Best Personal Loans With a Cosigner in 2026

Cosigners can help you qualify for loans and get better rates

Advertising Disclosures

Loading Disclosures…

- Cosigners are legally responsible for the loan if you can’t pay, but they don’t have access to the loan money.

- On the other hand, a co-borrower is legally responsible and has the same rights to the loan money.

- A cosigner with at least good credit (670+ FICO Score) can improve your chances of approval and help you qualify for better rates.

- Late or missed payments will damage both your credit and your cosigner’s credit — potentially straining your relationship.

- To protect your relationship and credit, compare multiple loan offers and choose the loan with the lowest total cost that fits your budget.

How cosigner loans work

Cosigner loans are personal loans you get with someone who guarantees repayment if you can’t pay back the loan. Here’s what you need to know:

- Who: A cosigner can be a friend, family member or another trusted person — but they’ll need to have at least good credit and a history of on-time payments to be helpful.

- Benefits: Since lenders take on less risk when two people are responsible for the loan, cosigners can make it easier to get a loan, borrow more money and get better rates.

- Risks: If you can’t pay back the loan, your cosigner will be responsible for payment. Late or missed payments will hurt your cosigner’s credit as well as your own.

How cosigners improve approval odds

Lenders want assurance that they’ll get all their money back. They typically use your credit score, income, amount of debt and employment to predict whether you’ll be able to pay them back. This is how they decide whether to approve you.

A cosigner with good or excellent credit vouches for your ability to pay. The lender considers your cosigner’s credit in addition to yours. That’s why you may be able to get better rates or more money with a cosigner — your cosigner’s credit and income count, too.

How to protect your cosigner

When you borrow with a cosigner, how you handle your loan payments will directly affect their credit — and your relationship. Here’s how to protect your cosigner:

1. Make sure you can afford the monthly payments. Before you sign, estimate your monthly payments with a personal loan calculator, then use an app like YNAB or Monarch to see if the payment fits in your budget. Be honest with yourself — this isn’t the time to fudge numbers.

2. Actively plan for on-time payments. Late payments will hurt your cosigner’s credit. If you know you’ll have enough money in your bank account, sign up for automatic payments to ensure you’re not late. You can also set a monthly calendar reminder on your phone.

3. Have an honest conversation. Make sure your cosigner understands the risks that come with cosigning a loan, and talk openly about their expectations. What should happen if you suddenly can’t make payments? Are they comfortable spotting you for a month or two? How will you earn extra money to pay back the loan?

Talking about finances with your cosigner before you get a loan will open lines of communication and minimize the risk that you don’t understand each other. Consider writing out a simple contract to make sure your expectations are aligned.

When to ask someone to cosign a loan

Cosigners can help you get the money you need and potentially make your loan cheaper. Here’s when to consider a cosigner:

- You can’t get a loan on your own. A cosigner could help you qualify if you have bad credit or a limited credit history. Lenders who have rejected your individual application may approve you when you apply with a cosigner.

- You want a cheaper loan. Lenders give lower rates to borrowers with good credit, so adding a cosigner with solid credit can help you get better rates and a cheaper loan.

- You need to borrow more money. Lenders may offer more money to two applicants instead of one, especially if the cosigner has better credit and a higher income.

Compare personal loan offers with LendingTree

You’d shop around for flights. Why not your loan? LendingTree makes it easy. Instead of applying to just one lender and hoping for a good rate, see multiple lenders compete for your business — so you can choose the best offer.

Tell us what you need

Take two minutes to tell us who you are and how much money you need. It’s free, simple and secure.

Shop your offers

LendingTree users get 11 personal loan offers on average. Compare your offers side by side to get the best deal.

Get your money

Users save an average of $1,659 by choosing the offer with the lowest rate. Once you pick a lender and sign your paperwork, you could see money in your account in as little as 24 hours.

Best cosigner and co-borrower loans

| Lender | User rating | Best for | APR | See Results |

|---|---|---|---|---|

|

|

Short-term, small co-borrower loans | 6.99% to 18.00% | ||

|

|

Cosigner loans with membership benefits | 6.09% to 17.99% (with autopay) | ||

|

|

Better approval odds with peer-to-peer co-borrower loans | 8.99% to 35.99% | ||

|

|

Big online loans with a co-borrower | 6.99% to 35.49% (with discounts) | ||

|

|

Getting multiple discounts on co-borrower loans | 7.74% to 35.99% (with discounts) |

Best for: Short-term, small co-borrower loans – First Tech Federal Credit Union

- APR

- 6.99% to 18.00%

- Can save money on interest by borrowing as little as $500 (most loans start at $1,000+)

- Terms start at 6 months (most loans start at 24 months)

- Low interest rates

- No fees

- Need to become a member to get a loan (but it’s easy to join)

- No info on minimum credit score or income requirements

If you need to borrow a small amount of money but don’t want to pay high credit card rates, consider a small, short-term loan from First Tech. The less you borrow and the sooner you pay it back, the cheaper your loan will be.

First Tech doesn’t publish minimum requirements, but you can find out if you’re eligible by prequalifying for a loan on First Tech’s website. This won’t impact your credit score.

You must meet at least one of the following criteria to join First Tech:

- Work for a partnering employer

- Be related to a current First Tech member

- Live in Lane County, Ore.

- Become a member of the Computer History Museum or Financial Fitness Association (First Tech may pay for your first year of membership, and you don’t have to maintain membership to keep your First Tech account)

Best for: Cosigner loans with membership benefits – PenFed Credit Union

- APR (with autopay)

- 6.09% to 17.99%

- Credit union membership comes with plenty of discounts and perks

- Loans start at $600 (most start at $1,000+)

- No upfront fees

- Rates capped at 17.99%

- Must become credit union member to get a loan (but everyone is eligible to apply)

- No info on minimum credit score or income requirements

Credit union membership usually comes with perks, and PenFed is no exception. After you join, you can get exclusive savings on rental cars, tax preparation software, car insurance and more. PenFed members also get free FICO Scores and monthly credit reports from Experian.

You’ll need to become a member in order to get a loan, but PenFed makes it easy to join. Note that while PenFed’s eligibility requirements are unclear, you can see if you qualify without affecting your credit score.

To qualify for a PenFed Credit Union loan, you must meet the following requirements:

- Membership: PenFed Credit Union membership (anyone can apply)

- Administrative: Open up PenFed Credit Union savings account with $5 deposit; may need to submit documents to verify your identity and income

Best for: Better approval odds with peer-to-peer co-borrower loans – Prosper

- APR

- 8.99% to 35.99%

- Peer-to-peer loans can be easier to get

- Fair credit OK

- No minimum credit history required

- Charges an upfront origination fee

- Loan review process could take five days

- Not available in all states

Prosper offers peer-to-peer loans, which can be easier to get because the money comes from individual investors instead of a bank or lender. Applying for a peer-to-peer loan with a co-borrower is a smart strategy to boost your odds of approval.

Choose another lender on this list if you need a quick loan. Prosper’s review process can take five days, which is longer than most lenders take.

To get a loan with Prosper, you must meet the following requirements:

- Age: Be 18 or older

- Administrative: Have a U.S. bank account and Social Security number

- Residency: Must live in an eligible U.S. state (Prosper operates in most states, with only a small number of states excluded)

- Credit score: 560+

Best for: Big online loans with a co-borrower – SoFi

- APR (with discounts)

- 6.99% to 35.49%

Terms and conditions apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. To qualify, a borrower must be a U.S. citizen or other eligible status, be residing in the U.S., and meet SoFi’s underwriting requirements. Not all borrowers receive the lowest rate. Lowest rates reserved for the most creditworthy borrowers. If approved, your actual rate will be within the range of rates at the time of application and will depend on a variety of factors, including term of loan, evaluation of your creditworthiness, income, and other factors. If SoFi is unable to offer you a loan but matches you for a loan with a participating bank, then your rate may be outside the range of rates listed above. Rates and Terms are subject to change at any time without notice. SoFi Personal Loans can be used for any lawful personal, family, or household purposes and may not be used for post-secondary education expenses. Minimum loan amount is $5,000. The average of SoFi Personal Loans funded in 2025 was around $32K. Information current as of 07/20/26. SoFi Personal Loans originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org). See SoFi.com/legal for state-specific license details. See SoFi.com/eligibility for details and state restrictions. Fixed rates from 6.99% APR to 35.49% APR. APR reflect the 0.25% autopay interest rate discount and a 0.25% member rate discount. SoFi Platform personal loans are made either by SoFi Bank, N.A. or , Cross River Bank, a New Jersey State Chartered Commercial Bank, operating from its Delaware branch, Member FDIC, Equal Housing Lender. SoFi may receive compensation if you take out a loan originated by Cross River Bank. These rate ranges are current as of 07/20/26 and are subject to change without notice. Not all rates and amounts available in all states. See SoFi Personal Loan eligibility details at https://www.sofi.com/eligibilitycriteria/#eligibility-personal. Not all applicants qualify for the lowest rate. Lowest rates reserved for the most creditworthy borrowers. Your actual rate will be within the range of rates listed above and will depend on a variety of factors, including evaluation of your credit worthiness, income, and other factors. Loan amounts range from $5,000– $100,000. The APR is the cost of credit as a yearly rate and reflects both your interest rate and an origination fee of 9.99% of your loan amount for Cross River Bank originated loans which will be deducted from any loan proceeds you receive and for SoFi Bank originated loans have an origination fee of 0%-7%, will be deducted from any loan proceeds you receive. Autopay: The SoFi 0.25% autopay interest rate reduction requires you to agree to make monthly principal and interest payments by an automatic monthly deduction from a savings or checking account. The benefit will discontinue and be lost for periods in which you do not pay by automatic deduction from a savings or checking account. Autopay is not required to receive a loan from SoFi. Member Rate Discount: To be eligible for an additional 0.25% interest rate reduction on a Personal Loan, you must, within 31 days of loan funding, either (1) meet SoFi Plus eligibility criteria, (2) receive an Eligible Direct Deposit into a SoFi Checking or Savings account, or (3) receive at least $5,000 in Qualifying Deposits into a SoFi Checking or Savings account. You must continue to meet at least one of the above eligibility criteria every 31 days to maintain the discount. See the SoFi Plus terms for details on SoFi Plus subscription. For more details on Eligible Direct Deposit or Qualifying Deposits, please see https://www.sofi.com/legal/banking-rate-sheet. Once you become eligible during the initial period, the discount will be removed or reinstated depending on whether the criteria have been met. Each time your loan is re-amortized, your monthly payment amount will change based upon the interest rate that was in place. SoFi reserves the right to modify or terminate this offer at any time for unenrolled participants. You are not required to meet these criteria to be approved for a loan.

- No required fees

- Can get money as soon as the day you’re approved

- 0.25% autopay discount

- Borrowers with bad credit won’t qualify

- Must borrow at least $5,000

SoFi has some of the quickest loans on the market — you could get your money as soon as the same business day you sign your agreement. You can also choose how you pay. You can get lower rates when you pay SoFi an upfront fee, or skip the fee for higher rates.

Since SoFi’s minimum credit score is 600, consider lenders like Prosper or Upstart if you have bad credit. You’ll also need to look elsewhere — like PenFed or Upgrade — for a loan smaller than $5,000 (SoFi’s minimum).

You must meet the requirements below to get a loan from SoFi:

- Age: Be the age of majority in your state (typically 18)

- Citizenship: Be a U.S. citizen, an eligible permanent resident or a non-permanent resident (a Deferred Action for Childhood Arrivals recipient or asylum-seeker, for instance)

- Employment: Have a job or job offer with a start date within 90 days, or have regular income from another source

- Credit score: 600+

Best for: Getting multiple discounts on co-borrower loans – Upgrade

- APR (with discounts)

- 7.74% to 35.99%

- Four discount opportunities

- Can get money in as soon as one business day

- Can send money directly to your creditors if you’re consolidating

- Customer service available daily, including weekends

- Fair credit OK

- Charges an upfront origination fee

Lending platform Upgrade stands out for its borrower-friendly features, low qualification requirements and highly rated customer service. Upgrade lets you save with four APR discount opportunities or by applying for a joint personal loan (a loan you share with a co-borrower) for better odds of a lower rate.

Keep in mind that if you take out an Upgrade personal loan, you’ll pay an upfront origination fee of 1.85% – 9.99% of your loan amount.

To qualify for a loan through Upgrade, you must meet the requirements below:

- Age: Be at least 18 years old (19 in some states)

- Citizenship: Be a U.S. citizen, permanent resident or live in the U.S. with a valid visa

- Administrative: Have a valid bank account and email address

- Credit score: 600+

Risks of using a cosigner

Before you decide to cosign a personal loan, it’s important to know about the downsides. Here’s what you need to know about the risks of using a co-applicant on a loan:

- Credit impact: Each applicant is legally responsible for the loan, so missing payments or going into default will hurt the credit of both parties. Plus, lenders typically pull your credit when you apply for a loan. This can cause a small, temporary dip in your credit score and your cosigner’s.

- Legal consequences: If you stop making payments, your debt will eventually go to collections, and one or both of you could be sued by a debt collector.

- Harder to qualify for future loans or credit: Cosigning a loan can increase your debt-to-income ratio, which may make it hard to take out more credit until the cosigned loan is paid off.

- Strained relationship: When you take out a loan with another person, your relationship with your cosigner hangs in the balance. How you handle payments will have real consequences for both of you. Learn how to protect your cosigner and your relationship.

Parents are hesitant to cosign loans for their kids, with many concerned about risk

Parents appear hesitant to put their own finances on the line for their children, even as many remain open to the idea under the right circumstances.

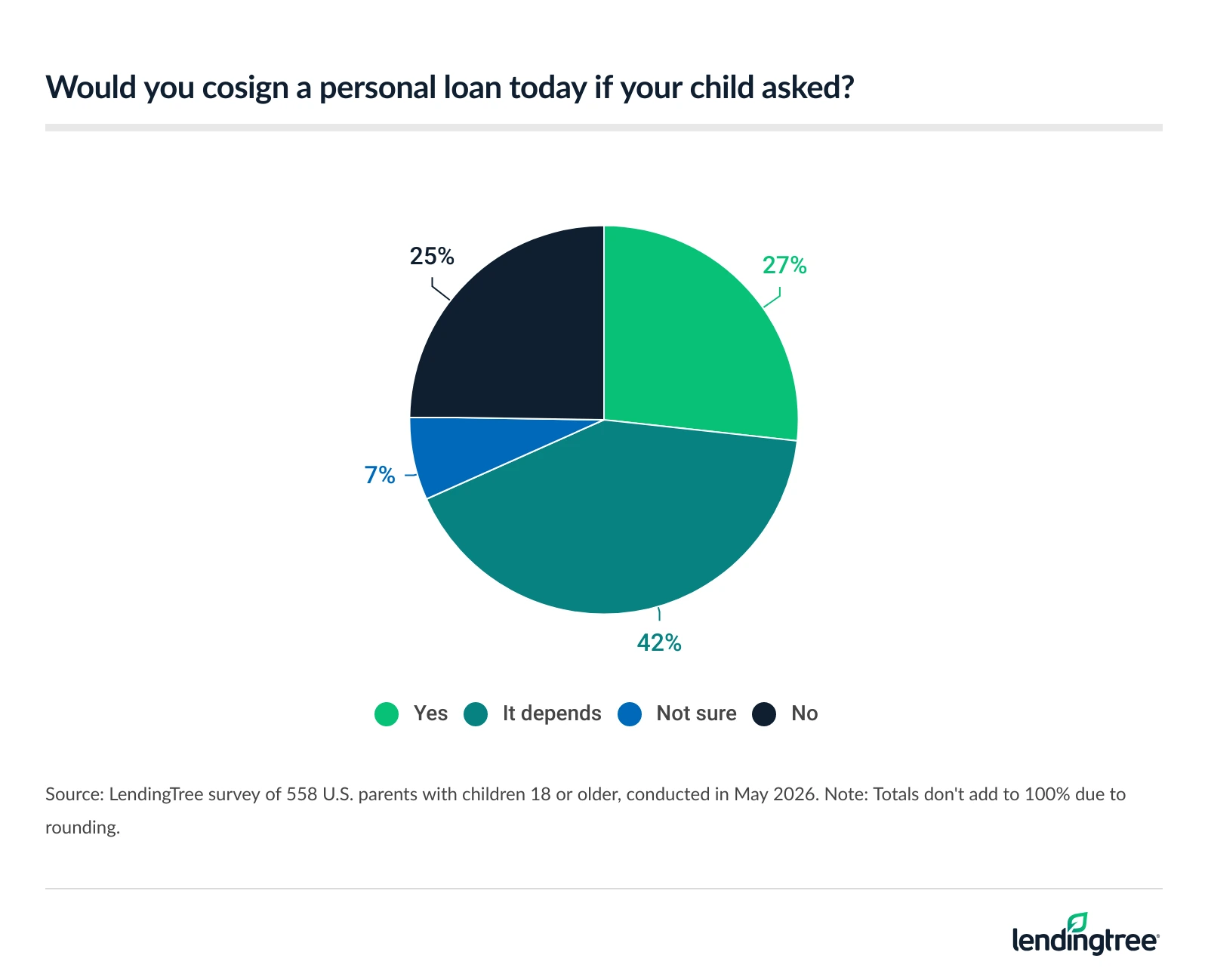

While only 23% of parents with children 18 or older say they’ve ever cosigned a personal loan for one of their kids, 21% who haven’t have at least considered it. Still, uncertainty dominates: 42% say whether they would cosign today depends, compared with 27% who say yes outright.

Among those unwilling to cosign today, the biggest concern is affordability, with 34% saying they can’t afford the risk. And for parents who’ve cosigned before, the experience hasn’t always been smooth — 20% say they made at least one payment on the loan themselves, while even more (23%) say the experience caused stress.

Key findings

- Parents are far from universally comfortable cosigning for their children. Just 27% of parents with kids 18 or older say they’d cosign a personal loan if asked today, while 25% say they wouldn’t and 42% say it depends. Among those unwilling to cosign, 34% say they can’t afford the risk.

- Only 23% of parents with children 18 or older say they’ve ever cosigned a personal loan for one of their kids. Among those who have, the financial stakes were often significant — 40% say the last loan they cosigned was for $10,000 or more. The experience also came with downsides for some: 20% say they made at least one payment on the loan themselves, while 23% say it caused them stress.

Methodology

LendingTree commissioned QuestionPro to conduct an online survey of 558 U.S. parents with kids 18 or older from May 4 to 6, 2026. The survey of parents ages 18 to 80 was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. Researchers reviewed all responses for quality control.

We defined generations as the following ages in 2026:

- Generation Z: 18 to 29

- Millennials: 30 to 45

- Generation X: 46 to 61

- Baby boomers: 62 to 80

Cosigner loan alternatives: Other ways to improve your odds

Prequalify

Many lenders allow you to check your eligibility and potential rates without impacting your credit. This is called prequalification. You can prequalify with individual lenders directly on their websites or check your offers with LendingTree.

Look at bad credit loans

If you want to improve your odds of qualifying but don’t want to use a cosigner, check out the top lenders for bad credit according to LendingTree’s objective rating system.

These lenders have low minimum credit scores but still charge rates below 36% (widely cited as the limit for affordable loans).

Use collateral

Another way to boost your odds of getting a loan is to put up collateral. This is called a secured loan. Instead of risking your cosigner’s credit, you’ll risk losing your collateral if you don’t make payments.

Try a joint loan

Joint loans are similar to cosigner loans with one key difference: Your co-borrower on a joint loan has equal access to the money, while your cosigner on a cosigned loan doesn’t. Some lenders only offer joint loans or cosigner loans, while others offer both types or neither.

What sets LendingTree content apart

Expert

Our personal loan writers and editors have 52 years of combined editorial experience and 42 years of combined personal finance experience.

Verified

100% of our content is reviewed by certified personal finance professionals and meets compliance and legal standards.

Trustworthy

We put your interests first. We’ll tell you about any loan drawbacks and be clear about when to consider alternatives.

How we chose the best personal loans with a cosigner

We reviewed more than 40 lenders and loan marketplaces to determine the best five personal loans with a cosigner or co-borrower. To make our list, lenders must offer cosigner or co-borrower loans with competitive annual percentage rates (APRs).

From there, we assessed each lender across four categories: eligibility and access; cost to borrow; loan terms and options; repayment support and tools.

According to our standardized rating system, the best cosigner loans come from First Tech Federal Credit Union, PenFed Credit Union, Prosper, SoFi and Upgrade.

Our categories

We assess how easy it is for people to qualify and apply. This includes state availability, soft-credit prequalification, membership requirements, funding speed and whether borrowers with less-than-excellent credit can get a loan.

We evaluate how affordable the loans are based on minimum and maximum APRs, loan fees and rate discounts. Lenders with unclear or potentially predatory costs receive lower scores.

We consider repayment term flexibility, loan amount ranges, and whether options such as secured loans, joint loans or direct-to-creditor payments are offered — plus whether the lender clearly communicates these options.

We evaluate borrower experience after funding: customer service access, hardship or forbearance programs, payment flexibility and digital tools like mobile apps or credit monitoring.

Our process

We gather data directly from lenders through their websites, disclosures and direct communication with company representatives. Our editorial team verifies and updates information regularly. We value transparency and award less favorable scores when lenders obscure or omit details.

Our editorial team applies the same scoring model and standards to every lender. Lenders cannot pay to influence our ratings. Read more about our editorial guidelines.

Why trust LendingTree’s methodology?

Our writers and editors dig through the facts, contact lenders directly and even go through the application process ourselves if it helps better explain what you can expect. As a Certified Financial Education Instructor, I’m committed to breaking down complex financial details so people can make confident, informed decisions with their money.

Jessica’s experience in editing and financial education helps shape LendingTree articles that are clear, accurate and truly useful to readers. Her certification means our recommendations are built on a foundation of consumer-first financial knowledge — not just numbers.

Frequently asked questions

Yes, adding a cosigner makes it easier to qualify. Cosigners lower the lender’s risk since two people are responsible for paying the loan. Adding a cosigner with good credit and a solid credit history can make it even easier to qualify.

Your cosigner should have good credit (670+ FICO Score) to improve your odds of getting a loan and help you qualify for more money or better offers. You can add a cosigner with worse credit, but you’ll be less likely to get the same benefits.

Consider getting a personal loan with a cosigner if you want:

- Better approval odds

- A large loan

- Lower interest rates

Note that your cosigner will need good or excellent credit to help you achieve these goals.

Missing payments will damage both your credit score and your cosigner’s. If neither of you makes payments, your lender will eventually send your loan to a collection agency. Consider debt relief options if you’re struggling to make payments.