Nearly Half of Credit Cardholders Still Prefer Debit Over Credit

Nearly half of all credit cardholders said their debit card is their primary payment method, according to a new report from LendingTree.

LendingTree surveyed more than 1,000 U.S. credit cardholders about their preferences, behaviors and beliefs around credit cards. What we found was that when people had both credit cards and debit cards in their wallet, the one they were most likely to reach for when paying for something was their debit card.

The survey found that those preferring debit over credit commonly reserved their credit card for specific purchases — such as big-ticket items or emergencies — and wanted to avoid the temptation to overspend.

However, as life returns to a post-pandemic normal and banks ramp up rewards offers and other perks to attract new customers, the truth is that those opting to use debit over credit might end up leaving money on the table.

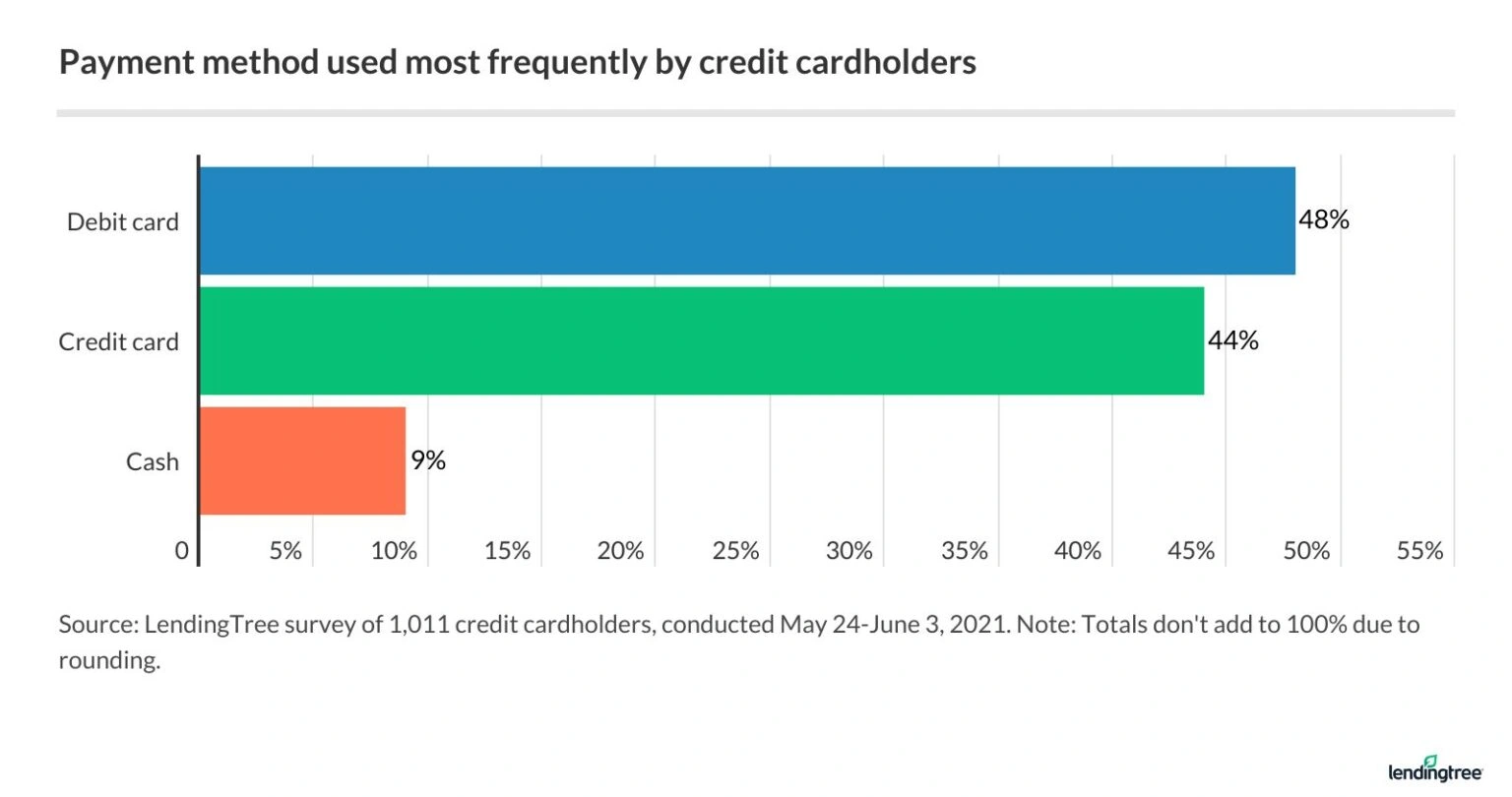

- Debit cards are credit cardholders’ preferred primary payment method. 48% of credit card-carrying consumers use their debit card more often than any other payment method.

- Cardholders admit to occasionally shunning their credit card statement due to anxiety. 43% say they sometimes avoid looking at their credit card bill because it’s stressful. That sentiment is especially true for Gen Zers (64%) and millennials (60%).

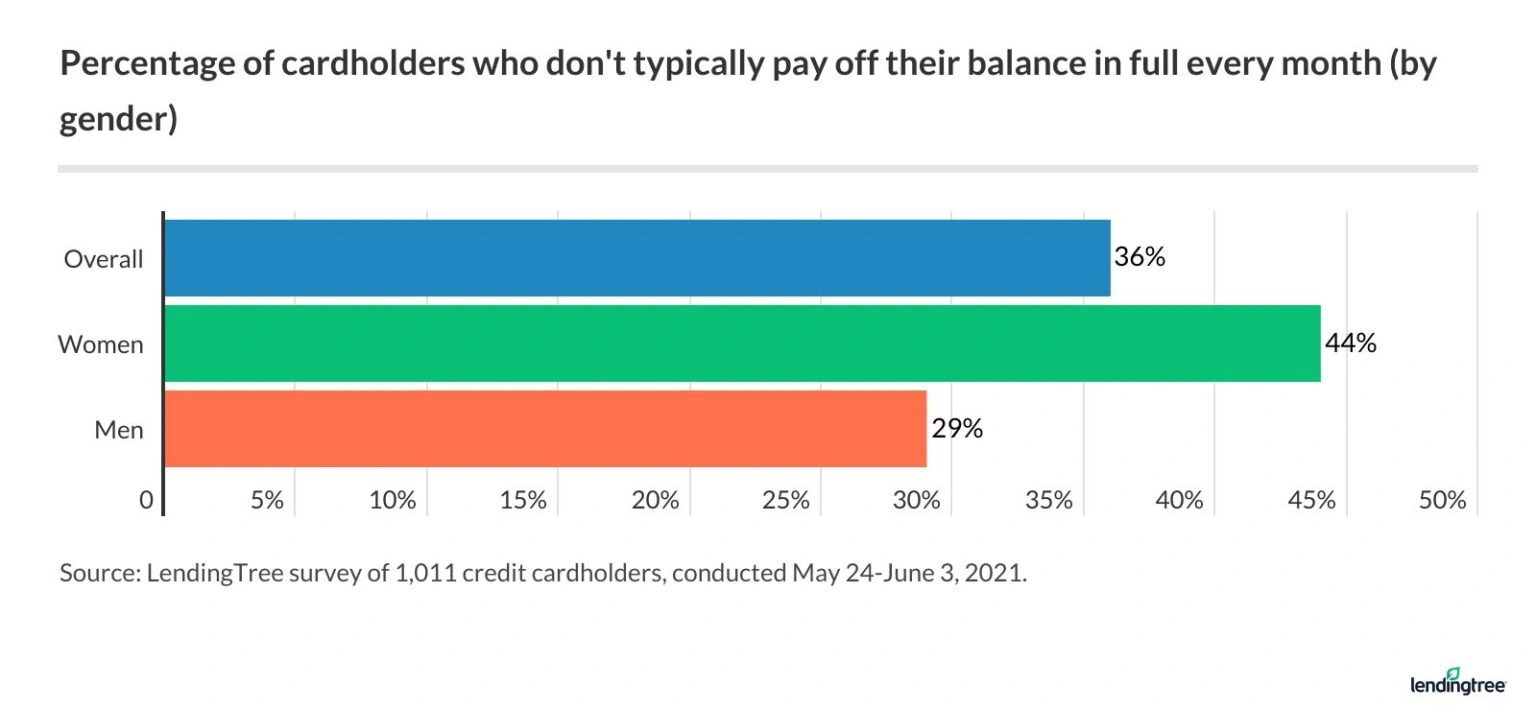

- Women are 41% more likely than men to carry a credit card balance, putting them at risk for costly interest charges. 44% of women typically don’t pay off their card in full each month, compared to 29% of men.

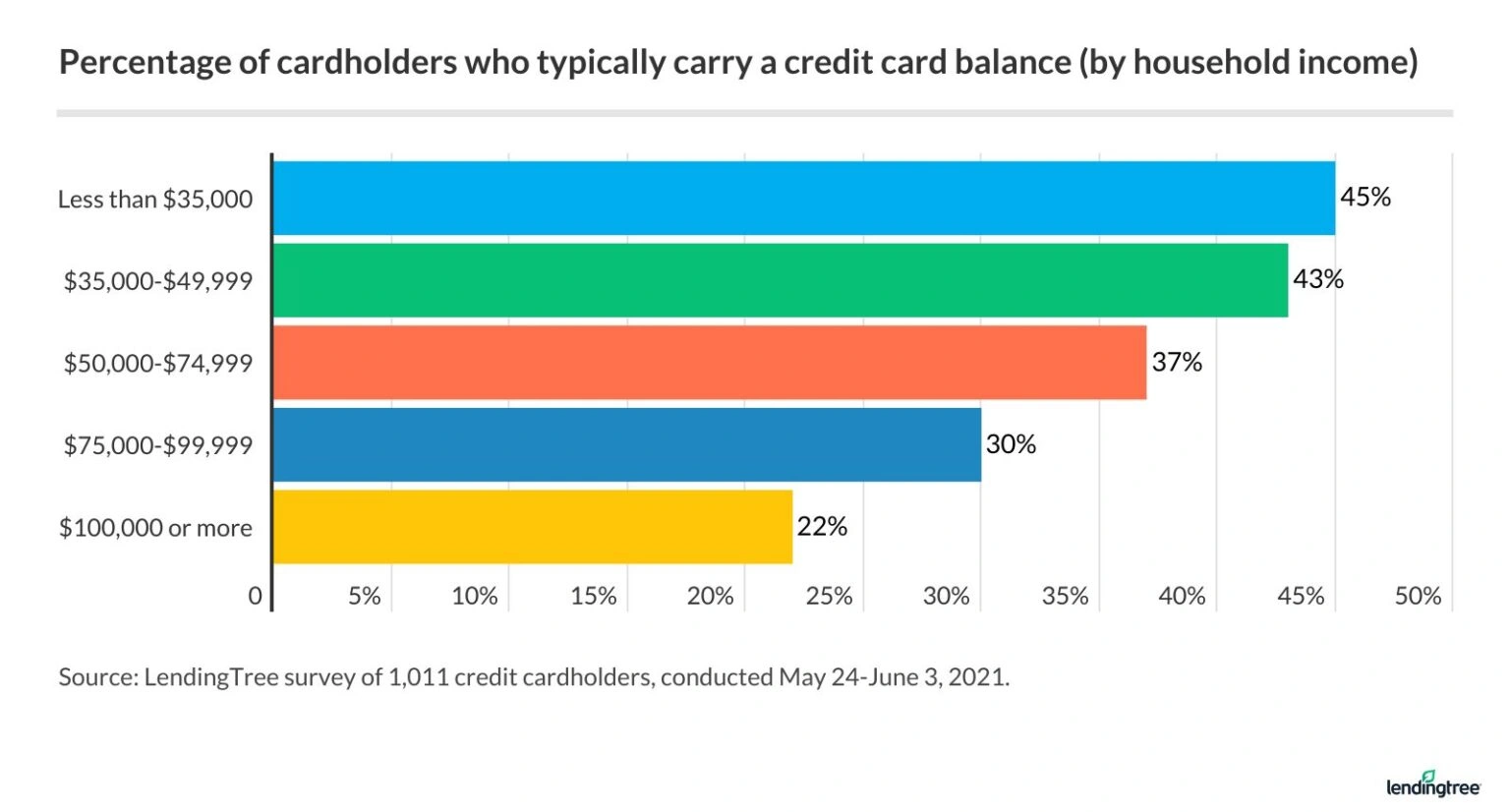

- Nearly half of low-income cardholders carry a balance each month — but a surprising number of six-figure earners do, too. Of those making less than $35,000 per year, 45% usually aren’t able to pay their credit card bill in full. As for those earning more than $100,000, 22% still carry a credit card balance.

- When it comes to opening a new credit card, some suffer from buyer’s remorse. 1 in 4 cardholders regret getting at least one of their cards, primarily because of high interest rates or hits to their credit score.

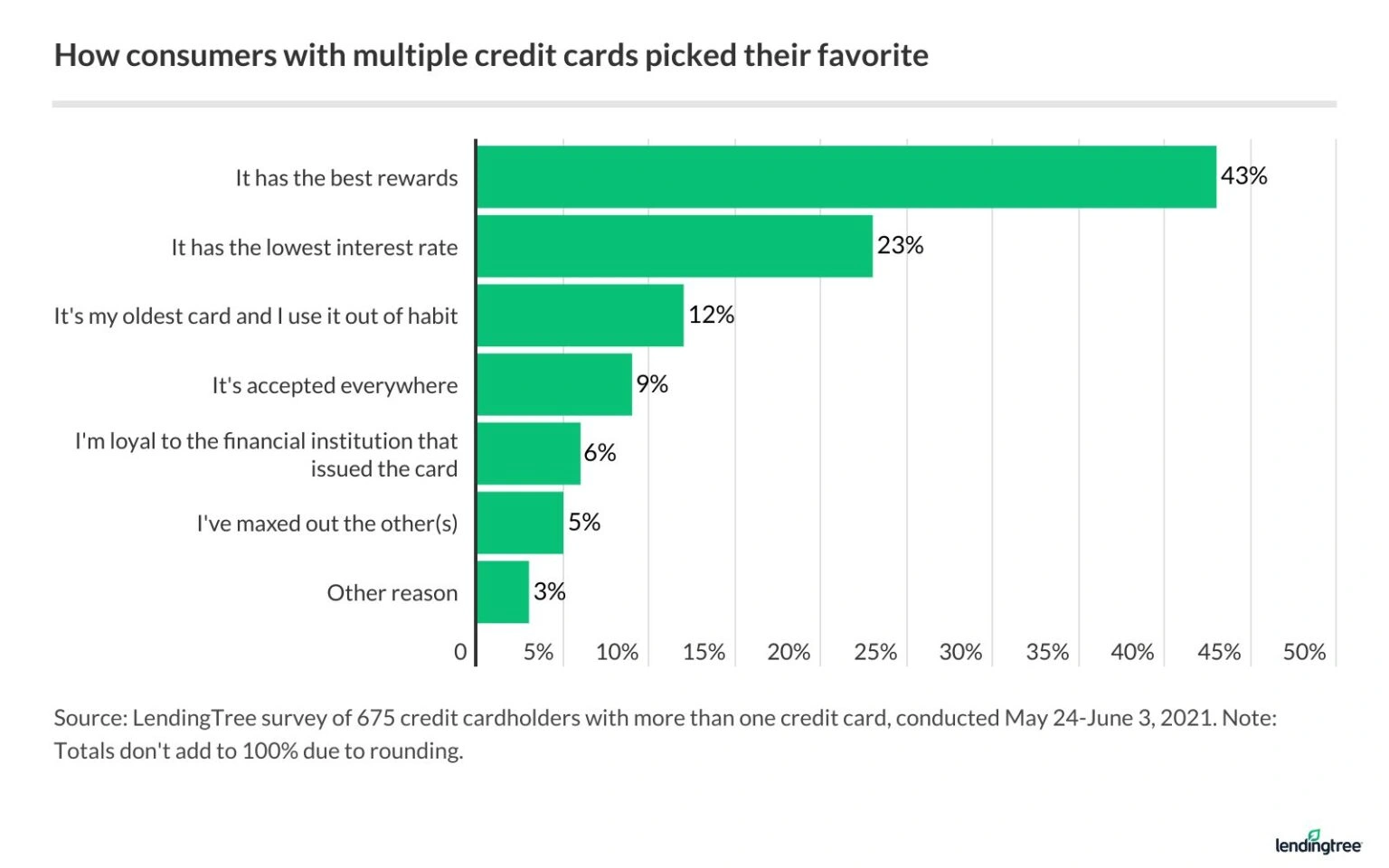

- Rewards, not interest rates, play the biggest role in how consumers pick their favorite card. Among cardholders with multiple credit cards, 43% say their preferred card has the best rewards, while only 23% say it has the lowest interest rate.

Credit cardholders still prefer debit

Millions of Americans have both a credit card and a debit card in their wallet or purse, and chances are that we’ve all been asked at some checkout counter whether we wanted to use debit or credit to pay for a purchase.

Our survey showed that for those who have the option of using both, debit is most often the preferred choice, though not by a huge margin.

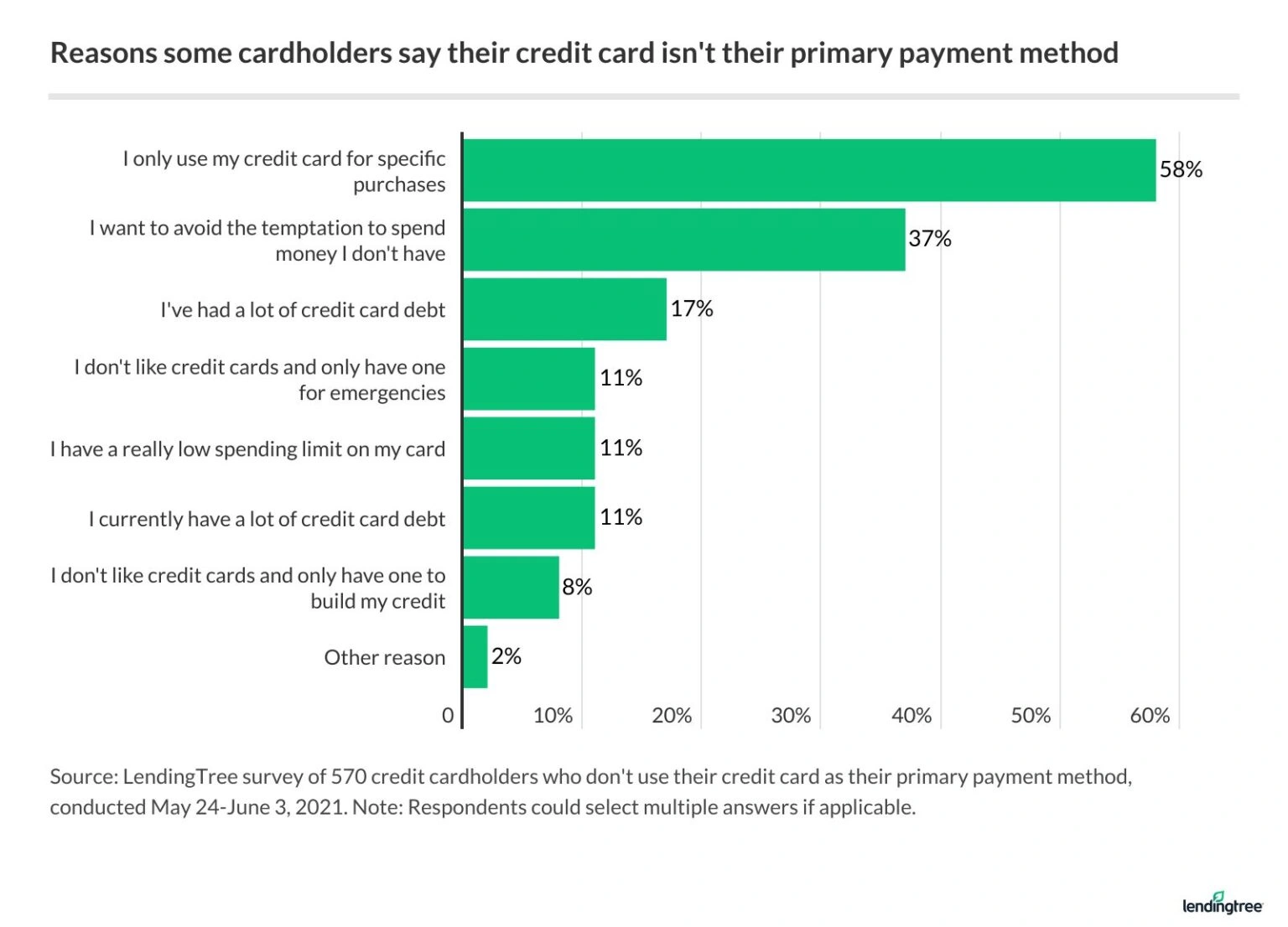

However, preferring debit doesn’t necessarily mean shunning credit altogether. When asked why credit cards aren’t their primary payment method, the most common answer by far was that they only used credit cards for specific purchases.

We didn’t ask what those specific purchases might include, but they likely include big-ticket items like computers, kitchen appliances and furniture that folks may not be able to pay for with cash. Nearly 6 in 10 (58%) of those asked said that, while another 11% said they only used credit in case of emergency and 8% said they use it to build credit.

The second most common reason for preferring debit was to avoid the temptation that comes with a credit card. Nearly 4 in 10 (37%) of those asked said that, while another 17% said they’ve had a lot of credit card debt and 11% said they have a lot of credit card debt now, spurring them to prefer other payment methods.

It’s all about the balances

Job No. 1 for anyone with a credit card is to pay your balance off as soon as possible. Ideally, you should pay in full every single month so you never have to worry about accruing interest and getting trapped in the cycle of debt that so many face. Unfortunately, however, that’s just not realistic for many Americans, and it causes a great deal of stress and anxiety for many cardholders.

That stress can be so acute that some cardholders will sometimes avoid looking at their credit card statement because of the anxiety it brings. In fact, 43% of cardholders said this — and that number is far higher for Gen Zers (64%) and millennials (60%). Perhaps paradoxically, these generations were also most likely to say that they checked their transactions and balances online on a weekly basis.

However, there’s no question that the stress caused by these regular checks is real and can be powerful.

Young cardholders aren’t the only ones carrying balances, though. For example, women are much more likely than men to say they carry a balance.

Those with lower incomes are most likely to say they carry a balance, too, though more than 1 in 5 (22%) of those with incomes of more than $100,000 a year carry a balance as well.

Picking a favorite card

For those who have more than one credit card, the most common reason a specific card was their favorite was that it came with the best rewards. That shouldn’t be surprising, given Americans’ seemingly undying passion for credit card rewards. However, the gap between the top two reasons might’ve been a bit bigger than expected.

Respondents were nearly twice as likely to say a card was their favorite because of rewards (43%) than because it had the lowest interest rate (23%). Those have long been the biggest factors driving credit card sign-ups, but it is clear that rewards, at least today, is the far bigger driver for most.

Still, Americans don’t always make the right choice when choosing a credit card. One in four cardholders said they have regretted getting at least one of their credit cards in the past. The biggest reason for regret was the card’s high interest rate, but respondents also cited damage to their credit score and extra debt brought on by that new available credit as key reasons.

The bottom line

In the wake of the economic chaos of the past year, it is completely understandable that many Americans would be leery of credit cards. The last thing many people want is the lure of available credit possibly leading them into debt in uncertain economic times.

However, the truth is that those leaning on debit cards over credit cards do so at a cost.

- Security: If a thief gets hold of your credit card and uses it, chances are all you’ll have to do is call your issuer, report the transaction and ask them to waive it. With debit cards, however, fraudsters can access real money from a real account, causing you real headaches. Yes, you’ll likely get that money back fairly quickly, but if bills come due before the money gets replaced, it can make things pretty dicey.

- Rewards: Some debit cards offer rewards, but they’re rarely as lucrative as what you can get with credit cards. That’s especially true when it comes to travel-focused cards. Plus, the credit card business is entering what is likely to be one of its most competitive times in its history, as Americans’ lives and spending habits return to normal as the pandemic’s economic impact wanes. Those who eschew credit cards will miss out on potentially unprecedented sign-up bonuses and other rewards offers.

- Credit building: A credit card is one of the best and easiest ways to get started with credit and to rebuild credit after you make mistakes, while debit card spending, generally speaking, won’t help at all. You can start with a secured credit card — where you deposit a small amount of money with an issuer to start a credit line — or a student credit card or a retail credit card if other types of cards aren’t available. You could also ask a relative to make you an authorized user on their credit card account, which jumpstarts your credit by transferring the history of that card account to your credit report. However you do it, a credit card can be a great credit building tool, and that’s important because there is little in life that is more expensive than crummy credit.

All that said, the right card for you is a personal choice. If you simply aren’t comfortable with all the trappings of credit card ownership, don’t get one. It’s OK. The stress and anxiety you feel can outweigh all the potential good — and credit card mistakes can have long-term financial consequences.

However, if you do feel like you’re ready to handle a credit card — financially and otherwise — it can be a great tool. The right card, used wisely, can make your life better.

Methodology

LendingTree commissioned Qualtrics to field an online survey of 1,011 U.S. credit cardholders, conducted May 24 to June 3, 2021. The survey was administered using a non-probability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2021:

- Generation Z: 18 to 24

- Millennial: 25 to 40

- Generation X: 41 to 55

- Baby boomer: 56 to 75

While the survey also included consumers from the silent generation (defined as those 76 and older), the sample size was too small to include findings related to that group in the generational breakdowns.

Recommended Articles

Best $100,000 Personal Loans of August 2026

Back-to-School Shopping Defies Inflation: Families Spend Nearly the Same as Before the Pandemic

Delaware, D.C. and Texas Have the Highest Business Bankruptcy Filing Rates in the US

Best Health Insurance Companies in Georgia in 2026

Homebuyer Down Payments by Generation in the 50 Largest US Metros

Best Merchant Cash Advances in August 2026

How To Refinance a Car Loan With Bad Credit

Best Bad Credit Auto Refinance Companies in August 2026

Home Insurance Takes Up Nearly a Fifth of Monthly Housing Costs in Some States

America’s Tourism-Dependent Metros Aren’t Always the Obvious Ones