Best Personal Loans with the Lowest Rates in July 2026

Estimate your rate and compare loans of up to $100,000

Advertising Disclosures

Loading Disclosures…

- Personal loan APRs range from about 6% to 36%. We’ll show you what those rates mean in real dollars and monthly payments.

- You could qualify even with fair or bad credit. The better your credit, the less you’ll likely pay in interest.

- SoFi ranks as the best overall personal loan lender right now based on LendingTree’s objective methodology.

- Comparing offers from several lenders can help you save thousands on your loan.

See how much your loan could cost in real dollars

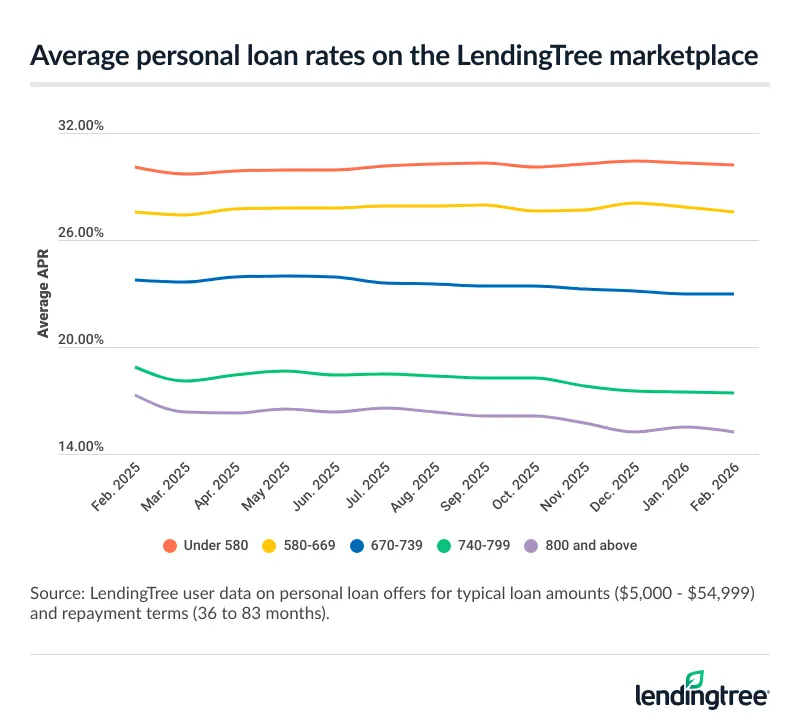

Use the table below to find the average annual percentage rate (APR) for your credit score based on real LendingTree marketplace data.

Then see how much your loan could cost by plugging the average APR for your credit score into the calculator below.

| Credit tier | Average APR |

|---|---|

| Excellent (800 and above) | 15.34% |

| Very good (740-799) | 17.46% |

| Good (670-739) | 22.70% |

| Fair (580-669) | 27.52% |

| Poor (under 580) | 30.51% |

Why borrowers apply for personal loans — and how needs vary by loan size and credit score

Debt consolidation is the leading reason borrowers apply for personal loans, accounting for nearly 1 in 3 requests (31.3%), according to a LendingTree analysis of consumer loan inquiries — far ahead of “other” at 19.5%.

Demand drops off from there: 10.6% of requests are for credit card refinancing, with smaller shares citing everyday bills (8.2%) and home improvements (6.6%).

Overall, the data shows personal loans serve a wide range of needs, from debt management to short-term expenses to larger planned purchases.

Key findings

- Debt consolidation leads by a wide margin. It accounts for 31.3% of requests — well ahead of the next category — with these borrowers requesting $11,829 on average and holding midrange credit scores (602).

- Smaller loans skew toward urgent needs. Requests for everyday bills, medical expenses and car repairs are typically under $6,000 and tied to lower average credit scores (571 to 574), suggesting short-term financial gaps.

- Larger loans align with planned spending. Homebuying ($18,838) and business ($14,704) have the highest average requested amounts and somewhat higher credit scores, indicating more deliberate use.

Why borrowers apply for personal loans

| Rank | Reason for personal loan | % of personal loan requests | Avg. requested loan size | Avg. credit score |

|---|---|---|---|---|

| 1 | Debt consolidation | 31.3% | $11,829 | 602 |

| 2 | Other | 19.5% | $5,889 | 573 |

| 3 | Credit card refinancing | 10.6% | $8,995 | 602 |

| 4 | Everyday bills | 8.2% | $4,317 | 574 |

| 5 | Home improvement | 6.6% | $10,769 | 600 |

| 6 | Major purchase | 5.3% | $10,630 | 614 |

| 7 | Medical expenses | 4.6% | $5,526 | 571 |

| 8 | Moving/relocation | 3.7% | $6,292 | 575 |

| 9 | Car financing | 3.5% | $9,997 | 585 |

| 10 | Car repair | 3.1% | $3,967 | 573 |

| 11 | Business | 1.6% | $14,704 | 580 |

| 12 | Vacation | 1.2% | $5,539 | 588 |

| 13 | Wedding expenses | 0.6% | $9,336 | 593 |

| 14 | Homebuying | 0.3% | $18,838 | 606 |

| 15 | Green loan | 0.0% | $7,187 | 597 |

Study methodology

This analysis is based on anonymized personal loan inquiries on the LendingTree platform from April 2025 through March 2026. Reasons for loan requests, requested loan amounts and self-reported credit scores were provided by consumers at the time of inquiry. Percentages reflect the share of total requests during the study period.

Estimate your monthly loan payment in seconds

You don’t need to know your exact loan term (how long you’ll pay off your loan) right away. Play around with the calculator to see how your term affects your monthly payments.

Rule of thumb: Choose the shortest loan term with a monthly payment you can afford. Short loan terms mean a cheaper loan overall, but higher monthly payments. Long terms mean more expensive loans overall, but lower monthly payments.

Save money and time by comparing real offers

You’d shop around for flights. Why not your loan? LendingTree makes it easy. Instead of applying to just one lender and hoping for a good rate, see multiple lenders compete for your business — so you can choose the best offer.

Tell us what you need

Take two minutes to share a few details about yourself and how much you want to borrow. It’s free, simple and secure.

Shop your offers

LendingTree users receive 11 personal loan offers on average. Compare yours side by side to find the one that works best for you.

Get your money

Users save an average of $1,659 by choosing the offer with the lowest rate. Once you pick a lender and sign your paperwork, you could see money in your account in as little as 24 hours.

Getting multiple offers makes lenders compete for your business, which can help you get a cheaper loan.

- You could save thousands. LendingTree users save an average of $1,659 by comparing personal loan offers and choosing the best one. People with fair or good credit could save up to $3,138 by getting six or more offers.

- The best time to save is when you apply. Once you take out a loan, you’d need to refinance (get a new loan) to get lower rates and payments down the line.

Best personal loan companies right now

Best personal loan company overall

As of July 2026, SoFi is the best personal loan company according to our methodology (how we evaluate and score lenders). SoFi offers quick funding, optional fees and competitive rates.

LendingTree personal loan experts evaluate and rate lenders using an impartial, proprietary rating system that considers the factors that matter most to you: how easy loans are to qualify for, how much they cost and how easy they are to pay back. We apply the same methodology to every lender to ensure fair comparisons.

Learn more about how we rate personal loan companies.

Best alternatives:

- Upgrade (low rates and accessible to people with fair credit)

- PenFed (low rates and no fees)

Best lenders by situation

| Lender recommendations | |

|---|---|

| Best personal loan lenders | SoFi, Upgrade, PenFed |

| No required fees | Discover, LightStream, PenFed, SoFi |

| Same-day funding | SoFi, LightStream, Rocket Loans |

| Loans for bad credit | Upstart, Prosper |

| Loans for fair credit | Best Egg, Happen Bank |

Top 10 best personal loan companies

| Lender | User rating | Best for | APR | See Results |

|---|---|---|---|---|

|

|

Overall personal loans | 6.99% to 35.49% (with discounts) | ||

|

|

Runner-up, overall personal loans | 6.09% to 17.99% (with autopay) | ||

|

|

Runner-up, overall personal loans | 7.74% to 35.99% (with discounts) | ||

|

|

Lowest rates with collateral | 5.99% to 29.99% | ||

|

|

Excellent customer service and no fees | 6.99% to 24.99% | ||

|

|

Joint loans, fair credit OK | 5.96% to 35.99% | ||

|

|

Big loans and no fees | 7.24% to 24.89% (with autopay) | ||

|

|

Better approval odds with peer-to-peer loans

Peer-to-peer loans come from individual investors (people) and are typically easier to get.

|

8.99% to 35.99% | ||

|

|

Same-day funding, fair credit OK | 7.99% to 29.99% (with autopay) | ||

|

|

Bad or no credit | 6.20% to 35.99% |

| Lender |

|

|

|

|

|

|

|

|

|

|

|---|---|---|---|---|---|---|---|---|---|---|

| User rating | ||||||||||

| Best for | Overall personal loans | Runner-up, overall personal loans | Runner-up, overall personal loans | Lowest rates with collateral | Excellent customer service and no fees | Joint loans, fair credit OK | Big loans and no fees |

Better approval odds with peer-to-peer loans

Peer-to-peer loans come from individual investors (people) and are typically easier to get.

|

Same-day funding, fair credit OK | Bad or no credit |

| APR | 6.99% to 35.49% (with discounts) | 6.09% to 17.99% (with autopay) | 7.74% to 35.99% (with discounts) | 5.99% to 29.99% | 6.99% to 24.99% | 5.96% to 35.99% | 7.24% to 24.89% (with autopay) | 8.99% to 35.99% | 7.99% to 29.99% (with autopay) | 6.20% to 35.99% |

Best for: Overall personal loans – SoFi

- APR (with discounts)

- 6.99% to 35.49%

Terms and conditions apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. To qualify, a borrower must be a U.S. citizen or other eligible status, be residing in the U.S., and meet SoFi’s underwriting requirements. Not all borrowers receive the lowest rate. Lowest rates reserved for the most creditworthy borrowers. If approved, your actual rate will be within the range of rates at the time of application and will depend on a variety of factors, including term of loan, evaluation of your creditworthiness, income, and other factors. If SoFi is unable to offer you a loan but matches you for a loan with a participating bank, then your rate may be outside the range of rates listed above. Rates and Terms are subject to change at any time without notice. SoFi Personal Loans can be used for any lawful personal, family, or household purposes and may not be used for post-secondary education expenses. Minimum loan amount is $5,000. The average of SoFi Personal Loans funded in 2025 was around $32K. Information current as of 07/20/26. SoFi Personal Loans originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org). See SoFi.com/legal for state-specific license details. See SoFi.com/eligibility for details and state restrictions. Fixed rates from 6.99% APR to 35.49% APR. APR reflect the 0.25% autopay interest rate discount and a 0.25% member rate discount. SoFi Platform personal loans are made either by SoFi Bank, N.A. or , Cross River Bank, a New Jersey State Chartered Commercial Bank, operating from its Delaware branch, Member FDIC, Equal Housing Lender. SoFi may receive compensation if you take out a loan originated by Cross River Bank. These rate ranges are current as of 07/20/26 and are subject to change without notice. Not all rates and amounts available in all states. See SoFi Personal Loan eligibility details at https://www.sofi.com/eligibilitycriteria/#eligibility-personal. Not all applicants qualify for the lowest rate. Lowest rates reserved for the most creditworthy borrowers. Your actual rate will be within the range of rates listed above and will depend on a variety of factors, including evaluation of your credit worthiness, income, and other factors. Loan amounts range from $5,000– $100,000. The APR is the cost of credit as a yearly rate and reflects both your interest rate and an origination fee of 9.99% of your loan amount for Cross River Bank originated loans which will be deducted from any loan proceeds you receive and for SoFi Bank originated loans have an origination fee of 0%-7%, will be deducted from any loan proceeds you receive. Autopay: The SoFi 0.25% autopay interest rate reduction requires you to agree to make monthly principal and interest payments by an automatic monthly deduction from a savings or checking account. The benefit will discontinue and be lost for periods in which you do not pay by automatic deduction from a savings or checking account. Autopay is not required to receive a loan from SoFi. Member Rate Discount: To be eligible for an additional 0.25% interest rate reduction on a Personal Loan, you must, within 31 days of loan funding, either (1) meet SoFi Plus eligibility criteria, (2) receive an Eligible Direct Deposit into a SoFi Checking or Savings account, or (3) receive at least $5,000 in Qualifying Deposits into a SoFi Checking or Savings account. You must continue to meet at least one of the above eligibility criteria every 31 days to maintain the discount. See the SoFi Plus terms for details on SoFi Plus subscription. For more details on Eligible Direct Deposit or Qualifying Deposits, please see https://www.sofi.com/legal/banking-rate-sheet. Once you become eligible during the initial period, the discount will be removed or reinstated depending on whether the criteria have been met. Each time your loan is re-amortized, your monthly payment amount will change based upon the interest rate that was in place. SoFi reserves the right to modify or terminate this offer at any time for unenrolled participants. You are not required to meet these criteria to be approved for a loan.

- No required fees

- Get money as soon as the day you’re approved

- 0.25% autopay discount

- Borrowers with bad credit won’t qualify

- Lowest rates require paying upfront origination fee

- Must borrow at least $5,000

I shopped for personal loans with SoFi using my real information. Here’s what I found:

- Application experience: SoFi’s application is quick and simple, and it’s easy to add a co-borrower. Plus, SoFi anticipates and answers questions about how much to borrow, what to include as income and what counts as your housing payment.

- Unusual questions to prepare for: None. Just have your Social Security number on hand.

SoFi has some of the quickest loans on the market — you could see money in your bank account as soon as the same business day you sign your agreement. You can also choose how you pay. You can get lower rates when you pay SoFi an upfront fee or skip the fee for higher rates.

Since SoFi’s minimum credit score is 600, consider lenders like Prosper or Upstart if you have bad credit. You’ll also need to look elsewhere — like PenFed Credit Union or Upgrade — for a loan smaller than $5,000 (SoFi’s minimum).

You must meet the requirements below to get a loan from SoFi:

- Age: Be the age of majority in your state (typically 18)

- Citizenship: Be a U.S. citizen, an eligible permanent resident or a non-permanent resident (a Deferred Action for Childhood Arrivals recipient or asylum-seeker, for instance)

- Employment: Have a job or job offer with a start date within 90 days, or have regular income from another source

- Credit score: 600+

Best for: Runner-up, overall personal loans – PenFed Credit Union

- APR (with autopay)

- 6.09% to 17.99%

- Borrow as little as $600

- No upfront fees

- Rates capped at 17.99%

- Must become credit union member to get a loan (but everyone is eligible to apply)

- Doesn’t publish minimum credit score, income or other info on how to qualify

I shopped for personal loans with PenFed Credit Union using my real information. Here’s what I found:

- Application experience: PenFed Credit Union’s application was quick and included helpful context to clarify potentially confusing questions. Be prepared to verify your phone number as part of the application process — this is an unusual step that most lenders skip.

- Unusual questions to prepare for: None! Just have your Social Security number on hand.

PenFed Credit Union loans can help you keep costs down with low rates, no fees and smaller loan amounts than most traditional lenders. Borrowing only what you need helps you avoid paying unnecessary interest, and PenFed’s small loans make that easy.

You’ll need to become a member in order to get a loan, but PenFed Credit Union makes it easy to join. Note that while PenFed Credit Union’s eligibility requirements are unclear, you can see if you qualify without affecting your credit score.

To qualify for a PenFed Credit Union loan, you must meet the following requirements:

- Membership: PenFed Credit Union membership (anyone can apply)

- Administrative: Open up PenFed Credit Union savings account with $5 deposit; may need to submit documents to verify your identity and income

Best for: Runner-up, overall personal loans – Upgrade

- APR (with discounts)

- 7.74% to 35.99%

- Recommended by 97% of LendingTree users who borrow from Upgrade

- Get money in as soon as one business day

- Can send money directly to your creditors if you’re consolidating

- Customer service available every day of the week, including weekends

- Fair credit OK

- Charges an upfront origination fee

- Some other lenders offer a lower starting APR

Lending platform Upgrade stands out for its borrower-friendly features, low qualification requirements and highly rated customer service. Upgrade lets you save with four APR discount opportunities or by applying for a joint personal loan (a loan you share with a co-borrower) for better odds at a lower rate.

Keep in mind that if you take out an Upgrade personal loan, you’ll pay an upfront origination fee of 1.85% – 9.99% of your loan amount. Want to skip the fees? Check out no-fee lenders like PenFed, Discover and LightStream.

To qualify for a loan through Upgrade, you must meet the requirements below:

- Age: Be at least 18 years old (19 in some states)

- Citizenship: Be a U.S. citizen, permanent resident or live in the U.S. with a valid visa

- Administrative: Have a valid bank account and email address

- Credit score: 600+

Best for: Lowest rates with collateral – Best Egg

- APR

- 5.99% to 29.99%

- Secured loans are generally easier to qualify for and can come with lower rates

- Get money in as soon as 24 hours

- Fair credit OK

- Not available in all states

- Charges an upfront fee on every loan

- Can’t apply for a loan with another person

I shopped for personal loans with Best Egg using my real information. Here’s what I found:

- Application experience: Best Egg asks more questions than the average lender, but its application is clear and easy to complete. Once you have offers, you can quickly click through to a loan agreement that outlines the next steps and how much you’ll pay.

- Unusual questions to prepare for: Annual income for other people in your household, other types of accounts held (e.g., savings, retirement and investments), car payment, number of cash advances taken in past six months

If you have fair to good credit, own your home and want to boost your approval odds, Best Egg’s secured loan for homeowners is worth considering. You’ll back your Best Egg secured loan with fixtures in your house like cabinets and lighting. Offering collateral can make it easier to get a loan (or even lower rates) because it reduces the lender’s risk.

Think twice about Best Egg’s secured loan if you’re planning to move or refinance. Because Best Egg puts a lien on your fixtures, the loan needs to be paid in full before you can sell or refinance your mortgage. Also note that you can’t apply for a Best Egg loan with another person (like the co-owner of your house, for instance).

Best Egg uses built‑in home fixtures as collateral but doesn’t require an appraisal of them. It reviews your credit history and home equity instead.

You must also meet the requirements below to qualify for a Best Egg loan:

- Age: Be of legal age to accept a loan in your state (usually 18)

- Citizenship: Be a U.S. citizen or permanent resident living in the U.S.

- Administrative: Have a personal checking account, email address and physical address

- Residency: Not live in the District of Columbia, Iowa, Vermont, West Virginia or U.S. territories

- Credit score: 620+

Best for: Excellent customer service and no fees – Discover

- APR

- 6.99% to 24.99%

- U.S.-based loan specialists available seven days a week

- Get money as soon as the next business day

- Repayment assistance options if you can’t make payments

- No fees

- Can’t apply for a loan with another person

- Need good or excellent credit to qualify

- Can only borrow up to $40,000

I shopped for personal loans with Discover using my real information. Here’s what I found:

- Application experience: Discover’s application process was quick and easy — there were only a few questions and the interface was intuitive. I got instant offers, and Discover gave me a reference number to log back in and review them again later.

- Unusual questions to prepare for: None! Just remember to have your Social Security number on hand.

With a 97% approval rating from LendingTree users, Discover earns high marks for customer satisfaction. Its U.S.-based loan specialists are available seven days a week, take phone calls and offer extended customer service hours as late as 11 p.m. Eastern time on weekdays.

Discover personal loans only go up to $40,000, so if you’re looking for a large personal loan, consider other lenders on this list like LightStream or SoFi.

You’ll need to meet these eligibility criteria to get a Discover loan:

- Age: Be at least 18

- Citizenship: Have a Social Security number

- Administrative: Have a physical address, email address and internet access

- Income: Minimum income of $40,000 (individually or as a household)

- Credit score: 720+

Best for: Joint loans, fair credit OK – Happen Bank

- APR

- 5.96% to 35.99%

- Get money as soon as 24 hours

- Available to people with fair credit

- Can apply with another person for better odds of approval

- May charge upfront origination fee (0.00% – 8.00%)

- Borrowers with bad credit won’t qualify

If you have fair credit and want to boost your odds of getting a loan with lower rates, check out Happen Bank. While many lenders don’t offer joint loans, Happen Bank allows co-borrowers — adding another person with good credit can help you qualify, get lower rates and even qualify for more money.

Happen Bank sometimes charges an upfront origination fee that it takes out of your loan before sending you the money. You won’t qualify for a Happen Bank loan with bad credit, so check out Prosper and Upstart if your credit score is below 580.

To be eligible for a Happen Bank personal loan, you must meet the following requirements:

- Age: Be at least 18 years old

- Citizenship: Be a U.S. citizen or permanent resident

- Administrative: Have a verifiable bank account

- Credit score: 600+

Best for: Big loans and no fees – LightStream

- APR (with autopay)

- 7.24% to 24.89%

Your loan terms, including APR, may differ based on loan purpose, amount, term length, and your credit profile. Excellent credit is required to qualify for lowest rates. Rate is quoted with AutoPay discount. AutoPay discount is only available prior to loan funding. Rates without AutoPay are 0.50% points higher. Subject to credit approval. Conditions and limitations apply. Advertised rates and terms are subject to change without notice. Payment example: Monthly payments for a $25,000 loan at 6.49% APR with a term of 3 years would result in 36 monthly payments of $766.11. © 2024 Truist Financial Corporation. Truist, LightStream and the LightStream logo are service marks of Truist Financial Corporation. All other trademarks are the property of their respective owners. Lending services provided by Truist Bank.

- Get money as soon as the same day

- No fees

- Borrow up to $100,000 (most lenders only offer up to $50,000)

- 0.50% autopay discount

- Checking rates will require a hard credit pull (and knock a few points off your score)

- No due date extensions

- Must have good or excellent credit to qualify

I started the application process with LightStream using my real information. Here’s what I found:

- Application experience: LightStream’s application has more questions than usual because you’re getting real rates rather than estimates from prequalified offers. You’ll also have to create an account to see rates. That said, I love how straightforward LightStream’s application is — it anticipates and answers common questions.

- Unusual questions to prepare for: Time at current address, time with current employer, estimated home equity, checking and savings balances plus stocks and bonds, retirement assets

LightStream is one of the few personal loan lenders that offers more than $50,000, making its loans ideal for big expenses. Its competitive rates and low fees could translate to huge savings if you need a large loan.

Unlike many personal loan companies, LightStream doesn’t let you check your rates by prequalifying. If you want to see your rates and terms, LightStream will do a hard credit pull, which can cause your credit score to take a small, temporary dip.

LightStream doesn’t specify its exact credit score requirements, but you must have good to excellent credit to qualify. Most of the applicants that LightStream approves have the following in common:

- At least five years of on-time payments under a variety of accounts (credit cards, auto loans, etc.)

- Stable income and the ability to handle paying their current debt obligations

- Savings, whether in a bank account, an investment account or a retirement account

Best for: Better approval odds with peer-to-peer loans – Prosper

- APR

- 8.99% to 35.99%

- Qualify with a score as low as 560

- Can apply for a loan with another person

- Get money as soon as one business day

- Charges an upfront origination fee

- Could take up to 14 days for investors to fund a loan, though this isn’t typical

- Not available in all states

I shopped for personal loans with Prosper using my real information. Here’s what I found:

- Application experience: Prosper’s application is quick and straightforward, and it’s easy to add a co-borrower with a click of a button. Prosper also includes helpful information about the types of income you’ll need to report, which can often be confusing when applying for a loan.

- Unusual questions to prepare for: Prosper asks if you’re enrolled in a debt settlement program. (If you don’t know what debt settlement is, the answer is likely no.)

When you apply for a loan with Prosper, individual investors (people) decide whether to fund your loan — not a bank. This is called peer-to-peer lending, and it’s typically easier to qualify for than a traditional personal loan. Prosper’s low credit requirement makes its loans accessible to people with fair credit who might otherwise only qualify for predatory loans.

Prosper could send your money as soon as one business day, but the timing largely depends on investors. While it typically takes investors between one and three business days to fund loans, it could take up to 14 days, which is on the long end compared to other personal loan timelines.

To get a loan with Prosper, you must meet the following requirements:

- Age: Be 18 or older

- Administrative: Have a U.S. bank account and Social Security number

- Residency: Must live in an eligible U.S. state (Prosper operates in most states, with only a small number of states excluded)

- Credit score: 560+

Best for: Same-day funding, fair credit OK – Rocket Loans

- APR

- 7.99% to 29.99%

- Get money as soon as the same day

- Available to people with fair credit

- Competitive maximum rate

- Charges an upfront fee (Up to 9.99%)

- Can’t apply with another person

- Only offers two loan term options (36 or 60 months)

- Not available in all states

Check out Rocket Loans if you have fair credit and need an emergency loan. You could get your money as soon as the same day — some of the fastest funding available on the market — and Rocket Loans’ rates only go up to 29.99% APR, which is lower than the average rate for fair credit.

Rocket Loans does charge upfront origination fees, which could add to the cost of your loan. Plus, it only offers two loan terms, so consider other lenders if you need a short-term or long-term loan.

To qualify for Rocket Loans, you’ll need to meet the following requirements:

- Citizenship: Must be a U.S. citizen

- Age: 18 or older

- Income: Minimum annual income of $24,000

- Residency: Must live in an eligible U.S. state (Rocket Loans operates in most states, with only a small number of states excluded)

- Credit score: 620+

Best for: Bad or no credit – Upstart

- APR

- 6.20% to 35.99%

- Low or no credit won’t disqualify you

- Get money in as soon as one business day

- Consistently rated top 3 in customer satisfaction by LendingTree users

- Can’t take out a loan with another person

- Only two repayment terms to choose from (Not specified or Not specified months)

- May charge an origination fee

“I had never taken out a personal loan before, but it only took me a few minutes to fill out Upstart’s application and hear back about whether I prequalified. On top of that, I got to skip paying an origination fee — which saved me money — and the monthly payments ended up fitting my budget.” – Amanda Push, LendingTree deputy editor

Upstart loans are worth considering for applicants with limited or bad credit history. Unlike most other lenders, Upstart offers loans to borrowers who are credit invisible or don’t have long enough credit histories to generate a credit score.

You’ll likely pay a high price to get an Upstart loan if you have bad or no credit — Upstart charges rates as high as 35.99%.

Upstart has transparent eligibility requirements, including:

- Age: Be 18 or older

- Administrative: Have a U.S. address, personal banking account, email address and Social Security number

- Income: Have a valid source of income, including a job, job offer or another regular income source

- Credit-related factors: No bankruptcies within the last three years, reasonable number of recent inquiries on your credit report and no current delinquencies

- Credit score: None

What is a personal loan?

A personal loan gives you a lump sum of money — typically sent straight to your bank account — that you’ll pay back in equal monthly payments. Here’s what to know:

- Fixed interest: Interest stays the same during the loan, and so do your payments. Credit card interest goes up and down with the market.

- How to qualify: There’s no universal minimum credit score for personal loans — but the better your credit, the cheaper your loan will likely be. Learn more about personal loan requirements.

- How to apply: You can apply for a personal loan on the lender’s website or use a service like LendingTree to get quotes from up to five lenders at once.

Personal loans are a popular solution for dealing with debt. Nearly three-quarters (72%) of Americans have a personal loan, have had one in the past or have considered getting one, according to a LendingTree survey.

Track personal loan rates with LendingTree

Personal loan rates have held steady over the past year, but they remain relatively high — making it more important than ever to compare lenders and find the best offer for your credit profile.

How your credit score affects what you’ll pay

It’s hard to know how much your loan will actually cost in dollars when you’re looking at APR ranges. The example below shows how your credit score can affect the amount you pay when you borrow $5,000 over 48 months.

| Credit score range | Average APR | Monthly payment | Interest | Total cost |

|---|---|---|---|---|

| Excellent (800 and above) | 15.75% | $141.06 | $1,770.98 | $6,770.98 |

| Very good (740-799) | 17.89% | $146.59 | $2,036.21 | $7,036.21 |

| Good (670-739) | 23.27% | $161.00 | $2,727.90 | $7,727.90 |

| Fair (580-669) | 27.79% | $173.66 | $3,335.70 | $8,335.70 |

| Poor (under 580) | 30.25% | $180.76 | $3,676.37 | $8,676.37 |

Improving your credit before getting a loan will help you get lower rates and save money. You could save more than $1,804 on your loan by raising your score from “fair” to “very good,” according to a LendingTree study.

How to choose the best loan for your credit score

When comparing personal loan offers, use the LendingTree loan calculator to compare APRs, monthly payment and total interest payments. Here’s what to expect and watch out for based on your credit score:

| Your credit band | Typical loan options | Tips |

|---|---|---|

| Excellent (800 and above) | Low rates, options with no fees | Prioritize offers with low rates and no origination fee. |

| Good to very good (670 – 799) | Slightly higher rates, may need to pay fees | Lenders deduct origination fees before sending your loan, so make sure you’ll get the full amount of money you need. |

| Fair (580 – 669) | Fewer options with higher rates, fees likely | Find the offer with the lowest APR that has a monthly payment you can afford. |

| Poor (under 580) | Few options, highest rates | Add a co-borrower or collateral for lower rates and better odds of approval. |

Expert insights on finding the lowest personal loan rate

If you don’t shop around for the best rate on your next personal loan, you’re probably going to pay too much. Rates, terms and amounts can vary significantly by lender, so it is absolutely worth the effort to compare offers from multiple personal loan companies.

Life’s too expensive today to settle for paying more than you need.

More personal loan guides

How we chose the best personal loans

We reviewed more than 40 lenders and loan marketplaces that offer personal loans to determine the overall best 10 lenders. LendingTree reviews and fact-checks our top lender picks on a monthly basis.

According to our systematic rating and review process, the best personal loans come from SoFi, Upgrade, Best Egg, Discover, Happen Bank, LightStream, PenFed Credit Union, Prosper, Rocket Loans and Upstart.

We assessed each lender across four categories: eligibility and access; cost to borrow; loan terms and options; repayment support and tools.

Our categories

We assess how easy it is for people to qualify and apply. This includes state availability, soft-credit prequalification, membership requirements, funding speed and whether borrowers with less-than-excellent credit can get a loan.

We evaluate how affordable the loans are based on minimum and maximum APRs, loan fees and rate discounts. Lenders with unclear or potentially predatory costs receive lower scores.

We consider repayment term flexibility, loan amount ranges and whether options like secured loans, joint loans or direct-to-creditor payments are offered — plus whether the lender clearly communicates these options.

We evaluate borrower experience after funding: customer service access, hardship or forbearance programs, payment flexibility and digital tools like mobile apps or credit monitoring.

Our process

We gather data directly from lenders through their websites, disclosures and direct communication with company representatives. Our editorial team verifies and updates information regularly. We value transparency and award less favorable scores when lenders obscure or omit details.

Our editorial team applies the same scoring model and standards to every lender. Lenders cannot pay to influence our ratings. Read more about our editorial guidelines.

Why trust LendingTree’s methodology?

Our writers and editors dig through the facts, contact lenders directly and even go through the application process ourselves if it helps better explain what you can expect. As a Certified Financial Education Instructor℠, I’m committed to breaking down complex financial details so people can make confident, informed decisions with their money.

Jessica’s experience in editing and financial education helps shape LendingTree articles that are clear, accurate and truly useful to readers. Her certification means our recommendations are built on a foundation of consumer-first financial knowledge — not just numbers.

Frequently asked questions

LendingTree’s top 10 lenders offer legitimate personal loans that you can apply for online. Read about personal loan disadvantages to protect yourself from the risks that come with any personal loan.

Choosing the right personal loan lender is all about shopping around. Prequalify (check your rates) with several lenders, compare your offers and choose the one that fits your budget. You can get offers from up to five lenders at once with LendingTree.

Online-only lenders typically offer fast funding and can be easier to qualify for than traditional personal loans from brick-and-mortar banks, but they sometimes come with one-time origination fees that can make your loan more expensive.

Yes, some personal loan comparison sites are trustworthy. LendingTree writers and editors evaluate lenders impartially and don’t receive compensation for reviews. Learn more about how we review lenders.