10.5 Million-Plus Homes With Mortgages Owned by People 65 and Older — Here’s Where They’re Most, Least Common

Mortgage debt is the largest type of debt in the U.S., with the average amount owed by individuals with mortgages on their credit reports totaling nearly $150,000. Because the debt burden is usually steep, it’s often recommended that homeowners pay off their mortgage balances before retiring. That leaves fewer bills to worry about during the golden years.

But paying off a mortgage before retirement age isn’t feasible for everyone. In fact, more than 10.5 million housing units across the U.S. are owned by people 65 and older who still have mortgages.

To better understand where homeowners are likely to pay off their mortgage near or past their retirement age, LendingTree analyzed the latest U.S. Census Bureau American Community Survey data. We utilized this data to look at the share of housing units with mortgages in each of the nation’s 50 largest metros owned and occupied by people 65 and older.

Across these 50 metros, nearly 20% of all homes with mortgages are owned by someone 65 or older. And homes owned by people in this age group tend to be less valuable than those owned by the general population, while monthly housing costs tend to be lower.

Key findings

- Las Vegas, Los Angeles and San Diego have the largest share of homes with mortgages owned by people 65 and older. Across these metros, more than a quarter — 25.31% — of housing units with mortgages are owned and occupied by someone in this age group. Comparatively, that figure is 19.76% across the 50 largest metros.

- Austin, Texas, Dallas and Salt Lake City have the smallest share of homes with mortgages owned by 65-and-older homeowners. Among the housing units with mortgages in these metros, only 14.64% are owned by people 65 and older.

- California metros tend to have larger shares of housing units with mortgages by people 65 and older, while Texas metros tend to have smaller shares. Five of the 10 metros with the largest share of homes with mortgages owned by people 65 and older are in California, while four of the 10 metros with the smallest share of homes with mortgages owned by those 65 and older are in Texas.

- Houses owned by people 65 and older are typically worth less than those owned by the general homeowner population. In all but one metro — San Jose, Calif. — the overall median home value for a given metro is higher than that metro’s median value of homes owned by those 65 and older. While the difference varies by metro, it’s often greater than $10,000.

- Even if older homeowners are still paying off their mortgage, they usually have lower housing costs. Largely because their homes are typically less expensive, median monthly housing costs paid by 65-and-older homeowners with mortgages are usually hundreds of dollars less expensive than median monthly housing costs paid by the general population of homeowners with mortgages. Other factors, such as lower mortgage rates or property tax exemptions, can also help reduce housing costs for older homeowners.

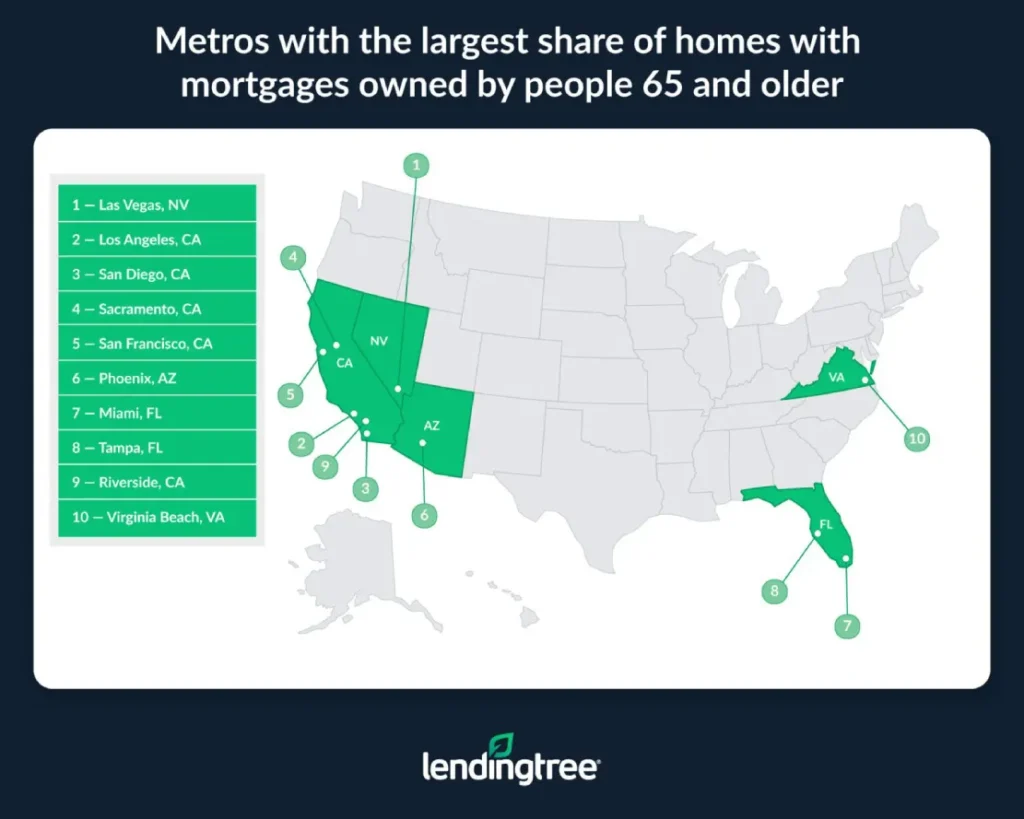

Metros with the largest share of homes with mortgages owned by people 65 and older

No. 1: Las Vegas

- Share of housing units with mortgages owned by people 65 and older: 25.75%

- Median value of homes owned and occupied by people 65 and older: $429,600

- Median value of all owner-occupied housing units: $437,900

- Difference between overall median home value and median home value for homes owned by people 65 and older: $8,300

- Median monthly housing costs for homes with mortgages owned and occupied by people 65 and older: $1,655

- Median monthly housing costs for all owner-occupied housing units with mortgages: $1,891

- Difference between overall median housing costs for homeowners with mortgages and median housing costs for homeowners 65 and older with mortgages: $236

No. 2: Los Angeles

- Share of housing units with mortgages owned by people 65 and older: 25.26%

- Median value of homes owned and occupied by people 65 and older: $861,000

- Median value of all owner-occupied housing units: $867,200

- Difference between overall median home value and median home value for homes owned by people 65 and older: $6,200

- Median monthly housing costs for homes with mortgages owned and occupied by people 65 and older: $2,564

- Median monthly housing costs for all owner-occupied housing units with mortgages: $3,096

- Difference between overall median housing costs for homeowners with mortgages and median housing costs for homeowners 65 and older with mortgages: $532

No. 3: San Diego

- Share of housing units with mortgages owned by people 65 and older: 25.13%

- Median value of homes owned and occupied by people 65 and older: $839,000

- Median value of all owner-occupied housing units: $864,900

- Difference between overall median home value and median home value for homes owned by people 65 and older: $25,900

- Median monthly housing costs for homes with mortgages owned and occupied by people 65 and older: $2,474

- Median monthly housing costs for all owner-occupied housing units with mortgages: $3,076

- Difference between overall median housing costs for homeowners with mortgages and median housing costs for homeowners 65 and older with mortgages: $602

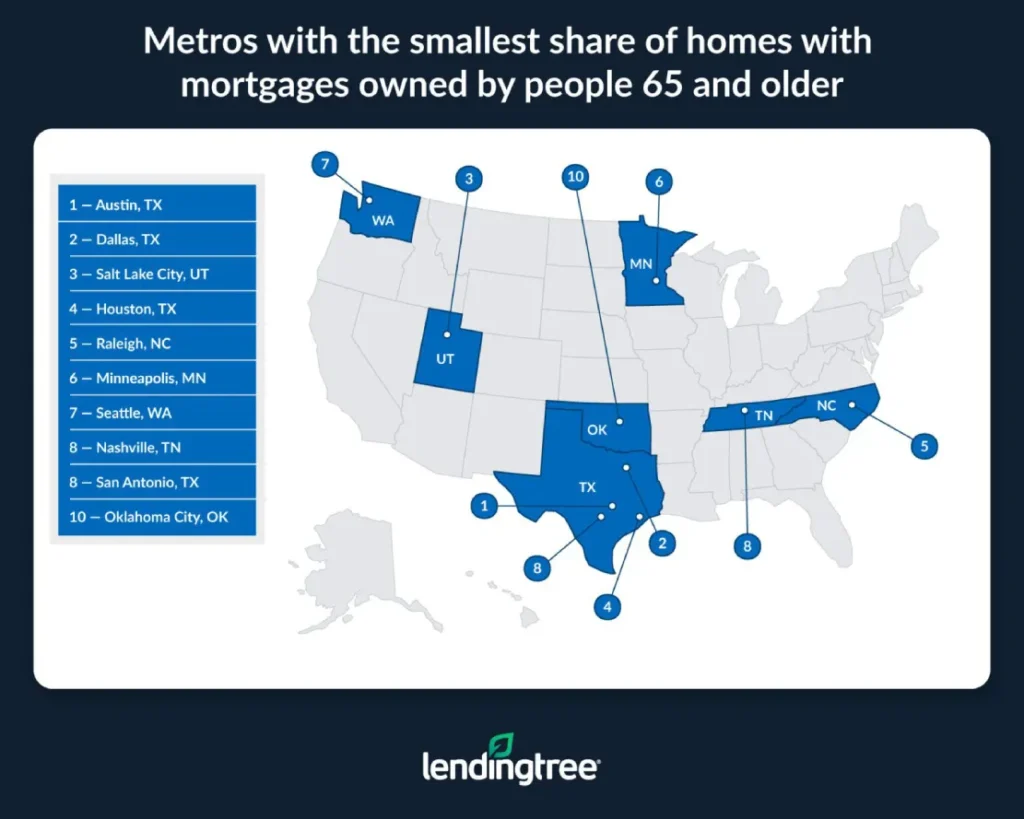

Metros with the smallest share of homes with mortgages owned by people 65 and older

No. 1: Austin, Texas

- Share of housing units with mortgages owned by people 65 and older: 14.58%

- Median value of homes owned and occupied by people 65 and older: $477,600

- Median value of all owner-occupied housing units: $487,200

- Difference between overall median home value and median home value for homes owned by people 65 and older: $9,600

- Median monthly housing costs for homes with mortgages owned and occupied by people 65 and older: $1,950

- Median monthly housing costs for all owner-occupied housing units with mortgages: $2,450

- Difference between overall median housing costs for homeowners with mortgages and median housing costs for homeowners 65 and older with mortgages: $500

No. 2: Dallas

- Share of housing units with mortgages owned by people 65 and older: 14.62%

- Median value of homes owned and occupied by people 65 and older: $340,300

- Median value of all owner-occupied housing units: $373,900

- Difference between overall median home value and median home value for homes owned by people 65 and older: $33,600

- Median monthly housing costs for homes with mortgages owned and occupied by people 65 and older: $1,840

- Median monthly housing costs for all owner-occupied housing units with mortgages: $2,358

- Difference between overall median housing costs for homeowners with mortgages and median housing costs for homeowners 65 and older with mortgages: $518

No. 3: Salt Lake City

- Share of housing units with mortgages owned by people 65 and older: 14.82%

- Median value of homes owned and occupied by people 65 and older: $526,800

- Median value of all owner-occupied housing units: $547,500

- Difference between overall median home value and median home value for homes owned by people 65 and older: $20,700

- Median monthly housing costs for homes with mortgages owned and occupied by people 65 and older: $1,740

- Median monthly housing costs for all owner-occupied housing units with mortgages: $2,086

- Difference between overall median housing costs for homeowners with mortgages and median housing costs for homeowners 65 and older with mortgages: $346

| Rank | Metro | Total # of housing units with mortgages | Total # of housing units with mortgages owned by people 65 and older | % of housing units with mortgages owned and occupied by people 65 and older | Median value of homes owned and occupied by people 65 and older | Median value of all owner-occupied housing units | Difference between overall median home value and median home value for homes owned by people 65 and older | Median monthly housing costs for homes with mortgages owned and occupied by people 65 and older | Median monthly housing costs for all owner-occupied housing units with mortgages | Difference between overall median housing costs for homeowners with mortgages and median housing costs for homeowners 65 and older with mortgages |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Las Vegas, NV | 338,447 | 87,155 | 25.75% | $429,600 | $437,900 | $8,300 | $1,655 | $1,891 | $236 |

| 2 | Los Angeles, CA | 1,486,465 | 375,531 | 25.26% | $861,000 | $867,200 | $6,200 | $2,564 | $3,096 | $532 |

| 3 | San Diego, CA | 443,036 | 111,333 | 25.13% | $839,000 | $864,900 | $25,900 | $2,474 | $3,076 | $602 |

| 4 | Sacramento, CA | 388,829 | 93,367 | 24.01% | $582,600 | $587,600 | $5,000 | $2,142 | $2,536 | $394 |

| 5 | San Francisco, CA | 660,489 | 155,107 | 23.48% | $1,080,900 | $1,105,100 | $24,200 | $2,925 | $3,811 | $886 |

| 6 | Phoenix, AZ | 843,948 | 197,592 | 23.41% | $433,000 | $457,400 | $24,400 | $1,553 | $1,850 | $297 |

| 7 | Miami, FL | 815,993 | 190,922 | 23.40% | $435,400 | $474,000 | $38,600 | $1,962 | $2,424 | $462 |

| 8 | Tampa, FL | 526,411 | 122,191 | 23.21% | $324,000 | $372,100 | $48,100 | $1,537 | $1,910 | $373 |

| 9 | Riverside, CA | 669,392 | 153,003 | 22.86% | $513,000 | $552,000 | $39,000 | $2,065 | $2,403 | $338 |

| 10 | Virginia Beach, VA | 319,477 | 71,756 | 22.46% | $333,500 | $343,700 | $10,200 | $1,736 | $1,901 | $165 |

| 11 | Cleveland, OH | 377,333 | 82,754 | 21.93% | $197,400 | $217,300 | $19,900 | $1,313 | $1,525 | $212 |

| 12 | Memphis, TN | 197,621 | 43,144 | 21.83% | $231,700 | $265,200 | $33,500 | $1,326 | $1,586 | $260 |

| 13 | San Jose, CA | 245,868 | 52,488 | 21.35% | $1,397,200 | $1,393,400 | -$3,800 | $3,133 | $4,000+* | >$867* |

| 14 | Providence, RI | 280,636 | 59,820 | 21.32% | $414,100 | $430,200 | $16,100 | $1,860 | $2,216 | $356 |

| 15 | Jacksonville, FL | 295,843 | 62,341 | 21.07% | $345,100 | $361,800 | $16,700 | $1,559 | $1,832 | $273 |

| 16 | Fresno, CA | 142,867 | 29,588 | 20.71% | $388,100 | $396,000 | $7,900 | $1,686 | $1,982 | $296 |

| 17 | Orlando, FL | 424,485 | 87,618 | 20.64% | $338,500 | $383,100 | $44,600 | $1,590 | $1,926 | $336 |

| 18 | Richmond, VA | 246,870 | 50,812 | 20.58% | $336,800 | $357,600 | $20,800 | $1,596 | $1,805 | $209 |

| 19 | Detroit, MI | 743,419 | 151,968 | 20.44% | $239,400 | $251,200 | $11,800 | $1,425 | $1,661 | $236 |

| 20 | New York, NY | 2,333,416 | 474,571 | 20.34% | $574,100 | $610,200 | $36,100 | $2,641 | $3,104 | $463 |

| 21 | Pittsburgh, PA | 416,730 | 83,823 | 20.11% | $203,900 | $218,300 | $14,400 | $1,302 | $1,533 | $231 |

| 22 | Baltimore, MD | 525,457 | 105,565 | 20.09% | $358,200 | $385,900 | $27,700 | $1,784 | $2,128 | $344 |

| 23 | Portland, OR | 446,073 | 89,047 | 19.96% | $540,800 | $560,900 | $20,100 | $1,893 | $2,335 | $442 |

| 24 | Birmingham, AL | 195,998 | 38,349 | 19.57% | $230,200 | $247,900 | $17,700 | $1,244 | $1,513 | $269 |

| 25 | St. Louis, MO | 532,698 | 104,220 | 19.56% | $231,200 | $247,900 | $16,700 | $1,395 | $1,592 | $197 |

| 26 | Chicago, IL | 1,552,575 | 302,449 | 19.48% | $295,800 | $316,500 | $20,700 | $1,744 | $2,112 | $368 |

| 27 | Boston, MA | 811,851 | 157,735 | 19.43% | $612,300 | $646,600 | $34,300 | $2,378 | $2,863 | $485 |

| 28 | New Orleans, LA | 136,598 | 26,454 | 19.37% | $243,700 | $263,500 | $19,800 | $1,607 | $1,869 | $262 |

| 29 | Washington, DC | 1,143,075 | 221,324 | 19.36% | $552,100 | $574,000 | $21,900 | $2,294 | $2,679 | $385 |

| 30 | Cincinnati, OH | 406,721 | 76,992 | 18.93% | $244,600 | $270,100 | $25,500 | $1,409 | $1,644 | $235 |

| 31 | Charlotte, NC | 495,437 | 92,219 | 18.61% | $338,600 | $381,200 | $42,600 | $1,373 | $1,715 | $342 |

| 32 | Philadelphia, PA | 1,060,630 | 196,286 | 18.51% | $334,400 | $356,700 | $22,300 | $1,782 | $2,091 | $309 |

| 33 | Louisville, KY | 249,068 | 45,924 | 18.44% | $246,400 | $253,600 | $7,200 | $1,310 | $1,507 | $197 |

| 34 | Buffalo, NY | 181,851 | 33,414 | 18.37% | $222,200 | $233,300 | $11,100 | $1,376 | $1,572 | $196 |

| 35 | Indianapolis, IN | 399,889 | 71,911 | 17.98% | $239,300 | $278,200 | $38,900 | $1,224 | $1,554 | $330 |

| 36 | Columbus, OH | 361,611 | 64,833 | 17.93% | $291,800 | $312,900 | $21,100 | $1,478 | $1,757 | $279 |

| 37 | Denver, CO | 568,569 | 101,781 | 17.90% | $588,300 | $611,300 | $23,000 | $1,949 | $2,474 | $525 |

| 38 | Atlanta, GA | 1,089,293 | 194,870 | 17.89% | $359,400 | $383,600 | $24,200 | $1,522 | $1,923 | $401 |

| 39 | Milwaukee, WI | 258,655 | 45,838 | 17.72% | $286,400 | $308,100 | $21,700 | $1,485 | $1,795 | $310 |

| 40 | Kansas City, MO | 381,393 | 66,522 | 17.44% | $266,000 | $289,200 | $23,200 | $1,559 | $1,798 | $239 |

| 41 | Oklahoma City, OK | 213,877 | 35,709 | 16.70% | $229,800 | $244,000 | $14,200 | $1,454 | $1,669 | $215 |

| 42 | San Antonio, TX | 382,230 | 62,703 | 16.40% | $257,200 | $292,700 | $35,500 | $1,561 | $1,936 | $375 |

| 42 | Nashville, TN | 373,719 | 61,286 | 16.40% | $407,700 | $437,200 | $29,500 | $1,491 | $1,839 | $348 |

| 44 | Seattle, WA | 676,302 | 110,636 | 16.36% | $686,200 | $712,200 | $26,000 | $2,274 | $2,839 | $565 |

| 45 | Minneapolis, MN | 726,050 | 116,911 | 16.10% | $355,500 | $369,500 | $14,000 | $1,744 | $2,042 | $298 |

| 46 | Raleigh, NC | 286,261 | 43,927 | 15.35% | $387,900 | $439,500 | $51,600 | $1,499 | $1,916 | $417 |

| 47 | Houston, TX | 985,706 | 147,662 | 14.98% | $286,900 | $308,200 | $21,300 | $1,784 | $2,193 | $409 |

| 48 | Salt Lake City, UT | 213,230 | 31,608 | 14.82% | $526,800 | $547,500 | $20,700 | $1,740 | $2,086 | $346 |

| 49 | Dallas, TX | 1,110,736 | 162,387 | 14.62% | $340,300 | $373,900 | $33,600 | $1,840 | $2,358 | $518 |

| 50 | Austin, TX | 399,366 | 58,246 | 14.58% | $477,600 | $487,200 | $9,600 | $1,950 | $2,450 | $500 |

Getting a mortgage later in life isn’t necessarily bad

As would-be homeowners age, there are various reasons why many might second-guess getting a mortgage, especially if they’re worried they’ll pay off their loan in their late 60s or beyond.

Some older buyers might be concerned they won’t be able to keep up with their monthly mortgage payments once they retire, while others might worry they’ll die before they finish paying off their loans and saddle their families with leftover debt.

Though these concerns can be valid, that doesn’t mean older people thinking about buying a home should necessarily shy away from getting a new mortgage — especially if they couldn’t afford a home without one.

In fact, those who get a mortgage later in life might, in some ways, be in a better position to handle their debt than someone younger. For example, older Americans generally have better credit scores than younger Americans. Because people with stronger credit scores tend to have better rates and smaller monthly payments than those with less cash or worse credit scores, older Americans who get a mortgage could find paying off their loan isn’t as challenging as feared.

Of course, income tends to drop when a person retires, but many thinking about a new mortgage in their 50s or 60s might find they’re more than capable of managing their debt, even as they grow older.

Tips for getting and paying off a mortgage when you’re older

Older Americans considering a mortgage should keep the following tips in mind to help ensure they qualify for a loan and keep on top of their new debt.

- Consider a retirement mortgage. As the name implies, retirement mortgages can help older homebuyers no longer in the workforce purchase a home. Because these types of mortgages don’t have the same income standards as traditional loans, some older buyers might find qualifying for them easier than traditional loans.

- Try to avoid taking out a massive loan. Though managing a mortgage after retiring is possible, it’s especially important for older homeowners not to bite off more than they can chew. The smaller their loan, the less money they’ll need to allocate each month toward paying it off, and the more money they’ll have for other expenses.

- Shop around before buying. Because different lenders can offer different rates, even to those with the same financial profiles, shopping around for a mortgage before buying a home is generally a good idea. Shopping around could increase an older homebuyer’s chances of finding a lender willing to work with them and help them secure a lower rate.

Methodology

Data in this study is derived at the metropolitan statistical area (MSA) level from the U.S. Census Bureau 2023 American Community Survey with one-year estimates — the latest available.

Because of how the Census Bureau organizes its data, LendingTree focused on housing units with mortgages owned and occupied by those 65 and older — even though 65 is below the current minimum full retirement age in the U.S. of either 66 or 67, depending on the year of birth.

View mortgage loan offers from up to 5 lenders in minutes

Recommended Articles