Best Loans for Bad Credit in July 2026

LendingTree users with credit scores under 580 get an average of four personal loan offers

Advertising Disclosures

Loading Disclosures…

- It’s possible to get a loan with bad credit (FICO Score below 580).

- It typically takes anywhere from the same day to five business days to get your loan money.

- Upstart, OneMain Financial, Avant and Upgrade rank as the best overall personal loan lenders right now based on LendingTree’s objective methodology.

How bad credit loans work

Yes, it’s possible to get a personal loan with bad credit — over 80,000 people with bad credit found a loan through LendingTree just last year. Here’s how it works.

-

What credit score do I need to get a loan?

Some bad credit lenders don’t have a minimum credit requirement, while others want to see a score of at least 500. The higher your score, the more offers you’re likely to get. -

How fast can I get money?

Some lenders offer same- or next-day funding, but getting your money can take up to five business days. Lenders sometimes take longer to consider your application when you have bad credit. -

Will a loan hurt my credit?

Lenders pull your credit when you apply, which can cause a small dip in your credit score (usually around five to 10 points). Scores return to baseline when you make payments on time, and the impact on your credit will be gone within a year.

What do lenders actually look at?

Lenders consider more than your credit score when deciding whether to offer you money. Check the table below to see how different parts of your financial situation could change your odds of getting offers, even with bad credit.

| Factor | Likely improves odds | Likely lowers odds |

|---|---|---|

| Employment | Long, stable job history | Unemployed or short job history |

| Income | High income, regular paychecks | Low income, erratic paychecks |

| Debt (including housing) | Low debt payments compared to income | High debt payments compared to income |

| Credit history | Long history of on-time payments | Short credit history, missed payments, bankruptcy |

| Loan amount | Small loans | Large loans |

Some lenders consider other factors like education in their evaluation process.

Borrowing money safely when you have bad credit

Understanding personal loan rates, loan terms and warning signs for scams can set you up for a safe, affordable loan. Here’s what you need to know.

Spot scams for bad credit loans

Rule of thumb: If a loan seems too good to be true, it probably is. Avoid lenders without an online footprint that reach out to you with promises of low rates or guaranteed approval.

To avoid scams and loans you can’t afford, watch for these signs:

-

Pressure to act.

It’s a red flag when a lender pressures you to make a decision in a short time frame. Reputable lenders give you time to think about your options. -

No physical address.

A legitimate lender will list its physical address on its website. You’ll be able to confirm the location with an online map, such as Google or Apple Maps.

Additional signs of a potential scam:

- Negative lender reviews. Read online personal loan reviews for your potential lender, paying attention to the rating and common customer complaints.

- They contact you. If a lender contacts you but you haven’t applied or done business with them before, don’t respond — it could be a scam. Legitimate lenders won’t cold call and ask for your personal information.

- Guarantees and promises. A reputable lender won’t guarantee approval before checking your credit score and report.

- High APRs and expensive fees. Expensive loans aren’t scams, but they can leave you worse off. Take control by shopping around for lower rates and avoiding offers with APRs of 36% or higher.

Contact law enforcement and file a police report. There may not be much the police can do, but it’s important to document the crime. You should also file a fraud report with the Federal Trade Commission to potentially prevent others from being scammed in the future.

Choose the right loan term

Rule of thumb: Choose the shortest loan term that comes with monthly payments you can afford. This can save you money on interest.

Your loan term (how long you make monthly payments) directly affects how much you pay.

Short loans usually come with higher (more expensive) monthly payments, but cost less money in total interest.

Long loans typically come with lower (cheaper) monthly payments, but cost more money in total interest.

Understand rates

Rule of thumb: Look for loans with APRs below 36% and avoid triple-digit APRs entirely.

Some bad credit loans are much more expensive than others. You’ll pay higher rates with bad credit, but there’s a big difference between average bad credit rates and predatory rates.

See how much you’d pay if you borrowed $5,000 over 48 months:

Cost comparison: Average vs. predatory APRs

| APR | Monthly payment | Total interest | |

|---|---|---|---|

| Average APR for bad credit on LendingTree* | 30.25% | $180.76 | $3,676.37 |

| Predatory (very high) APR | 105% | $445.45 | $16,381.45 |

In this comparison, the predatory APR makes monthly payments cost over twice as much and total interest cost nearly five times more than the loan with the average APR for bad credit. You’d pay three times more than you borrowed in interest alone with the predatory rate.

See how much your loan could cost in dollars

The average APR for LendingTree users with bad credit is 30.25%, assuming typical loan amounts ($5,000-$54,999) and repayment terms (36 to 83 months).

See how much your loan could cost in dollars by plugging 30.25% into the calculator below with the amount you want to borrow and your ideal repayment term.

What to know about bad credit loans

How to improve your chances of getting approved

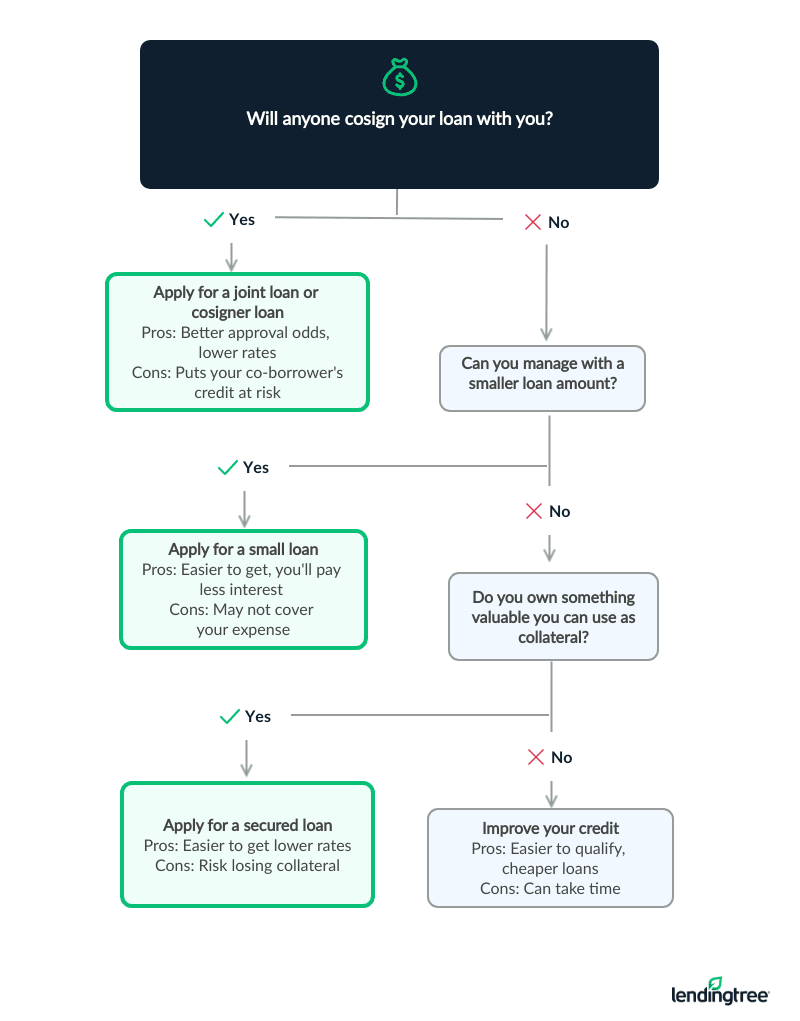

Getting a loan if you have bad credit can be hard, but certainly not impossible. Finding a friend or family member willing to be a cosigner or co-borrower can significantly boost your approval chances, especially if that other person has a longer and better credit history than you.

But you’re more than a credit score, and that isn’t the only thing lenders consider. Your income, employment history and even education level can be green flags, too. Finding stable employment and boosting your income could give you an ‘in’ with some lenders.

Application timeline and checklist

1. Check your rates

You can fill out individual forms on lender websites or use the LendingTree marketplace to compare offers from up to five lenders at once.

- Basic personal info

- Employment and income

- Loan amount and purpose

- Housing payment

2. Compare offers

Compare monthly payments and total loan cost to decide which option is right for you.

3. Formally apply

Submit documents like proof of income, address and identity along with a loan application to the lender you choose.

4. Sign your offer

Read your loan offer carefully and ask questions before accepting.

5. Get your money

Your money can arrive in your bank account from the same day up to around five business days.

Learn more about how to apply for a personal loan and how long it takes to get your money.

How to choose a loan when you have bad credit

| Situation | Strategy | Next steps |

|---|---|---|

| You have several offers from different lenders | Choose the loan with the lowest total interest that has monthly payments you can afford. | Use a personal loan calculator to compare monthly payments and total interest. |

| You have only a couple of offers, and they’re expensive | See if you can manage the payments, and if not, choose an alternative. | See if the monthly payments fit in your budget. If you can’t afford them, use our expert strategies to find other ways to get a lower loan rate. |

| You don’t qualify | Choose a strategy to improve your odds when you apply again. | Evaluate strategies and consider alternatives like family loans and payday alternative loans. |

What happens if you can’t repay

Missing payments on a personal loan can hurt your finances and credit. Here’s what happens:

-

Damage to credit score and report.

Your credit score can drop significantly when you stop making payments. The negative mark will stay on your credit report for seven years. -

Harder to get credit and housing.

Missing loan payments can make bad credit even worse, making it harder to qualify for new loans or even rent an apartment. -

Loan goes to collections.

Lenders typically send your debt to a collections agency after 120 to 180 days. Debt collectors will then contact you to collect payment. -

Can be sued.

Your lender or debt collector can eventually sue you for payment. If they win, they can ask to garnish your wages, freeze your accounts or put a lien on your property.

Estimate your monthly payment and compare it to your budget to see if you can afford a loan. Still not sure if you can afford it? Look into other ways to borrow money. Taking out a loan you can’t afford can lead to an even worse financial situation with chronic debt.

More guides to bad credit personal loans

Find the right type of loan for your situation — whether you need cash fast, want to avoid fees or are consolidating debt.

Compare loan offers from trusted lenders — even with bad credit

You’d shop around for flights. Why not your loan? LendingTree makes it easy. Instead of applying to just one lender and hoping for a good rate, see multiple lenders compete for your business — so you can choose the best offer.

Tell us what you need

Take two minutes to tell us who you are and how much money you need. It’s free, simple and secure.

Shop your offers

LendingTree users with bad credit receive four personal loan offers on average. Compare your offers side by side to get the best deal.

Get your money

Pick a lender and sign your loan paperwork. You could see money in your account in as soon as 24 hours.

Best bad credit loans with the lowest rates

| Lender | User rating | APR | Amount | Min. credit score | See Results |

|---|---|---|---|---|---|

|

|

6.20% to 35.99% |

$1k – $75k |

None | ||

|

|

11.99% to 35.99% |

$1.5k – $30k |

None | ||

|

|

9.95% to 35.99% |

$2k – $35k |

580 | ||

|

|

7.74% to 35.99% (with discounts) |

$1k – $50k |

600 |

Read more about how we made our picks for the best bad credit loans.

Best for: Overall bad credit loans – Upstart

- APR

- 6.20% to 35.99%

- Get money in as soon as one business day

- Considers factors beyond your credit score

- May be able to use your paid-off car as collateral for better odds

- 99% recommendation rating from LendingTree users who borrow from Upstart

- Can’t boost your approval odds with a co-borrower

- Lender could keep some of your loan as an origination fee

Upstart’s application was straightforward but more detailed than those of most lenders we tested. Upstart asked additional questions tied to its AI approval system, including savings balances and vehicle information.

Upstart could be the best fit if you’re looking for a bad credit loan but have a stable income, employment or a strong educational background.

Upstart lets you boost your approval odds with:

- Collateral

- Smaller loans

- Factors like your education and employment history

Upstart has transparent eligibility requirements. You must:

- Age: Be 18 or older

- Administrative: Have a U.S. address, personal banking account, email address and Social Security number

- Income: Have a valid source of income, including a job, job offer or another regular income source

- Credit-related factors: Have no bankruptcies within the last three years, a reasonable number of recent inquiries on your credit report and no current delinquencies

- Credit score: No formal minimum requirement

Best for: Same-day loans for bad credit – OneMain Financial

- APR

- 11.99% to 35.99%

California residents must borrow at least $3,000

- Get your loan in as soon as an hour using your debit card

- Use your car as collateral for a bigger loan or easier approval

- 94% recommendation rating from LendingTree users who borrow from OneMain

- Charges an up-front origination fee on every loan

- Paying off your loan faster might not save you money

OneMain’s application is fast and easy to navigate compared to others we tested, especially if you’re prepared to answer questions about your monthly take-home pay, employer phone number and car payment.

OneMain could be the best fit if you’re looking for some of the fastest funding on the market. You can use your debit card number to get your money directly deposited into your bank account in as soon as an hour.

OneMain lets you boost your approval odds with:

- Collateral

- Smaller loans

- Cosigners/co-borrowers

OneMain Financial isn’t transparent about its personal loan eligibility requirements, but it has no minimum credit score requirements. Before closing on a loan, you must provide:

- Government-issued identification (such as a driver’s license or passport)

- Proof of residence (such as a rental agreement or utility bill)

- Proof of income (such as pay stubs or tax returns)

OneMain loans are not available in Alaska, Arkansas, Connecticut, Massachusetts, Rhode Island, Vermont, Washington, D.C., or in U.S. territories.

Best for: Live support 7 days a week – Avant

- APR

- 9.95% to 35.99%

- Live application support seven days a week

- Get money as soon as the next business day

- 95% recommendation rating from LendingTree users who borrow from Avant

- Up to 9.99% of your loan is taken as an up-front origination fee

- Can’t boost your odds with a secured loan or a co-borrower

Avant’s application is straightforward and fast — easily one of the best application experiences we tested.

Avant could be the best fit if you need someone to walk you through your loan application. You can contact Avant application support by phone or email seven days a week.

Avant lets you boost your approval odds with smaller loans.

To get a loan with Avant, these are the requirements and restrictions:

- Residency: Not available to residents of Hawaii, Iowa, Maine, Massachusetts, Washington or West Virginia

- Administrative: Must have a bank account. May need to submit bank statements, pay stubs or tax documents to prove your income. Avant may also call your employer to verify your employment

- Credit score: 580+

Best for: Spreading out payments – Upgrade

- APR (with discounts)

- 7.74% to 35.99%

- Discounts for autopay and paying your creditors directly

- Use your car or home fixtures as collateral for better odds

- Get lower monthly payments with a long loan term

- 97% recommendation rating from LendingTree users who borrow from Upgrade

- Lender takes 1.85% – 9.99% from all loans as an origination fee

Upgrade’s application is very quick, with few questions, and it’s easy to apply with a co-borrower — you can add their information on the first page. You will need to create an account to see your rates, though.

Upgrade could be the best fit if you need to stretch out your loan across an extra-long loan term to make monthly payments affordable. Keep in mind that longer loan terms mean you’ll pay more in interest overall.

Upgrade lets you boost your approval odds with:

- Collateral

- Smaller loans

- Cosigners/co-borrowers

To qualify for a loan through Upgrade, you must meet the requirements below:

- Age: Be at least 18 years old (19 in some states)

- Citizenship: Be a U.S. citizen, permanent resident or live in the U.S. with a valid visa

- Administrative: Have a valid bank account and email address

- Credit score: 600+

Other ways to get money with bad credit

This article focuses on unsecured personal loans for bad credit, but there are other options that may be a better fit for you.

| Ways to borrow | Best if… | Pros and cons |

|---|---|---|

| Secured loans | You have collateral you can afford to lose | Pros: Easier to get, lower rates Cons: Risk losing your collateral if you can’t make payments |

| No-credit-check loans | You need a smaller loan that you can pay off fast | Pros: No credit check, can get online Cons: High rates/fees, apps can lead to overborrowing |

| Joint personal loans | You have a supportive family member/friend willing to back your loan | Pros: Easier to get, lower rates Cons: Missing or late payments will hurt both of your credit scores |

| Cash advances | You have a financial emergency and need fast cash | Pros: No credit check, fast cash Cons: Potential fees and high rates |

| Payday loans | You can afford high fees and can pay the loan off fast | Pros: No credit check, fast cash Cons: APRs up to 400% could trap you in a cycle of debt |

| Pawnshop loans | You have something of value to offer the pawnshop that you can stand to lose | Pros: No credit checks, fast cash Cons: Risk losing collateral, high fees |

| Car title loans | You understand the risk of using your car as collateral and have no other options | Pros: No credit check, fast cash Cons: High rates, risk losing your car |

Why use LendingTree?

$200M+ in funding

In 2025 alone, LendingTree helped find funding for over $200 million in personal loans for people with credit scores below 580.

$1,659 in savings

LendingTree users save $1,659 on average just by shopping and comparing personal loan rates.

360,000+ loans

In 2025, LendingTree helped find funding for over 360,000 personal loans.

What sets LendingTree content apart

Expert

Our personal loan writers and editors have 52 years of combined editorial experience and 42 years of combined personal finance experience.

Verified

100% of our content is reviewed by certified personal finance professionals and meets compliance and legal standards.

Trustworthy

We put your interests first. We’ll tell you about any loan drawbacks and be clear about when to consider alternatives.

How we chose the best personal loans for bad credit

LendingTree’s team of expert writers and editors reviewed more than 40 lenders and loan marketplaces — and shopped directly with 15 of them — to find the best personal loans for bad credit. To make our list, lenders must advertise a minimum credit score of 600 or lower and cap their annual percentage rates (APRs) below 36%.

From there, we assessed each lender across four categories: eligibility and access; cost to borrow; loan terms and options; repayment support and tools.

According to our systematic rating and review process, the best personal loans for bad credit come from Upstart, OneMain Financial, Avant and Upgrade. LendingTree reviews and fact-checks our top lender picks on a monthly basis.

Our categories

We assess how easy it is for people to qualify and apply. This includes state availability, soft-credit prequalification, membership requirements, funding speed and whether borrowers with less-than-excellent credit can get a loan.

We evaluate how affordable the loans are based on minimum and maximum APRs, loan fees and rate discounts. Lenders with unclear or potentially predatory costs receive lower scores.

We consider repayment term flexibility, loan amount ranges and whether options like secured loans, joint loans or direct-to-creditor payments are offered — plus whether the lender clearly communicates these options.

We evaluate borrower experience after funding: customer service access, hardship or forbearance programs, payment flexibility and digital tools like mobile apps or credit monitoring.

Our process

We gather data directly from lenders through their websites, disclosures and direct communication with company representatives. Our editorial team verifies and updates information regularly. We value transparency and award less favorable scores when lenders obscure or omit details.

Our editorial team applies the same scoring model and standards to every lender. Lenders cannot pay to influence our ratings.

Why trust LendingTree’s methodology?

LendingTree’s writers and editors diligently vet dozens of lenders to narrow down which ones offer the most affordable rates and a customer-centered experience. We have ongoing conversations with loan companies to ensure accuracy and collect first-person feedback to understand the holistic process of getting and repaying a loan.

Using my financial health counseling certification, I’m here to walk you through the important — and sometimes stressful — process of understanding your personal finances and credit.

Amanda’s experience in editing and financial education helps shape LendingTree articles that are clear, accurate and truly useful to readers. Her certification means our recommendations are built on a foundation of consumer-first financial knowledge — not just numbers.

Frequently asked questions

Upstart is our top expert pick for the best loan for bad credit. Its credit score minimum is one of the lowest on the market, and it caps its rates at 35.99%, which is reasonable for a bad credit loan.

Yes, it’s possible to get a personal loan with a 500 credit score — two lenders on our list (Upstart and OneMain Financial) don’t have a specified minimum credit score requirement you have to meet. However, they will likely consider other factors such as your credit history, income and current amount of debt.

Check out our expert tips on how to improve your chances of approval. Here’s the short version: Apply with a co-borrower, take out less money, use collateral or take the time to improve your credit.

Yes, your credit score will drop slightly when the lender pulls your credit. But as long as you make payments on time, any drop will likely be temporary and small.