Where Auto Loan Defaults Are Most Common — Who Defaults (and When)

Auto loan payments can feel deceptively manageable at first — until a steep bill elsewhere, an unexpected repair or an emergency expense turns it into a cost you can’t afford.

Among consumers with recently active auto loans, 1.99% have a default on record. Here’s a closer look at where auto loan defaults are most common and the typical characteristics of consumers with defaulted loans.

For this analysis, LendingTree researchers looked at about 162,000 anonymized credit reports from LendingTree users from Oct. 1 through Dec. 31, 2025. The sample includes consumers with at least one auto loan on record, including both individual and joint accounts. Researchers calculated:

- Auto loan default rate by state: The percentage of consumers with at least one defaulted auto loan, calculated among consumers with an eligible auto loan in each state.

- Distribution of defaulted consumers by credit score band: The share of consumers with defaulted auto loans across credit score ranges.

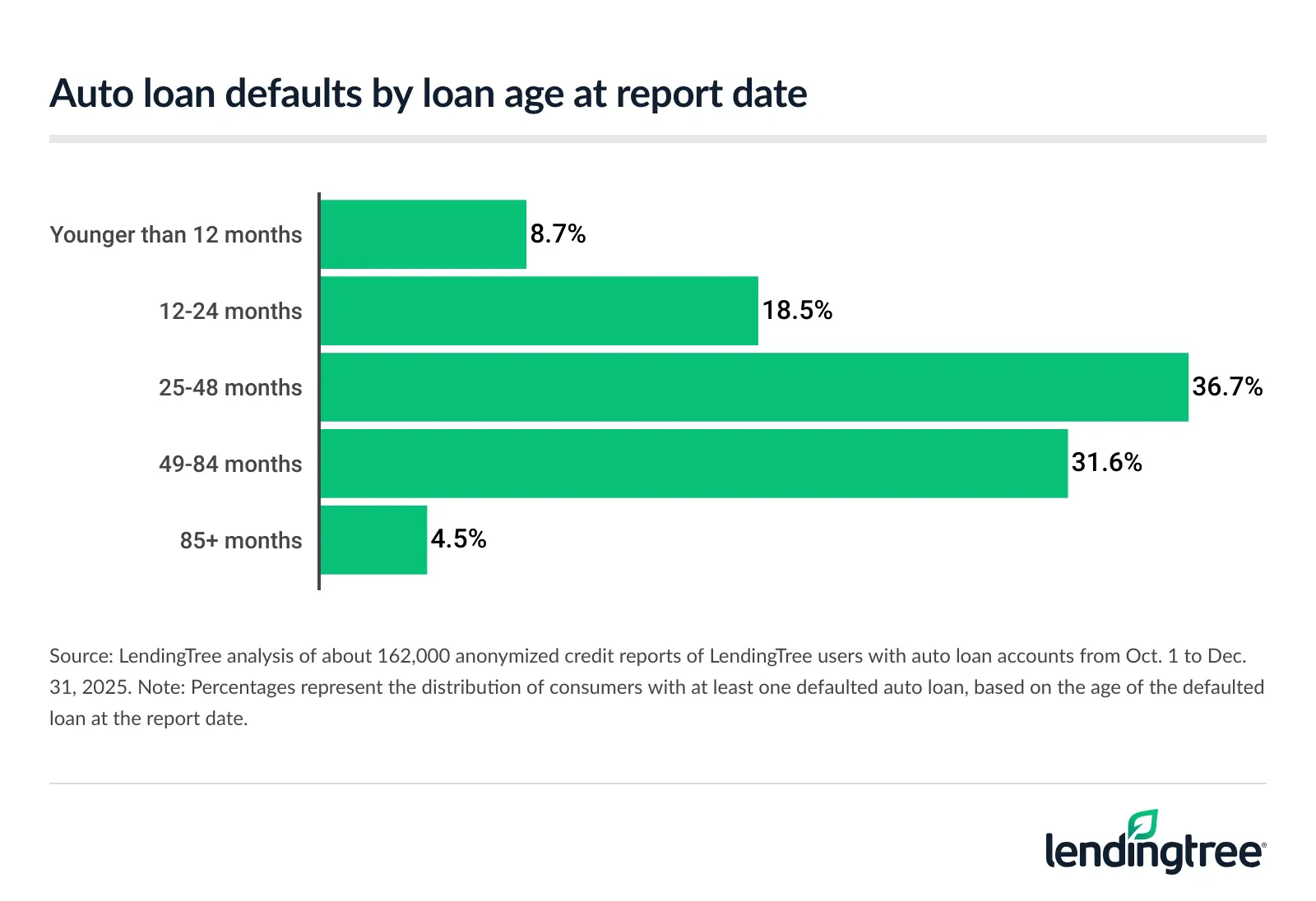

- Distribution of defaulted consumers by loan age at report date: The share of consumers with defaulted auto loans by the age of the defaulted loan, defined in months.

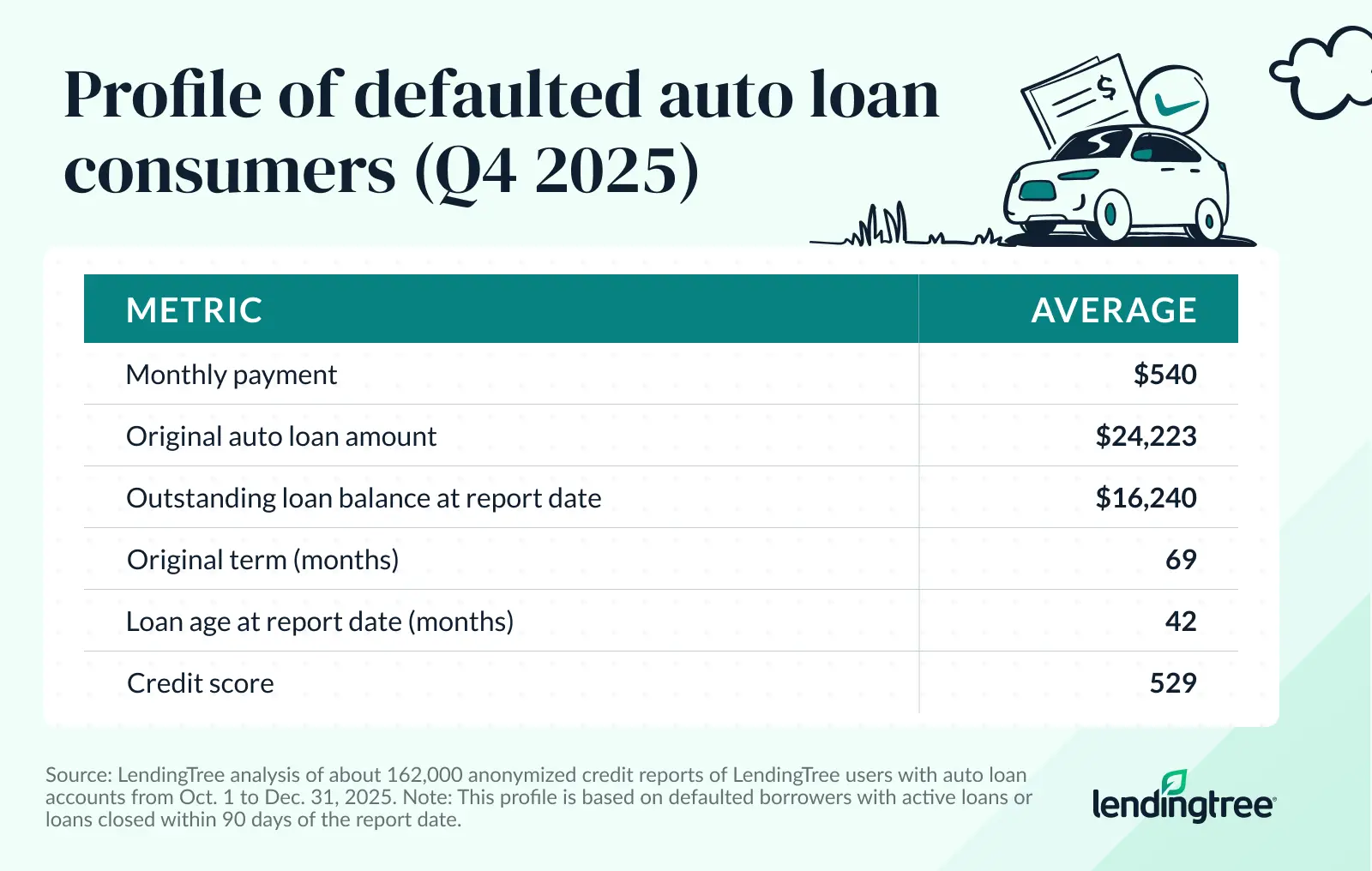

- Profile of defaulted auto loan consumers: The average characteristics of consumers with defaulted auto loans, including monthly payment, current balance, loan age at report date, original term and credit score.

A default is defined as an auto loan that’s 90 or more days past due, charged off, in collections or repossessed. Additionally, “recently active” auto loans are defined as active auto loans and auto loans closed within 90 days of the report date.

- Nationwide, 1.99% of consumers with recently active auto loans have a default on record. Consumers with defaulted auto loans as of the fourth quarter of 2025 pay an average of $540 a month, and they typically default 42 months into a 69-month loan. Long-term auto loans are common among defaulted borrowers, with 61.9% of defaulted consumers holding loans with terms of 72 months or longer.

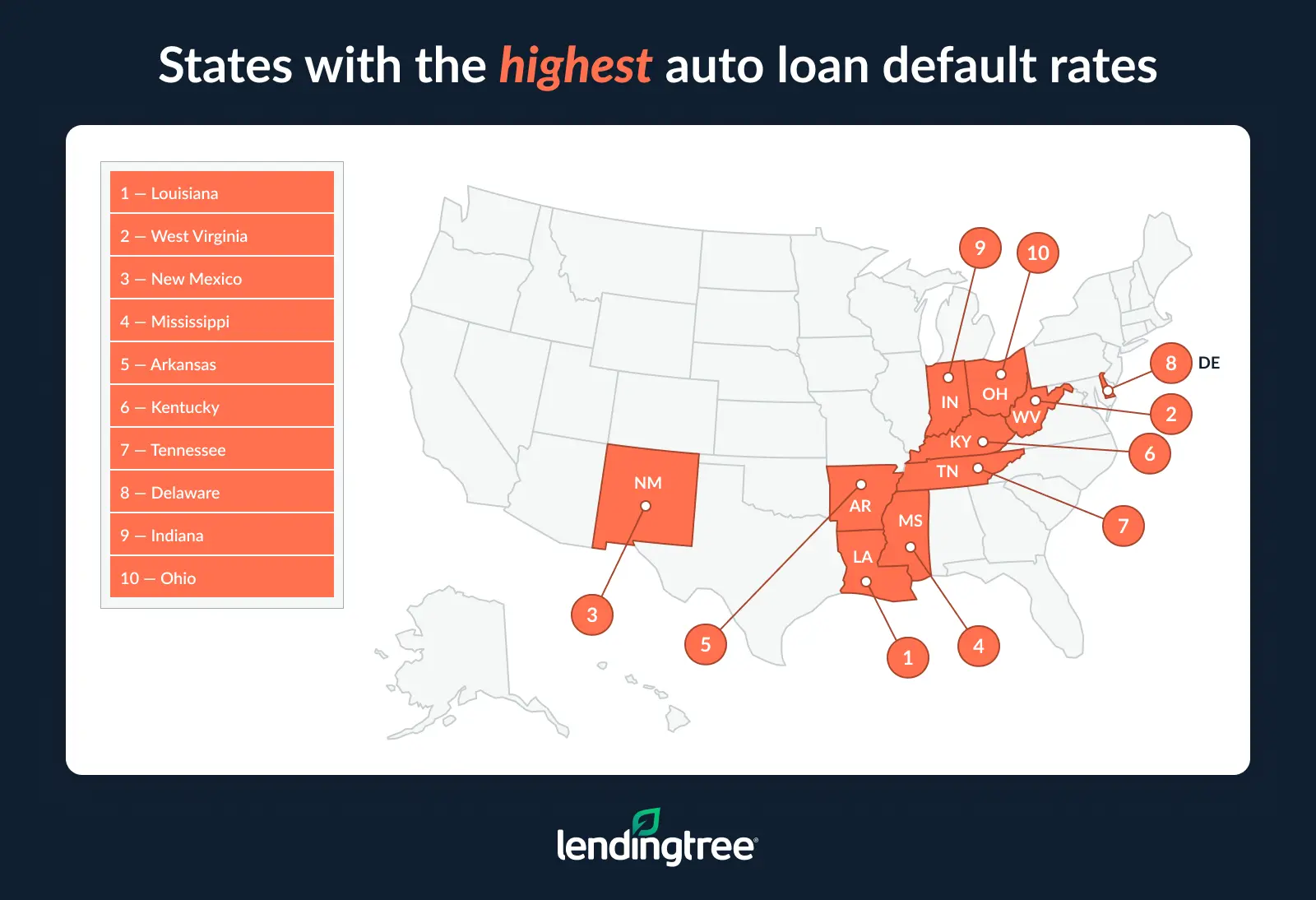

- Louisiana leads the nation with the highest auto loan default rate — 5.00%. West Virginia (4.59%) and New Mexico (4.31%) follow. In contrast, Minnesota (1.05%), Utah (1.13%) and Massachusetts (1.20%) have the lowest default rates.

- Auto loan defaults are highly concentrated among consumers with lower credit scores. 83.7% of consumers with defaulted auto loans are deep subprime borrowers with credit scores below 580. The average credit score among defaulted borrowers is 529.

- Defaults on auto loans are rare in the first year, with just 8.7% of defaulted loans under a year old. The highest default rates occur between two and four years after the loan is issued, accounting for 36.7% of defaults.

1.99% of consumers with recent auto loans have defaulted

Among consumers with auto loans active or closed within 90 days of the report period, 1.99% have a default on record.

Consumers with defaulted auto loans pay an average of $540 a month, with an original loan amount of $24,223 on average. Additionally, the average default occurs 42 months into a 69-month loan.

Long-term auto loans are common among defaulted borrowers, with 61.9% of defaulted consumers holding loans with terms of 72 months or longer.

Matt Schulz, LendingTree chief consumer finance analyst and author of “Ask Questions, Save Money, Make More: How to Take Control of Your Financial Life,” says that auto loan payments are just one of the many affordability challenges facing Americans today, but it’s a big one.

“For most Americans, $540 a month is an awful lot of money, so it shouldn’t be surprising that many are struggling mightily with that size of payment,” he says. “However, when you factor in the high prices of vehicles today and the high rates that many shoppers face, especially those with imperfect credit, many Americans have little choice but to accept that monthly payment when financing their new or used car.”

Louisiana has highest auto loan default rate

By state, Louisiana has the highest auto loan default rate at 5.00%. That’s more than twice the national rate.

West Virginia (4.59%) and New Mexico (4.31%) follow closely behind.

Schulz says those are states with both lower incomes and lower credit scores in comparison to much of the country. “That’s a troubling combination because lower credit scores typically lead to higher interest rates, which lead to bigger monthly payments and costlier loans, which in turn lead to real affordability issues for those with low incomes,” he says.

At the other end of the list, Minnesota has the lowest auto loan default rate at 1.05%. Utah (1.13%) and Massachusetts (1.20%) rank second and third, respectively.

Full rankings: Percentage of consumers with defaulted auto loans by state

| Rank | State | Default rate (%) |

|---|---|---|

| 1 | Louisiana | 5.00% |

| 2 | West Virginia | 4.59% |

| 3 | New Mexico | 4.31% |

| 4 | Mississippi | 3.97% |

| 5 | Arkansas | 3.38% |

| 6 | Kentucky | 2.98% |

| 7 | Tennessee | 2.94% |

| 8 | Delaware | 2.82% |

| 9 | Indiana | 2.76% |

| 10 | Ohio | 2.62% |

| 11 | Pennsylvania | 2.53% |

| 12 | Missouri | 2.44% |

| 13 | Michigan | 2.32% |

| 14 | Montana | 2.28% |

| 15 | Kansas | 2.21% |

| 16 | Texas | 2.10% |

| 17 | Alabama | 2.09% |

| 18 | South Carolina | 1.99% |

| 19 | Wisconsin | 1.95% |

| 20 | Wyoming | 1.94% |

| 20 | Arizona | 1.94% |

| 22 | Iowa | 1.91% |

| 23 | North Carolina | 1.88% |

| 24 | New York | 1.85% |

| 25 | North Dakota | 1.83% |

| 26 | South Dakota | 1.82% |

| 27 | Oklahoma | 1.80% |

| 28 | Illinois | 1.78% |

| 29 | New Jersey | 1.68% |

| 30 | Nevada | 1.67% |

| 31 | Rhode Island | 1.65% |

| 32 | Florida | 1.64% |

| 33 | Colorado | 1.63% |

| 34 | Maine | 1.52% |

| 35 | Idaho | 1.49% |

| 36 | Georgia | 1.48% |

| 37 | Nebraska | 1.47% |

| 38 | Hawaii | 1.43% |

| 39 | California | 1.35% |

| 40 | Vermont | 1.34% |

| 41 | Connecticut | 1.32% |

| 42 | Washington | 1.31% |

| 43 | Virginia | 1.30% |

| 44 | New Hampshire | 1.29% |

| 44 | Oregon | 1.29% |

| 46 | Maryland | 1.28% |

| 47 | Alaska | 1.21% |

| 48 | Massachusetts | 1.20% |

| 49 | Utah | 1.13% |

| 50 | Minnesota | 1.05% |

Those with lower credit scores are more likely to default

Auto loan defaults are particularly common among those with lower credit scores. In fact, 83.7% of consumers with defaulted auto loans are deep subprime borrowers with credit scores below 580. That’s followed by subprime borrowers with scores between 580 and 619.

Generally, Schulz believes auto loan defaults are concentrated among deep subprime borrowers because they’re more likely to be struggling financially. “Even a small shock can derail their ability to pay,” he says. “Add in that they’re paying higher interest rates than others with better credit, and it makes for a tenuous situation.”

Auto loan defaults by credit score band

| Credit score band | Share of defaulted consumers |

|---|---|

| Deep subprime (<580) | 83.7% |

| Subprime (580-619) | 11.1% |

| Near-prime (620-659) | 3.6% |

| Prime (660-719) | 1.4% |

| Super-prime (720+) | 0.2% |

On average, the credit score among defaulted borrowers is 529.

“There’s little in life that’s more expensive than crummy credit, and that’s certainly true with auto loans,” Schulz says. “A credit score of 529 is going to make it challenging just to get an auto loan, and the ones that’ll be available will come with sky-high rates and plenty of fees. A poor credit score can cost someone tens of thousands of dollars over their lifetime in the form of higher interest rates and fees on auto financing, a mortgage and other loans.”

Default likelihood is highest between 2 and 4 years after the loan is issued

The likelihood of defaulting on an auto loan rises with the loan’s age. While just 8.7% of defaulted loans occur under a year old, 36.7% of defaults occur between two and four years after the loan is issued, taking up the higher share of defaults.

“People are less likely to default in the first year because the loan is new, the car is still working well and the payment usually feels doable,” Schulz says. “A couple years in, the car starts needing repairs, the loan balance is still high and if money gets tight, people are more likely to give up on a payment that no longer feels worth it.”

Taking out a loan you can handle: Top expert tips

If you’re shopping for an auto loan, determining affordability entails accounting for more than just your current financial situation. We offer the following advice:

- Shop around for the best rate. “Taking the time to compare rates from multiple lenders well before you set foot in the dealership is crucial,” Schulz says. “Unless you’re getting a special 0% or deeply reduced rate, the dealership is highly unlikely to be able to give you a lower rate than what you could find from other lenders. This is important even if you have imperfect credit. Crummy credit may mean fewer and less appealing options, but they are still worth considering.”

- Build your emergency fund. “This is easier said than done,” he says. “However, having some extra cash in savings can be a game-changer during a short-term rough patch. It can mean the difference between successfully making a payment and having to default. And, yes, you should still build your savings even if you have other types of debt.”

- Treat the car like the valuable commodity it is. “Staying ahead on maintenance lowers the odds that a surprise repair forces you to choose between fixing the car and paying the loan,” he says.

Methodology

LendingTree researchers analyzed a sample of about 162,000 anonymized credit reports from LendingTree users from Oct. 1 to Dec. 31, 2025. The sample includes consumers with at least one auto loan on record, including both individual and joint accounts.

The analysis is conducted at the consumer level. A consumer is classified as having a defaulted auto loan if they have at least one auto loan that’s 90 or more days past due, charged off, in collections or repossessed. Both active auto loans and auto loans closed within 90 days of the report date are included to ensure recently defaulted accounts are captured.

Using this definition, the following metrics are calculated:

- Auto loan default rate by state (the percentage of consumers with at least one defaulted auto loan, calculated among consumers with an eligible auto loan in each state)

- Distribution of defaulted consumers by credit score band (the share of consumers with defaulted auto loans across credit score segments at the report date)

- Distribution of defaulted consumers by loan age at report date (the share of consumers with defaulted auto loans by the age of the defaulted loan, calculated as the number of months between the loan origination date and the report date)

- Profile of defaulted auto loan consumers (average characteristics of consumers with defaulted auto loans, including monthly payment, current balance, loan age at the report date, original loan term and credit score; loan characteristics are based on a representative defaulted auto loan per consumer)

Get auto loan offers from up to 5 lenders in minutes