How To Choose the Right Type of Business Entity

A business entity is the legal structure of your business. It affects how you’re taxed, your personal liability and how your company ownership works. Choosing the right one can help you protect your assets and support your business as it grows.

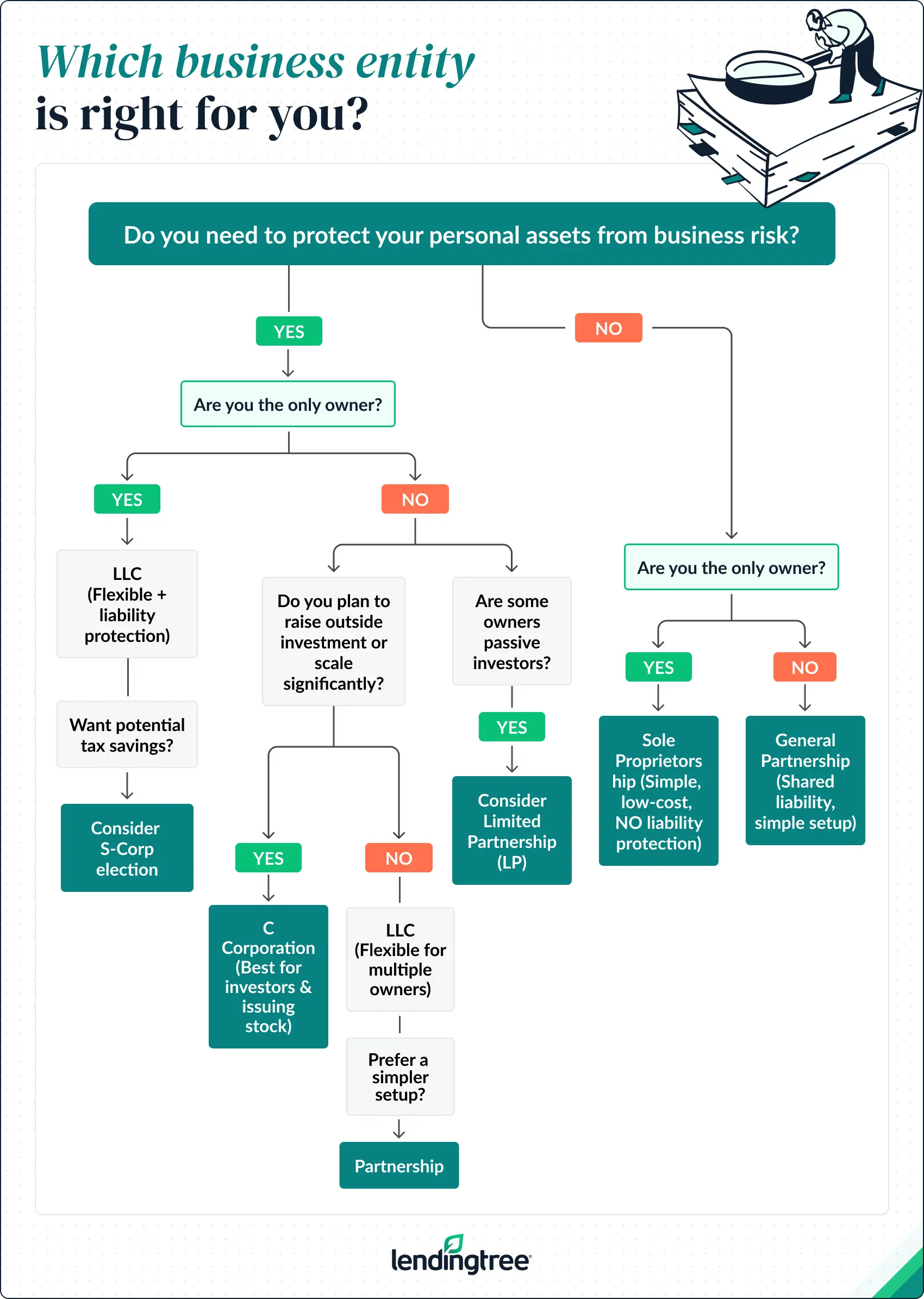

The right business entity depends on your goals, risk tolerance and how you plan to run your business.

- LLCs are a popular choice for small businesses because they balance liability protection and flexibility.

- Sole proprietorships are the simplest to start but offer no liability protection.

- Corporations are best for raising investors or scaling.

Compare business entity types

When choosing a business entity, most small business owners consider the following common structures:

| Entity type | Best for | Liability protection | Tax treatment |

|---|---|---|---|

| Sole proprietorship | Solo owners, low-risk businesses | None | Personal tax |

| Partnership | Businesses with multiple owners | ⚠️Varies by type | Personal tax or self-employment tax (except for limited liability partnership) |

| Limited liability company (LLC) | Small businesses seeking flexibility | Yes | Self-employment tax, personal tax or corporate tax |

| C corporation | Businesses raising investors or going public | Yes | Corporate tax |

| S corporation | Owners seeking tax savings | Yes | Personal tax |

| Nonprofit corporation | Charitable or mission-driven organizations | Yes | Tax exempt, but corporate profits can’t be distributed |

| Benefit corporation | Businesses balancing profit and purpose | Yes | Corporate tax |

Types of business entities

Now that you’ve compared your options, here’s a closer look at each type of business entity, including how they work and who they’re best for.

Sole proprietorship

A business owned and operated by one person with no legal separation between the owner and the business.

A sole proprietorship is the simplest business structure and often doesn’t require formal registration if you operate under your own name. However, because there’s no separation between personal and business assets, you’re personally responsible for any debts or legal issues.

Best for: Low-risk businesses or testing a business idea

- Pro: Simple to start and you maintain full control

- Con: No liability protection

Partnership

A business owned by two or more people who share profits, responsibilities and, in some cases, liability.

Partnerships can take several forms, including limited partnerships and limited liability partnerships. Liability and tax treatment vary by type, but most partnerships pass income through to the owners’ personal tax returns.

Best for: Businesses with multiple owners

- Pro: Simple to establish and operate

- Con: Owners may be personally liable, depending on the structure

Limited liability company (LLC)

A flexible business structure that separates your personal assets from your business liabilities.

LLCs are popular because they protect your personal assets while allowing you to choose how you’re taxed. Profits typically pass through to your personal tax return, but you can elect corporate taxation. Requirements and fees vary by state. You can use a secretary of state business search to look up registration requirements where you operate.

Best for: Small business owners who want liability protection with flexible taxes

- Pro: Liability protection with flexible tax options

- Con: Ongoing fees and administrative requirements

C corporation

A separate legal entity owned by shareholders that can raise capital by issuing stock.

C corporations are independent from their owners, which limits personal liability and allows the business to continue if ownership changes. However, profits may be taxed at both the corporate and shareholder levels.

Best for: Businesses planning to raise investors or scale quickly

- Pro: Can raise capital by selling stock

- Con: May be subject to double taxation

S corporation

A tax designation that allows a corporation to pass income directly to shareholders.

S corporations are taxed similarly to partnerships, with profits passing through to owners’ personal tax returns. However, they must meet IRS requirements, including limits on the number and type of shareholders.

Best for: Business owners who want liability protection with pass-through taxation

- Pro: Avoids double taxation

- Con: Ownership restrictions and eligibility requirements

Check out LendingTree’s guide on how to incorporate a business.

Nonprofit corporation

A tax-exempt organization formed for charitable, educational or similar purposes.

Nonprofits must apply for tax-exempt status with the IRS and follow specific rules, including restrictions on distributing profits. Requirements vary by state and organization type.

Best for: Mission-driven organizations

- Pro: May qualify for tax-exempt status

- Con: Strict compliance and reporting requirements

Check out LendingTree’s guide on how to start a nonprofit.

Benefit corporation

A for-profit company that aims to generate both profit and a positive social or environmental impact.

Benefit corporations are legally required to consider their impact on society and may need to publish benefit reports. Rules differ depending on where the business is formed.

Best for: Businesses balancing profit and purpose

- Pro: Supports mission-driven goals alongside profit

- Con: Requirements and regulations vary by state

Key factors to consider when choosing a business entity

Choosing the right business entity comes down to how much risk you’re willing to take, how you want to be taxed and how you plan to grow your business.

Liability protection

If you want to protect your personal assets, choose a structure that offers liability protection, such as an LLC or corporation. Sole proprietorships and general partnerships don’t separate personal and business liability.

Ownership structure

Consider how many people will own the business and how responsibilities will be shared. Sole proprietorships are owned by one person, while partnerships, LLCs and corporations can have multiple owners.

Taxes

Different business entities are taxed in different ways. Sole proprietorships, partnerships and most LLCs use pass-through taxation, while C corporations are taxed separately. S corporations allow pass-through taxation with a corporate structure. Depending on your state and business structure, you may also owe franchise tax — a separate charge some states levy just for the privilege of doing business there.

Cost and complexity

Some structures are easier and cheaper to set up than others. Sole proprietorships require little to no formal setup, while LLCs and corporations involve filing fees, ongoing paperwork and compliance requirements.

Future growth plans

If you plan to raise investment, issue stock or go public, you’ll need a corporate structure. If you want flexibility with fewer requirements, an LLC may be a better fit.

Can you change your business entity later?

Yes, you can change your business entity as your company grows. Many business owners start as a sole proprietorship or LLC and switch to a corporation later to raise capital or expand operations.

However, changing your business structure may involve additional paperwork, fees and tax implications, so it’s important to plan ahead.

Frequently asked questions

A sole proprietorship is the easiest business structure to start. If you begin operating a business without registering as another entity, you’re automatically considered a sole proprietor.

It depends on your needs. An LLC offers liability protection, while a sole proprietorship is simpler and less expensive to set up. Many business owners choose an LLC for added protection as their business grows.

There isn’t a single structure that always pays the least taxes. Sole proprietorships, partnerships and S corporations use pass-through taxation, which means business income is reported on your personal tax return, while C corporations are taxed separately. The best option depends on your income and financial goals.

A business entity name is the name under which you operate your business. If you use a different name than your legal name, you may need to register a DBA (“doing business as”) with your state or local government.

Sole proprietorships, partnerships and LLCs do not require incorporation. However, LLCs must file formation documents (often called articles of organization), and some partnerships may need to register with the state.

Compare business loan offers