Personal Loan Statistics: 2026

Americans hold $277 billion in personal loan debt across 26.4 million accounts. While this is far less than what Americans owe on mortgages, auto loans or credit cards, personal loan balances have grown steadily in recent years.

Explore how consumers use personal loans and how this form of borrowing affects household finances. These personal loan statistics provide a closer look at borrowing trends and debt levels.

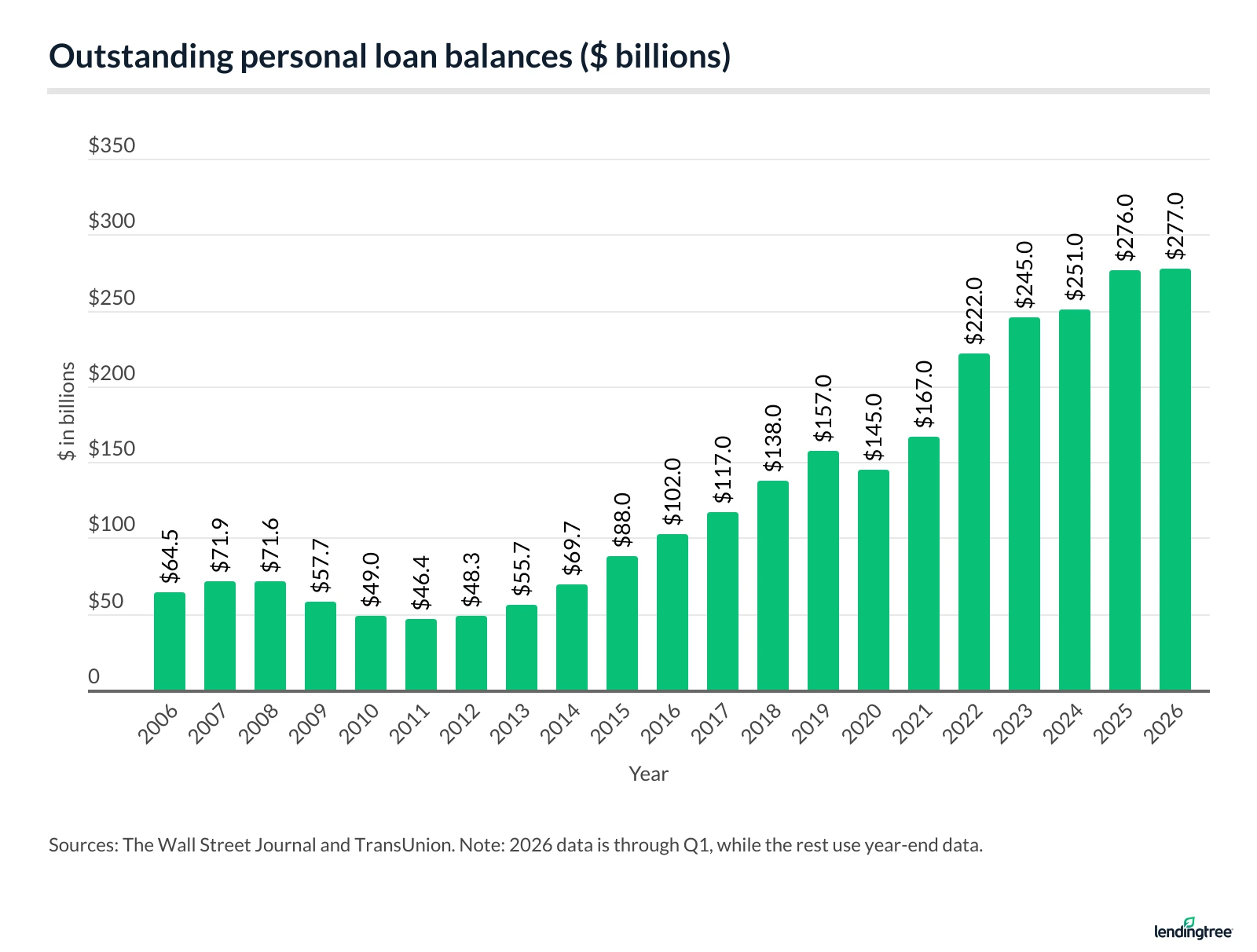

- Americans owe $277 billion in personal loan debt as of the first quarter of 2026, an increase of $1 billion from the previous quarter and $24 billion from a year earlier, representing a 9.5% year-over-year rise.

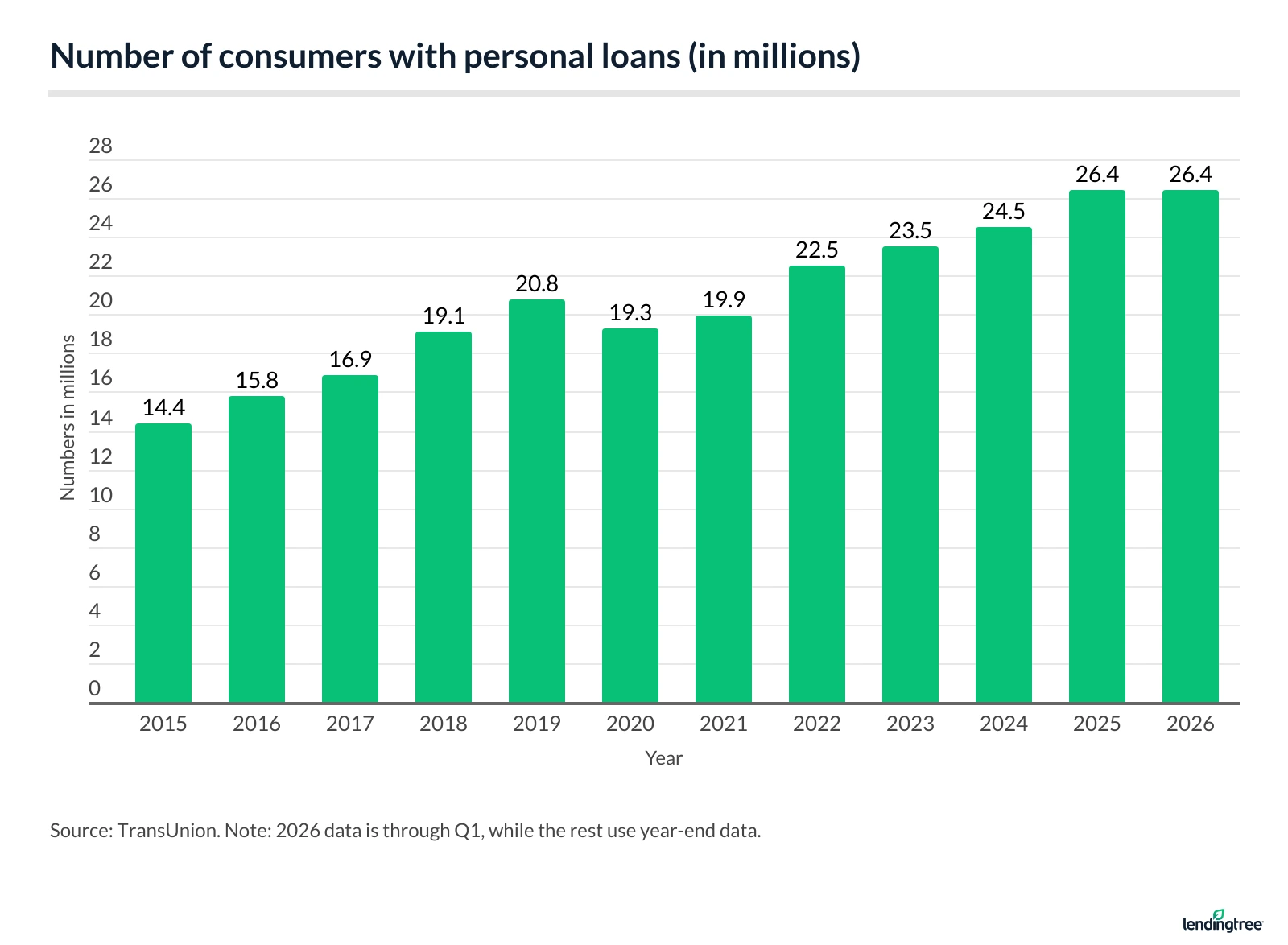

- 26.4 million Americans have a personal loan as of Q1 2026, up from 24.6 million a year earlier, a 7.3% year-over-year increase.

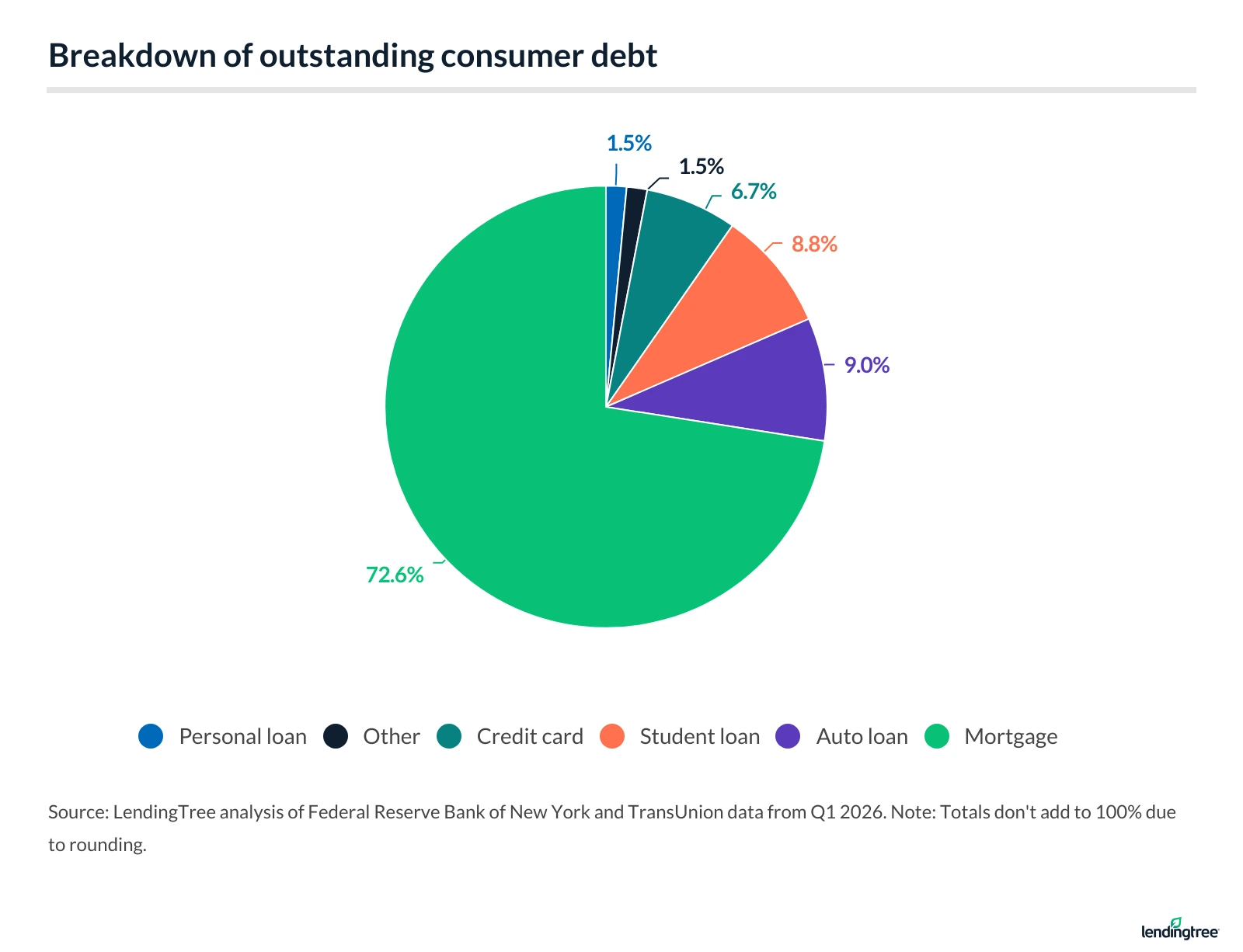

- Personal loan debt comprises 1.5% of all outstanding consumer debt as of Q1 2026. Personal loans account for 5.4% of nonhousing consumer debt. By comparison, Americans owe $1.252 trillion in credit card debt, equal to 6.7% of total outstanding consumer debt.

- The delinquency rate (60 days or more past due) for personal loans is 3.98% as of Q1 2026. This is up from 3.49% a year earlier.

- The average personal loan debt per borrower is $11,768 as of Q1 2026. The average debt per borrower was $11,631 a year earlier.

- More than half of borrowers (53.1%) take out a personal loan to consolidate debt or refinance credit cards. Paying everyday bills is the second-most common reported reason at 8.4%.

Americans owe $277 billion in personal loan debt

Personal loan borrowers owe $277 billion in debt as of Q1 2026, up $1 billion from the previous quarter, reaching the highest level in more than 20 years of available data. That is a 9.5% increase from Q1 2025, when Americans owed $253 billion.

The chart below shows how total personal loan debt has changed over time.

26.4 million Americans have a personal loan

As of Q1 2026, 26.4 million Americans have a personal loan, up from 24.6 million in Q1 2025.

The number of personal loan borrowers decreased during the coronavirus pandemic, falling from a then-high of 20.8 million in Q4 2019 to 18.7 million in Q2 2021. Borrower counts then rose for six consecutive quarters before slipping slightly from 22.5 million in Q4 2022 to 22.4 million in Q1 2023. Since then, the number of borrowers has climbed to more than 26 million.

The chart below shows the number of consumers with personal loans since 2015:

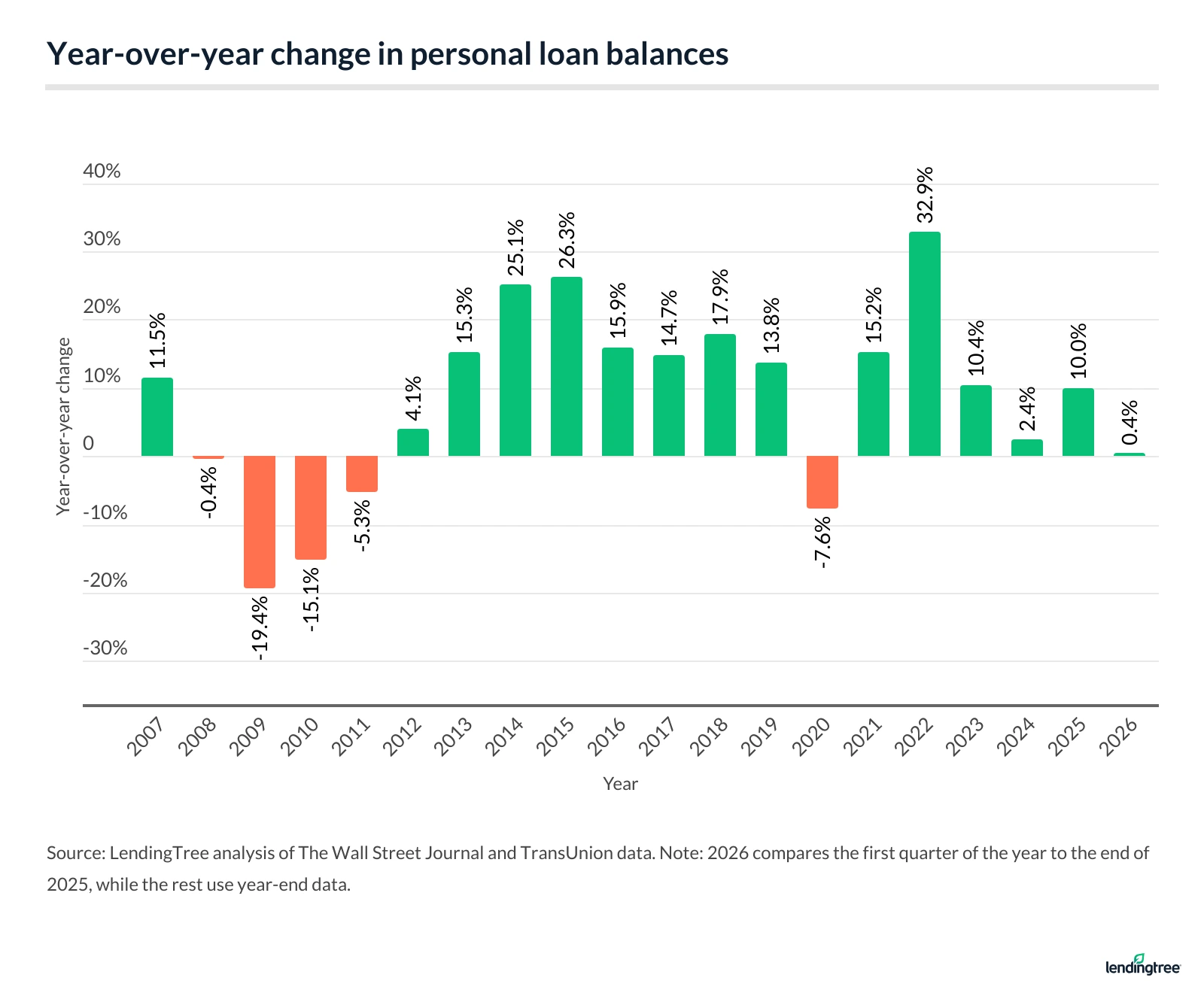

Personal loan growth returns after dropping early in the pandemic

The nearly decade-long increase in personal loan debt ended in 2020 as the pandemic disrupted borrowing trends. Personal loan balances fell 7.6% in 2020, marking the first decline since 2011.

However, personal loan debt balances rose 15.2% in 2021, reversing the previous year’s decline. As of Q1 2026, balances were 0.4% higher than in Q4 2025.

The chart below shows annual changes in personal loan debt since 2007:

Personal loans account for 1.5% of consumer debt

Personal loans account for 1.5% of outstanding consumer debt in the U.S., despite significant growth over the past decade.

By comparison, Americans owe $1.252 trillion in credit card debt, representing 6.7% of outstanding consumer debt.

Excluding mortgage debt, personal loans account for 5.4% of nonhousing consumer debt.

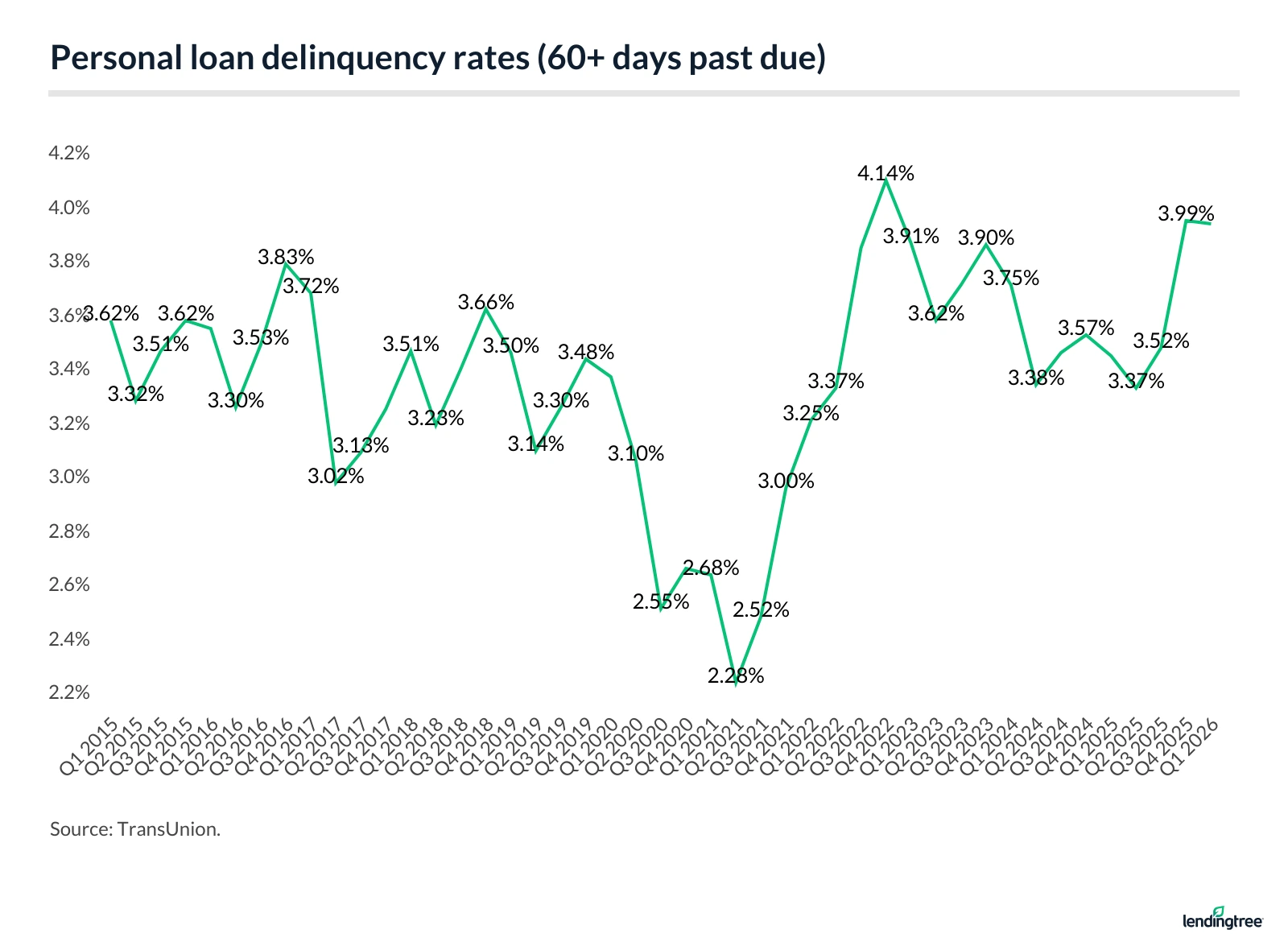

3.98% of personal loan accounts are 60 days or more past due

An estimated 3.98% of personal loan accounts are 60 days or more past due as of Q1 2026, up from 3.49% in Q1 2025 and 3.75% in Q1 2024.

The personal loan delinquency rate remains higher than those for other major forms of consumer debt, including mortgages (1.57%), auto loans (1.57%) and credit cards (2.53%). (Note that credit card delinquencies are tracked at 90 days or more past due.)

For historical context, the 30-day delinquency rate for consumer loans was 4.77% in 2009, the year the Great Recession ended.

Average personal loan debt per borrower is over $11,700; APRs vary by credit score

The average personal loan debt per borrower is $11,768 as of Q1 2026. This compares with:

- $11,631 in Q1 2025

- $11,829 in Q1 2024

- $11,281 in Q1 2023

Borrowers with credit scores of 680 or higher typically qualify for personal loan APRs that are competitive with, and often lower than, credit card rates.

The average APR on new credit card offers is 23.79% as of June 2026, with minimum and maximum rates between 20.19% and 27.40%. As the table below shows, personal loan APRs generally rise as borrower credit scores decline.

Personal loan statistics by borrower credit score

| Credit score range | Avg. APR | Avg. loan amount |

|---|---|---|

| 720+ | 14.80% | $20,599 |

| 680-719 | 22.98% | $18,309 |

| 660-679 | 26.66% | $15,535 |

| 640-659 | 28.92% | $13,457 |

| 620-639 | 30.22% | $12,425 |

| 580-619 | 31.22% | $11,853 |

| 560-579 | 32.44% | $10,681 |

| Less than 560 | 30.62% | $11,518 |

Subprime borrowers generally face the highest APRs and may have fewer borrowing options available.

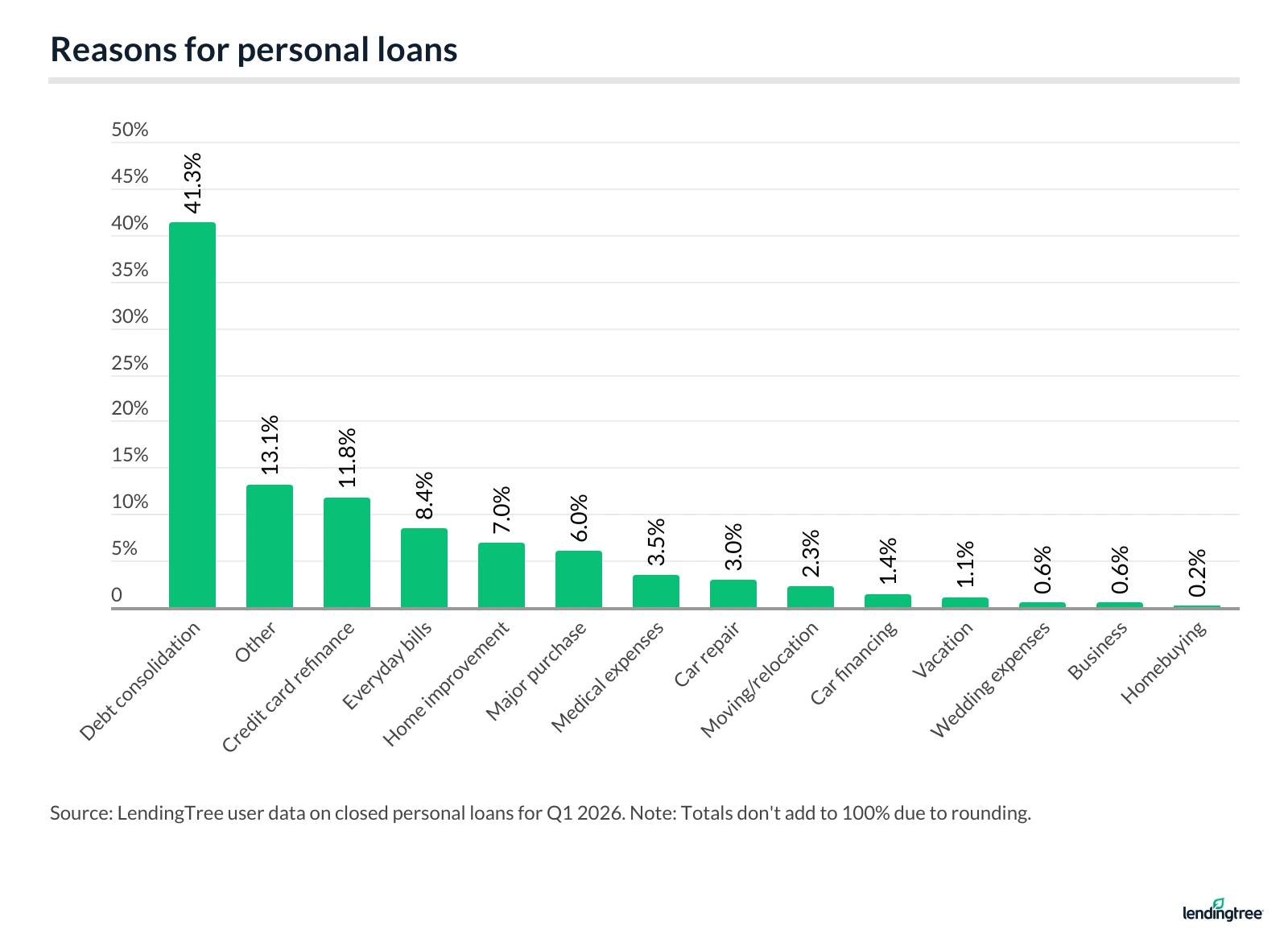

Consumers often borrow personal loans to pay down debt

More than half (53.1%) of LendingTree users who take out personal loans report using the funds to pay down existing debt, including 41.3% for debt consolidation and 11.8% to refinance credit card balances.

The next most common reasons for obtaining a personal loan are covering everyday expenses (8.4%) and financing home improvements (7.0%).

These findings highlight the role personal loans can play in debt management and household budgeting.

Personal loans can help borrowers consolidate higher-interest debt or meet other financial needs, but outcomes depend on factors such as borrowing costs, repayment terms and a borrower’s ability to manage the debt responsibly.

Expect personal loan debt to keep growing

Personal loan debt has continued to grow in recent years, and current trends suggest further increases are possible. Rising credit card balances may contribute to continued demand for personal loans, particularly among borrowers seeking lower-cost ways to manage existing debt.

Many borrowers use personal loans to consolidate credit card balances, and these loans can reduce borrowing costs when they offer lower interest rates than existing debt. If you have really good credit, a 0% balance transfer credit card may be a more cost-effective option for consolidating certain debts. Personal loans, however, may be a better fit for some borrowers depending on loan terms, balances and repayment timelines.

Interest rate trends may differ from borrowing trends. LendingTree data shows personal loan rates have remained relatively stable over the past year, even as the Fed cut rates multiple times in late 2025. If the Federal Reserve keeps rates unchanged in the near term, personal loan rates may remain relatively stable as well.

Personal loans are not used exclusively by consumers facing financial hardship. Many people use them to finance home improvements, weddings, vacations and other large expenses. Demand for personal loans is influenced by a range of factors, including consumer confidence, borrowing costs and household spending needs.

Although future borrowing trends will depend on economic conditions and lending standards, personal loan balances could continue to rise if consumer demand remains strong. Borrowers who use personal loans strategically — particularly for debt consolidation — may benefit from lower borrowing costs and more structured repayment terms.

Sources

- TransUnion

- The Wall Street Journal

- Federal Reserve Bank of New York

- LendingTree

Get personal loan offers from up to 5 lenders in minutes