Personal Loan Use for Everyday Bills Climbs, Led by Gen Z and Deep Subprime Borrowers

Personal loans are often used to fund large purchases, home improvement projects and even lavish vacations. But more Americans are turning to them just to get by.

Covering everyday bills is among the most common reasons borrowers apply for personal loans, with younger borrowers and those with lower credit scores relying on them most heavily. This study examines the growing dependence on personal loans for basic expenses, including when, where and among whom the trend is strongest.

- More Americans are seeking personal loans to help with everyday bills. Everyday bills account for 8.2% of personal loan requests on the LendingTree platform — the fourth most popular reason. That’s up significantly from 3.4% in our 2023 report. Borrowers applying for this reason request an average of $4,317 and have an average credit score of 574.

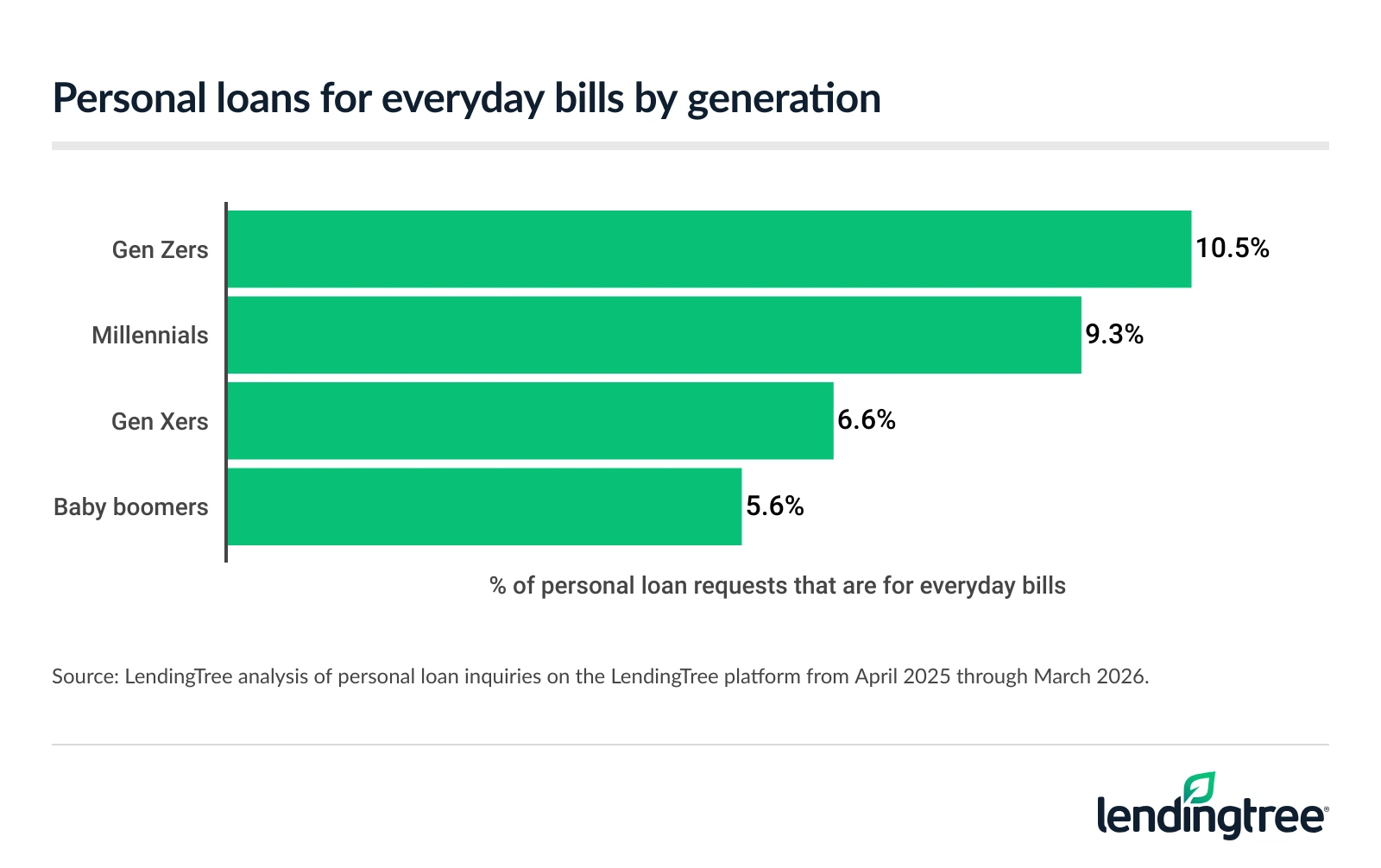

- Younger borrowers are the most likely to seek personal loans for everyday bills. 10.5% of personal loan requests among Gen Zers are for everyday bills, compared with 9.3% among millennials, 6.6% among Gen Xers and 5.6% among baby boomers.

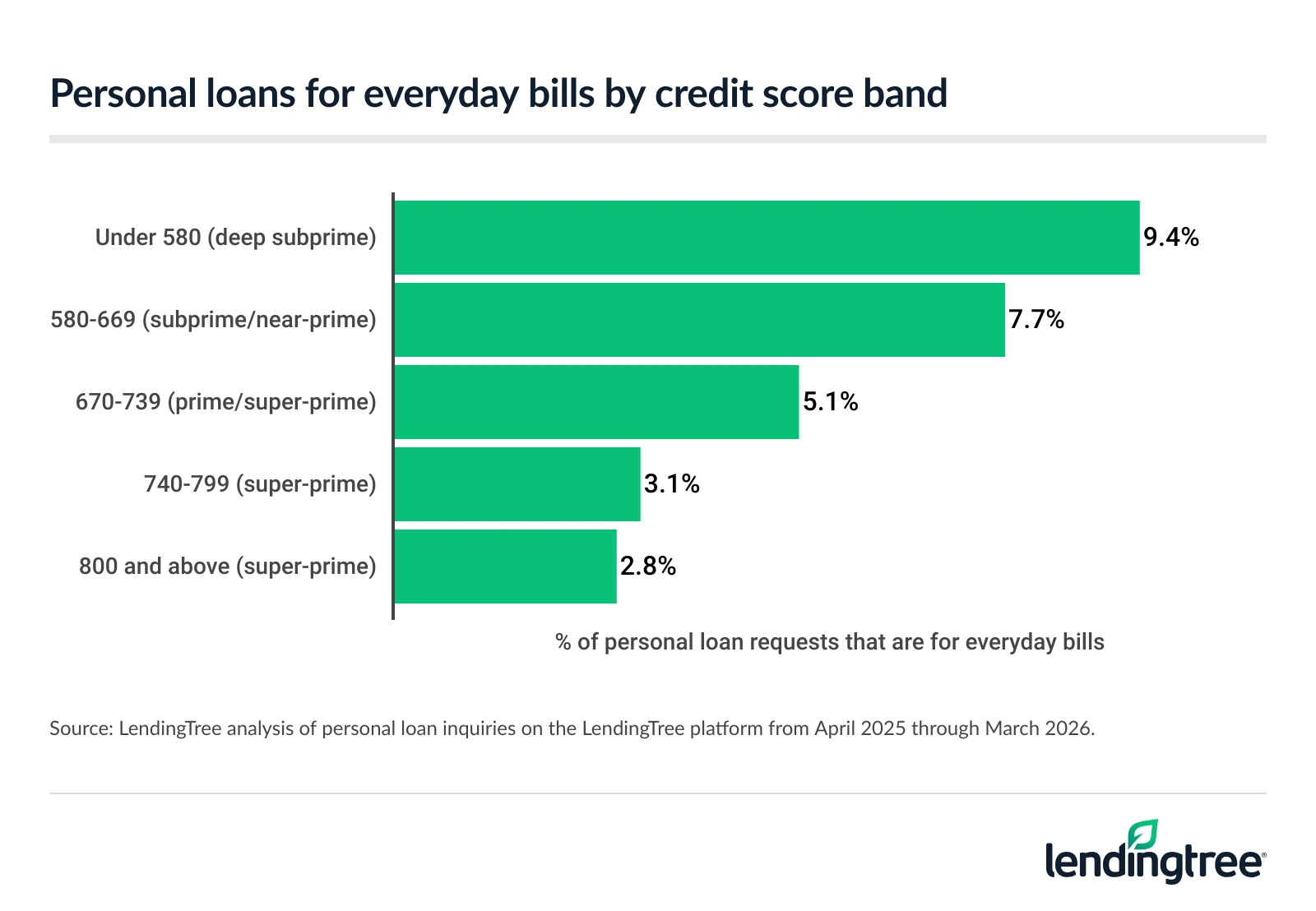

- Low-credit borrowers are far more likely than high-credit ones to seek personal loans for everyday bills. 9.4% of requests from deep subprime borrowers with credit scores below 580 are for everyday bills, versus 2.8% among borrowers with super-prime scores of 800 and above. Overall, 57.5% of requests for personal loans for everyday bills are made by borrowers with credit scores below 580.

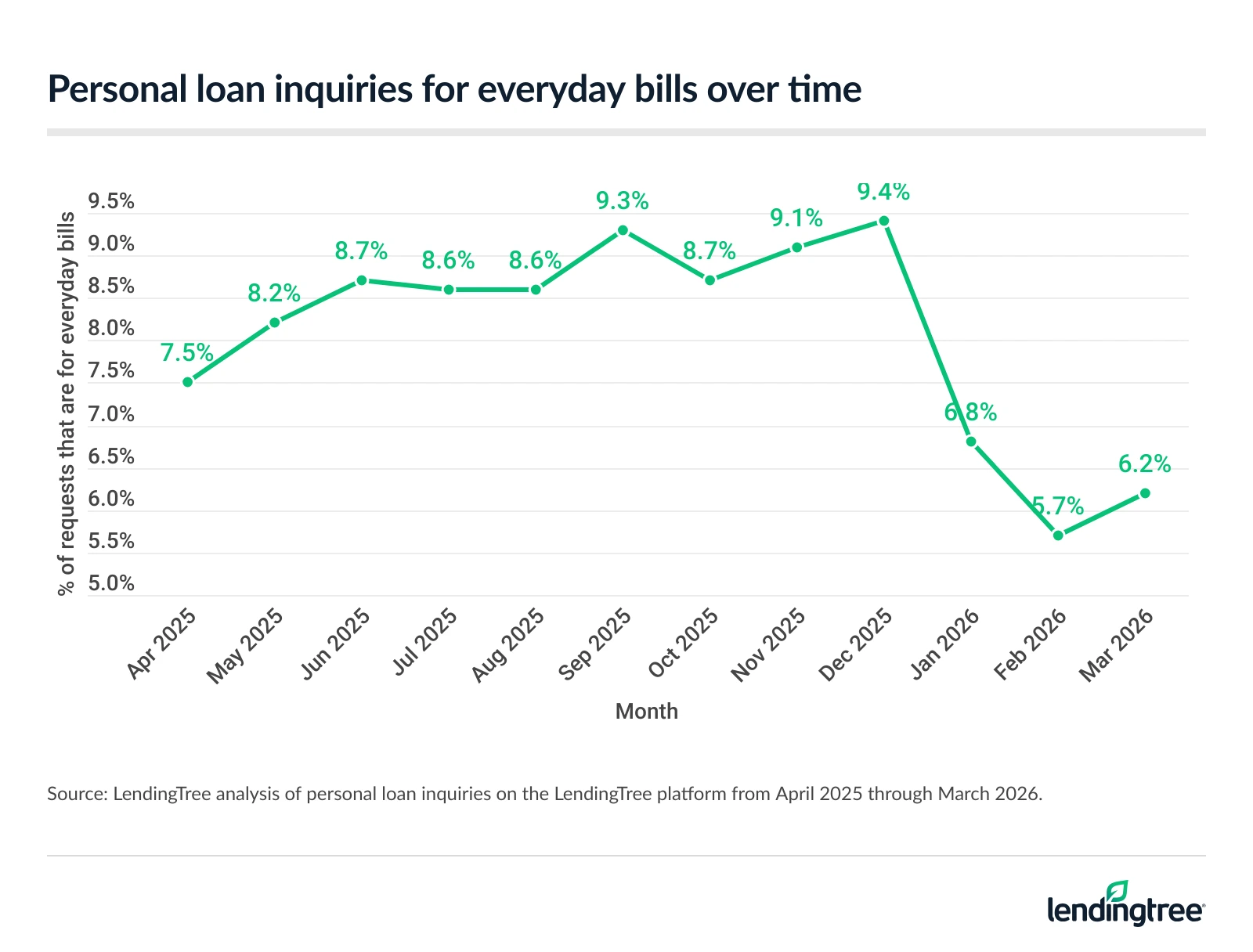

- In the past year, personal loan requests for everyday bills peaked in December, highlighting a potential link to holiday shopping. The share of personal loan requests for everyday bills rose from 7.5% in April 2025 to 9.4% in December, before dropping to 5.7% in February 2026 and ticking up to 6.2% in March.

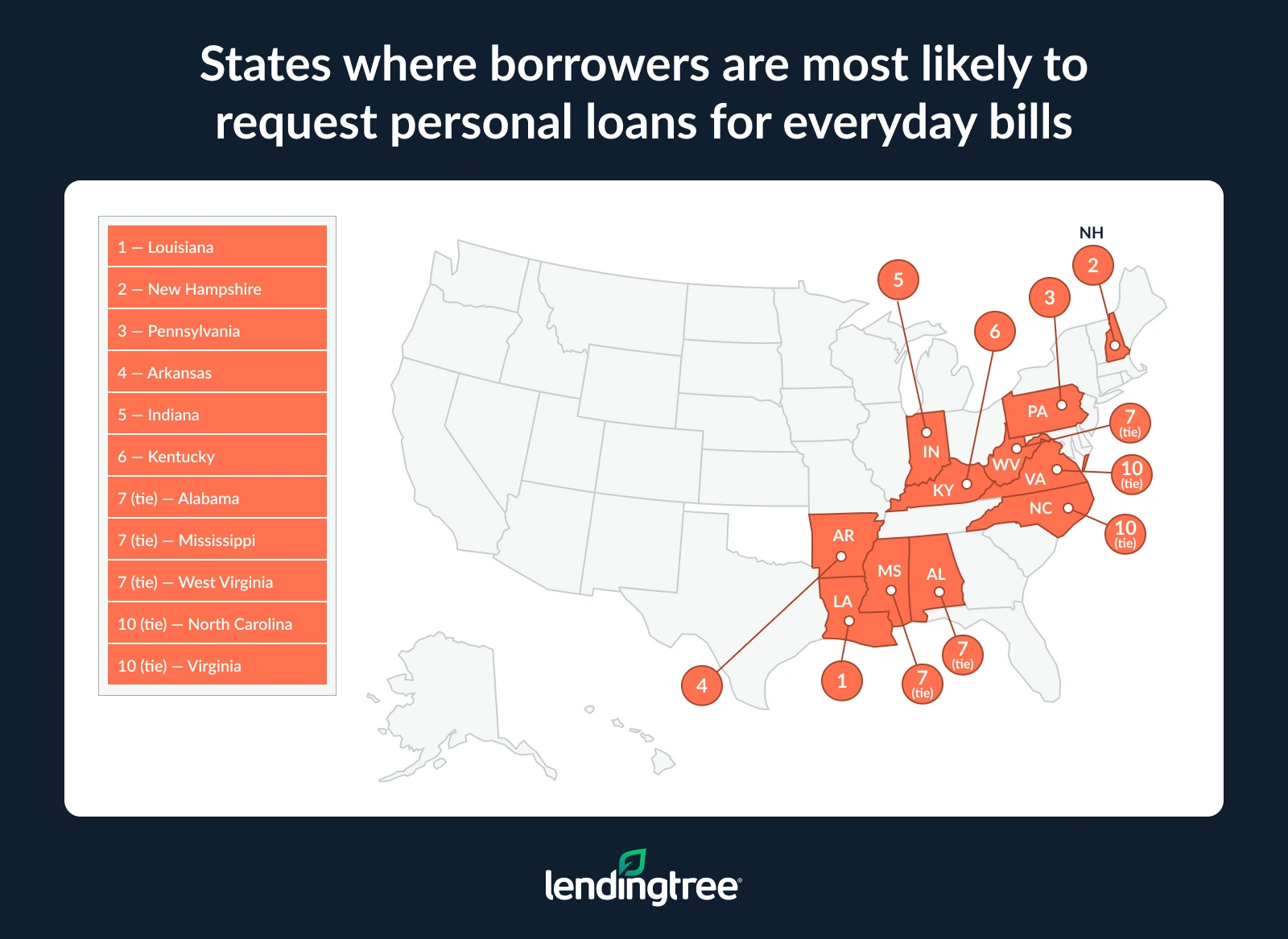

- Borrowers in some states are more likely to request a personal loan for everyday expenses. Louisiana has the highest share of personal loan requests for everyday bills at 10.0%, followed by New Hampshire (9.8%) and Pennsylvania (9.7%). Meanwhile, Nevada and Oregon tie for the lowest at 6.2%, followed by Massachusetts (6.5%).

Everyday bills are one of the top reasons Americans request personal loans

American consumers are increasingly turning to personal loans to keep up with routine expenses. Nearly 1 in 10 (8.2%) personal loan inquiries on the LendingTree platform are for everyday bills — the fourth most common reason for borrowing.

That share has more than doubled since 2023, when only 3.4% of borrowers needed the funds for regular bills — the 10th most common reason. And while other top personal loan uses — debt consolidation and credit card refinancing — are also tied to managing bills, this surge is among borrowers depending on personal loans for immediate, essential expenses rather than restructuring existing debt.

Borrowers using personal loans for everyday bills tend to request smaller amounts, averaging $4,317 — the second-lowest across loan purposes, after car repair ($3,967). They also have lower credit scores, averaging 574. That compares with an average FICO Score of 713 among U.S. consumers, according to Experian.

“When more borrowers turn to personal loans just to cover everyday bills, it’s a sign that budgets are stretched thin and that many are relying on credit to bridge routine shortfalls, not just emergencies,” says Matt Schulz, LendingTree chief consumer finance analyst.

“Unfortunately, it’s the reality for many Americans. If you’re borrowing to pay essential bills, it becomes extremely difficult to get ahead financially. It means there’s no extra money to put toward emergency funds, retirement savings or any other big financial goals.”

Younger borrowers are most likely to turn to personal loans for basic expenses

Younger consumers are far more likely to rely on personal loans for routine bills than older consumers. On the LendingTree platform, 10.5% of personal loan inquiries among Gen Z borrowers ages 18 to 29 are for everyday expenses — higher than millennials ages 30 to 45 (9.3%), Gen Xers ages 46 to 61 (6.6%) and baby boomers ages 62 to 80 (5.6%).

Today’s consumers are navigating a challenging mix of persistent inflation, elevated interest rates and ongoing housing affordability issues. Additionally, wages haven’t kept pace with the rising cost of essentials. These pressures disproportionately affect younger borrowers uniquely, as many are also managing student loan debt and are at earlier life and career stages than older adults.

“Younger borrowers are coming of age in a much tougher financial environment, where essentials like housing, transportation and insurance are taking up a bigger share of income than they did for prior generations,” says Schulz, also the author of “Ask Questions, Save Money, Make More: How to Take Control of Your Financial Life.”

“At the same time, many haven’t had the chance to build savings cushions yet, so when everyday costs spike, they may turn to credit to fill the gap,” Schulz says. “Previous generations certainly faced challenges early on, but costs were generally lower relative to income, making it a bit easier to stay afloat without borrowing for basic needs.”

Consumers with lower credit scores are far more likely to borrow for basic needs

Consumers with lower credit scores are much more likely to rely on personal loans for everyday bills than those with stronger credit. Nearly 1 in 10 (9.4%) requests from deep subprime borrowers — those with credit scores below 580 — are for routine expenses, more than three times the share among super-prime borrowers with scores of 800 or higher (2.8%).

Looking at the full borrower mix, 57.5% of personal loan requests for everyday bills come from those with credit scores below 580.

“This gap highlights the financial vulnerability of many lower-credit households,” Schulz says. “They’re far more likely to be living paycheck to paycheck with little to no safety net. When an essential expense hits, they often don’t have savings or access to low-cost credit, so personal loans become a last resort rather than a strategic choice.”

Lower-credit borrowers often turn to credit options with higher interest rates, shorter repayment periods, fees and other unfavorable terms, such as secured credit cards, payday loans and buy now, pay later (BNPL) services.

As a result, relying on credit for basic needs can become a difficult cycle to break, making it harder to pay down debt while still covering everyday expenses. This dynamic can also affect younger borrowers, who are more likely to have lower credit scores because they’ve had less time to build credit.

Demand for everyday bill loans peaks in December

Over the past year, personal loan requests for everyday bills reached their highest level in December, with 9.4% of inquiries for routine expenses. The spike suggests a connection to the holiday season, when gift shopping and travel can stretch already tight budgets — or leave borrowers playing catch-up on bills in the new year.

Notably, personal loan requests for everyday bills rose from 7.5% in April 2025 to 9.3% in September, coinciding with the back-to-school and back-to-college seasons. After a slight dip in October, demand climbed again — to the December peak — and then dropped to 5.7% in February 2026. Requests then ticked up slightly to 6.2% in March.

Major spending moments — from winter holidays to back-to-school season — tend to put added pressure on household finances, making it more likely that some borrowers turn to loans just to keep up with everyday bills. According to the National Retail Federation, consumers in 2025 budgeted an average of $890 for winter holiday gifts and celebrations.

“It’s no surprise that borrowing and spending spike during the holidays,” Schulz says. “But it makes for a really challenging start to the year. It means taking on additional debt at a time when many families are already financially stretched.”

Borrowers in some states are far more likely to use personal loans for everyday expenses

Consumers in some states rely heavily on personal loans for essential bills, reflecting uneven financial pressures across the country. Louisiana leads the way, with 10.0% of personal loan requests seeking funds for everyday bills, followed by New Hampshire (9.8%) and Pennsylvania (9.7%).

“That hints at greater financial strain for families in those states — whether that’s due to lower incomes, higher relative costs or less access to savings,” Schulz says. “It might also signal that they don’t have any other good options.”

Louisiana has a relatively low cost of living, mostly connected to lower-than-average housing costs. However, residents tend to have both lower median household incomes ($60,756 versus $80,734 nationally) and lower average credit scores (686 versus 713), suggesting budgets may still be stretched despite cheaper home prices and rents.

In New Hampshire, the pressure likely comes from the opposite direction. Higher living costs — especially for housing — can squeeze monthly budgets, helping explain the elevated share of borrowers turning to loans for routine expenses. Pennsylvania falls somewhere in between: While overall costs are moderate, higher utility and transportation expenses, paired with slightly lower median incomes ($77,971 versus $80,734), may be adding to financial strain.

Where borrowers are least likely to use personal loans for everyday expenses

On the other end of the spectrum, Nevada and Oregon tie for the lowest share of personal loan requests for everyday bills (6.2%), followed by Massachusetts (6.5%).

Interestingly, consumers in Oregon and Massachusetts face higher costs of living — particularly in Massachusetts, which ranks among the most expensive in the country. However, they also tend to have higher household incomes, higher home values and stronger average credit profiles than those in many other states.

That combination may give borrowers more financial flexibility when money gets tight. Instead of relying on personal loans, they may have access to other options, such as tapping home equity or qualifying for lower-cost credit. In Nevada, the lack of a state income tax may also provide some additional breathing room for household budgets.

Full rankings: States where borrowers are most likely to request personal loans for everyday bills

| Rank | State | % of personal loan requests for everyday bills | Avg. requested loan size | Avg. credit score |

|---|---|---|---|---|

| 1 | Louisiana | 10.0% | $3,340 | 580 |

| 2 | New Hampshire | 9.8% | $4,938 | 568 |

| 3 | Pennsylvania | 9.7% | $4,492 | 571 |

| 4 | Arkansas | 9.6% | $3,961 | 571 |

| 5 | Indiana | 9.3% | $3,897 | 569 |

| 6 | Kentucky | 9.2% | $3,588 | 571 |

| 7 | Alabama | 9.1% | $3,509 | 569 |

| 7 | Mississippi | 9.1% | $3,373 | 572 |

| 7 | West Virginia | 9.1% | $4,415 | 568 |

| 10 | North Carolina | 9.0% | $3,992 | 573 |

| 10 | Virginia | 9.0% | $4,184 | 575 |

| 12 | Oklahoma | 8.8% | $3,727 | 572 |

| 13 | Iowa | 8.7% | $4,339 | 572 |

| 13 | Illinois | 8.7% | $4,384 | 576 |

| 13 | Arizona | 8.7% | $4,117 | 571 |

| 13 | Ohio | 8.7% | $3,777 | 570 |

| 13 | South Dakota | 8.7% | $4,574 | 578 |

| 13 | Texas | 8.7% | $3,850 | 570 |

| 19 | Tennessee | 8.5% | $3,759 | 571 |

| 20 | Washington | 8.4% | $4,938 | 579 |

| 20 | District of Columbia | 8.4% | $4,930 | 583 |

| 22 | Connecticut | 8.3% | $5,629 | 579 |

| 23 | Missouri | 8.2% | $3,660 | 575 |

| 24 | Michigan | 8.1% | $4,270 | 572 |

| 24 | Vermont | 8.1% | $5,663 | 580 |

| 26 | North Dakota | 8.0% | $5,240 | 577 |

| 27 | Maryland | 7.9% | $5,236 | 573 |

| 27 | Wisconsin | 7.9% | $4,288 | 575 |

| 27 | Kansas | 7.9% | $3,958 | 574 |

| 30 | South Carolina | 7.8% | $3,803 | 570 |

| 30 | Nebraska | 7.8% | $4,386 | 577 |

| 30 | New Mexico | 7.8% | $4,242 | 573 |

| 33 | Delaware | 7.7% | $4,141 | 573 |

| 34 | Georgia | 7.6% | $4,325 | 572 |

| 34 | Florida | 7.6% | $4,388 | 572 |

| 36 | New York | 7.4% | $6,388 | 584 |

| 37 | Hawaii | 7.3% | $6,540 | 583 |

| 37 | Wyoming | 7.3% | $4,897 | 574 |

| 39 | Montana | 7.2% | $5,143 | 582 |

| 39 | Alaska | 7.2% | $5,282 | 586 |

| 41 | Maine | 7.0% | $5,099 | 578 |

| 42 | Colorado | 6.9% | $5,015 | 582 |

| 43 | New Jersey | 6.8% | $5,831 | 578 |

| 43 | Idaho | 6.8% | $4,092 | 574 |

| 43 | Minnesota | 6.8% | $4,799 | 585 |

| 46 | Rhode Island | 6.6% | $4,942 | 580 |

| 46 | Utah | 6.6% | $4,271 | 575 |

| 46 | California | 6.6% | $5,250 | 582 |

| 49 | Massachusetts | 6.5% | $6,072 | 583 |

| 50 | Oregon | 6.2% | $4,249 | 578 |

| 50 | Nevada | 6.2% | $4,702 | 573 |

Managing everyday bills when financially strained: Top expert tips

Handling routine bills can be a challenge in today’s economic climate, especially as everyday costs continue to rise. While debt — including personal loans — can be a useful tool to bridge short-term gaps, it’s not the only option. A mix of smart borrowing, cost-cutting and proactive communication can help you stay on track, even when finances feel tight.

- Trim and renegotiate recurring bills. Review subscriptions, utilities, insurance premiums and other monthly expenses, looking for opportunities to cancel, downgrade or negotiate. Adjusting payment due dates can also improve cash flow, and many utilities, landlords and service providers offer flexible schedules or payment plans.

- Boost short-term cash flow. Picking up extra hours, freelance work or selling unused items can provide a temporary cushion without adding new debt.

- Lower your interest rates where you can. “A 0% balance transfer credit card would be about the best possible weapon in this battle, but you need pretty good credit to get one. If you can’t, a low-interest personal loan can work, too,” Schulz says. “You can even call your card issuer and ask for a lower interest rate. Saving a few dollars a month on these other payments can make a real difference.”

- Communicate with lenders early. “If you can’t make a payment, let your lender know as soon as possible,” Schulz advises. “Most lenders have hardship programs that allow them to offer temporary breaks such as waived fees, delayed payments, lower APRs and more to those going through a temporary rough patch.”

- Shop around before borrowing. Rates, fees and terms can vary widely among lenders, so compare multiple offers before borrowing. “If you don’t take the time to comparison shop, there’s a good chance you’ll pay more than necessary for the loan,” Schulz warns. Using a personal loan calculator can also help you estimate how changes in loan amount, term or rate may affect your monthly payment.

Methodology

LendingTree researchers reviewed millions of online forms filled out by people inquiring about personal loans on the LendingTree platform from April 2025 through March 2026.

We defined generations as the following ages in 2026:

- Generation Z: 18 to 29

- Millennials: 30 to 45

- Generation X: 46 to 61

- Baby boomers: 62 to 80

Get personal loan offers from up to 5 lenders in minutes