22.1% of New US Businesses Close Within a Year — Here’s Where They Fail Fastest

More than 1 in 5 U.S. businesses fail in their first year, according to U.S. Bureau of Labor Statistics (BLS) data. To put that into perspective, there are 36.2 million small businesses nationwide, which means hundreds of thousands of new ones are closing yearly.

To determine where businesses fail at higher rates, LendingTree researchers examined state and industry data. Here’s what we found, plus some tips for how those considering starting a business can boost their chances of success.

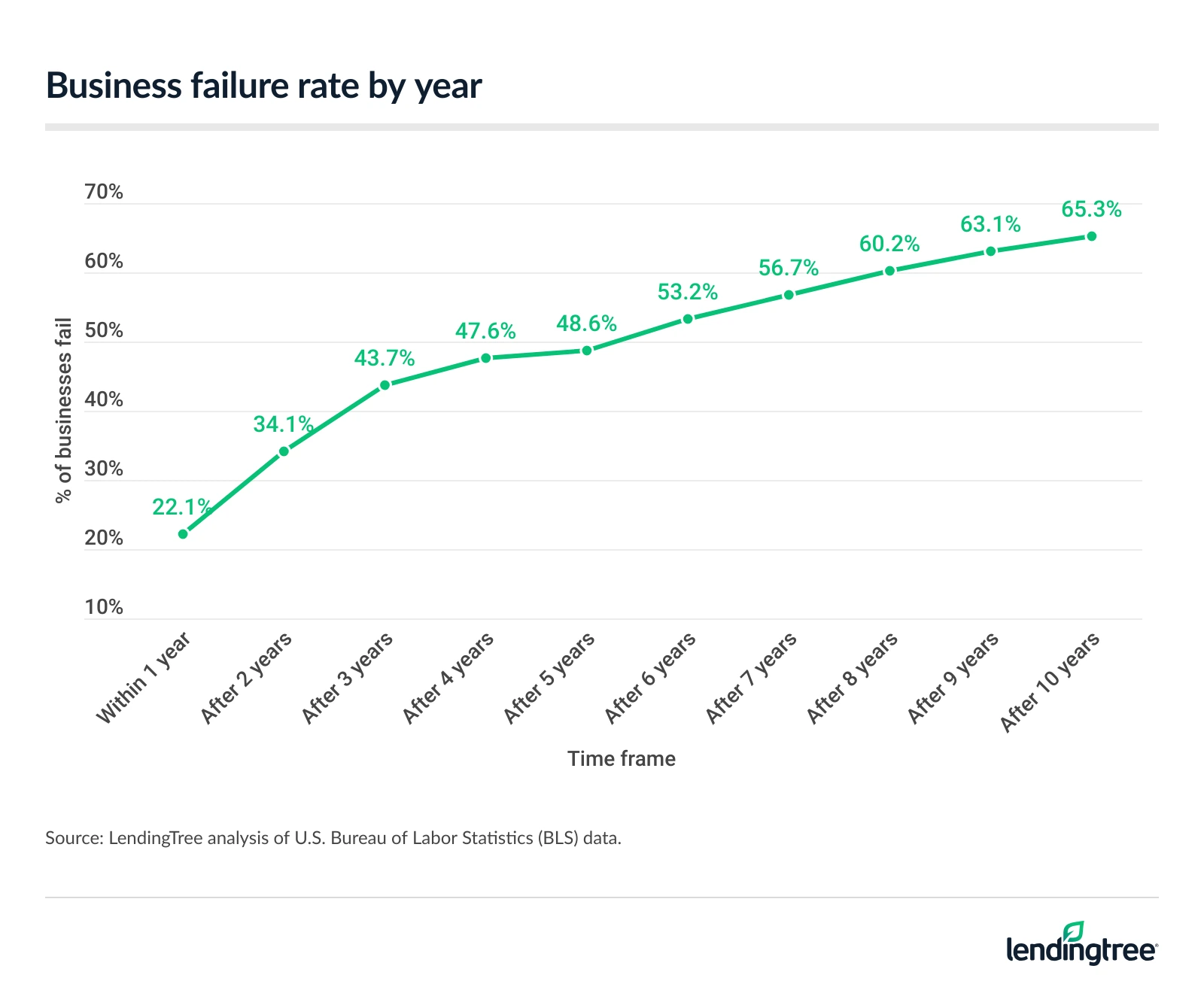

- 22.1% of new private-sector businesses in the U.S. fail within their first year. After five years, nearly half (48.6%) close. And after 10 years, about two-thirds (65.3%) are no longer operating. Of the nearly 1 million newly opened businesses in the latest data, 218,861 closed within their first year — roughly 600 a day.

- The District of Columbia has the highest first-year business failure rate, with nearly one-third of new businesses (32.9%) closing within 12 months. Tennessee (29.3%) and Delaware (27.2%) follow.

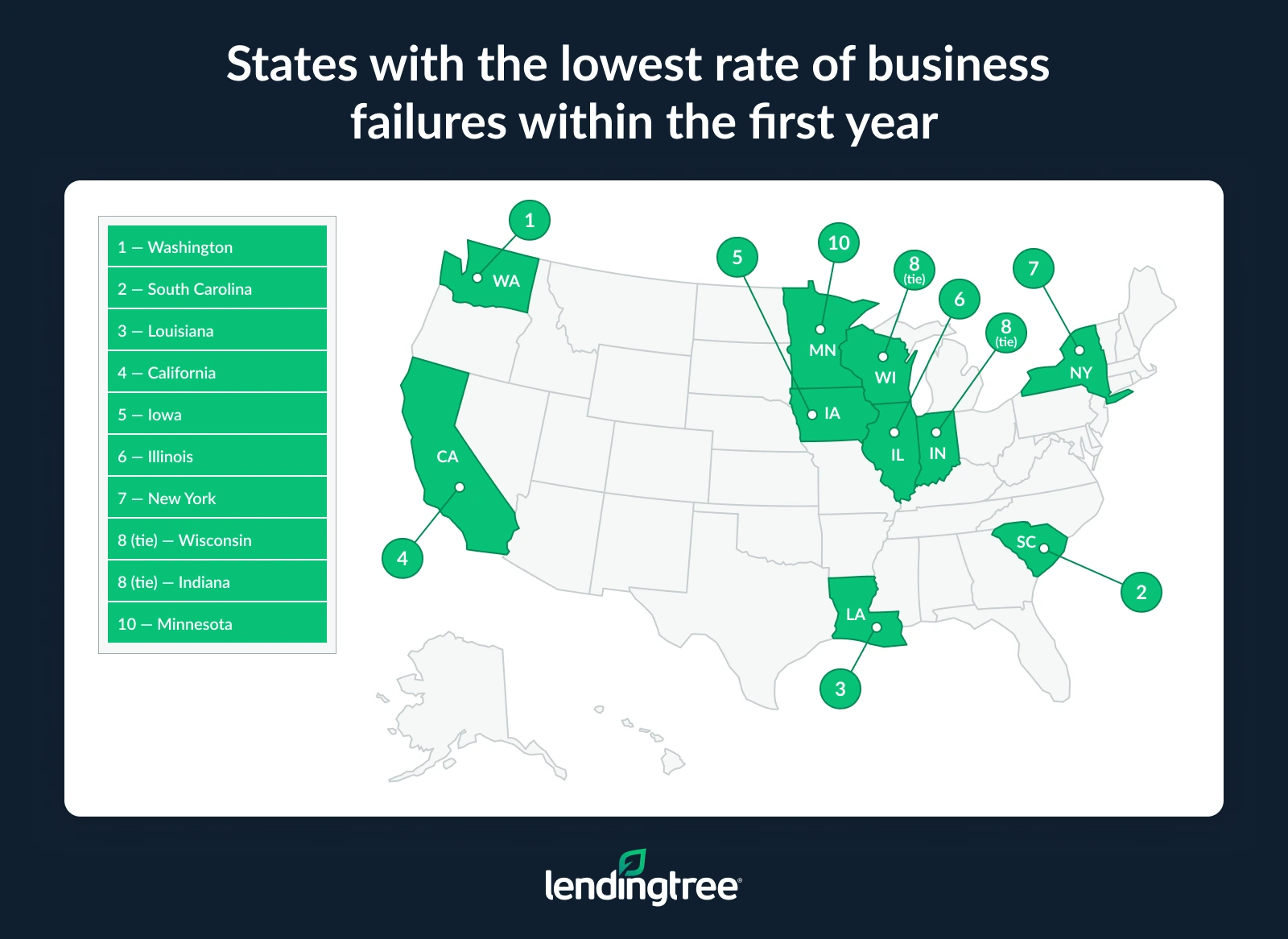

- Washington state has the lowest first-year business failure rate at 17.5%, followed closely by South Carolina (17.7%) and Louisiana (19.6%). In total, 21 states have first-year failure rates below the national average of 22.1%.

- The information industry has the highest failure rate for new businesses, with 28.4% not surviving thefirst year. Professional, scientific and technical services (25.5%) and administrative and waste services (24.3%) also rank among the most challenging industries for new businesses.

22.1% of businesses fail in the first year

Looking at new data from March 2024 to March 2025, 22.1% of new private-sector businesses in the U.S. fail within their first year. That’s up from 21.5% when we compared March 2023 to March 2024.

For context, there are 36.2 million small businesses in the U.S. as of 2025. Of the nearly 1 million new businesses opened in the latest data, 218,861 closed within their first year — roughly 600 a day.

The percentage of businesses closing rises to 48.6% after five years. After 10 years, a whopping 65.3% are no longer operating.

Matt Schulz, LendingTree chief consumer finance analyst and author of “Ask Questions, Save Money, Make More: How to Take Control of Your Financial Life,” says that failure is often the result of not understanding your market.

“One of the biggest problems is going in without a real focus on what you’re trying to accomplish and who you’re trying to serve,” he says. “Starting a business is hard and incredibly risky. If you don’t have a plan for the audience you’re targeting and what problem you’re helping those people solve, your odds of success just get smaller and smaller.”

While starting up a business may feel easy, it can be a different story when it comes to keeping it open. “Yes, it’s easier and cheaper than ever to start a small business,” Schulz says. “However, that just means that things are perhaps more competitive than ever, too, making it even more imperative that you approach that business with a well-thought-out approach.”

Where businesses are most — and least — likely to fail in the first year

By state, the District of Columbia has the highest first-year business failure rate. Here, a significant 32.9% close within the first year. Following are Tennessee (29.3%) and Delaware (27.2%), which rank second and third, respectively.

On the other end of the list, Washington (17.5%) has the lowest first-year business failure rate. South Carolina (17.7%) and Louisiana (19.6%) follow. Across all states, 21 have first-year failure rates below the national average of 22.1%.

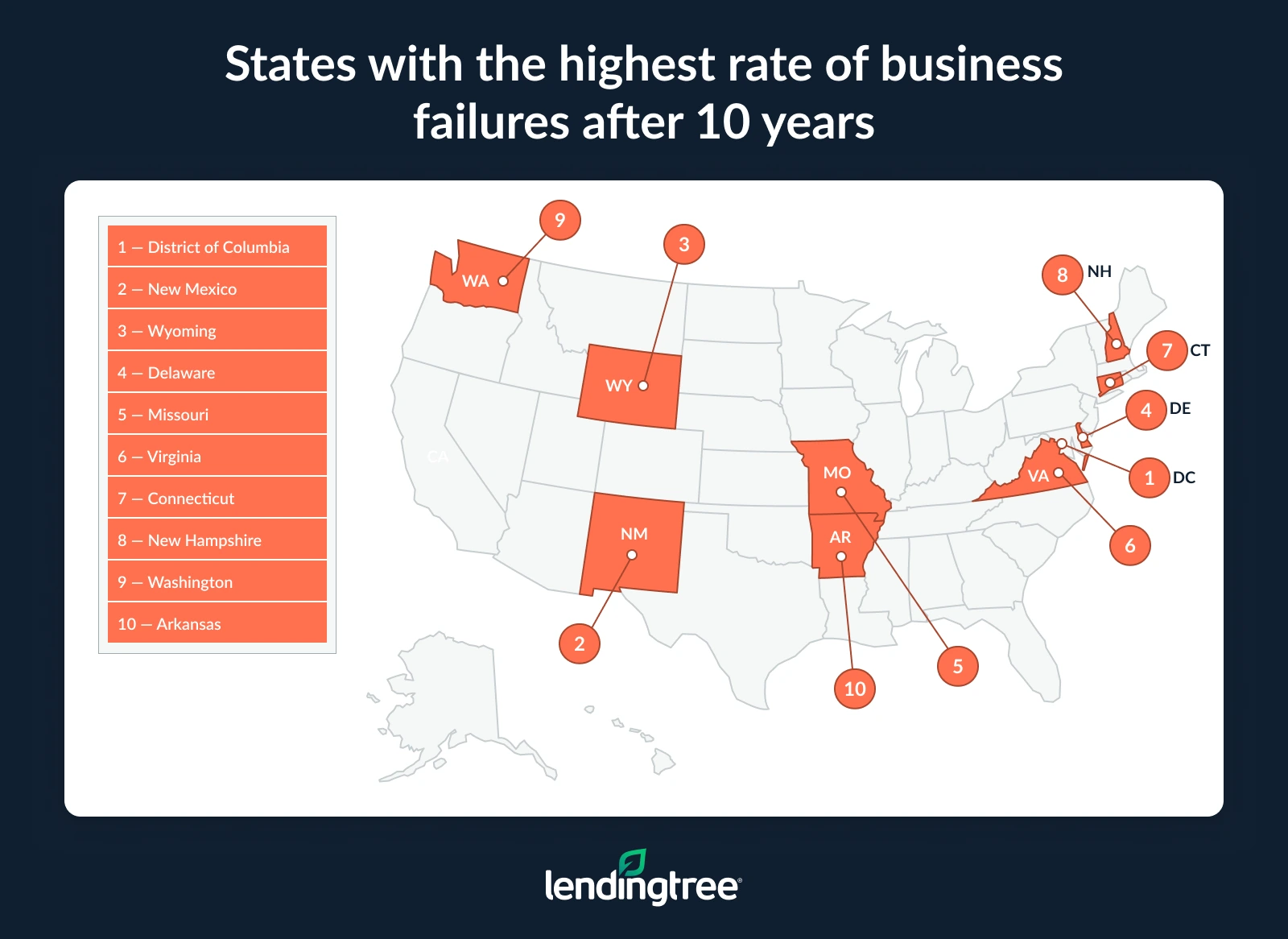

While many businesses fail in the first year after opening, it’s after the 10-year mark that surviving as a business really gets tough. In the District of Columbia (72.7%), New Mexico (72.6%), Wyoming (71.1%), Delaware (70.4%) and Missouri (70.3%), more than 7 in 10 businesses fail in that time frame.

Meanwhile, Minnesota and Hawaii (both at 58.1%) have the lowest failure rates after 10 years. Iowa rounds out the top three, with 60.1% of businesses failing over that period.

Full rankings: States with the highest rate of businesses that fail within a year of opening

| Rank | State | Failure rate within 1 year | Failure rate after 5 years | Failure rate after 10 years |

|---|---|---|---|---|

| 1 | District of Columbia | 32.9% | 57.6% | 72.7% |

| 2 | Tennessee | 29.3% | 53.6% | 67.2% |

| 3 | Delaware | 27.2% | 51.9% | 70.4% |

| 4 | Oregon | 26.7% | 54.2% | 62.9% |

| 5 | Oklahoma | 26.5% | 49.8% | 68.1% |

| 6 | Missouri | 25.9% | 57.1% | 70.3% |

| 7 | Alaska | 25.6% | 49.2% | 66.6% |

| 8 | Georgia | 24.9% | 50.1% | 67.9% |

| 8 | New Hampshire | 24.9% | 52.3% | 68.5% |

| 10 | Wyoming | 24.8% | 52.5% | 71.1% |

| 11 | Maryland | 24.5% | 49.9% | 65.4% |

| 12 | Colorado | 24.1% | 51.5% | 68.1% |

| 12 | Nevada | 24.1% | 52.4% | 67.1% |

| 12 | Vermont | 24.1% | 53.4% | 64.6% |

| 15 | Florida | 24.0% | 50.5% | 66.0% |

| 15 | Virginia | 24.0% | 51.2% | 69.6% |

| 17 | North Carolina | 23.9% | 45.8% | 62.8% |

| 18 | Utah | 23.7% | 50.3% | 64.5% |

| 18 | West Virginia | 23.7% | 46.4% | 62.0% |

| 20 | Kansas | 23.6% | 52.6% | 65.4% |

| 20 | Massachusetts | 23.6% | 47.3% | 63.8% |

| 22 | Arkansas | 23.4% | 52.0% | 68.2% |

| 22 | Idaho | 23.4% | 54.4% | 66.7% |

| 24 | Maine | 23.1% | 45.1% | 62.4% |

| 25 | New Mexico | 23.0% | 53.7% | 72.6% |

| 26 | Alabama | 22.9% | 48.6% | 63.6% |

| 26 | Hawaii | 22.9% | 49.0% | 58.1% |

| 28 | Michigan | 22.4% | 45.0% | 64.3% |

| 29 | Mississippi | 22.1% | 46.5% | 64.1% |

| 29 | Rhode Island | 22.1% | 51.9% | 66.7% |

| 31 | Connecticut | 21.8% | 48.9% | 68.8% |

| 32 | Montana | 21.7% | 47.0% | 61.5% |

| 33 | Texas | 21.6% | 47.5% | 63.4% |

| 34 | South Dakota | 21.5% | 47.3% | 61.2% |

| 35 | Kentucky | 21.3% | 45.9% | 63.6% |

| 35 | Ohio | 21.3% | 45.6% | 61.6% |

| 37 | Nebraska | 21.2% | 49.1% | 67.4% |

| 37 | Pennsylvania | 21.2% | 42.9% | 63.6% |

| 39 | Arizona | 21.0% | 47.9% | 65.7% |

| 40 | North Dakota | 20.9% | 45.6% | 67.2% |

| 41 | New Jersey | 20.7% | 49.5% | 66.0% |

| 42 | Minnesota | 20.6% | 45.1% | 58.1% |

| 43 | Indiana | 20.5% | 45.7% | 61.5% |

| 43 | Wisconsin | 20.5% | 47.6% | 62.6% |

| 45 | New York | 20.4% | 48.1% | 66.3% |

| 46 | Illinois | 20.3% | 44.4% | 61.6% |

| 47 | Iowa | 19.8% | 46.3% | 60.1% |

| 48 | California | 19.7% | 46.3% | 65.9% |

| 49 | Louisiana | 19.6% | 47.1% | 64.4% |

| 50 | South Carolina | 17.7% | 44.1% | 64.3% |

| 51 | Washington | 17.5% | 57.8% | 68.3% |

Information industry has the highest rate of early failure

Failure doesn’t affect all industries equally, either. The information industry — which involves producing and distributing information and cultural products and processing data — has the highest failure rate for new businesses. In this sector, 28.4% of businesses don’t make it past their first year.

Schulz says this is likely a result of competition. “The information industry is relatively inexpensive and easy to get into, but that means that it’s an incredibly crowded space that can be challenging to stand out in,” he says. “And even if you do stand out, it isn’t always clear or easy to figure out how to monetize that traffic and visibility you receive. That’s because many people enter this industry focusing on making the most of their creative talents and don’t think all that much about the business side of things.”

Professional, scientific and technical services — which includes legal services, accounting, engineering services and more — follows, with just over a quarter (25.5%) of businesses failing in the first year. Administrative and waste services — including executive assistants, office clerks, waste removal services and more — follows at 24.3%.

“With professional, scientific and technical services and administrative and waste services, the fixed costs may be higher than they’d be in other fields,” Schulz says. “In these fields, you might need advanced degrees or licensing before you can even get started, and then you may need expensive equipment and tools to be successful. Starting a waste services firm or a scientific facility isn’t the same as just throwing together a website to sell knick-knacks.”

At the other end, agriculture, forestry, fishing and hunting has the lowest failure rate, with just 14.3% of new businesses failing in the first year. Accommodation and food services (14.7%) and retail trade (15.6%) follow.

Industries with the highest rate of businesses that fail within a year of opening

| Rank | Industry | Failure rate within 1 year | Failure rate after 5 years | Failure rate after 10 years |

|---|---|---|---|---|

| 1 | Information | 28.4% | 54.3% | 70.0% |

| 2 | Professional, scientific and technical services | 25.5% | 49.2% | 65.7% |

| 3 | Administrative and waste services | 24.3% | 48.5% | 63.0% |

| 4 | Utilities | 23.1% | 38.4% | 52.8% |

| 5 | Transportation and warehousing | 23.0% | 47.3% | 63.9% |

| 6 | Mining, quarrying, and oil and gas extraction | 22.3% | 51.5% | 75.5% |

| 7 | Arts, entertainment and recreation | 21.6% | 42.9% | 59.2% |

| 7 | Educational services | 21.6% | 41.8% | 56.9% |

| 9 | Finance and insurance | 20.8% | 46.2% | 61.6% |

| 10 | Wholesale trade | 20.5% | 48.8% | 65.6% |

| 11 | Construction | 20.3% | 43.5% | 57.4% |

| 12 | Manufacturing | 19.9% | 41.6% | 54.7% |

| 13 | Management of companies and enterprises | 19.5% | 47.9% | 64.2% |

| 14 | Real estate and rental and leasing | 19.0% | 42.1% | 55.0% |

| 15 | Health care and social assistance | 17.9% | 47.4% | 63.6% |

| 16 | Other services (except public administration) | 17.4% | 40.0% | 57.9% |

| 17 | Retail trade | 15.6% | 40.2% | 55.8% |

| 18 | Accommodation and food services | 14.7% | 40.7% | 58.4% |

| 19 | Agriculture, forestry, fishing and hunting | 14.3% | 38.2% | 47.0% |

Surviving (and thriving) the first year: Top tips for new businesses

Starting a business isn’t an easy undertaking. Usually, it requires discipline from the start. If there were three fundamentals that every new business owner should get right from day one, Schulz believes they’d be the following:

- Make sure you know what problem you’re trying to solve for people. “It all starts there,” he says. “If you’re crystal clear on what problem you’re trying to solve for people, you have a massive leg up on many other businesses. Too many people start a business with a vague idea rather than a specific problem they’re trying to solve, and that can be a recipe for trouble.”

- Target a specific audience. “Niches bring riches, as the saying goes,” he says. “Drilling down on who you’re trying to sell to takes time and effort, but it can be so worth it because it allows you greater focus when it comes to how you spend your money.”

- Be extremely intentional about your spending. “Countless businesses have gone belly up because they burn through their funding in a flash,” he says. “Being incredibly disciplined when it comes to planning and tracking how you spend your money is a must. It all starts with knowing what your biggest priorities are, and that starts with knowing what problem you’re trying to solve and who you’re trying to help solve it.”

Methodology

LendingTree researchers analyzed the latest U.S. Bureau of Labor Statistics (BLS) Business Employment Dynamics (BED) survival data to calculate business failure rates.

For each state and industry, we analyzed establishment cohorts based on their opening year and measured survival rates “since birth.”

- One-year survival rates reflect the share of businesses opened in the year ended March 2024 that were still operating in March 2025.

- Five-year survival rates reflect the share of businesses opened in the year ended March 2020 that were still operating in March 2025.

- Ten-year survival rates reflect the share of businesses opened in the year ended March 2015 that were still operating in March 2025.

Failure rates were calculated as 100% minus the corresponding survival rate. The BED data tracks establishments (individual business locations), not firms, meaning closures reflect location-level exits and may include cases where a company continues operating other locations.

Compare business loan offers