Best Loans for Credit Card Refinancing in July 2026

SoFi is the best lender for credit card refinancing because of its competitive rates, APR discounts and free perks

Advertising Disclosures

Loading Disclosures…

- Credit card refinancing is using a new loan or credit card to pay off your credit card debt.

- A balance transfer card could be the cheapest option, but only if you can pay off your debt during the 0% APR intro period. Otherwise, interest can add up quickly.

- Refinancing moves your debt; it doesn’t eliminate it. If you don’t slow down using your credit cards after refinancing, you’ll end up worse off than before you started.

How does credit card refinancing work?

To refinance your credit cards, you’ll pay them off with a personal loan or move your debt to a balance transfer credit card. Afterwards, you’ll only have one debt bill to pay each month (your personal loan or balance transfer card, depending on the refinancing option you choose).

Why refinance your credit cards?

People typically refinance for two reasons:

1. Save money on interest. Credit card debt can come with high annual percentage rates (APRs). Credit card debt also compounds, making it harder to dig out of the hole. You could save money with a low-rate personal loan or even skip paying interest for a period of time with a 0% intro APR balance transfer card.

2. Cheaper monthly credit card payments. You could get cheaper monthly payments with a credit card refinancing loan when you qualify for lower rates or choose a long repayment term. Note that extending your loan term could help you get cheaper payments, but you’ll spend more money on interest in the long run.

Borrowers with excellent credit (760+) could save $1,750 and get out of debt six months sooner by refinancing $10,000 in credit card debt with a personal loan, according to a LendingTree study.

Although your outcome depends on your actual credit score, how much credit card debt you need to refinance and other details, odds are good that a personal loan will help you save.

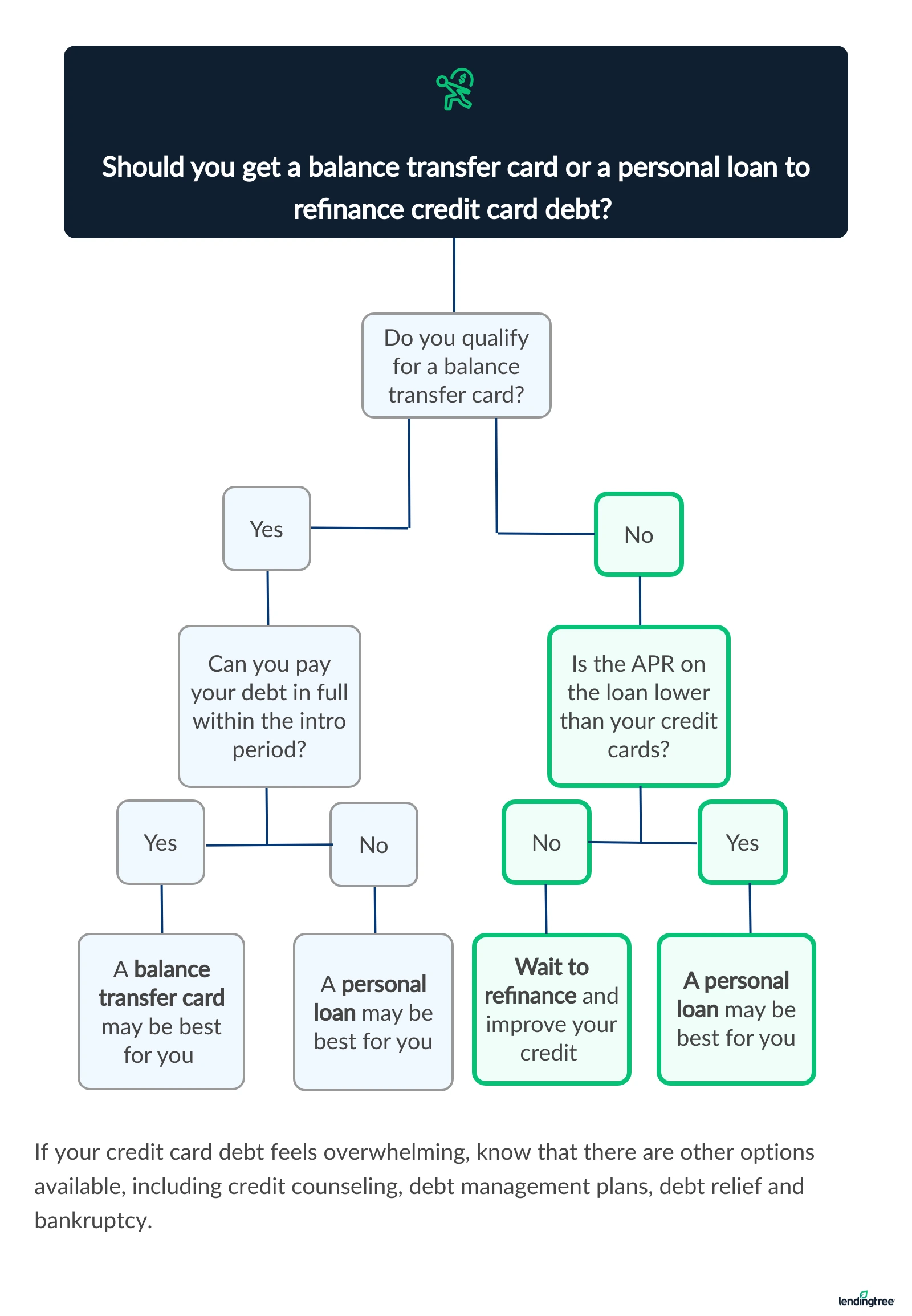

Should I refinance my credit cards?

- You have good or excellent credit. Personal loans tend to have lower rates than cards if you have excellent credit. Balance transfer cards usually require good credit.

- You have multiple credit card debts. Consolidating multiple payments into one can help you manage payments.

- You can afford the new monthly payment. Only refinance if your new monthly payment is affordable. If it’s not, consider alternatives and other ways to get out of debt.

- Your credit score is too low. It’s possible to find a debt consolidation loan for bad credit, but it may be hard to find a loan with lower rates than you’re already paying.

- The fees are too high. Both loans and cards can come with fees. If fees make it too expensive to refinance, consider other options.

- You have to significantly extend repayment. Choosing a long loan term to get a lower monthly payment can wipe out potential savings.

Best ways to refinance credit cards

0% intro APR balance transfer credit cards

- Best for: People with good credit and can pay off their debt within six to 21 months.

- How it works: Transfer your credit card balances to a new credit card, ideally with an introductory 0% APR period.

- APR: No interest charged during the intro 0% APR period, but your regular variable APR will apply to any leftover balance.

- Upfront fees: You’ll probably pay a balance transfer fee, typically from 3% to 5% of each balance transferred.

- Requirements: You’ll typically need good to excellent credit to qualify.

Personal loans

- Best for: People who don’t have excellent credit and want regular, fixed payments.

- How it works: Use a personal loan to pay off credit card balances, then pay off the loan in fixed monthly payments.

- APR: Your rate will depend on your creditworthiness. Typical rates are from 6% to 36%. See the current average personal loan rates by credit score.

- Upfront fees: Some lenders take out a one-time origination fee (typically between 1% to 10%) from your loan money before sending it to you.

- Requirements: Personal loan requirements vary by lender.

Choosing between a balance transfer card and a personal loan

When refinancing credit debt, a balance transfer card will save you the most money if you can pay your balance off within the card’s intro period. If you need at least a couple of years to tackle your debt, a personal loan is likely a better fit.

Best loans for credit card refinancing

| Lender | User rating | Best for | APR | See Results |

|---|---|---|---|---|

|

|

Overall credit card refinancing loans | 6.99% to 35.49% (with discounts) | ||

|

|

Runner-up, overall credit card refinancing loans | 7.74% to 35.99% (with discounts) | ||

|

|

Fast payment to credit card company | 6.99% to 35.99% | ||

|

|

No fees | 6.99% to 24.99% | ||

|

|

Lower credit scores | 8.99% to 35.99% |

Learn more about how we made our picks for the best credit card refinancing loans.

Credit card refinancing lenders at a glance

Best for: Overall credit card refinancing loans – SoFi

- APR (with discounts)

- 6.99% to 35.49%

Terms and conditions apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. To qualify, a borrower must be a U.S. citizen or other eligible status, be residing in the U.S., and meet SoFi’s underwriting requirements. Not all borrowers receive the lowest rate. Lowest rates reserved for the most creditworthy borrowers. If approved, your actual rate will be within the range of rates at the time of application and will depend on a variety of factors, including term of loan, evaluation of your creditworthiness, income, and other factors. If SoFi is unable to offer you a loan but matches you for a loan with a participating bank, then your rate may be outside the range of rates listed above. Rates and Terms are subject to change at any time without notice. SoFi Personal Loans can be used for any lawful personal, family, or household purposes and may not be used for post-secondary education expenses. Minimum loan amount is $5,000. The average of SoFi Personal Loans funded in 2025 was around $32K. Information current as of 07/20/26. SoFi Personal Loans originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org). See SoFi.com/legal for state-specific license details. See SoFi.com/eligibility for details and state restrictions. Fixed rates from 6.99% APR to 35.49% APR. APR reflect the 0.25% autopay interest rate discount and a 0.25% member rate discount. SoFi Platform personal loans are made either by SoFi Bank, N.A. or , Cross River Bank, a New Jersey State Chartered Commercial Bank, operating from its Delaware branch, Member FDIC, Equal Housing Lender. SoFi may receive compensation if you take out a loan originated by Cross River Bank. These rate ranges are current as of 07/20/26 and are subject to change without notice. Not all rates and amounts available in all states. See SoFi Personal Loan eligibility details at https://www.sofi.com/eligibilitycriteria/#eligibility-personal. Not all applicants qualify for the lowest rate. Lowest rates reserved for the most creditworthy borrowers. Your actual rate will be within the range of rates listed above and will depend on a variety of factors, including evaluation of your credit worthiness, income, and other factors. Loan amounts range from $5,000– $100,000. The APR is the cost of credit as a yearly rate and reflects both your interest rate and an origination fee of 9.99% of your loan amount for Cross River Bank originated loans which will be deducted from any loan proceeds you receive and for SoFi Bank originated loans have an origination fee of 0%-7%, will be deducted from any loan proceeds you receive. Autopay: The SoFi 0.25% autopay interest rate reduction requires you to agree to make monthly principal and interest payments by an automatic monthly deduction from a savings or checking account. The benefit will discontinue and be lost for periods in which you do not pay by automatic deduction from a savings or checking account. Autopay is not required to receive a loan from SoFi. Member Rate Discount: To be eligible for an additional 0.25% interest rate reduction on a Personal Loan, you must, within 31 days of loan funding, either (1) meet SoFi Plus eligibility criteria, (2) receive an Eligible Direct Deposit into a SoFi Checking or Savings account, or (3) receive at least $5,000 in Qualifying Deposits into a SoFi Checking or Savings account. You must continue to meet at least one of the above eligibility criteria every 31 days to maintain the discount. See the SoFi Plus terms for details on SoFi Plus subscription. For more details on Eligible Direct Deposit or Qualifying Deposits, please see https://www.sofi.com/legal/banking-rate-sheet. Once you become eligible during the initial period, the discount will be removed or reinstated depending on whether the criteria have been met. Each time your loan is re-amortized, your monthly payment amount will change based upon the interest rate that was in place. SoFi reserves the right to modify or terminate this offer at any time for unenrolled participants. You are not required to meet these criteria to be approved for a loan.

- Discount for direct payment to credit card companies

- No-cost financial consultation available by phone 24/7

- Same-day funding available

- Improve your approval odds with a co-borrower

- Origination fee is optional

- Not good for small credit card balances (minimum borrowing amount is $5,000+)

- Won’t qualify with bad credit

SoFi loans are fast and come with plenty of discount opportunities. Plus, when you get a loan with SoFi, you can also become a SoFi member. Membership comes with perks like a free financial planning session and discounts on flights, hotels and rental cars.

While many lenders let you use a personal loan to refinance credit card debt, SoFi offers a discount for it — just apply 50% or more of your loan money toward paying your credit card company directly and meet other terms and conditions.

SoFi’s origination fee is also optional, offering borrower flexibility and choice. Just ask for offers that do and don’t include the fee to find what makes sense for you.

SoFi’s minimum loan amount is $5,000. If you have more than that to refinance, then you’ll need to look for another lender. And while SoFi doesn’t require perfect credit, you must have a score of at least 600. That means no bad credit loans.

You’ll need to meet the requirements below to get a loan from SoFi:

- Age: Be the age of majority in your state (typically 18)

- Citizenship: Be a U.S. citizen, an eligible permanent resident or a non-permanent resident (a DACA recipient or asylum-seeker, for instance)

- Employment: Have a job or job offer with a start date within 90 days, or have regular income from another source

- Credit score: 600+

Best for: Runner-up, credit card refinancing loans – Upgrade

- APR (with discounts)

- 7.74% to 35.99%

- Lower rate for direct payment to credit card companies

- Fair credit OK

- Boost your approval odds with a co-borrower

- Discounts for auto pay and offering collateral

- Charges a one-time fee of 1.85% – 9.99% on every loan

- Accepts fair credit, but not bad credit

Like SoFi, Upgrade offers lower rates when you meet certain requirements, like using your loan to pay off your credit card company.

Upgrade also offers secured loans and accepts more than one type of collateral, including your car and permanent household fixtures. Collateral can make getting approved easier and may result in lower rates. It can be risky, though, as Upgrade could repossess your collateral if you fall too far behind.

Keep in mind that Upgrade charges a mandatory origination fee of 1.85% – 9.99% on every loan. You also may not qualify with bad credit, but including a co-borrower with excellent credit could help.

To qualify for a loan through Upgrade, you’ll have to meet the requirements below:

- Age: Be at least 18 years old (19 in some states)

- Citizenship: Be a U.S. citizen, permanent resident or live in the U.S. with a valid visa

- Administrative: Have a valid bank account and email address

- Credit score: 600+

Best for: Fast payment to credit card company – Best Egg

- APR

- 6.99% to 35.99%

- Fast direct payment to credit card companies

- Can check status of each individual credit card payoff via your Best Egg account

- Competitive rates for excellent credit

- Charges a one-time fee of 0.99% – 9.99% on every loan

- Can’t add a co-borrower to boost approval odds

Best Egg offers quick loans and could pay your credit card company in two to three business days. Best Egg also makes it easy to keep track of your loan with its online portal. There, you can see whether your loan has been applied to your credit card debts. This can help you avoid missing a payment during the refinancing process.

Approved borrowers can pay off up to 10 accounts at a time with their Best Egg loan. Plus, if you have good or excellent credit, you could qualify for some of the best starting rates on the market with Best Egg.

But Best Egg charges a one-time origination fee of 0.99% – 9.99% on every loan, which adds to the cost of refinancing.

You’ll need to meet the requirements below to qualify for a Best Egg loan:

- Age: Be of legal age to accept a loan in your state (usually 18)

- Citizenship: Be a U.S. citizen or permanent resident living in the U.S. and have a Social Security number

- Administrative: Have a personal checking account, email address and physical address

- Residency: Not live in the District of Columbia, Iowa, Vermont, West Virginia or U.S. territories

- Credit score: 620+

Best for: No fees – Discover

- APR

- 6.99% to 24.99%

- Direct payment to credit card company

- No fees whatsoever

- Repayment assistance options in case of financial hardship

- Need at least good credit

- Can’t use on Discover or Capital One credit cards

- No discount opportunities

Discover’s credit card refinancing loans can help you keep refinancing costs down with no fees and competitive rates. And if you hit a snag after refinancing and find it hard to keep up on payments, Discover’s repayment assistance program could help get you back on track.

With a minimum credit score of 720, Discover requires at least good credit (a 670 to 739 FICO Score). Plus, you can’t use a Discover loan to refinance a Discover or Capital One credit card.

You’ll need to meet these eligibility criteria to get a Discover loan:

- Age: Be at least 18

- Citizenship: Have a Social Security number

- Administrative: Have a physical address, email address and internet access

- Income: Minimum income of $40,000 (individually or as a household)

- Credit score: 720+

Best for: Lower credit scores – Prosper

- APR

- 8.99% to 35.99%

- Accepts bad credit scores

- No minimum income or credit history requirement

- Peer-to-peer lending can make approval easier

- Can’t send loan directly to credit card company

- Loan may not get funded by investors, even after Prosper approves you

Prosper is a peer-to-peer lender. Instead of funding loans itself, individual investors provide the money. Generally, peer-to-peer loans can be easier to get than a traditional personal loan.

If Prosper approves you, your loan request gets sent to investors who can choose to fund your loan (almost like GoFundMe). Investors then have 14 days to fund at least 70% of your loan. Otherwise, your loan request will be denied and you’ll have to apply again.

With this in mind, funding is possible within a day, and Prosper says most loans are fully funded within one to three business days. Still, it’s important to understand how the peer-to-peer process works in case it takes investors some time to pick up on your loan request.

To get a loan with Prosper, you must meet the following requirements:

- Age: Be 18 or older

- Administrative: Have a U.S. bank account and Social Security number

- Residency: Must live in an eligible U.S. state (Prosper operates in most states, with only a small number of states excluded)

- Credit score: 560+

Read more about how we made our picks for best loans to refinance credit cards.

See how much you can save by refinancing with a personal loan

How your credit score affects credit card refinancing rates

Credit card interest rates have hovered around 24% since March of 2025, according to LendingTree’s credit card rate tracker. Your rate may be different — credit card rates fluctuate with the market and depend on your credit — but this benchmark can be helpful for some napkin math.

The table below shows average LendingTree marketplace rates for debt consolidation loans

| Credit score range | Average APR |

|---|---|

| 800-850 (excellent) | 14.95% |

| 740-799 (very good) | 17.08% |

| 670-739 (good) | 22.56% |

| 580-669 (fair) | 27.35% |

| 300-579 (poor) | 30.45% |

Common mistakes to avoid when refinancing credit card debt

Refinancing credit card debt can be a smart way to save money, but it isn’t guaranteed. There are ways that refinancing could do you more harm than good. Be strategic and avoid these mistakes for the best results.

- Continuing to add to credit card debt. Refinancing is meant to help you take control over your debt, hopefully saving money in the process. If you keep using your credit cards, then you’ll owe on them plus your credit card refinancing loan.

- Focusing on the monthly payment, not overall interest. You could lower your monthly debt payment by choosing a long repayment term. However, you could end up paying more interest over the life of your loan.

- Missing credit card payments during the process. It can take a week or two for your loan to be applied to your credit cards. Until you know for sure that your credit card debt has been paid, continue making payments as normal. Missing a payment can cause your score to tumble.

- Closing your credit cards after refinancing. Unless you are having trouble not using your cards, you should leave them open after refinancing. Closing your credit cards could shorten the length of your credit history, which makes up 15% of your FICO Score.

- Forgetting about fees. Credit card refinancing costs money through interest and fees. Most balance transfer cards have a balance transfer fee and personal loans can have an origination fee.

Alternatives to credit card refinancing

Work out a payment plan

Best for anyone

Your credit card company may work with you if you reach out directly to tell them you’re having trouble making payments. Ask if your credit card company has a hardship program and if you can defer or temporarily lower your payments.

You can even ask to lower your APR permanently — 83% of people who asked for a lower credit card interest rate in the past year got one.

Use a debt repayment strategy

Best for manageable credit card debts

Pay off your credit card debts one by one with the debt snowball method (smallest debts first) or debt avalanche method (highest-interest debts first) while still making minimum payments on your other cards. Both methods are effective ways to get out of debt, so choose the strategy that works for you.

Debt management plan

Best for credit card debt you can’t afford to pay back

If you’re up at night worrying about how you’re going to pay off your credit card debt, know that there are resources that can help you become debt-free. The first step is to contact a nonprofit credit counselor who can help you create a debt management plan to help you get free from debt in three to five years.

How credit card refinancing loans impact your credit

A LendingTree study found that you could improve your credit score by more than 80 points

Hard credit pull

When you take out a loan, the lender will pull your credit. This can cause your credit score to temporarily drop, typically by up to five points. Credit pulls are part of FICO’s “new credit” credit scoring factor, which accounts for 10% of your FICO Score.

More diverse credit mix

When you replace your credit card debt with personal loan debt, this can improve your credit mix. This is one of five factors that affect your credit and is worth 10% of your FICO Score.

Regular payments

If refinancing for lower credit card payments helps you make your payments regularly, you’ll likely see your credit score improve. Payment history is worth 35% of your FICO Score, so catching up with payments can make a huge difference.

Credit utilization

Credit utilization measures how much of your revolving credit you’re using compared to how much you have available. Paying off your credit card debt with a personal loan, your credit utilization should go down, and lower is generally better. Credit utilization is part of FICO’s “amounts owed” category, which makes up 30% of your FICO Score.

How to compare credit card refinancing loans with LendingTree

You’d shop around for flights. Why not your loan? LendingTree makes it easy. Instead of applying to just one lender and hoping for a good rate, see multiple lenders compete for your business so you can choose the best offer.

Tell us what you need

Take two minutes to tell us who you are and how much money you need. It’s free, simple and secure.

Shop your offers

LendingTree users receive 11 personal loan offers on average. Compare yours side by side to get the best deal.

Get your money

Users save an average of $1,659 by choosing the offer with the lowest rate. Once you pick a lender and sign your paperwork, you could see money in your account in as little as 24 hours.

How we chose the best loans for credit card refinancing

We reviewed more than 40 lenders and loan marketplaces to determine the overall best five credit card refinancing loans. To make our list, companies must offer credit card consolidation loans with competitive APRs and direct payment to creditors.

From there, we assessed each lender or marketplace across four categories: eligibility and access; cost to borrow; loan terms and options; repayment support and tools.

According to our standardized rating system, the best credit card consolidation loans come from SoFi, Upgrade, Best Egg, Discover and Prosper.

Our categories

We assess how easy it is for people to qualify and apply. This includes state availability, soft-credit prequalification, membership requirements, funding speed and whether borrowers with less-than-excellent credit can get a loan.

We evaluate how affordable the loans are based on minimum and maximum APRs, loan fees and rate discounts. Lenders with unclear or potentially predatory costs receive lower scores.

We consider repayment term flexibility, loan amount ranges and whether options like secured loans, joint loans or direct-to-creditor payments are offered — plus whether the lender clearly communicates these options.

We evaluate borrower experience after funding: customer service access, hardship or forbearance programs, payment flexibility and digital tools like mobile apps or credit monitoring.

Our process

We gather data directly from companies through their websites, disclosures and direct communication with company representatives. Our editorial team verifies and updates information regularly. We value transparency and award less favorable scores when lenders obscure or omit details.

Our editorial team applies the same scoring model and standards to every lender. Lenders cannot pay to influence our ratings. Read more about our editorial guidelines.

Frequently asked questions

Credit card refinancing is the act of using a loan or another credit card to pay off your existing credit card debt.

Credit card refinancing can lower your current monthly payment and help you save money on interest with lower rates. Credit card refinancing also combines your multiple credit card bills into one, which can make budgeting easier.

Credit card refinancing and debt consolidation are similar. Credit card refinancing is just paying off your current credit card debt with a new credit card or loan, and then paying that off. Debt consolidation is using a loan or credit card to pay off multiple debts.

No, credit card refinancing isn’t bad. It can be a smart financial strategy when you use it to save money on high-interest debt. But if you’re refinancing credit card debt because you can’t afford your monthly payment, refinancing might not help. It doesn’t get rid of your debt, it just moves it to a loan or a balance transfer card.

If you have more debt than you feel you can manage, credit counseling is a free or low-cost way to get budgeting advice and in some cases, a special payment plan called a debt management plan.

Yes, it usually costs money to refinance your credit cards.

If you use a balance transfer card, you should expect a balance transfer fee of 3%-5% of every balance you transfer. This gets added to the debt you’re transferring. You could find a balance transfer card with no balance transfer fees, but the card might come with a shorter 0% APR period.

Personal loans can have origination fees that vary by lender. Some lenders don’t charge an origination fee. Others only charge them if you have bad credit. When origination fees apply, they typically range from 1%-10%. This fee is usually rolled into your loan balance, where it will be subject to interest.