The Most and Least Financially Responsible Metros: 2026 Report

Where do America’s most financially responsible people live? Many are in the Midwest.

LendingTree research ranked the nation’s largest 100 metros based on a combination of housing cost, debt burden and credit usage indicators. The results show that half of the top 10 metros are in the Midwest.

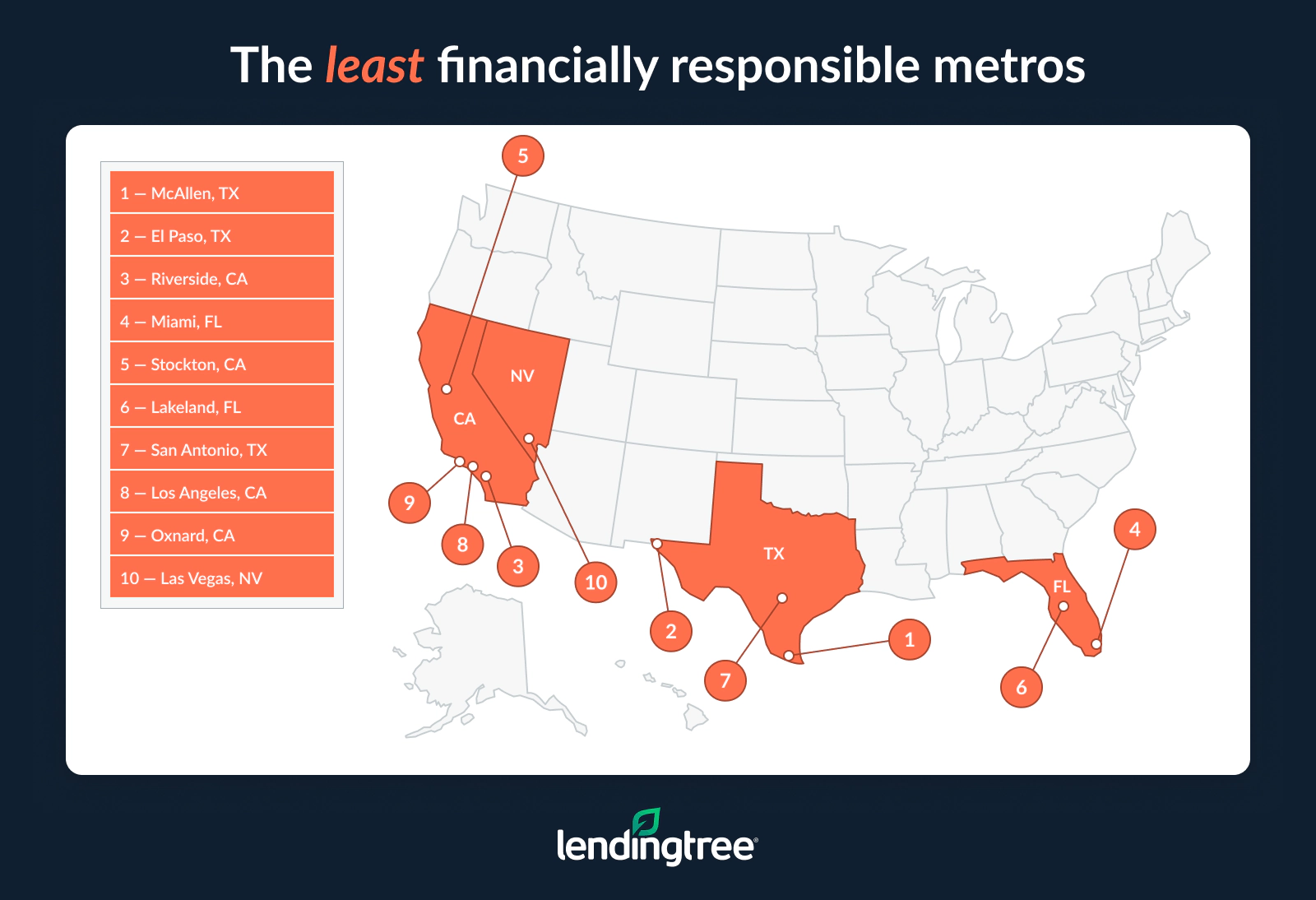

Meanwhile, the bottom of the rankings is dominated by two states: Texas and California. Together, they account for seven of the bottom 10 metros.

Read on to see where your metro ranks, gain more insights into Americans’ spending habits and learn how to spend within your means.

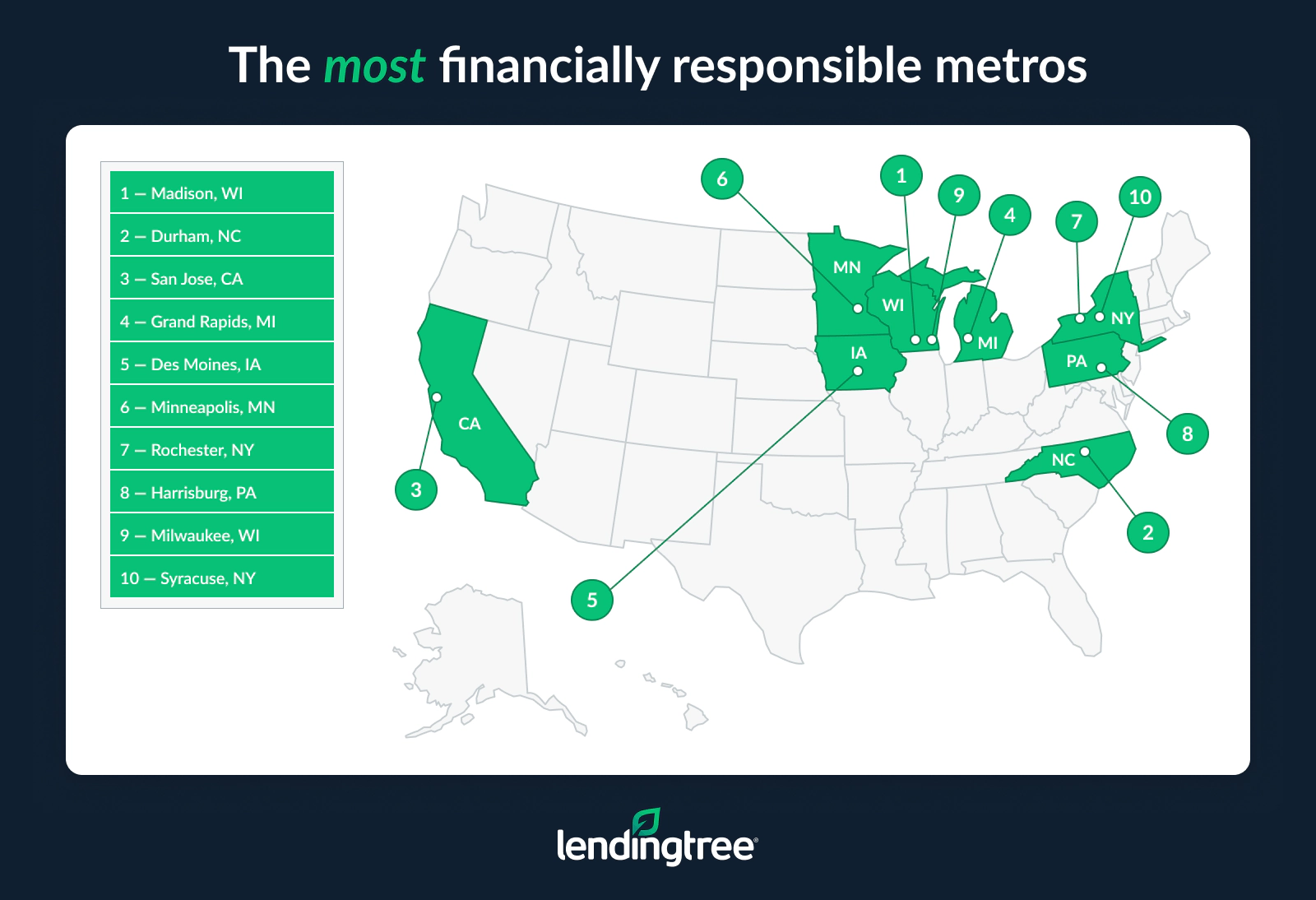

- Madison, Wis., is the most financially responsible metro. Across the 100 largest metros, Madison has the lowest share of credit cardholders with at least one maxed-out card, at 13.2%. Five of the 10 most financially responsible metros are in the Midwest.

- Even with that Midwest concentration, the top three metros are spread across the Midwest, South and West. Durham, N.C., representing the South, and San Jose, Calif., representing the West, round out the top three behind Madison. San Jose has the largest share of cardholders with credit utilization below 30%, at 77.6%.

- The least financially responsible metro is McAllen, Texas. McAllen residents have the highest average number of credit inquiries over the past two years (5.8). El Paso, Texas, and Riverside, Calif., follow. El Paso also has the highest share of cardholders with at least one maxed-out card (32.3%) and the lowest share of cardholders with credit utilization below 30% (46.3%). Riverside ties for the highest household debt-to-income ratio, at 251%.

- California and Texas are heavily represented at the bottom of the ranking. Four California metros — Riverside, Stockton, Los Angeles and Oxnard — and three Texas metros — McAllen, El Paso and San Antonio — rank among the bottom 10. No Texas metro ranks among the 50 most financially responsible metros.

Madison, Wis., takes the top spot as the nation’s most financially responsible metro

Madison, Wis., is home to the most responsible money managers this year, earning the No. 1 spot in our rankings of the most financially responsible metros. This is based on five metrics, including:

- Percentage of households spending at least 35% of their income on housing costs

- Household debt-to-income (DTI) ratio

- Credit inquiries in the previous two years

- Percentage of cardholders with at least one maxed-out card

- Percentage of cardholders with credit utilization below 30%

While residents of Wisconsin’s capital city rank high across several measures of financial health, they lead the nation with the lowest share of credit cardholders with at least one maxed-out card (13.2%). This measure is significant, as keeping credit balances low (or, better yet, nonexistent) means lower monthly payments. It also gives you room to cover unexpected expenses without taking on additional debt.

“When your credit cards are at or near their limits, even a small emergency can become a major financial setback,” says Matt Schulz, LendingTree chief consumer finance analyst and author of “Ask Questions, Save Money, Make More: How to Take Control of Your Financial Life.” “Keeping balances well below the limit shows lenders that you’re not overly dependent on credit to get by.”

Lowest share of credit cardholders with at least one maxed-out card

| Rank | Metro | % with maxed-out card(s) |

|---|---|---|

| 1 | Madison, WI | 13.2% |

| 2 | Milwaukee, WI | 14.1% |

| 3 | Des Moines, IA | 14.8% |

| 3 | Spokane, WA | 14.8% |

Madison’s first-place overall ranking is a slight step up from last year, when it ranked as the third most financially responsible metro.

Why do so many people in Madison seem to manage their money well? Several factors may be at play. The metro has a relatively low unemployment rate and a highly educated population, thanks, in part, to the presence of the University of Wisconsin-Madison. Higher levels of education and stable employment often translate to healthier financial habits.

Culture may also play a role. Five of the 10 most financially responsible metros are in the Midwest, a region often associated with practicality and a strong work ethic. But financial responsibility isn’t confined to one part of the country. The top three most financially responsible metros in this year’s rankings are spread out across the country, suggesting that a mix of economic conditions and local demographics may matter more than geography alone.

The top 3 performers span the Midwest, South and West

It’s not all Midwestern metros taking the top spots. Durham, N.C., in the South, takes second place, and San Jose, Calif., on the West Coast, rounds out the top three most financially responsible metros.

As for why these metros are at the top, there’s no one factor but rather a combination of conditions that likely contribute. For example, Durham has a highly educated population (54.7% have a bachelor’s degree or higher) and has seen large job growth in high-paying industries such as healthcare and technology.

While San Jose is one of the most expensive places to live in the U.S., it still ranks high, likely due in part to the fact that the area has seen a strong labor market and a low rate of unemployment.

Higher earnings help, but Schulz says they don’t always correlate with financial responsibility.

“A big paycheck doesn’t automatically mean someone is good with money,” he said. “If spending rises right along with income, even high earners can end up stretched thin, carrying debt or living paycheck to paycheck. Financial health is less about how much you make and more about how consistently you live below your means.”

Also in the top 10 are two upstate New York metros — Rochester (seventh) and Syracuse (10th). New York City ranks 76th.

In last year’s analysis, Des Moines, Iowa, and San Jose tied for first, while Madison ranked third. This year, Madison moves into the top spot, San Jose ranks third and Des Moines ranks fifth.

While San Jose slipped from its first-place ranking overall, the California metro does have the highest share of cardholders with utilization below 30% (77.6%) in this year’s rankings. Schulz says this is commonly cited as a credit-health benchmark because it’s simple, memorable and generally a solid target for consumers.

“It doesn’t mean 29% is perfect or 31% is disastrous, but lower utilization is typically better for your credit score,” he says. “The goal for utilization should always be 0%, meaning that you’ve paid your bill in full, so think of 30% as a useful ceiling rather than an ideal destination.”

Highest share of credit cardholders with utilization below 30%

| Rank | Metro | % with utilization below 30% |

|---|---|---|

| 1 | San Jose, CA | 77.6% |

| 2 | Madison, WI | 75.6% |

| 3 | Durham, NC | 72.9% |

Another measure of our ranking formula considered the percentage of income that people spend on housing in the 100 largest metros. We found that Fayetteville, Ark., has the lowest share of households spending at least 35% of their income on housing (17.9%), while Miami has the highest share (38.6%).

McAllen, Texas, ranks as the least financially responsible metro in America

Looking at the bottom of the rankings, McAllen, Texas, comes in as the least financially responsible metro in the U.S. One factor weighing on McAllen’s ranking is that residents there have the highest average number of credit inquiries over the past two years (5.8).

A high number of credit inquiries can be a red flag for financial stress, as it often indicates someone is applying for credit and considering taking on more debt. While a single inquiry isn’t usually a concern, multiple inquiries in a short period can cause unease for lenders. These inquiries can also lower your credit score, making it more difficult and more expensive to qualify for loans and credit cards in the future.

Highest average number of credit inquiries in the past 2 years

| Rank | Metro | Credit inquiries in past 2 years |

|---|---|---|

| 1 | McAllen, TX | 5.8 |

| 2 | Jackson, MS | 4.4 |

| 3 | Augusta, GA | 4.3 |

| 3 | Memphis, TN | 4.3 |

El Paso, Texas, and Riverside, Calif., follow McAllen at the bottom of our overall rankings. Certain metrics stood out in these metros’ scores: El Paso has the highest share of cardholders with at least one maxed-out card (32.3%), as well as the lowest share of cardholders with credit utilization below 30% (46.3%). Riverside, meanwhile, ties for the highest household debt-to-income ratio, at 251%.

At the other end of the spectrum, consumers in Denver have the fewest credit inquiries over the past two years, averaging 1.2.

California and Texas dominate the bottom of the ranking

Seven of the metros in the bottom 10 come from two big states: California and Texas. California metros take four spots — Riverside, Stockton, Los Angeles and Oxnard — while Texas metros take three — McAllen, El Paso and San Antonio — of the bottom 10 spots.

While a couple of California metros rank in the top 50 — San Jose (third) and San Francisco (39th) — not a single Texas metro does.

Why? Even though both Texas and California are high-growth states, other factors, such as housing affordability challenges, contribute as well. For example, California has some of the highest housing costs in the country.

Demographics may also play a role. Both California and Texas have large Hispanic and Latino populations. Research has shown that Latino households continue to face several financial challenges, including poor access to credit, according to a survey from UnidosUS. Those broader challenges may influence metros’ financial health.

Full rankings: The most and least financially responsible metros

| Rank | Metro | Final score | % spending at least 35% on housing | DTI ratio | Credit inquiries in past 2 years | % with maxed-out card(s) | % with utilization below 30% | Index: % spending at least 35% on housing | Index: DTI ratio | Index: Credit inquiries in past 2 years | Index: % with maxed-out card(s) | Index: % with utilization below 30% |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Madison, WI | 84.7 | 23.1% | 102% | 2.1 | 13.2% | 75.6% | 74.9 | 74.5 | 80.4 | 100.0 | 93.6 |

| 2 | Durham, NC | 80.5 | 23.8% | 51% | 2.5 | 18.1% | 72.9% | 71.5 | 100.0 | 71.7 | 74.3 | 85.0 |

| 3 | San Jose, CA | 79.6 | 27.9% | 51% | 1.6 | 21.8% | 77.6% | 51.7 | 100.0 | 91.3 | 55.0 | 100.0 |

| 4 | Grand Rapids, MI | 79.3 | 18.9% | 114% | 2.4 | 16.0% | 69.3% | 95.2 | 68.5 | 73.9 | 85.3 | 73.5 |

| 5 | Des Moines, IA | 79.2 | 19.3% | 114% | 2.9 | 14.8% | 71.3% | 93.2 | 68.5 | 63.0 | 91.6 | 79.9 |

| 6 | Minneapolis, MN | 79.1 | 21.5% | 125% | 2.3 | 15.1% | 72.5% | 82.6 | 63.0 | 76.1 | 90.1 | 83.7 |

| 7 | Rochester, NY | 77.7 | 23.4% | 51% | 2.7 | 16.9% | 67.3% | 73.4 | 100.0 | 67.4 | 80.6 | 67.1 |

| 8 | Harrisburg, PA | 77.5 | 20.8% | 51% | 2.7 | 18.2% | 65.2% | 86.0 | 100.0 | 67.4 | 73.8 | 60.4 |

| 9 | Milwaukee, WI | 77.1 | 24.4% | 102% | 2.7 | 14.1% | 71.3% | 68.6 | 74.5 | 67.4 | 95.3 | 79.9 |

| 10 | Syracuse, NY | 75.3 | 22.4% | 51% | 2.6 | 18.7% | 64.2% | 78.3 | 100.0 | 69.6 | 71.2 | 57.2 |

| 11 | Pittsburgh, PA | 74.4 | 19.3% | 102% | 2.6 | 19.2% | 67.0% | 93.2 | 74.5 | 69.6 | 68.6 | 66.1 |

| 12 | Fayetteville, AR | 73.2 | 17.9% | 114% | 3.2 | 19.4% | 69.3% | 100.0 | 68.5 | 56.5 | 67.5 | 73.5 |

| 13 | Salt Lake City, UT | 73.0 | 22.5% | 114% | 1.9 | 19.0% | 66.4% | 77.8 | 68.5 | 84.8 | 69.6 | 64.2 |

| 14 | Boise, ID | 72.4 | 21.2% | 179% | 2.3 | 15.6% | 70.9% | 84.1 | 36.0 | 76.1 | 87.4 | 78.6 |

| 15 | Albany, NY | 72.3 | 22.2% | 102% | 2.3 | 19.6% | 66.7% | 79.2 | 74.5 | 76.1 | 66.5 | 65.2 |

| 16 | Wichita, KS | 72.2 | 19.7% | 102% | 3.3 | 17.1% | 65.5% | 91.3 | 74.5 | 54.3 | 79.6 | 61.3 |

| 17 | Cincinnati, OH | 71.8 | 21.0% | 114% | 3.2 | 17.0% | 67.9% | 85.0 | 68.5 | 56.5 | 80.1 | 69.0 |

| 18 | Kansas City, MO | 71.7 | 21.9% | 125% | 2.6 | 18.0% | 68.3% | 80.7 | 63.0 | 69.6 | 74.9 | 70.3 |

| 19 | Akron, OH | 71.4 | 21.8% | 114% | 3.0 | 18.3% | 69.2% | 81.2 | 68.5 | 60.9 | 73.3 | 73.2 |

| 20 | Omaha, NE | 70.9 | 22.2% | 135% | 2.6 | 17.5% | 68.3% | 79.2 | 58.0 | 69.6 | 77.5 | 70.3 |

| 21 | Toledo, OH | 70.6 | 21.1% | 51% | 3.5 | 19.3% | 62.1% | 84.5 | 100.0 | 50.0 | 68.1 | 50.5 |

| 22 | Columbus, OH | 70.3 | 22.5% | 114% | 2.9 | 18.1% | 67.6% | 77.8 | 68.5 | 63.0 | 74.3 | 68.1 |

| 23 | Chattanooga, TN | 70.1 | 20.1% | 147% | 3.2 | 18.8% | 71.9% | 89.4 | 52.0 | 56.5 | 70.7 | 81.8 |

| 24 | St. Louis, MO | 69.7 | 20.3% | 125% | 3.1 | 17.7% | 65.7% | 88.4 | 63.0 | 58.7 | 76.4 | 62.0 |

| 25 | Dayton, OH | 69.0 | 20.9% | 102% | 3.2 | 19.0% | 64.8% | 85.5 | 74.5 | 56.5 | 69.6 | 59.1 |

| 26 | Buffalo, NY | 68.3 | 22.5% | 51% | 3.0 | 22.2% | 61.9% | 77.8 | 100.0 | 60.9 | 52.9 | 49.8 |

| 27 | Spokane, WA | 67.5 | 25.2% | 161% | 2.6 | 14.8% | 67.1% | 64.7 | 45.0 | 69.6 | 91.6 | 66.5 |

| 28 | Raleigh, NC | 67.2 | 21.4% | 161% | 3.1 | 17.8% | 69.2% | 83.1 | 45.0 | 58.7 | 75.9 | 73.2 |

| 28 | Knoxville, TN | 67.2 | 19.4% | 135% | 3.5 | 20.8% | 69.7% | 92.8 | 58.0 | 50.0 | 60.2 | 74.8 |

| 30 | Seattle, WA | 67.0 | 26.9% | 135% | 2.0 | 20.5% | 70.1% | 56.5 | 58.0 | 82.6 | 61.8 | 76.0 |

| 31 | Indianapolis, IN | 66.5 | 21.3% | 114% | 3.2 | 19.6% | 64.3% | 83.6 | 68.5 | 56.5 | 66.5 | 57.5 |

| 32 | Denver, CO | 66.2 | 26.4% | 161% | 1.2 | 20.2% | 66.2% | 58.9 | 45.0 | 100.0 | 63.4 | 63.6 |

| 32 | Portland, OR | 66.2 | 27.4% | 161% | 2.4 | 15.4% | 68.1% | 54.1 | 45.0 | 73.9 | 88.5 | 69.6 |

| 34 | Provo, UT | 65.8 | 21.2% | 251% | 1.9 | 16.2% | 70.0% | 84.1 | 0.0 | 84.8 | 84.3 | 75.7 |

| 34 | Ogden, UT | 65.8 | 19.0% | 206% | 2.0 | 19.1% | 65.1% | 94.7 | 22.5 | 82.6 | 69.1 | 60.1 |

| 36 | Boston, MA | 65.3 | 28.3% | 114% | 2.0 | 21.2% | 67.4% | 49.8 | 68.5 | 82.6 | 58.1 | 67.4 |

| 37 | Hartford, CT | 65.1 | 25.7% | 102% | 2.3 | 21.5% | 63.8% | 62.3 | 74.5 | 76.1 | 56.5 | 55.9 |

| 38 | Cleveland, OH | 64.8 | 22.5% | 102% | 3.4 | 21.1% | 65.4% | 77.8 | 74.5 | 52.2 | 58.6 | 61.0 |

| 39 | San Francisco, CA | 64.5 | 30.6% | 125% | 1.7 | 23.2% | 72.7% | 38.6 | 63.0 | 89.1 | 47.6 | 84.3 |

| 40 | Allentown, PA | 63.8 | 24.3% | 125% | 2.7 | 20.4% | 64.2% | 69.1 | 63.0 | 67.4 | 62.3 | 57.2 |

| 41 | Louisville, KY | 63.7 | 21.1% | 114% | 3.5 | 21.5% | 64.7% | 84.5 | 68.5 | 50.0 | 56.5 | 58.8 |

| 41 | Tucson, AZ | 63.7 | 26.0% | 179% | 2.4 | 17.5% | 68.2% | 60.9 | 36.0 | 73.9 | 77.5 | 70.0 |

| 43 | Detroit, MI | 63.5 | 23.3% | 125% | 2.8 | 21.1% | 64.1% | 73.9 | 63.0 | 65.2 | 58.6 | 56.9 |

| 44 | Philadelphia, PA | 63.0 | 25.8% | 125% | 2.3 | 22.6% | 66.1% | 61.8 | 63.0 | 76.1 | 50.8 | 63.3 |

| 45 | Chicago, IL | 62.5 | 26.1% | 114% | 2.7 | 21.8% | 65.5% | 60.4 | 68.5 | 67.4 | 55.0 | 61.3 |

| 46 | Greenville, SC | 62.3 | 20.7% | 147% | 3.6 | 20.4% | 66.0% | 86.5 | 52.0 | 47.8 | 62.3 | 62.9 |

| 47 | Worcester, MA | 61.9 | 26.2% | 161% | 2.0 | 18.1% | 61.2% | 59.9 | 45.0 | 82.6 | 74.3 | 47.6 |

| 48 | Winston-Salem, NC | 61.5 | 20.7% | 147% | 3.6 | 19.8% | 63.7% | 86.5 | 52.0 | 47.8 | 65.4 | 55.6 |

| 49 | Tulsa, OK | 60.4 | 21.4% | 125% | 4.0 | 19.6% | 62.0% | 83.1 | 63.0 | 39.1 | 66.5 | 50.2 |

| 50 | Richmond, VA | 59.8 | 23.6% | 135% | 3.2 | 21.1% | 63.0% | 72.5 | 58.0 | 56.5 | 58.6 | 53.4 |

| 51 | Nashville, TN | 59.6 | 23.6% | 147% | 3.6 | 21.5% | 68.0% | 72.5 | 52.0 | 47.8 | 56.5 | 69.3 |

| 51 | Oklahoma City, OK | 59.6 | 23.2% | 125% | 3.6 | 20.2% | 61.8% | 74.4 | 63.0 | 47.8 | 63.4 | 49.5 |

| 53 | Birmingham, AL | 58.5 | 21.8% | 125% | 3.9 | 21.9% | 62.7% | 81.2 | 63.0 | 41.3 | 54.5 | 52.4 |

| 54 | Little Rock, AR | 58.2 | 21.5% | 125% | 3.9 | 21.2% | 60.7% | 82.6 | 63.0 | 41.3 | 58.1 | 46.0 |

| 55 | Baltimore, MD | 58.0 | 25.2% | 147% | 2.7 | 22.1% | 62.7% | 64.7 | 52.0 | 67.4 | 53.4 | 52.4 |

| 55 | Providence, RI | 58.0 | 27.1% | 161% | 2.2 | 21.3% | 63.0% | 55.6 | 45.0 | 78.3 | 57.6 | 53.4 |

| 57 | Washington, DC | 57.7 | 24.4% | 147% | 2.2 | 26.9% | 65.5% | 68.6 | 52.0 | 78.3 | 28.3 | 61.3 |

| 58 | Palm Bay, FL | 57.4 | 25.4% | 179% | 3.0 | 19.8% | 65.4% | 63.8 | 36.0 | 60.9 | 65.4 | 61.0 |

| 59 | Phoenix, AZ | 57.0 | 25.2% | 161% | 2.7 | 21.9% | 63.0% | 64.7 | 45.0 | 67.4 | 54.5 | 53.4 |

| 59 | New Haven, CT | 57.0 | 30.0% | 125% | 2.3 | 22.5% | 62.9% | 41.5 | 63.0 | 76.1 | 51.3 | 53.0 |

| 61 | Austin, TX | 56.5 | 26.7% | 135% | 2.9 | 24.7% | 66.4% | 57.5 | 58.0 | 63.0 | 39.8 | 64.2 |

| 62 | Greensboro, NC | 56.4 | 23.3% | 125% | 3.7 | 21.9% | 60.4% | 73.9 | 63.0 | 45.7 | 54.5 | 45.0 |

| 63 | Albuquerque, NM | 55.6 | 25.1% | 147% | 3.6 | 21.1% | 63.3% | 65.2 | 52.0 | 47.8 | 58.6 | 54.3 |

| 64 | North Port, FL | 55.3 | 27.6% | 251% | 2.5 | 18.8% | 71.6% | 53.1 | 0.0 | 71.7 | 70.7 | 80.8 |

| 64 | Colorado Springs, CO | 55.3 | 27.2% | 206% | 1.4 | 23.6% | 64.3% | 55.1 | 22.5 | 95.7 | 45.5 | 57.5 |

| 66 | Charlotte, NC | 54.5 | 23.0% | 147% | 3.5 | 24.0% | 62.4% | 75.4 | 52.0 | 50.0 | 43.5 | 51.4 |

| 67 | Jackson, MS | 53.9 | 24.0% | 125% | 4.4 | 21.5% | 61.6% | 70.5 | 63.0 | 30.4 | 56.5 | 48.9 |

| 68 | Dallas, TX | 52.9 | 27.6% | 125% | 3.1 | 24.7% | 61.9% | 53.1 | 63.0 | 58.7 | 39.8 | 49.8 |

| 69 | Cape Coral, FL | 51.6 | 29.4% | 206% | 3.0 | 19.9% | 66.7% | 44.4 | 22.5 | 60.9 | 64.9 | 65.2 |

| 70 | Baton Rouge, LA | 51.5 | 23.7% | 125% | 3.7 | 25.4% | 59.1% | 72.0 | 63.0 | 45.7 | 36.1 | 40.9 |

| 71 | Sacramento, CA | 50.6 | 30.7% | 179% | 2.4 | 21.5% | 61.5% | 38.2 | 36.0 | 73.9 | 56.5 | 48.6 |

| 71 | Kiryas Joel, NY | 50.6 | 30.3% | 179% | 2.2 | 23.5% | 62.7% | 40.1 | 36.0 | 78.3 | 46.1 | 52.4 |

| 73 | Atlanta, GA | 49.9 | 26.1% | 147% | 3.2 | 25.7% | 60.7% | 60.4 | 52.0 | 56.5 | 34.6 | 46.0 |

| 74 | Tampa, FL | 49.5 | 28.8% | 161% | 3.1 | 23.2% | 61.6% | 47.3 | 45.0 | 58.7 | 47.6 | 48.9 |

| 74 | San Diego, CA | 49.5 | 35.4% | 179% | 2.0 | 22.9% | 66.4% | 15.5 | 36.0 | 82.6 | 49.2 | 64.2 |

| 76 | New York, NY | 49.2 | 34.2% | 102% | 1.9 | 30.0% | 63.0% | 21.3 | 74.5 | 84.8 | 12.0 | 53.4 |

| 77 | Charleston, SC | 49.1 | 25.5% | 179% | 3.4 | 24.2% | 62.4% | 63.3 | 36.0 | 52.2 | 42.4 | 51.4 |

| 78 | Honolulu, HI | 49.0 | 33.4% | 206% | 2.1 | 22.0% | 66.0% | 25.1 | 22.5 | 80.4 | 53.9 | 62.9 |

| 79 | Augusta, GA | 48.6 | 22.2% | 161% | 4.3 | 22.1% | 56.6% | 79.2 | 45.0 | 32.6 | 53.4 | 32.9 |

| 80 | Orlando, FL | 48.3 | 31.4% | 147% | 3.2 | 23.8% | 63.1% | 34.8 | 52.0 | 56.5 | 44.5 | 53.7 |

| 81 | Deltona, FL | 47.8 | 27.7% | 251% | 3.3 | 19.5% | 66.7% | 52.7 | 0.0 | 54.3 | 67.0 | 65.2 |

| 82 | Bridgeport, CT | 47.2 | 31.6% | 161% | 1.8 | 29.9% | 64.4% | 33.8 | 45.0 | 87.0 | 12.6 | 57.8 |

| 83 | Bakersfield, CA | 46.9 | 33.1% | 161% | 2.9 | 18.5% | 55.0% | 26.6 | 45.0 | 63.0 | 72.3 | 27.8 |

| 84 | Jacksonville, FL | 46.8 | 26.5% | 179% | 3.5 | 24.7% | 61.8% | 58.5 | 36.0 | 50.0 | 39.8 | 49.5 |

| 85 | Fresno, CA | 46.7 | 31.9% | 161% | 2.7 | 21.5% | 56.4% | 32.4 | 45.0 | 67.4 | 56.5 | 32.3 |

| 86 | Houston, TX | 46.3 | 28.1% | 114% | 3.6 | 27.1% | 57.9% | 50.7 | 68.5 | 47.8 | 27.2 | 37.1 |

| 87 | Virginia Beach, VA | 45.9 | 27.8% | 179% | 3.4 | 22.7% | 58.4% | 52.2 | 36.0 | 52.2 | 50.3 | 38.7 |

| 88 | New Orleans, LA | 45.4 | 31.3% | 114% | 3.5 | 25.7% | 58.4% | 35.3 | 68.5 | 50.0 | 34.6 | 38.7 |

| 89 | Memphis, TN | 45.3 | 27.5% | 114% | 4.3 | 24.8% | 56.5% | 53.6 | 68.5 | 32.6 | 39.3 | 32.6 |

| 89 | Columbia, SC | 45.3 | 23.5% | 147% | 3.8 | 26.5% | 54.9% | 72.9 | 52.0 | 43.5 | 30.4 | 27.5 |

| 91 | Las Vegas, NV | 45.1 | 32.0% | 161% | 2.5 | 26.9% | 61.5% | 31.9 | 45.0 | 71.7 | 28.3 | 48.6 |

| 92 | Oxnard, CA | 45.0 | 33.0% | 251% | 1.9 | 23.1% | 66.6% | 27.1 | 0.0 | 84.8 | 48.2 | 64.9 |

| 93 | Los Angeles, CA | 44.9 | 37.9% | 161% | 2.0 | 25.2% | 64.0% | 3.4 | 45.0 | 82.6 | 37.2 | 56.5 |

| 94 | San Antonio, TX | 42.5 | 26.9% | 161% | 4.0 | 25.5% | 57.6% | 56.5 | 45.0 | 39.1 | 35.6 | 36.1 |

| 95 | Lakeland, FL | 38.3 | 27.0% | 206% | 3.5 | 25.3% | 54.5% | 56.0 | 22.5 | 50.0 | 36.6 | 26.2 |

| 96 | Stockton, CA | 37.0 | 31.2% | 206% | 2.8 | 25.6% | 54.6% | 35.7 | 22.5 | 65.2 | 35.1 | 26.5 |

| 97 | Miami, FL | 34.1 | 38.6% | 147% | 3.0 | 29.9% | 60.4% | 0.0 | 52.0 | 60.9 | 12.6 | 45.0 |

| 98 | Riverside, CA | 31.1 | 33.2% | 251% | 2.8 | 26.0% | 56.0% | 26.1 | 0.0 | 65.2 | 33.0 | 31.0 |

| 99 | El Paso, TX | 28.5 | 27.9% | 161% | 3.7 | 32.3% | 46.3% | 51.7 | 45.0 | 45.7 | 0.0 | 0.0 |

| 100 | McAllen, TX | 28.0 | 24.3% | 147% | 5.8 | 29.7% | 47.9% | 69.1 | 52.0 | 0.0 | 13.6 | 5.1 |

How consumers can spend within their means

Maintaining good financial habits isn’t always easy, especially with today’s rising costs. But staying on top of your spending and minimizing debt can reduce stress, help you reach life goals and keep you better prepared for unexpected expenses.

Schulz offers the following five tips to help keep your spending in check:

- Know where your money is going. It’s hard to make smart choices if you’re guessing. Look at a month or two of spending and identify what’s helping you, what’s hurting you and what’s happening out of habit.

- Prioritize ruthlessly. Spend on the things that matter to you and bring real value to your life, then be just as intentional about cutting back on the things that don’t. A good budget should be a reflection of your priorities, so be thoughtful in creating it.

- Pay yourself first. Treat savings like a must-pay bill, even if you’re starting small. Building that habit gives you more breathing room and makes it easier to avoid leaning on credit cards when life gets expensive.

- Make a list. It sounds simple, but it helps. Impulse purchases wreck budgets. Making a list of what you want to buy on that shopping trip can help you stay focused on what you’re there to buy.

- Lower your interest, if at all possible. High interest rates are a killer for those with credit card debt. The good news is, you may have options to rein in rates a bit. A 0% balance transfer credit card can be among the best weapons in your battle against credit card debt, though you’ll likely need good credit to get one. If you don’t qualify, consolidating your debts with a low-interest personal loan can be a great option, too. You can even call your credit card issuer and ask for a lower rate on your credit card, even if it’s just temporarily.

Methodology

LendingTree analysts scored the 100 largest U.S. metros on five metrics:

- Percentage of households spending at least 35% of their income on housing costs, based on U.S. Census Bureau 2024 American Community Survey five-year estimates

- Household debt-to-income (DTI) ratio, based on Federal Reserve data from the fourth quarter of 2025, the latest available; Connecticut metros use fourth-quarter 2022 data because of a reporting geography change

- Credit inquiries in the previous two years, based on a sample of about 260,000 anonymized LendingTree users from Jan. 1 to March 31, 2026

- Percentage of cardholders with at least one maxed-out card, based on a sample of about 260,000 anonymized LendingTree users from Jan. 1 to March 31, 2026

- Percentage of cardholders with credit utilization below 30%, based on a sample of about 260,000 anonymized LendingTree users from Jan. 1 to March 31, 2026

All metrics were evenly weighted to create a final score. Credit inquiry averages were calculated using all consumers in the sample. Maxed-out card and credit utilization metrics were calculated only among consumers in the sample with at least one active credit card.

Researchers used U.S. Census Bureau 2024 American Community Survey five-year estimates to identify the 100 largest metros.

Get debt consolidation loan offers from up to 5 lenders in minutes