Compare Low Boat Loan Rates in July 2026

Sail into savings with rates as low as 5%

Advertising Disclosures

Loading Disclosures…

- Average boat loan rates range from around 7.5% to just under 10%, according to LendingTree data.

- Because boat loans are larger and have longer repayment terms, rates are typically higher than those for auto loans.

- Boat loan rates can vary widely across lenders, which is why comparing offers can help you save money and find a lower rate.

What are boat loan rates right now?

The average boat loan rate is 8.40% as of the fourth quarter of 2025, based on the LendingTree quarterly boat loan rate report. The table below shows the average rates real borrowers were offered by credit score, giving you a clearer idea of what you might qualify for.

If your score is below 580, that doesn’t automatically mean that you won’t qualify for a boat loan, but approval can be more difficult and rates will be higher.

Still, lenders typically look at more than just scores, so don’t count yourself out if you have less-than-perfect credit. Instead, get prequalified or preapproved to see if now is a good time to buy or if you should wait and improve your financial situation in order to get better rates.

| Credit score | Average APR |

|---|---|

| All scores | 8.40% |

| Very good (740-799) | 8.12% |

| Good (670-739) | 8.94% |

| Fair (580-669) | 9.70% |

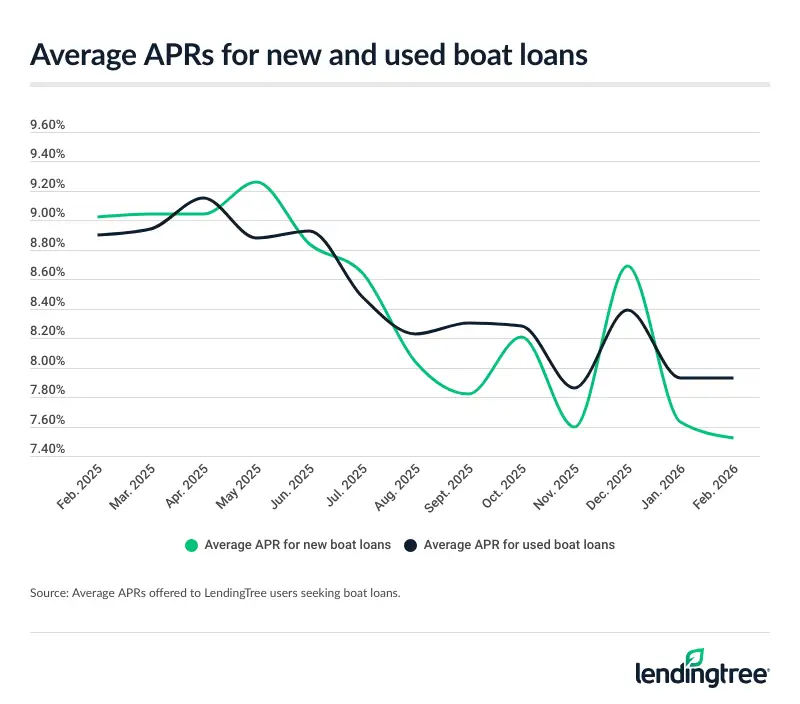

Boat loan rate trends, based on LendingTree data

Boat loan rates can fluctuate throughout the year based on market conditions, borrower profiles and boat shopping trends.

Rates increased toward the end of 2025, but have since leveled out. The winter spike was likely due to fewer boat loan shoppers rather than an actual rate trend. Smaller data sets are more easily skewed by borrowers with lower credit scores, which can make the average rate higher.

While watching loan rate trends can give you a high-level picture of the market, improving your credit score has a bigger impact on the rate you receive.

Spring and summer are the busiest times for boat loan lenders, which can lead to longer processing times. Start comparing rates early. Many boat loans take a week or more to finalize, and delays can be more common during peak boating season. Getting prequalified now can help you secure financing faster when you find the right boat later.

What does a boat actually cost?

The average amount financed to buy a boat through LendingTree in 2025 was just over $54,000, but that number is just a starting point. Boat prices vary widely based on type, size, age and features, so the boats you’re considering may be significantly more or less expensive than the average.

Just getting started? Use $54,000 as a rough benchmark to see how much your monthly boat payments could cost and decide whether boat ownership fits your lifestyle.

Already have a type of boat in mind? Check live marketplaces like Boat Trader or Boats.com for real-time pricing for similar boats in your area.

Trying to decide if a specific boat is a good deal? Get a boat history report and compare boat values on a site like J.D. Power.

How much does a boat loan cost per month?

Find out your estimated monthly boat loan payment with our boat loan calculator. Consider it a handy life vest to help you stay afloat as you plan your purchase.

| Lender | Starting APR | Term | Amount | |

|---|---|---|---|---|

|

|

5.00% | 12 to 84 months | Not specified | |

|

|

5.49% | 60 to 180 months | Up to $1,000k | |

|

|

5.99% | 60 to 252 months |

$10k – $9.9M |

|

|

|

5.99% | 60 to 240 months | Starting at $10k | |

|

|

6.49% | 72 to 240 months |

$10k – $5M |

Learn more about how we made our picks for the best boat loans.

Boat loan lenders with the lowest rates

Southeast Financial Credit Union (SFCU)

- Starting APR

- 5.00%

- Extra low rates for shorter loan terms

- No model year or boat type restrictions

- Can skip a payment if experiencing financial hardship

- Must become a credit union member (but it’s easy to join)

- Costs $60 to skip a payment (can be rolled into loan)

- Shorter loan terms compared to most boat loans

Southeast Financial Credit Union (SFCU) offers some of the lowest rates around for new and used boat loans. With rates starting at 5.00% for new boats and 5.75% for used, SFCU offers some of the lowest rates around.

SFCU’s lowest rates are reserved for 12-month loan terms and gradually increase with longer loan terms. Loan terms with SFCU are shorter than with most boat lenders, capping at 84 months. Depending on how much time you need to pay off your boat, you may need to go with a lender with longer terms.

You must have a credit score of at least 600 to qualify for a boat loan. You also need to join the credit union before you can borrow.

All SFCU members must open a savings account with a deposit of at least $5. To become a member, you must meet one of the requirements below:

- Make a $5 donation to Autism Tennessee

- Be a current employee or retiree of a Southeast Financial Select Employee Group

- Be related to a current SFCU member

- Live, work, worship or go to school in certain parts of Kentucky, Mississippi or Tennessee

Affinity Plus Federal Credit Union

- Starting APR

- 5.49%

- Can get assistance via live chat or video conference

- Financial coaches on staff to help with budgeting

- Has a Skip-a-Payment program

- Requires credit union membership (but anyone can join with a $25 donation)

- Can take a few hours to get an approval decision

- Skipping a payment costs $30

Affinity Plus Federal Credit Union offers cheap boat loans with a starting annual percentage rate (APR) of 5.49%. You have to join the credit union to borrow, but you can donate $25 to the Affinity Plus Foundation if you don’t meet traditional eligibility requirements.

Although this credit union is based in Minnesota, you can become a member and apply for a loan online. You can also meet virtually with a financial coach. Boats can be expensive and come with long-term costs. It may be a good idea to get a professional to look over your budget.

To get a boat loan with Affinity Plus Federal Credit Union, you must first become a member. You can join as long as you meet one of the following requirements:

- Work for the State of Minnesota or another partner employer

- Live, work or go to school in certain Minnesota communities

- Be related to or a roommate of a current Affinity Plus Federal Credit Union member

- Make a one-time $25 donation to the Affinity Plus Foundation

Boatloan.com

- Starting APR

- 5.99%

- Handles title and doc process (for an extra charge)

- Long repayment terms

- Finances boats up to 30 years old (some lenders only allow up to 20 years)

- No short-term loan options

- May not qualify if you have poor credit

Boatloan.com is a loan marketplace that helps potential buyers finance their boats. When you apply, an agent will work with you to find an offer. You can also pay extra and have Boatloan.com handle the title and registration process.

Boatloan.com also offers terms as long as 252 months. That’s a full year longer than most lenders. Although it typically costs more total interest, a longer term can bring down your monthly payment, making your boat easier to afford.

To get a boat loan through Boatloan.com, you and your boat must meet the requirements below:

- Minimum credit score: 620+

- Age of boat: 30 years old or newer

- Residency: Can’t live in Alaska, Hawaii or Oregon

My Financing USA

- Starting APR

- 5.99%

- Can get preapproved

- Customer service is available via live chat and text message

- Could result in multiple hard credit pulls

- Same-day funding possible, but may need to wait up to 48 hours

My Financing USA is a loan marketplace that connects potential buyers with boat financing partners. It offers two types of boat loans: one for good credit and one for bad credit. This writeup focuses on good credit boat loans, which start at 5.99% APR.

A great thing about shopping with a loan marketplace is that you can compare offers from multiple lenders at once. This can help you find the lowest rate without having to contact lenders individually.

However, using My Financing USA to shop for a boat loan could result in multiple hard credit pulls, depending on the number of lenders it matches you with. But as long as you get your rate shopping done within the rate shopping window (14 days for VantageScore and 45 days for FICO Score), only one pull will count against you.

To qualify for a good credit boat loan from My Financing USA, you must meet the following criteria:

- Minimum credit score: 670+

- Other credit considerations: No bankruptcies or collections

- Residency: Not available in Alaska or Hawaii

- Boat restrictions: No salvage, rebuilt or branded titles

Good Sam

- Starting APR

- 6.49%

- Free membership comes with a trip planning tool and discounts

- Private-party boat loans available

- Finances powerboats and houseboats

- Approval can take up to two days and getting money can take up to 12 business days

- Some loans may have a prepayment penalty

- Charges a loan processing fee

Loan marketplace Good Sam helps connect borrowers with lenders that offer boat loans, RV loans and unsecured personal loans. Its partners offer boat loans starting at 6.49% APR.

When you get a loan through Good Sam, you can also sign up for Good Sam membership. The Basic plan is free and gives you access to a rewards program and exclusive discounts. There are other paid tiers available that come with more robust perks.

However, how long it takes to get your loan — and whether it comes with prepayment penalties — depends on the lender Good Sam connects you with. Good Sam also charges a loan processing fee prior to closing.

To qualify for a boat loan from Good Sam, you’ll need to meet the following requirements:

- Minimum credit score: 600+

- Residency: Must live in one of the 50 U.S. states (excluding Washington, D.C.); U.S. citizenship not required for some loans

- Age of boat: Must be 25 years old or newer

- Administrative: Must provide copies of your driver’s license, purchase agreement, current title and registration, proof of down payment and proof of insurance

What affects boat loan rates the most?

Boat loan rates tend to run a few percentage points higher than auto loan rates. Compared to car loans, boat loans are bigger and have longer terms. This makes boat loans riskier for lenders, so they charge higher interest rates to compensate.

Lenders rarely disclose exactly how they calculate boat loan rates, and each lender has a different formula. This means the same borrower could get drastically different offers from lender to lender. Generally, though, the following metrics greatly impact the boat loan rates you’ll see.

- Credit score: Higher credit scores usually equal lower boat loan rates. Good credit is a signal to lenders that you are more likely to keep up on payments.

- Credit history: Lenders favor borrowers with a proven record of on-time payments on a variety of loans.

- Loan amount: Larger loans are usually more expensive because the lender has more to lose if the borrower defaults.

- Boat term: A boat term measures how long you have to pay off your loan. Shorter terms typically carry lower rates than longer terms.

- Debt-to-income ratio: DTI, or debt-to-income ratio, measures how much debt you have compared to your income. Lenders usually consider a DTI of 35% as “good,” but the lower the better, generally.

- Loan-to-value ratio: LTV, or loan-to-value ratio, measures the loan amount against the boat’s value. Higher LTVs indicate higher lender risk and, as a result, higher boat loan rates.

- New versus used: Used boats are riskier for lenders (they’re more prone to mechanical issues, for instance), so rates are typically higher for used boats than they are for new.

- Cosigner status: Adding a cosigner or co-borrower with excellent credit can help you qualify for a loan and/or lower rates.

When you’re looking for the best boat loan rates, it’s smart to shop with both lenders and your dealer. Dealer financing can unlock manufacturer rebates and sometimes even 0% APR offers.

But dealers can also mark up your rate, so you could end up paying more than necessary. Comparing lender offers helps you spot markups and understand what rates you actually qualify for.

Compare boat loan rates and save with LendingTree

You’d shop around for flights. Why not your loan? LendingTree makes it easy. Instead of applying to just one lender and hoping for a good rate, see multiple boat lenders compete for your business — so you can choose the best offer.

Tell us what you need

Take two minutes to tell us who you are and how much money you need for your vessel — we’ll take care of the rest. It’s free, simple and secure.

Shop your offers

We’ll send you offers from up to five trusted lenders. Compare your offers side by side to see which one will save you the most money.

Get your money

It’s smooth sailing once you finalize your loan with your lender — you could see money in your account in as soon as 24 hours.

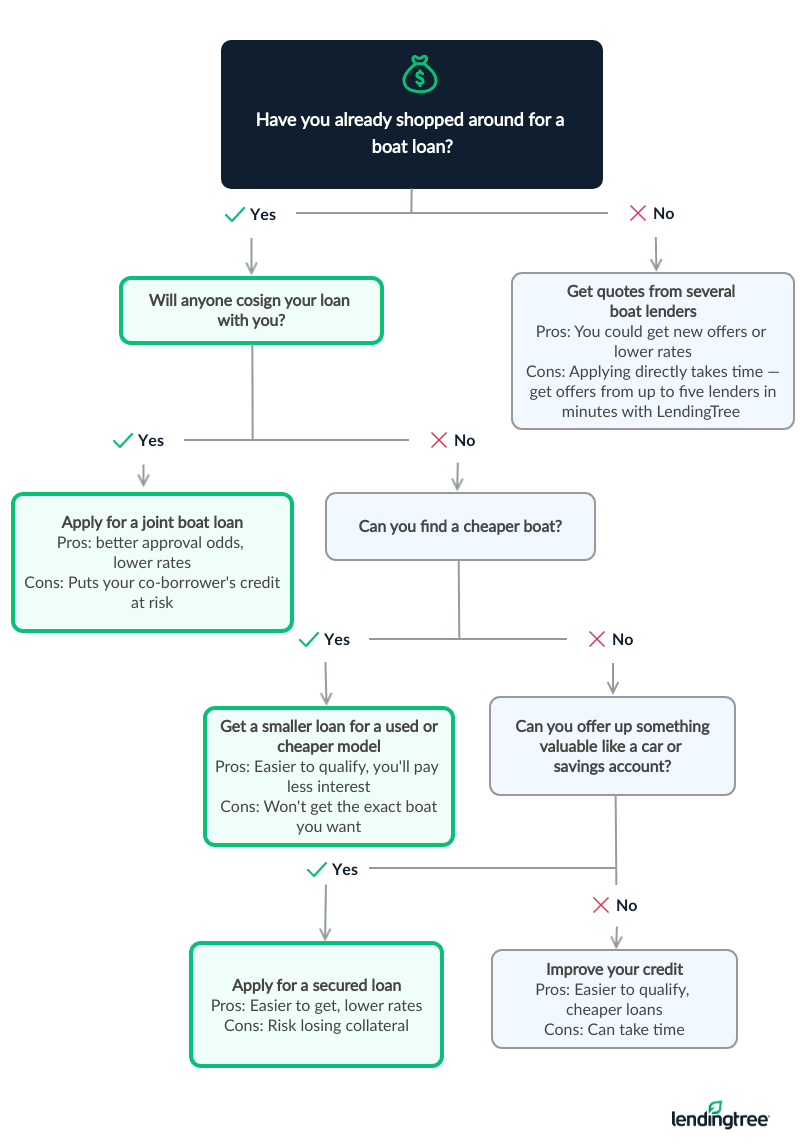

How to improve your chances of getting approved or a lower rate

It’s possible to get a bad credit boat loan, but qualifying isn’t always easy. Plus, the rate may not be worth it if you have poor credit but are eligible to borrow. Use the strategies below to find a boat loan that you can afford.

Your monthly boat loan payment is only one cost of boat ownership. Titling, registration, boating classes, equipment, insurance, trailers and slip fees all add up. You may even want to consider an umbrella policy to protect your assets in case someone sues you in a boat-related accident. Before buying a boat, make sure you can afford not just the loan but everything else that comes along with it.

Making sense of boat loan offers, rates and terms

So, you have a handful of boat loan offers. Now it’s time to choose. But how? It depends on your situation — just like every borrower is different, so is every loan shopping experience.

To help you make your pick, we’ve listed some common roadblocks borrowers face when comparing boat loan offers.

- What to know: Even if rates look the same, longer loan terms will cost you more interest

- What to do: Compare your offers using LendingTree’s boat loan calculator

- Pro tip: Choose the offer with the lowest total interest that has monthly payments you can afford

- What to know: Lenders usually offer lower rates on shorter repayment terms

- What to do: Choose the shortest loan term with monthly payments you can afford

- Pro tip: Don’t forget to add the costs of owning a boat to your monthly budget

- What to know: Bad credit boat loans can come with double-digit APRs

- What to do: Boost your odds by using a loan marketplace to shop with multiple lenders at once

- Pro tip: Boats are a luxury item, not a necessity — if rates are high, consider paying cash for a cheaper boat

- What to know: Boats require a lot of upkeep, so if you can’t afford a down payment, ownership costs may strain your budget down the line

- What to do: Consider renting or using a personal loan to finance your boat (personal loans don’t require down payments)

- Pro tip: Some boat loan lenders may waive your down payment, but skipping one can increase your risk of going upside down, or owing more than your boat is worth

Expert insights on boat loans in 2026

A short repayment term can save you money on interest, but tends to come with higher monthly payments. The savings won’t be worth it if you fall behind.

“If you’re worried about monthly payments, consider a longer loan term, and throw extra money toward your balance when possible to pay it off faster. Just make sure your loan doesn’t come with prepayment penalties for paying off your boat early.

Other ways to pay for your boat

If you need money for a boat but don’t qualify for an affordable boat loan or don’t want to put your boat up as collateral, you still have options.

Personal loans

Best for: Borrowers with good or excellent credit

Getting a personal loan is straightforward, perhaps more so than a traditional boat loan. A personal loan doesn’t use your boat as collateral so it often requires less paperwork. But personal loans tend to come with higher rates, so you’ll likely spend more money on interest.

Home equity loans

Best for: Homeowners

You pay for your boat by tapping into your home equity with a home equity loan or line of credit. Financing using equity in your home comes with perks like low interest rates, but your home will be on the line if you miss payments.

Renting or leasing

Best for: Part-time boaters

You can save some serious cash by renting or leasing a boat, but it comes at a price: your captain’s hat. If you’re ready to trade in your dreams of boat ownership, you’ll save on the total cost of owning a boat with a lease or short-term rental.

Should you actually own a boat?

If you find yourself repeatedly recalculating boat payments just to make the numbers fit your budget, pause. This could be a sign that the boat you want will stretch your current budget beyond your comfort zone. Consider cheaper vessels or look into leasing and renting.

Here are other common situations for boat buyers, along with our expert takes on when to consider leasing, buying and renting:

| Situation | LendingTree expert take |

|---|---|

| You’re always on the water (or planning to be) | Consider boat ownership or leasing. Look into boat loans if you can comfortably afford ownership costs and are confident you’ll use the boat regularly. Consider leasing if you’re a new boater and aren’t sure exactly how much you’ll use your boat. |

| You’ve only rented before, but want to spend more time boating | Leasing could be a good fit if you’re not sure how long you’ll use the boat or can’t afford ownership costs. A boat loan may be best if you’re planning to spend years out on the water and can afford boat ownership with room to spare in your budget. |

| You love boating, but only go a few times each season | Renting or fractional boat ownership can keep you from spending money on a boat you’re not actively using. |

| You’re new to boating | Try renting to start — you’ll avoid locking yourself into an expensive contract with a boat you may not use as much as you’d anticipated. |

| You’re an experienced boater but aren’t sure if you can afford ownership | Only move forward with a boat loan if you’re confident you can make your payments and afford associated costs like storage, maintenance and fuel. Consider renting and leasing in the short term while you boost your income or reduce other debts. |

Why do millions of Americans trust LendingTree?

25+ years in business. 110+ million Americans served. $260+ billion in funded loans.

Security

Instead of sharing information with multiple lenders, fill out one simple, secure form in five minutes or less.

Savings

We’ll match you with up to five lenders from our network of 300+ lenders who will call to compete for your business.

Support

We provide ongoing support with free credit monitoring, budgeting insights and personalized recommendations to help you save.

How we chose the boat loans with the lowest rates

We reviewed over a dozen boat loan lenders and marketplaces and selected those advertising starting APRs below 8% at the time of writing.

According to our systematic rating and review process, the best boat loans come from Southeast Financial Credit Union, Affinity Plus Federal Credit Union, Good Sam, Boatloan.com and My Financing USA.

We also prioritized the following factors:

Accessibility: We look for lenders with fewer barriers to approval and award points for lower credit requirements, nationwide access, fast funding and simple applications.

Rates and terms: We prioritize lenders that offer low starting rates, minimal fees, flexible terms and APR discount opportunities.

Repayment experience: We choose lenders with strong reputations, convenient self-service tools, responsive support and borrower-friendly perks.

LendingTree partners with dozens of lenders, but partners and nonpartners receive equal treatment in our scoring and review process. Read more about our editorial guidelines.

Why trust LendingTree’s methodology?

Our writers and editors dig through the facts, contact lenders directly and even go through the application process ourselves if it helps better explain what you can expect. As a Certified Financial Education Instructor℠, I’m committed to breaking down complex financial details so people can make confident, informed decisions with their money.

Jessica’s experience in editing and financial education helps shape LendingTree articles that are clear, accurate and truly useful to readers. Her certification means our recommendations are built on a foundation of consumer-first financial knowledge — not just numbers.

Frequently asked questions

According to LendingTree’s research, the boat loan companies offering some of the lowest starting APRs right now include:

- Southeast Financial Credit Union: 5.00%

- Affinity Plus Federal Credit Union: 5.49%

- Good Sam: 6.49%

- Boatloan.com: 5.99%

- My Financing USA: 5.99%

Only the most qualified borrowers qualify for a lender’s lowest advertised rates. Unless you have stellar credit and a high income (among other factors), expect your rate to vary. Boat loan rates are specific to your financial profile, the term you choose and the boat you’re financing.

You usually need at least fair credit (a FICO Score of 580 to 669) to get a boat loan with affordable rates. For instance, Southeast Financial Credit Union works with less-than-perfect credit and accepts credit scores as low as 600. Keep in mind that while you may qualify for a boat loan with bad credit, your interest rates may be high.

Some lenders offer same-day preapproval, while others take a couple of days to decide if you qualify for a boat loan. Check the lender’s FAQs or disclosures to learn more about its approval and funding timeline.

Approval may take longer depending on your credit profile, the boat you’re buying and how many applications the lender has to process. In general, approval can take longer if you have bad credit, if you’re applying during peak boating season and/or if the lender requires a boat inspection (which may be the case if you’re buying a used boat).

You risk losing your boat if you don’t make your loan payments. Defaulting will also damage your credit and could prevent you from getting an affordable loan, credit card or even mortgage in the future.