Climate Risks Are Reshaping Homeownership in America

Americans are increasingly feeling the effects of climate change where it matters most to them: their homes.

Growing concerns about extreme weather and rising insurance costs are reshaping how people think about homeownership and where they choose to live. In fact, 30% of homeowners have decided not to buy or make an offer on a home due to concerns about hazard risks, according to our survey of 2,060 U.S. consumers.

- Americans are significantly concerned about the impact of climate change on their homes. 68% of homeowners are worried that climate-related hazards could impact their home in the next 10 years. Additionally, 72% of Americans think climate risks will get worse over the next decade. The hazards that Americans are most concerned about are power outages from extreme weather (40%), winter storms and extreme cold (36%), and severe storms (34%).

- Most Americans have experienced a climate-related hazard in their area in the past five years. 88% say they’ve endured some form of a climate-related hazard in that period. Of those who did, 27% say it caused damage, and 18% say it forced repairs.

- Climate risks are impacting where young Americans choose to live. 30% of homeowners have decided not to buy or make an offer on a home because of hazard risk concerns. That percentage rises to 62% among Gen Zers. Additionally, 25% of Gen Zers are considering moving in the next two years because of climate risk, while 32% of this age group say they have already done so.

- Climate change is becoming a costly reality. 56% of those with home insurance say their premiums have increased in the past year, while 30% say it’s likely they’ll be dropped by their insurer due to local hazard risk. Further, 32% of Americans would choose a home with higher insurance costs in a low-risk area compared to a home with lower costs in a high-risk area.

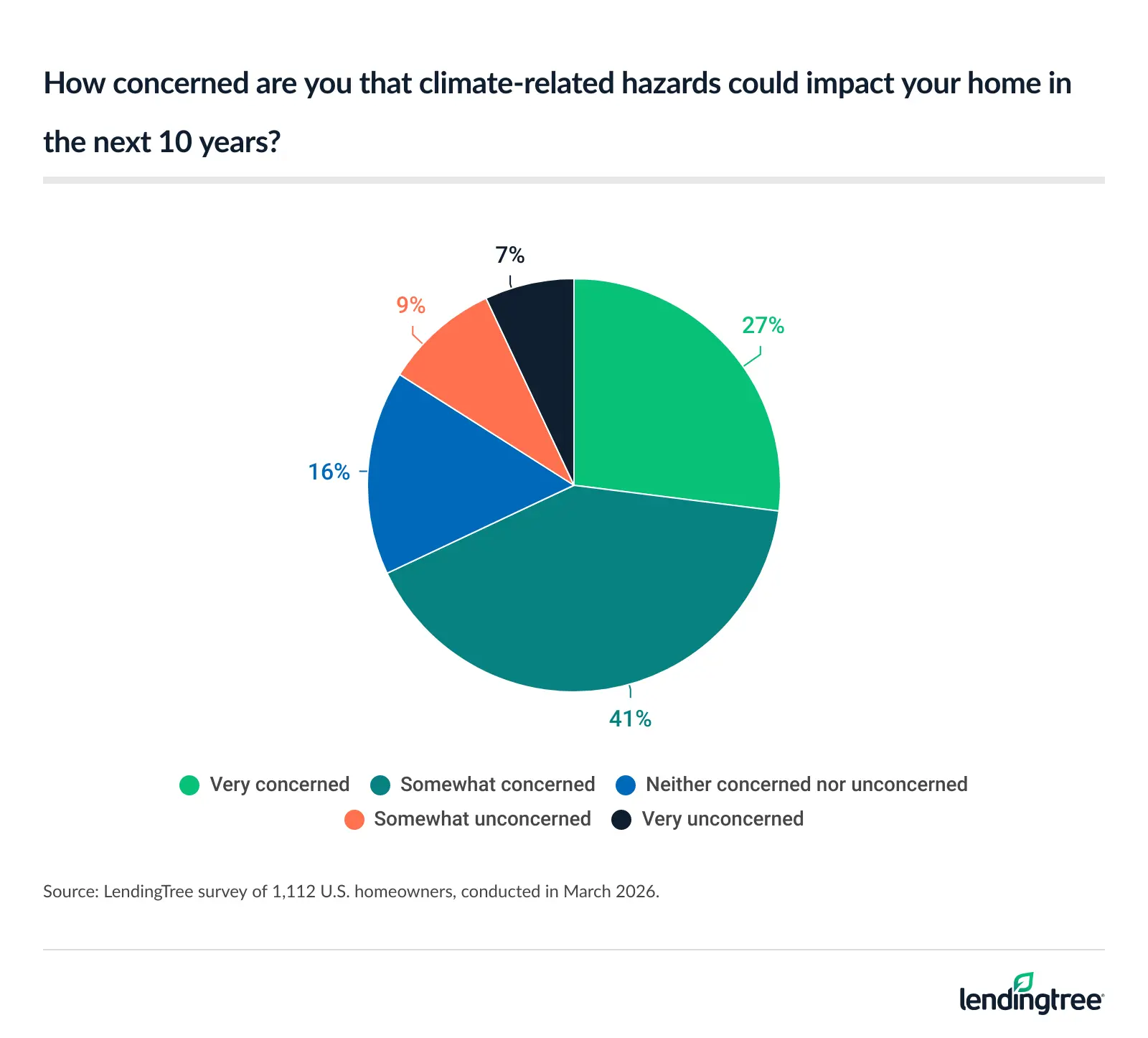

68% of homeowners worry about climate-related hazards

Americans are increasingly concerned about how climate change could affect their homes. Nearly 7 in 10 (68%) homeowners worry that climate-related hazards may impact their property within the next decade.

This concern extends beyond immediate risks. Across all Americans, 72% believe that climate-related threats will intensify over the next 10 years, and 60% say extreme weather risks are already increasing in areas where they might choose to live.

Among the most pressing concerns are power outages caused by severe weather (40%), winter storms and extreme cold (36%), and severe storms (34%). That’s followed by:

- Extreme heat (32%)

- Flooding (23%)

- Poor air quality or smoke (22%)

- Drought/water scarcity (19%)

- Hurricane and tropical storm (19%)

- Wildfire (16%)

- Coastal flooding and sea level rise (11%)

- Earthquake (9%)

- Landslide (5%)

These concerns align with industry data: According to the Insurance Information Institute, wind and hail are the leading causes of home insurance claims. As LendingTree home insurance expert and licensed insurance agent Rob Bhatt explains, “More than 40% of claims payments are for wind and hail damage, making them the most significant drivers of loss for homeowners.”

However, it’s also important to note that not all climate-related risks are covered equally by standard homeowners insurance.

“Homeowners insurance doesn’t cover floods,” Bhatt says. “That means many Americans may need separate policies to fully protect against certain climate-related hazards, like wind and hail coverage.”

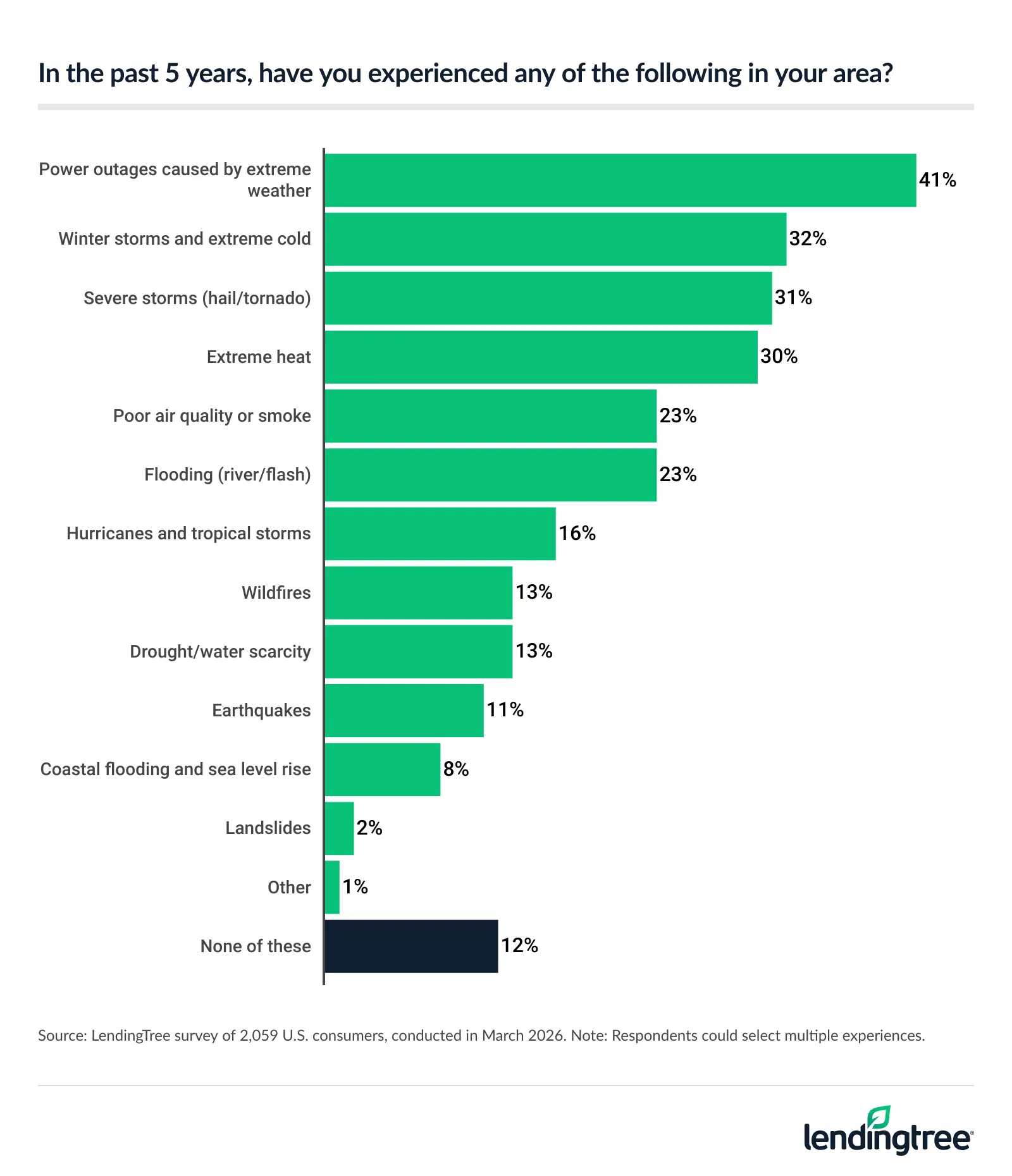

Majority of Americans have experienced a climate hazard

Within the past five years, 88% of Americans have endured some form of a climate-related hazard. The most common events experienced include power outages caused by severe weather (41%), winter storms (32%), severe storms (31%) and extreme heat (30%).

These experiences span a wide range of living situations. A majority (61%) of respondents live in single-family homes, while 21% live in apartments. Geographically, 45% are in suburban areas, 32% in urban areas and 23% in rural communities — meaning climate-related impacts are being felt across housing types and regions alike.

Among those who have been affected, 27% say these events caused damage, and 18% report that they needed to make repairs as a result.

Filing insurance claims for damage and repairs is a common pain point for policyholders, Bhatt says, particularly among those who don’t have a home inventory. “It may seem daunting, but all you have to do is turn on your smartphone camera and walk through your home taking pictures or video of your belongings, including serial numbers and model numbers,” he says. “You can then list your items on a spreadsheet, along with their approximate value.”

If you ever need to make a claim, having a home inventory ready to go allows you to quickly give your insurance company the information it needs to process your claim. Just make sure you store your inventory in a location you can easily access after a disaster, like on a cloud server.

3 in 10 chose not to buy a home due to climate risks

Climate risks are increasingly shaping where Americans choose to live — especially for younger generations.

Overall, 30% of homeowners say they’ve decided not to buy or make an offer on a home due to concerns about hazard risk. That share climbs significantly among younger buyers, with 62% of Gen Zers (ages 18 to 29) and 46% of millennials (ages 30 to 45) reporting that they’ve walked away from a property for this reason.

Climate concerns are also influencing relocation decisions. Nearly 1 in 5 (18%) Americans are considering moving within the next two years due to climate risk, while 17% say they’ve already moved for that reason. Gen Zers are the most proactive, with 25% considering a move and 32% having already relocated because of these risks. Those figures are similar among millennials, at 26% and 25%, respectively.

As climate risks become a more central factor in housing decisions, Americans are calling for greater transparency during the homebuying process. The most commonly requested disclosures include flood zone or flood risk ratings (73%) and past flooding or wildfire damage (72%). That’s followed by:

- Prior wind, hail or storm damage (66%)

- Local hazard history (66%)

- Wildfire risk rating (66%)

- Whether the property is in an evacuation zone (66%)

- Estimated insurance costs (63%)

- Insurance availability constraints (63%)

Bhatt believes it’s definitely worth keeping climate risks in mind as you shop for a home, particularly major or obvious risks.

“Interestingly, you can learn a little about a property’s past claims when you get a homeowners insurance quote for it,” he says. “Most quoting systems will flag information about recent claims at a home, as these can increase the price of insuring it, even if the claim was filed by a previous owner.”

To get this information, though, “it may be better to work with a live agent, rather than going through the entire process online,” Bhatt advises.

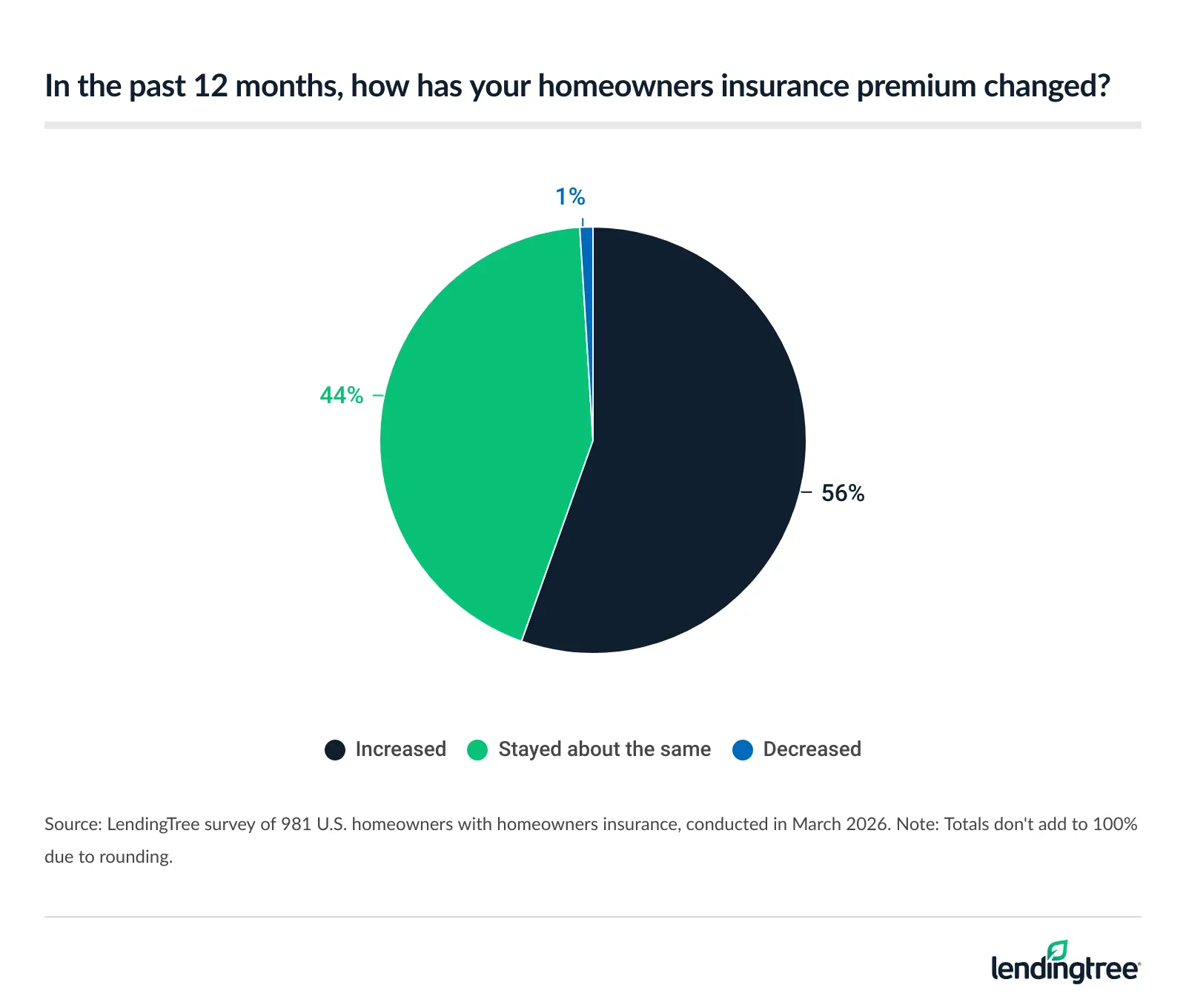

Impact on insurance is costly

Climate change isn’t only worrisome — it’s increasingly translating into higher costs for homeowners. While 88% of homeowners have home insurance, more than half (56%) of those policyholders say their premiums have gone up over the past year.

Concerns about future coverage are also growing, as 30% believe it’s likely they could be dropped by their insurer due to local hazard risk.

As a result, many Americans are rethinking their priorities when choosing where to live. Almost one-third (32%) say they would opt for a home with higher insurance costs in a lower-risk area rather than a less expensive option in a higher-risk location. This preference is even more pronounced among those with children under the age of 18 (46%), as well as among Gen Zers (43%) and millennials (41%).

Regardless, it’s always important to factor insurance costs into your overall homebuying and ownership expenses, Bhatt says. “Some of this is already done for you,” he says. “When you get a mortgage, your lender uses your household income to determine how much of a loan you can afford, based on your estimated PITI (principal, interest, taxes and insurance) payments.”

While home insurance used to be an afterthought, Bhatt says that these days, insurance has become so expensive that it is now necessary to think about it ahead of time. “The cost of homeowners insurance is going to affect your PITI payments and the amount you can borrow,” Bhatt explains. “Buying a home in an area with high insurance costs means you may have to choose a lower-priced home. Buying in an area with lower insurance costs may help you afford a higher-priced home.”

3 tips to protect both your home and finances amid climate change

As climate risks and insurance costs rise, there are practical steps that homeowners can take to better protect both their property and their finances. We offer the following guidance:

- Strengthen your home against local risks. “It’s good to reinforce your home to withstand the risks in your area,” Bhatt says. “Impact-resistant roofs are a smart investment in regions prone to hail, while fire-resistant materials are often worth the cost in wildfire-prone areas. Upgrades like these can go a long way in minimizing potential damage from natural disasters.”

- Be strategic about filing insurance claims. “Avoid filing claims for smaller repairs you can afford to handle out of pocket,” Bhatt advises. “Most claims will cause your premiums to rise, and multiple claims within a short period could even lead to your insurer dropping your coverage. It’s generally best to reserve insurance for major losses you wouldn’t be able to cover on your own.”

- Adjust your deductible and compare options regularly. “Choosing a higher deductible is one of the simplest ways to lower your insurance premium,” Bhatt explains. “Just make sure you have enough savings set aside to cover that out-of-pocket cost if needed. It’s also wise to shop around every few years — or anytime your rate increases significantly — as pricing models and your eligibility can change over time.”

Methodology

LendingTree commissioned QuestionPro to conduct an online survey of 2,060 U.S. consumers ages 18 to 80 on March 17-23, 2026. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. Researchers reviewed all responses for quality control.

We defined generations as the following ages in 2026:

- Generation Z: 18 to 29

- Millennials: 30 to 45

- Generation X: 46 to 61

- Baby boomers: 62 to 80

Recommended Articles