Younger Generations Prioritize Homeownership Over Major Milestones Like Marriage or Kids

Move over, wedding bells and baby showers — the American dream prioritizes keys to a front door over the rest of the white picket fence life.

According to the latest LendingTree survey of nearly 2,000 U.S. Gen Zers and millennials, hopeful young homebuyers are putting off major life events like marriage and parenthood until they buy a home. And for 60% of these nonhomeowners, that’ll take at least three years.

Here’s what else we found.

Key findings

- Most young Americans aren’t homeowners, and those who want to buy face major hurdles. Just 40% of Gen Zers and millennials currently own a home, though 84% of those who’ve never owned say they want to in the future. When asked about their biggest hurdles, 27% of those who want to buy in the future cite low income and 25% cite home prices. Additionally, 68% of this group say high mortgage interest rates have affected their interest or their ability to buy a home.

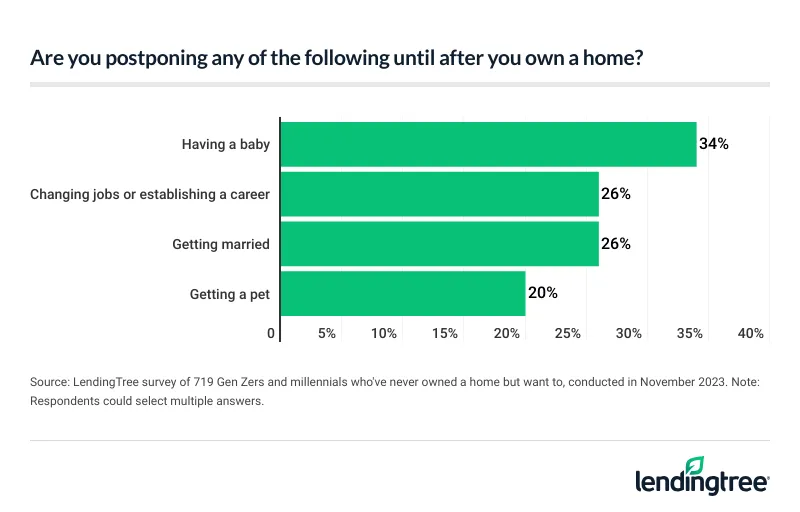

- Some hopeful homebuyers are putting off other major milestones until they own. 48% of Gen Zers and 25% of millennials among this group are waiting to have a baby until after they buy, while 36% of Gen Zers and 21% of millennials are postponing marriage until after they sign a deed. Additionally, over a quarter (26%) of these young Americans are delaying a job or career change until they purchase a home.

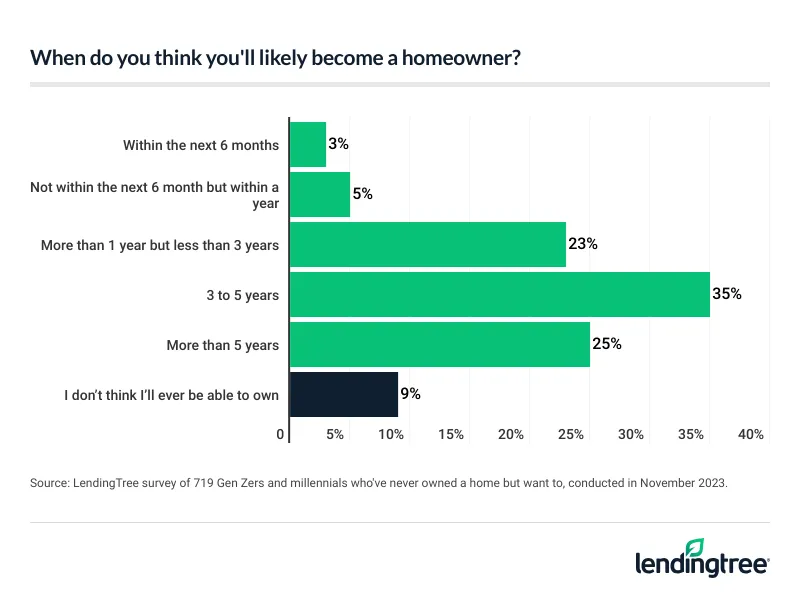

- Most of these young Americans don’t see themselves being able to purchase anytime soon. Just 7% of prospective Gen Z and millennial homebuyers think they’ll likely buy within the next year, while 60% think it’ll take at least three years. Additionally, 9% don’t think they’ll ever be able to call themselves homeowners. When asked about their largest financial obligations, 43% of hopeful homebuyers cite rent, 17% cite credit card debt and 13% cite student loan debt.

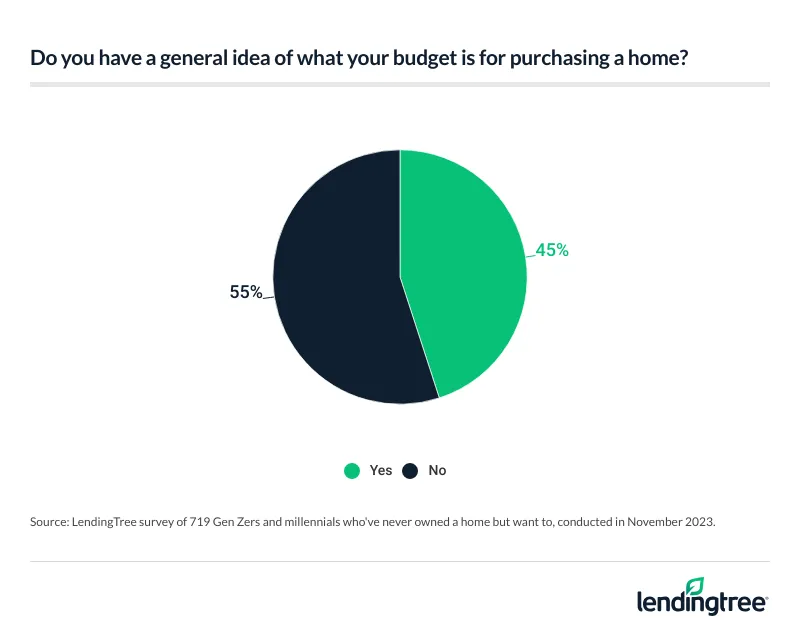

- More than half of prospective buyers don’t know their budget. 55% of young Americans who want to buy say they don’t have even a general idea of their budget. Among those with a budget, 57% hope to purchase for less than $250,000 and 87% put their budget under $500,000. Beyond budgets, most (58%) of the hopeful buyers admit they don’t have a good understanding of all the costs involved.

Young Americans struggle to buy a home

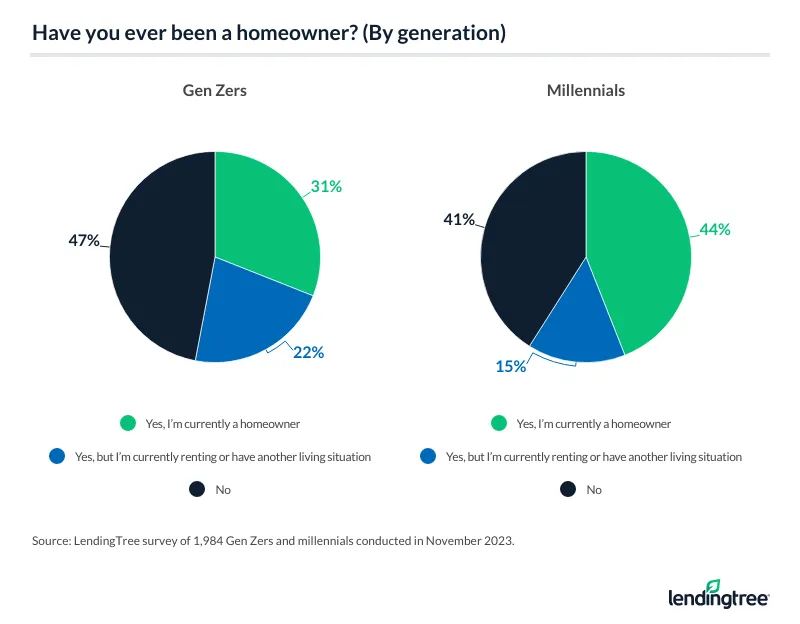

Homeownership has always been a major goal for most Americans, but most young Americans aren’t quite there yet. In fact, just 40% of Gen Zers (ages 18 to 26 at the time of the November 2023 survey) and millennials (ages 27 to 42) currently own a home. Unsurprisingly, millennials (44%) are more likely to be homeowners than Gen Zers (31%).

However, 84% of young Americans who’ve never owned a home say they want to in the future. That’s especially true of young Americans with children younger than 18 (91%), those who are married or in a domestic partnership (91%) and those making $50,000 to $74,999 a year (90%).

When asked about their biggest hurdles, low income (27%) and home prices (25%) were the most common responses. That’s followed by:

- Lack of savings (10%)

- Low credit score (8%)

- Outstanding debt obligations (5%)

- Other (4%)

- Lack of knowledge about the process (4%)

- Low housing inventory (3%)

- Self-employment (3%)

- Desire for marriage first (2%)

- Job history (2%)

What’s more, 68% of this group say high mortgage interest rates have affected their interest or their ability to buy a home, though that’s particularly true for those earning $50,000 to $74,999 (75%) or $35,000 to $49,999 (73%). Additionally, women (71%) are much more concerned about interest rates than men (62%), while millennials (71%) are more concerned than Gen Zers (61%).

LendingTree senior economist Jacob Channel says these concerns are well-founded.

“Though I wish it weren’t the case, high home prices and relatively high mortgage rates are valid concerns, not just for younger buyers but for almost anyone looking to buy a home with a mortgage,” he says. “Fortunately, it’s not all bad news. Keep in mind that as you age, you tend to make more money as you become more established in your career.”

Peak earning years vary quite a bit, but many people don’t see their incomes reach their highest levels until their mid-40s to 50s, according to the U.S. Bureau of Labor Statistics (BLS).

Not only that, but Channel notes you may also have more opportunities to save as you reach middle age and beyond. After all, common expenses you may incur when you’re younger, like child care costs or student loan payments, can drop off considerably as your children get older and as you pay off more of your student loans.

“Just because you can’t afford to buy a home in your 20s or 30s doesn’t mean you’ll never be able to buy,” he says. “So, while it’s no fun for younger generations to put their homebuying aspirations on hold, becoming a homeowner won’t forever be out of their reach. Ultimately, by being responsible and doing your best to save and pay down debt when you’re young, you can set yourself up for a lot of financial success in the future.”

To some, parenthood and marriage aren’t as important as homeownership

For some, homeownership is more important than other major life milestones. Among hopeful homebuyers, 48% of Gen Zers and 25% of millennials are waiting to have a baby until after they buy, while 36% of Gen Zers and 21% of millennials are postponing marriage.

Beyond that, 26% of these young Americans are delaying a job or career change until they purchase a home. That’s particularly true for men (31%). Meanwhile, 20% of these young Americans are putting off getting a pet.

Channel believes putting off major milestones can be reasonable, though only to an extent.

“There’s nothing inherently helpful or harmful about putting off getting married or having kids until you own a home,” he says. “In some cases, it makes sense. After all, buying a house is typically stressful, and it can be made even more difficult if you’re doing it at the same time that you’re changing jobs, planning a wedding or raising your kids.”

That said, Channel believes you shouldn’t assume every major life event will suddenly get easier just because you’re a homeowner. “If you wait too long to do something that you want to do like get married, have kids or change your job, you could shoot yourself in the foot,” he says. “Don’t let not owning a home stop you from pursuing an opportunity that could help you better your financial and emotional well-being.”

Majority of young Americans don’t expect to be homeowners for years

Despite the desire (and the lengths they’re willing to go to), most young Americans don’t expect to buy a home anytime soon. Among these hopeful homebuyers, just 7% think they’ll likely buy within the next year. On the other hand, 23% think it’ll take more than a year but less than three years and 60% think it’ll take at least three years.

Millennials (27%) are more likely than Gen Zers (17%) to say they expect to buy in more than a year but less than three years, while Gen Zers (69%) are more likely than millennials (55%) to say it’ll take at least three years.

Meanwhile, 9% of young Americans don’t think they’ll ever be able to call themselves homeowners.

According to Channel, more young Americans might be able to buy this year than they might currently believe.

“From where things currently stand, it looks like 2024 might be easier on would-be homebuyers than 2023 was,” he says. “That’s because mortgage rates should come down even if home prices remain steep. On top of that, inflation growth should continue to cool, meaning people won’t need to worry as much about the cost of necessities like food dramatically spiking.”

This doesn’t mean buying is going to be easy, Channel warns. Rather, people should understand they’ll probably need to give themselves plenty of time to do things like pay down other debts and save up for a down payment.

Of course, other financial obligations may present the biggest hurdle to saving up for a home. When asked about their largest financial obligations, rent (43%), credit card debt (17%) and student loan debt (13%) were the most common responses. That’s followed by:

- Children and related expenses (7%)

- Auto loan debt (4%)

- Medical debt (2%)

55% of young hopeful homeowners don’t know their budget

When it comes to homebuying, the budget is half the battle. However, more than half (55%) of young Americans who want to buy say they don’t have a general idea of their budget. That’s especially true of women (61%), those earning less than $35,000 (61%) and Gen Zers (60%).

Depending on where you are in the homebuying process, Channel believes not having a budget might not be a big deal. “A big part of the initial stages of finding a home is sitting down and figuring out what you can afford to spend on a mortgage each month,” he says. “If you’re really lost, meeting with a Realtor or using an online home affordability calculator can help you shed more light on what your budget will likely be.”

That said, if you’re actively touring homes or trying to make an offer on a home before you’ve nailed down your budget, Channel says you’re almost certainly going to have a bad time. “If you rush through the homebuying process without carefully considering what you can afford, you might end up stuck with a mortgage you seriously struggle (or even outright fail) to pay off,” he says.

Among those with a budget, 87% put their budget at under $500,000, with 57% aiming to purchase at less than $250,000. To break that down even further:

- 21% have a budget under $100,000

- 36% have a budget between $100,000 and $249,999

- 30% have a budget between $250,000 and $499,999

- 11% have a budget between $500,000 and $749,999

- 2% have a budget between $750,000 and $999,999

- 1% have a budget over $1 million

Budgets aside, 58% admit they don’t understand all the costs involved in buying a home, leaving 42% who believe they have a good or very good understanding. Men are the most likely to have confidence, with 14% believing they have a very good understanding of homebuying costs.

Saving up for a home? Top expert tips for young Americans

While becoming a homeowner is a great goal, it’s important to remember that buying a home is often a long process. For young Americans saving up, Channel recommends the following:

- Don’t rush. “Odds are, whether you end up buying tomorrow or 10 years from now, there will probably be homes on the market,” he says. “If you’re not in a place where you can comfortably afford a home, or if you’d rather prioritize other goals over homeownership, then it’s perfectly OK to wait to buy.”

- Budget. “While you don’t have to have an itemized list of every single expense you’ll likely incur when buying a home, a general (but realistic) budget is extremely helpful,” Channel says. “Be honest with yourself about how much you can afford to spend on things like a down payment or a mortgage payment and remember doing things like burning through every penny of your savings just to purchase property or buying under the assumption that you’ll get a big raise in the near future are often recipes for disaster.”

Methodology

LendingTree commissioned QuestionPro to conduct an online survey of 1,984 Gen Zers and millennials ages 18 to 42 from Nov. 16 to 20, 2023. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. Researchers reviewed all responses for quality control.

We defined generations as the following ages in 2023:

- Generation Z: 18 to 26

- Millennial: 27 to 42

View mortgage loan offers from up to 5 lenders in minutes