Nearly 6 in 10 Gen Z Cardholders Typically Pay Just the Minimum on a Credit Card

Almost 6 in 10 Gen Z credit cardholders say they typically make only the minimum payment on at least one of their cards each month.

LendingTree surveyed more than 1,500 American cardholders about bad habits, misconceptions and mistakes they make with their cards. While paying just the minimum is one of the worst habits you can get into with your credit card, it’s hardly the only common misstep cardholders make. A troubling number of cardholders believe costly credit myths, don’t know basic information about key details of their cards and even forgo emergency savings because they see their credit card as a safety net.

Here’s more of what we found.

- Minimum payments are a way of life, especially among younger adults. More than 4 in 10 cardholders (41%) typically pay just the minimum on at least one card, but that jumps to nearly 6 in 10 (58%) among Gen Zers and drops to nearly 2 in 10 (19%) among baby boomers.

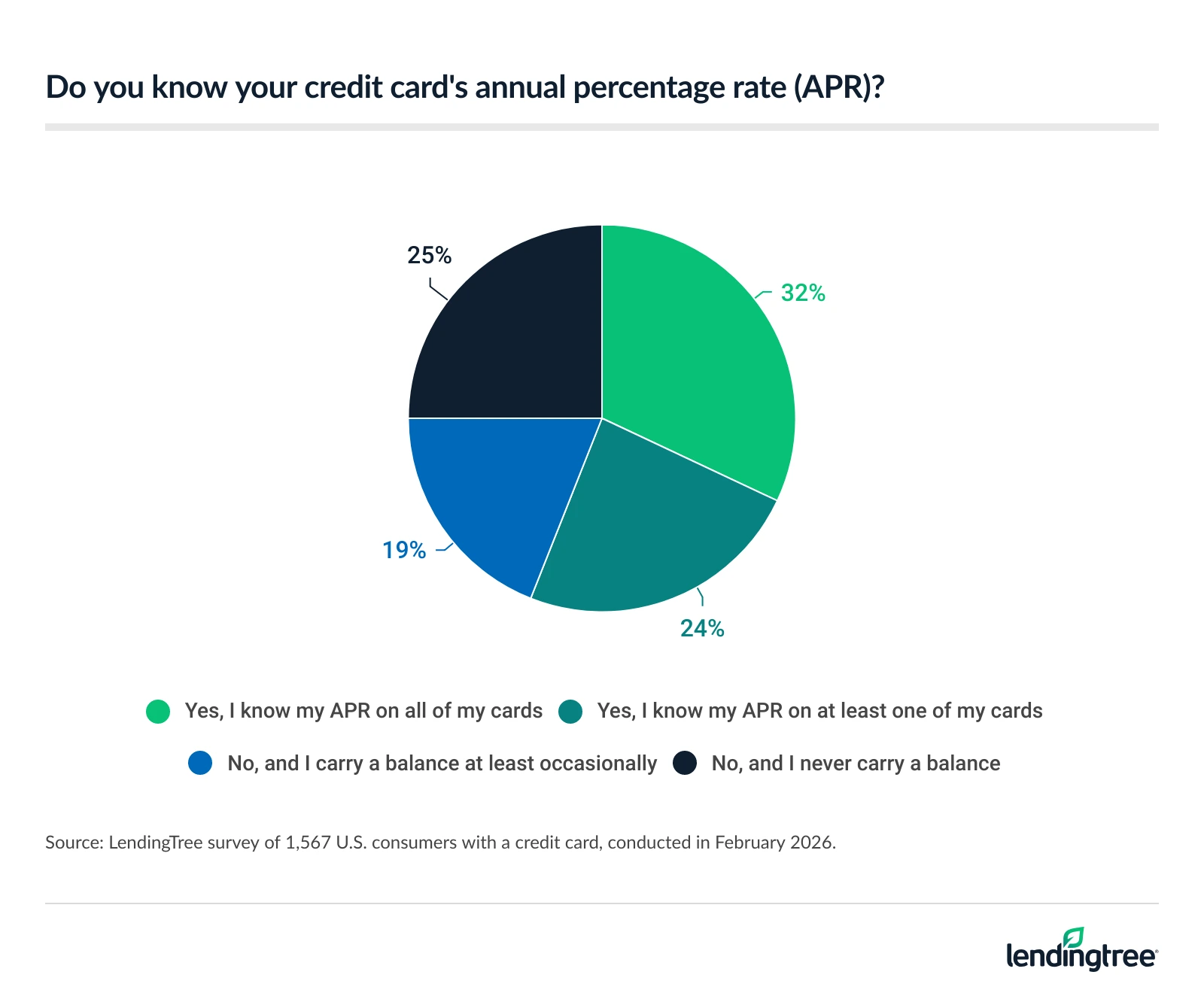

- 44% of cardholders don’t know the interest rate on any of their credit cards. That includes 19% who also carry a balance at least occasionally. Another 24% say they know the rate on some, but not all, of their cards. Women are far more likely than men to not know any of their cards’ interest rates — 51% versus 38%. The knowledge gap is most pronounced among older cardholders: 57% of baby boomers and 49% of Gen Xers don’t know any of their APRs.

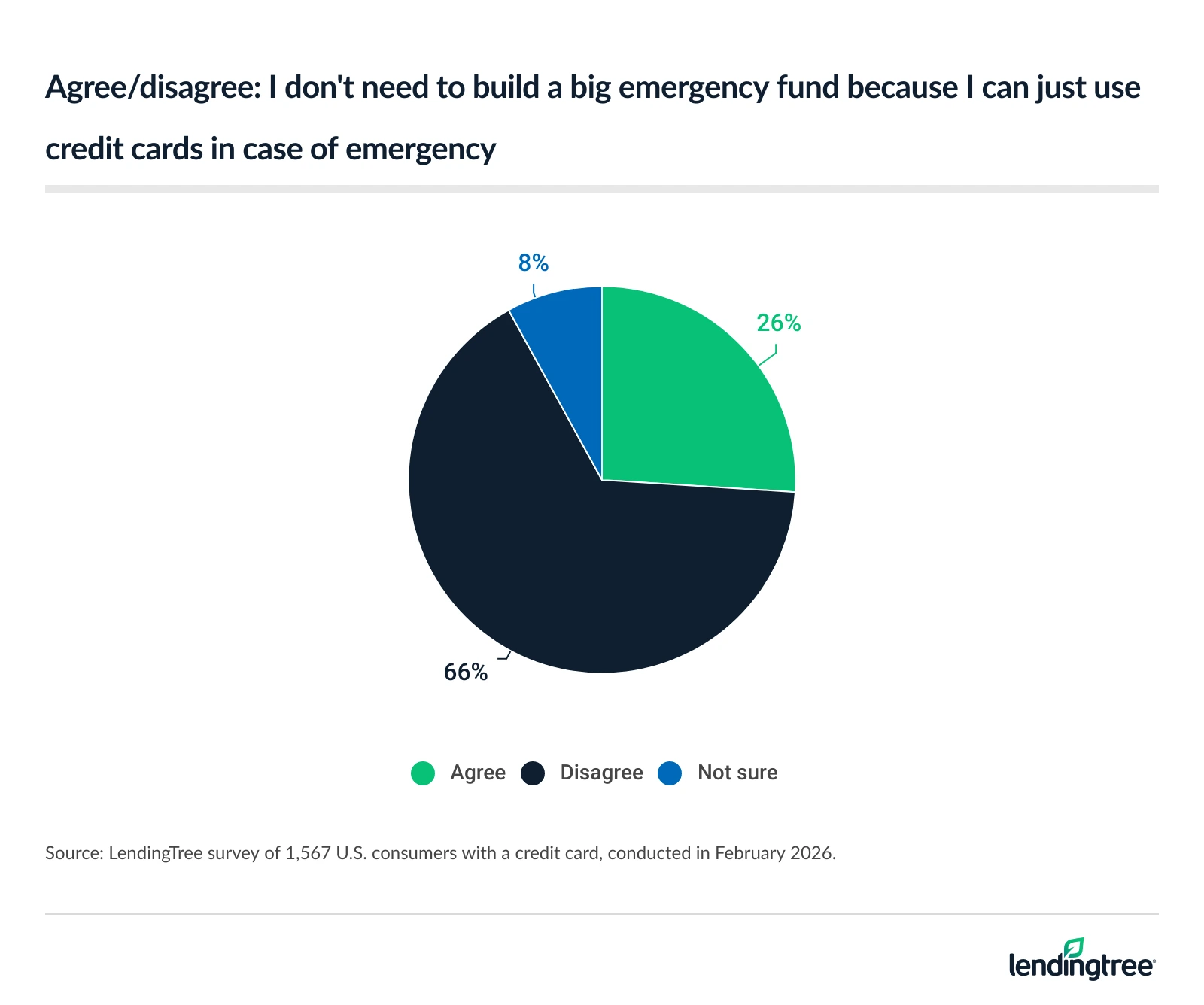

- Credit cards double as emergency funds. More than 1 in 4 cardholders (26%) agree they don’t need a big emergency fund because they can rely on credit cards in case of emergency, including 43% of Gen Zers and 41% of parents of young kids. Meanwhile, 72% of cardholders say they’ve used a credit card to cover emergency expenses.

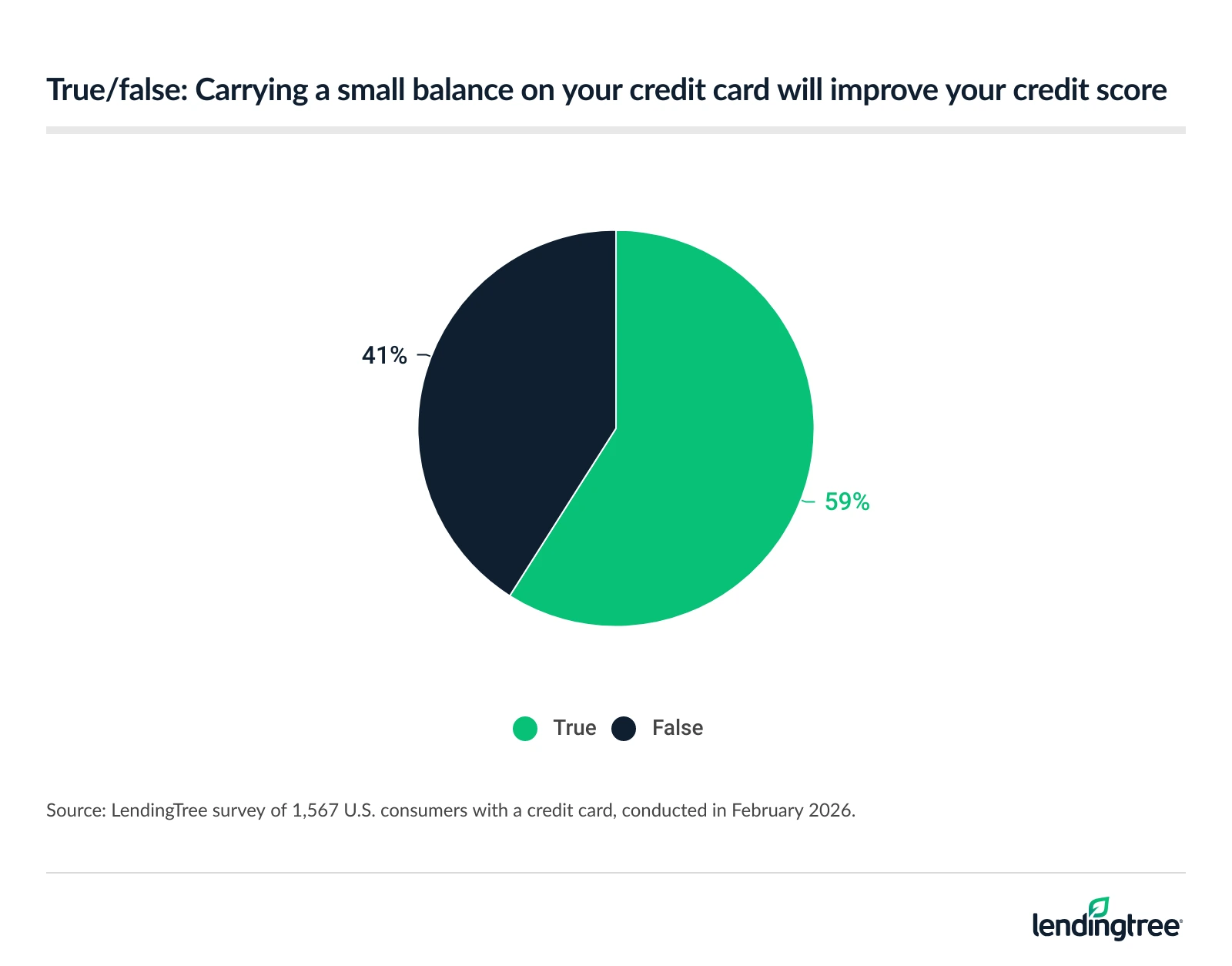

- A majority believes a common credit myth. Despite 88% of cardholders feeling confident in their understanding of how credit cards affect credit scores, 59% say carrying a small balance will improve their score. Unfortunately, those most likely to believe this myth are among the least likely to be able to afford to carry that balance: The lower your income, the more likely you are to believe it.

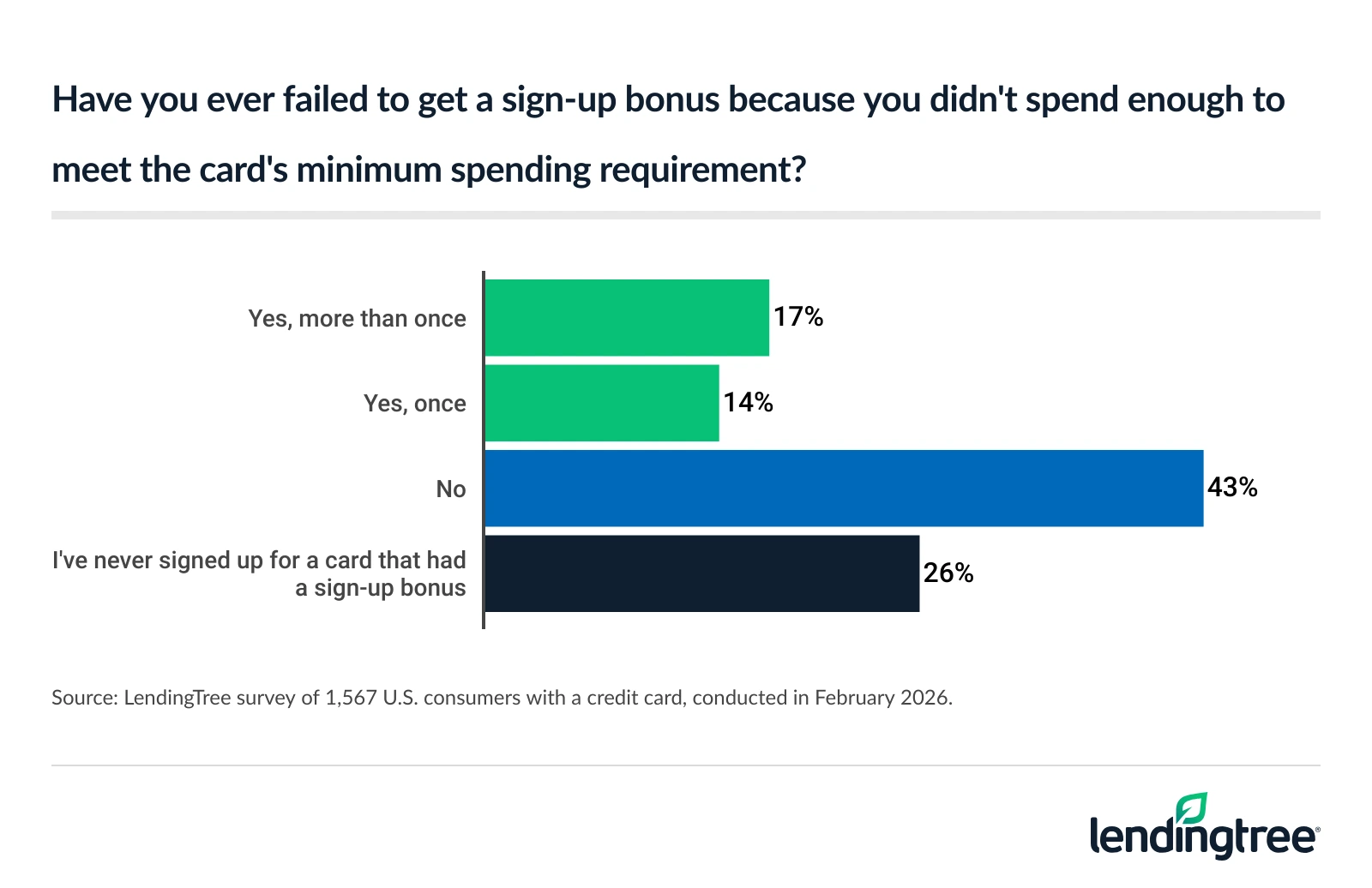

- Plenty have dropped the ball in pursuit of a sign-up bonus. 74% of cardholders say they’ve signed up for a card that featured a sign-up bonus offer. 31% of cardholders say they’ve failed to get a sign-up bonus because they didn’t meet the card’s minimum spending requirement, including 17% who say they’ve done so more than once. Additionally, 24% of cardholders admit they’ve had buyer’s remorse after redeeming points or miles, and 31% have previously lost rewards from canceling a card.

Minimum payments are a way of life, especially among younger adults

Slightly more than 4 in 10 credit cardholders (41%) say they typically pay just the minimum required on at least one of their cards each month. That’s a big deal because regularly making only the minimum payment can be a recipe for staying mired in debt.

- Overall: 41% of credit cardholders typically pay just the minimum on at least one credit card in a given month

- Men: 42%

- Women: 40%

- Gen Zers: 58%

- Millennials: 55%

- Gen Xers: 37%

- Baby boomers: 19%

- Parents with young kids: 56%

- Parents with kids 18 or older: 26%

- Nonparents: 38%

- People who earn less than $30,000: 46%

- People who earn $30,000 to $49,999: 47%

- People who earn $50,000 to $99,999: 37%

- People who earn $100,000 or more: 40%

To be clear, there are times when it can make sense to pay just the minimum. For example, people with significant debt across multiple cards may pay only the minimum on one or more cards so they can put money toward the card with the highest APR or the largest balance. Also, if there’s a choice between paying more than the minimum on a credit card or paying for essentials such as utilities and groceries, the latter can take precedence over the former.

Still, it’s troubling that more than 40% of cardholders regularly pay just the minimum. The numbers are even more concerning for younger Americans. Nearly 6 in 10 Gen Z cardholders ages 18 to 29 (58%) say they only pay the minimum regularly, as do 55% of millennials ages 30 to 45. Just 37% of Gen X cardholders ages 46 to 61 and 19% of baby boomers ages 62 to 80 say the same.

Perhaps surprisingly, 40% of those earning at least $100,000 a year say they typically pay the minimum on at least one card. That’s a higher percentage than the share seen among cardholders earning $50,000 to $99,999 (37%), and not too much lower than the share of those earning $30,000 to $49,999 (47%) or less than $30,000 (46%).

44% of cardholders don’t know the interest rate on any of their credit cards

If you regularly carry a balance, your credit card’s interest rate is a big deal. That’s especially true if you typically make only the minimum payment on one or more cards each month. It’s what determines how much interest you’ll pay on that unpaid balance. However, more than 4 in 10 cardholders (44%) say they don’t know the interest rate on any of their credit cards, including 19% who also carry a balance at least occasionally.

A deeper dive into the data shows a massive knowledge gap among generations: 57% of baby boomers and 49% of Gen Xers don’t know the APRs of any of their credit cards, versus 35% of millennial cardholders and 33% of Gen Zers. It also shows that women are far more likely than men (51% versus 38%) to not know the APRs of any of their credit cards. Also, the lower your income, the more likely you are to be unaware of your credit cards’ APRs.

It’s important to note that not everyone needs to know their credit card’s interest rate. For example, if you use your card only sparingly or have never carried a balance, your card’s APR doesn’t really matter. Typically, you’re only charged interest if you carry a balance from month to month.

Credit cards double as emergency funds

While countless Americans have credit card debt because they need their card to help them make ends meet, many others are thrust into card debt because of an emergency. Anything from a surprise trip to the vet or a flat tire to a job loss or medical crisis can lead to a spiral of debt.

Nearly 3 in 4 cardholders (72%) say they’ve used a credit card to cover an emergency expense. A stunning 81% of parents of young kids have done so. Millennials (77%) and Gen Xers (74%) are the most likely age groups to have used a credit card to cover emergency expenses, but even 67% of Gen Zers and 66% of boomers say the same.

Most of us have been there at some point. Life happens, and sometimes you just have to do what you have to do. What isn’t OK, however, is thinking that you don’t really need to build an emergency fund because you have credit cards to fall back on. Unfortunately, that’s how many Americans say they feel.

We asked cardholders if they agreed with this statement, “I don’t need to build a big emergency fund because I can just use my credit card(s) in case of an emergency,” and 26% said yes. Among the groups most likely to agree: Gen Zers (43%), parents of young kids (41%) and millennials (37%).

A majority believes a common credit myth

Many Americans are stuck in a seemingly never-ending battle to get out of credit card debt. However, despite 88% of cardholders feeling confident in their understanding of how credit cards affect credit scores, a significant number of Americans are perfectly happy to carry a bit of a balance from month to month because they mistakenly believe that doing so will help their credit score.

Nearly 6 in 10 cardholders (59%) say carrying a small balance on their cards will improve their score. While every credit report and score is unique and different, and there can be exceptions to almost any rule, it’s — generally speaking — not true that carrying a balance helps your score. In fact, the opposite is more likely to be true. Along with being expensive, carrying a balance can do real damage to your credit picture.

Unfortunately, among those most likely to believe this myth are those least likely to be able to afford to carry that balance. The lower your income, the more likely you are to believe that carrying a small balance helps your credit score. In fact, 67% of those making less than $30,000 a year say so, compared with 53% of those making $100,000 or more.

Plenty have dropped the ball in pursuit of a sign-up bonus

While many cardholders find themselves spending too much, some have the opposite problem: They spend too little, and it costs them.

Hurt by spending too little? What?

It’s true when it comes to cards with sign-up bonuses. These rewards would more accurately be called sign-up-and-spend-X-amount-within-a-specific-time-frame bonuses because you don’t get them just for signing up. You might have to spend anywhere from a few hundred dollars to several thousand dollars, typically within about three months, to collect the reward.

Of course, sign-up bonuses are enormously popular, with 74% of cardholders saying they’ve signed up for a card that offered one. However, 31% of cardholders say they’ve failed to get a sign-up bonus because they didn’t meet the card’s minimum spending requirement, including 17% who say they’ve done so more than once.

More than half of Gen Z cardholders (56%) and parents of young kids (53%) say they’ve missed out on sign-up bonuses because they didn’t spend enough. Men are much more likely than women to have done the same (35% versus 27%).

That’s hardly the only mistake people have made in managing their rewards. About a quarter of cardholders (24%) say they’ve had buyer’s remorse after redeeming points or miles, and another 31% have previously lost rewards because they canceled a card.

Tips for steering clear of costly mistakes

There’s rarely a one-size-fits-all answer when it comes to managing your money. One person’s mistake is another’s shrewd move. Minimum payments are a perfect example. When they’re part of a well-thought-out debt repayment strategy, paying the minimum on some cards temporarily can make all the sense in the world. In most other cases, however, it’s a costly mistake to be avoided.

It isn’t always easy to know the right path. Today, countless “experts” are screaming at you on your social media feeds, in your email, on your TV or in your browser, all saying different things but proclaiming that they have all the answers. Just sign up for this course that just happens to be on sale at an unbeatable price…

None of us knows it all, though. All we can do is try to make the best decisions for ourselves and our families based on our knowledge, goals and priorities.

Here are a few things to keep in mind.

- Know yourself. What’s your risk tolerance? What are you comfortable spending in a month? What are your main financial priorities and goals? How much work do you want to put into something like credit card rewards? Do you feel you know enough about money? Are you a spender or a saver? There are a million possible questions to ask, but taking the time to ask them of yourself before you make financial decisions is usually wise. It may not lead you to all the right answers, but it can certainly point you in the right direction.

- Understand the power of interest, both for good and for ill. Interest is one of the most powerful things on Earth. It can be exhilarating to see it grow when it works in your favor and downright terrifying when working against you. The good news is that you have real power over rates on both sides. Shopping around and comparing lender offers can help you minimize the interest you pay on a loan, as can consolidating debt with a 0% balance transfer credit card or a low-interest personal loan. Meanwhile, swapping traditional savings accounts for online high-yield accounts is a good example of maximizing the interest you earn.

- When in doubt, save more. It’s hard to overstate the importance of a robust emergency fund. It can bring peace of mind in a time of great uncertainty. It can help you break a cycle of debt. It can give you the freedom to extract yourself from an unpleasant or even unsafe circumstance. And the truth is that very, very few of us have nearly enough savings to feel comfortable. Yes, credit cards can be a useful safety net when times get tough, but a real emergency fund stocked with real cash is a far better tool. Easier said than done, for sure, but an important goal nonetheless.

- Protect your credit by keeping it simple. Few things in life are more expensive than poor credit. It can cost you tens of thousands of dollars over the years in the form of higher interest rates and fees on loans. However, people tend to overthink credit. That’s how myths like the one we discussed earlier get started. Yes, there are plenty of details and nuances around credit, but the truth is that credit is really simpler than you think. Ultimately, it comes down to three things: paying your bills on time every time, keeping your balances as low as possible, and not applying for too much credit too often. Do those three things repeatedly over the years, and your credit will likely be just fine.

- Never stop learning. Think you know it all? Trust me. You don’t. No one does. While some personal finance basics haven’t changed in generations, so much else related to your money is constantly evolving. I’m not saying you need to get an advanced economics degree or become a certified financial planner. However, curiosity about what is happening and a willingness to learn new things can serve you well and leave you better equipped for whatever may be ahead.

Methodology

LendingTree commissioned QuestionPro to conduct an online survey of 2,000 U.S. consumers ages 18 to 80 on Feb. 13-17, 2026. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. Researchers reviewed all responses for quality control.

We defined generations as the following ages in 2026:

- Generation Z: 18 to 29

- Millennials: 30 to 45

- Generation X: 46 to 61

- Baby boomers: 62 to 80