delaware | $256 | $116 |

| Florida | $264 | $87 |

| Georgia | $155 | $68 |

| Hawaii | $126 | $46 |

| Idaho | $127 | $45 |

| Illinois | $154 | $61 |

| Indiana | $144 | $53 |

| Iowa | $149 | $36 |

| Kansas | $199 | $64 |

| Kentucky | $176 | $84 |

| Louisiana | $277 | $94 |

| Maine | $107 | $43 |

| Maryland | $172 | $84 |

| Massachusetts | $152 | $70 |

| Michigan | $218 | $78 |

| Minnesota | $194 | $68 |

| Mississippi | $176 | $59 |

| Missouri | $198 | $70 |

| Montana | $183 | $46 |

| Nebraska | $171 | $48 |

| Nevada | $280 | $147 |

| New Hampshire | $113 | $50 |

| New Jersey | $209 | $119 |

| New Mexico | $188 | $66 |

| New York | $192 | $92 |

| North Carolina | $124 | $60 |

| North Dakota | $158 | $43 |

| Ohio | $124 | $48 |

| Oklahoma | $193 | $55 |

| Oregon | $172 | $86 |

| Pennsylvania | $166 | $56 |

| Rhode Island | $224 | $94 |

| South Carolina | $152 | $66 |

| South Dakota | $177 | $31 |

| Tennessee | $150 | $53 |

| Texas | $199 | $79 |

| Utah | $193 | $90 |

| Vermont | $101 | $35 |

| Virginia | $132 | $67 |

| Washington | $188 | $71 |

| Washington, D.C. | $218 | $95 |

| West Virginia | $150 | $56 |

| Wisconsin | $146 | $41 |

| Wyoming | $111 | $27 |

Other factors to calculate for car insurance

Insurance companies analyze dozens of factors about you to calculate your rate, including your driving record, age, vehicle and in most states, your credit.

Driving record

In the eyes of an insurance company, a recent violation or at-fault accident makes you a risky driver. Higher risk almost always means a higher rate, but it depends on the nature of your incident.

For example, a speeding ticket raises the average price of full coverage by 24%, while a DUI (driving under the influence) conviction raises rates by 86%.

Car insurance estimates by driving record (full coverage)

| Driving record | Monthly cost | % increase |

|---|---|---|

| Clean | $177 | Not applicable |

| Ticket | $219 | 24% |

| Accident | $263 | 49% |

| DUI | $329 | 86% |

It’s good to shop around after you see how much your rate goes up after a driving incident. A different company may have cheaper insurance for a bad driving record.

Age

You usually pay the most for car insurance in your teens and early 20s. This is when you have the least driving experience and the greatest risk of a crash.

If you avoid tickets and accidents, your rates usually start getting affordable after you turn 25. Most people see their rates continue to go down through their mid-60s.

Unfortunately, your rates may increase in your retirement years. This is mainly because senior citizens have higher accident rates than middle-aged drivers.

Vehicle type

The type of car you drive affects how much your insurance company may have to pay out in a claim. High repair and replacement costs usually make luxury cars expensive to insure.

You usually also pay more to insure cars with higher crash rates.

If you’re shopping for a car, consider getting sample quotes for the vehicles you want to buy. This can help you narrow your choices to models with affordable insurance.

Credit record

In most states, your credit also has a big influence on your car insurance rates. Drivers with excellent credit pay 19% less for full coverage, on average, than drivers with good credit. And getting car insurance with bad credit can be very expensive.

Estimated insurance rates by credit tier

| Credit tier | Monthly liability | Monthly full coverage |

|---|---|---|

| Excellent | $62 | $143 |

| Good | $68 | $177 |

| Average | $84 | $195 |

| Fair | $92 | $214 |

| Poor | $137 | $345 |

Insurance companies usually check your credit for things like your payment history and borrowing amounts.

However, a few states

What you need for a car insurance estimate

You usually have to share information about yourself and vehicle for your car insurance estimate. This usually includes:

- Personal information: Your name and birth date may be enough, but insurance companies might also need your driver’s license number.

- Vehicle identification number (VIN): Insurance companies use your VIN to find details about your car.

- Driving record: Being honest about recent tickets and accidents helps you get accurate insurance estimates. Insurance companies usually find out about them later, anyway, when they check your driving record.

You can contact insurance companies for quotes or use a comparison site like LendingTree.

Frequently asked questions

Car insurance companies review your driving record, location and other factors to calculate your rate. Your age, vehicle and even your credit can also affect your price. Each company calculates rates a little differently, making it important to shop around.

Most car insurance companies can estimate your rate in less than 15 minutes. You‘ll provide some information about yourself and your car to get a quote, which you can usually request online.

Methodology

How we obtained car insurance rates

LendingTree uses insurance rate data from Quadrant Information Services using publicly sourced insurance company filings. Rates are based on an analysis of hundreds of thousands of car insurance quotes for a typical driver. Prices are shown for comparative purposes only. Your own rates may be different.

Unless noted otherwise, quotes are for a full-coverage policy for a 30-year-old man with good credit and a clean driving record who drives a 2018 Honda CR-V EX.

Coverage limits

Liability policies provide the minimum insurance coverages and limits required in each state.

Full coverage policies include collision, comprehensive and liability coverage:

- Bodily injury liability: $50,000 per person, $100,000 per accident

- Property damage liability: $50,000

- Uninsured / underinsured motorist bodily injury: $50,000 per person and $100,000 per accident

- Personal injury protection: minimum limits, where required by law

- Collision: $500 deductible

- Comprehensive: $500 deductible

Read LendingTree’s full editorial guidelines here.