More Tax Filers Relying on Refunds, With Most Spending the Money Within a Month

For the third straight year, a growing percentage of Americans who plan to file a federal tax return say they’re relying on a refund.

Our survey of over 1,500 tax filers found that nearly half (46%) are relying on getting a refund, up four points from 2025, six points from 2024 and 10 points from 2023.

2026 filers say they plan to use their refund to pay for everyday expenses, such as groceries or rent, as well as to pay off debt or build savings. That means most refunds are being put to good use rather than being spent frivolously, which is encouraging. More concerning, however, is that two-thirds of filers say their tax refund is very or somewhat important to their financial situation.

Here’s what else we found.

- More tax filers are becoming reliant on tax refunds. Nearly half (46%) of this year’s filers say they’re relying on getting a tax refund. That’s up from 42% in 2025, 40% in 2024 and 36% in 2023. Filers with young children, millennials and Gen Zers are most likely to say they’re reliant on their refunds. Meanwhile, an additional 45% aren’t relying on getting one but say it would be a pleasant surprise if they did.

- A majority of tax filers (68%) say their refund is very or somewhat important to their financial situation. While 75% of filers with an income below $30,000 a year report that their tax refund is very or somewhat important, 70% of filers earning $100,000 or more say the same. Most filers (54%) say that if they do get a refund, they expect to use it within a month.

- Refunds cover essentials, not luxuries. Nearly 9 in 10 tax filers expect to get a refund, though the majority of filers (59%) expect less than $2,000 back. About a third (34%) of filers plan to use it for everyday expenses like groceries, rent or bills, another 34% plan to use it to pay off debt and 32% plan to put it into savings or an emergency fund.

- Refund or not, tax season is still stressful for filers. Half of filers say tax season is very or somewhat stressful. That figure is even higher for groups that are more reliant on their refund, including Gen Zers (63%) and filers with young kids (62%).

More tax filers are becoming reliant on tax refunds

Almost half (46%) of Americans who plan to file a federal tax return in 2026 say they’re relying on getting a refund. That’s up four points from 2025, six points from 2024 and 10 points from 2023. (It’s still well below the pandemic-era peak of 55% seen in 2021, however.) Meanwhile, another 45% aren’t relying on a refund but say it would be a pleasant surprise if they ended up getting one.

Percentage of federal income tax filers this year who say they’re relying on getting a tax refund (by demographic)

- Overall: 46%

- Men: 48%

- Women: 44%

- Gen Zers: 53%

- Millennials: 58%

- Gen Xers: 45%

- Baby boomers: 28%

- Parents with kids younger than 18: 63%

- Parents with kids 18 or older: 32%

- Adults without children: 40%

- Adults who earned less than $30,000: 52%

- Adults who earned $30,000 to $49,999: 41%

- Adults who earned $50,000 to $99,999: 44%

- Adults who earned $100,000 or more: 50%

More than 6 in 10 (63%) filers who are parents of young kids say they’re reliant on their tax refund. Men are slightly more likely than women to say the same — 48% versus 44%. Millennials ages 30 to 45 are the age group most likely to say so (58%), while baby boomers ages 62 to 80 are the least likely (28%).

Those earning less than $30,000 a year (52%) are the most likely to rely on tax refunds, but the second-most likely income bracket is those earning $100,000 or more. Half of that group says so.

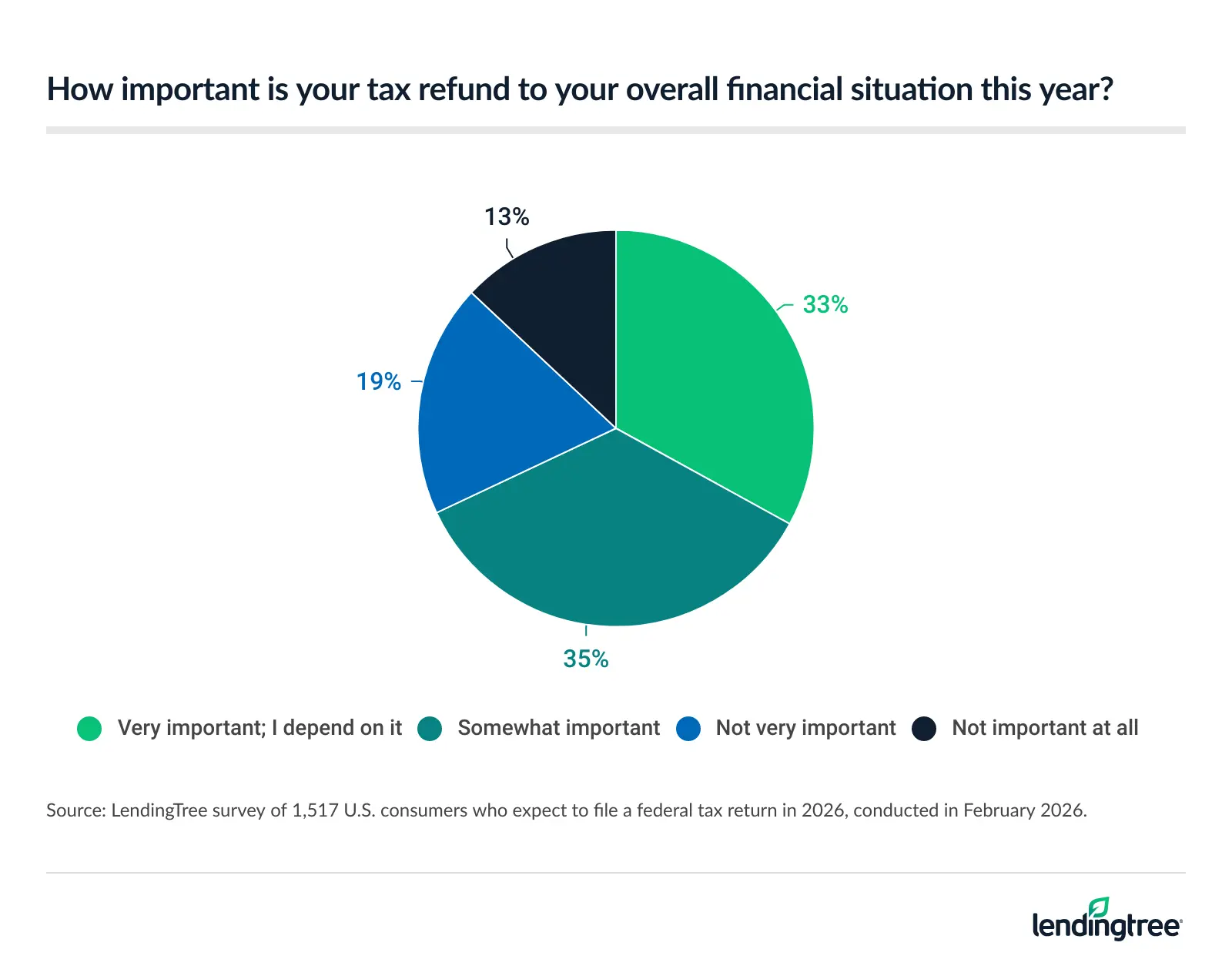

Most filers say their tax refund is very or somewhat important

Even if filers aren’t completely reliant on getting a tax refund, most think that it’s important to get one.

About 2 in 3 filers (68%) say that a tax refund is important to their overall financial situation in 2026, including 33% who say it’s very important.

Three-fourths of filers with an income below $30,000 a year report that their tax refund is very or somewhat important to their financial situation, but a similar 70% of filers earning $100,000 or more say the same. The younger you are, the more likely you are to say that a refund is important to your financial situation, with 83% of Gen Zers ages 18 to 29 saying so, versus just 40% of boomers.

Driving home the importance of the refund, 54% of filers say they’d need to use the refund within a month of receiving it. Just 21% say they could go three months or longer without touching it, while another 12% say they aren’t sure how long they could wait to use it.

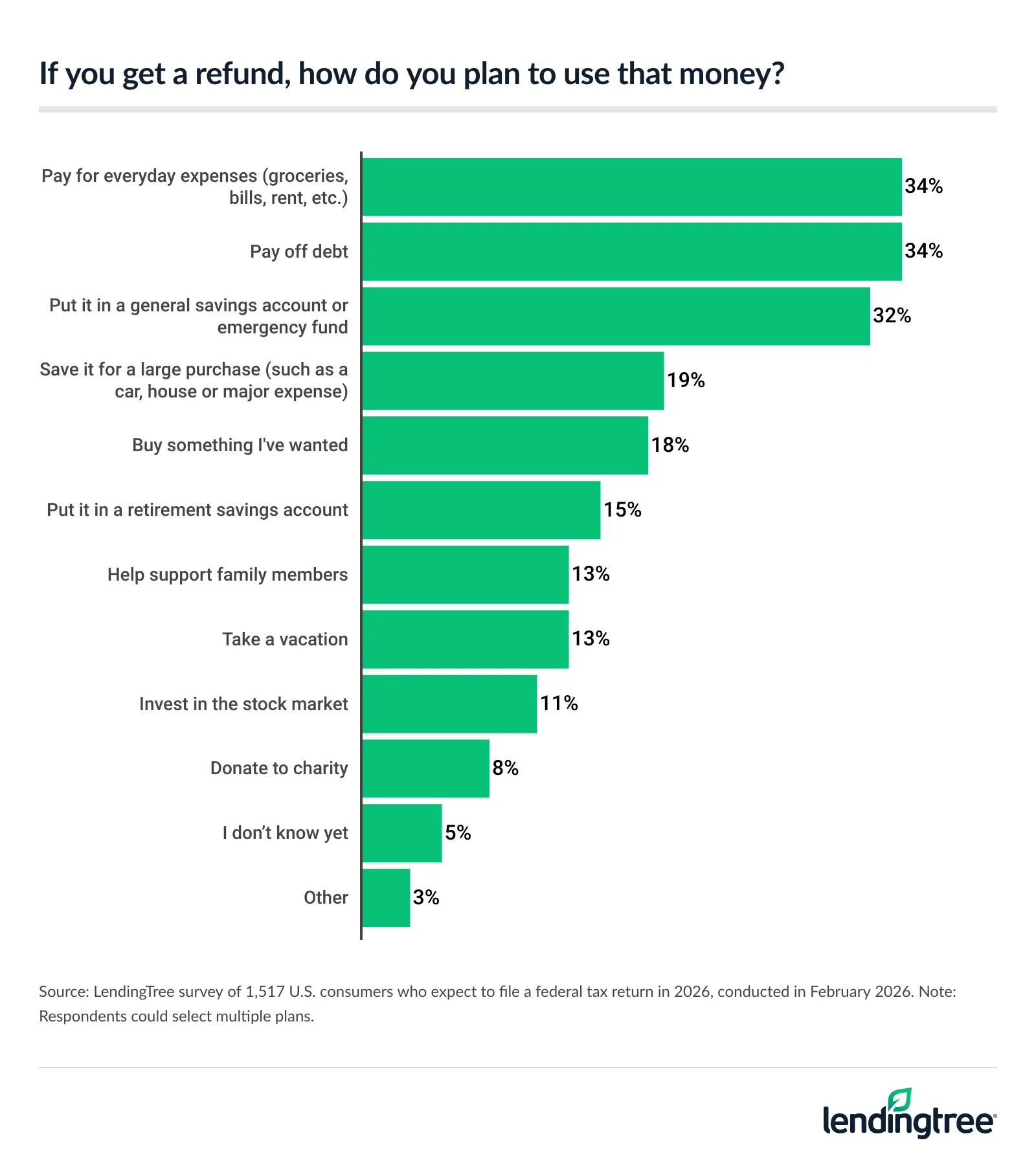

Refunds cover essentials, not luxuries

Our survey found that nearly 9 in 10 filers (89%) expect to get at least some refund. However, that seems unrealistic, given that 63% of filers in 2025 got refunds, according to IRS data. That means that many families expecting a windfall from Uncle Sam may end up disappointed.

Most filers (59%) expect to get less than $2,000 in their refund, including 26% who expect to get less than $500. Meanwhile, 12% expect to get refunds of $4,000 or more.

When we asked how they’d spend the money if they did get a refund, three answers were more popular than the rest: 34% said they’d spend it on everyday expenses, such as groceries, rent or bills, 34% said they’d pay off debt and 32% said they’d put it into savings or an emergency fund.

Filers earning less than $30,000 a year (43%), millennials (42%) and parents of young kids (41%) are among the most likely to say their refund would go to paying everyday expenses.

About 1 in 5 Gen Z and millennial filers (21% and 20%, respectively) say at least part of their refund would go toward helping support family members. That’s well above the 13% of all filers who say the same.

Meanwhile, just 8% of filers say at least part of their refund would go to charity. The younger you are, the more likely you are to say that you’d use your refund this way (12% of Gen Z filers say so, versus just 4% of boomers).

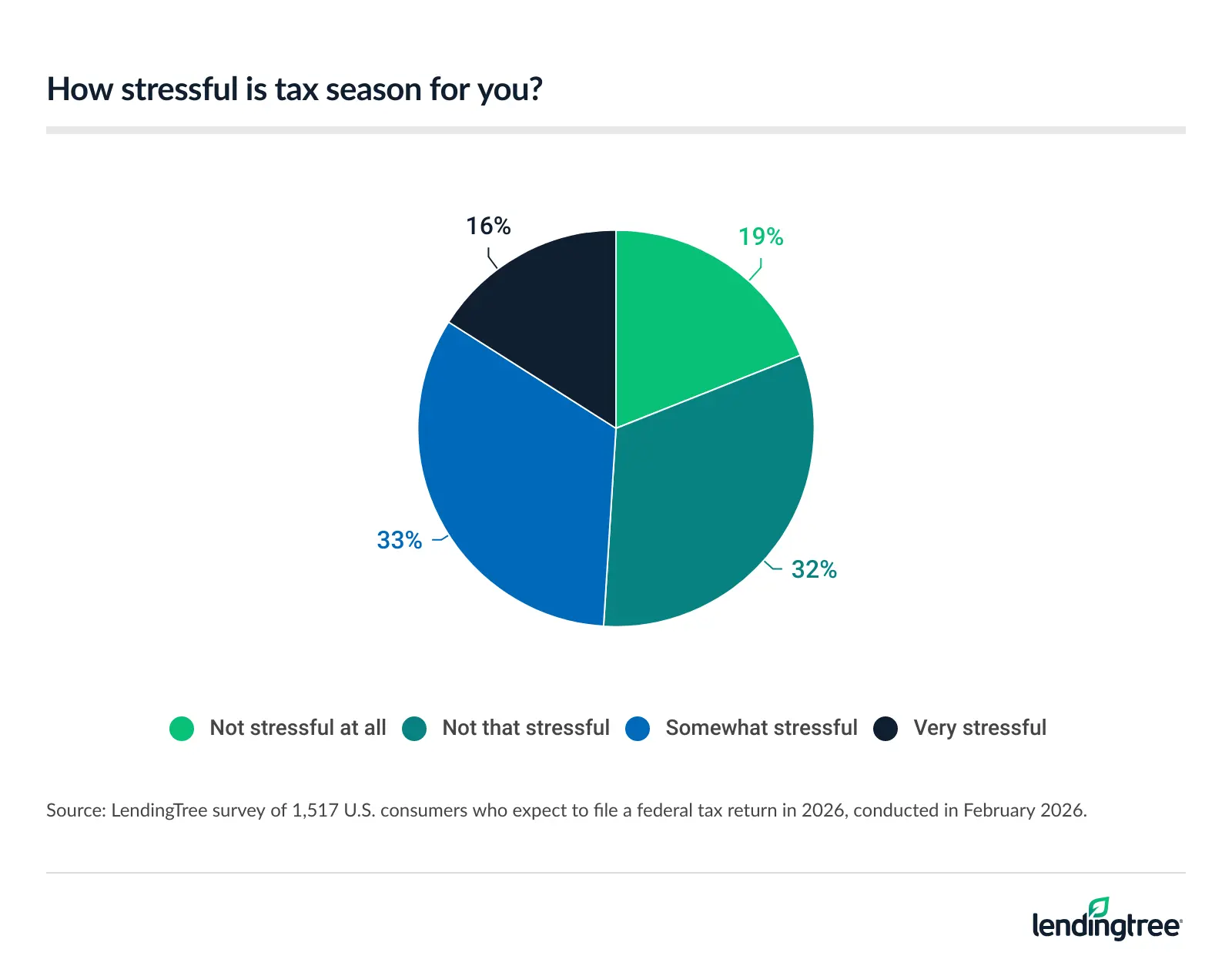

Refund or not, tax season is still stressful for filers

Half (50%) of those who plan to file a federal tax return in 2026 say tax season is very or somewhat stressful.

A deeper dive into the data shows that groups that are more reliant on their refund are among the most likely to feel the stress of the season. Nearly two-thirds (63%) of Gen Z filers say tax season is at least somewhat stressful, while 62% of filers with children under 18 say the same. Also, the highest earners are among the most likely to be stressed out, with 60% of those earning $100,000 or more saying they feel that way.

Consider reducing your refund next year — no, really

As much as we might wish it were different, windfalls just don’t come our way very often. When they do, it feels incredible, and their impact on our finances can be monumental.

However, not all windfalls are created equal. When it comes to tax refunds, you might be better off not getting one at all.

Don’t want a tax refund? Have you lost your mind?

Nope.

Here’s why: That money that you’re being refunded has been yours all along. It’s money that you’ve overpaid the government to withhold, and that they’ve held onto in the interim. In other words, you’ve basically given Uncle Sam a short-term, interest-free loan rather than keeping the money for yourself and investing it, saving it or putting it toward your own financial goals.

The good news is that you can often fix that. For many, all that is needed is to adjust the withholdings on your W-4 form to make sure that less money is taken out of every paycheck for taxes. Your company’s HR department should be able to help you with that. The IRS tax withholding estimator could be useful as well. For others with more complicated finances, it might make sense to contact a tax professional for guidance.

Once you’ve adjusted your withholdings, take advantage of that extra cash. Two great options:

have it automatically deposited into a high-yield savings account to build your emergency savings or use it to pay off your high-interest debt. Either way, you’re putting your money to work for you rather than having it collect interest for the government — and I’m pretty sure that you need it more than they do.

Methodology

LendingTree commissioned QuestionPro to conduct an online survey of 2,000 U.S. consumers ages 18 to 80 on Feb. 4-10, 2026. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. Researchers reviewed all responses for quality control.

We defined generations as the following ages in 2026:

- Generation Z: 18 to 29

- Millennials: 30 to 45

- Generation X: 46 to 61

- Baby boomers: 62 to 80

Get debt consolidation loan offers from up to 5 lenders in minutes