Many Say It Would Take a Housing Market Crash — or a 50-Year Mortgage — to Buy

The possibility of homeownership has gotten so far out of reach for many Americans that they’re even rooting for the housing market to crash so they can afford to buy.

That’s perhaps the biggest — and bleakest — takeaway from a LendingTree survey of 2,000 Americans on the nation’s housing market.

Here’s what else we found.

In our survey, we described a housing crash as one “characterized by sharp declines in real estate values, significantly reduced buyer demand and rapidly rising rates of foreclosures and mortgage delinquencies.”

While a crash could be seen as good for first-time homebuyers because it means lower home prices, those slashed home values also mean dramatically reduced equity for current homeowners and a much more challenging environment in which to sell a home. Many homeowners may even find themselves underwater, meaning they owe more on the house than it’s worth. That’s a precarious situation, especially if the crash is part of an overall economic downturn marked by rising unemployment.

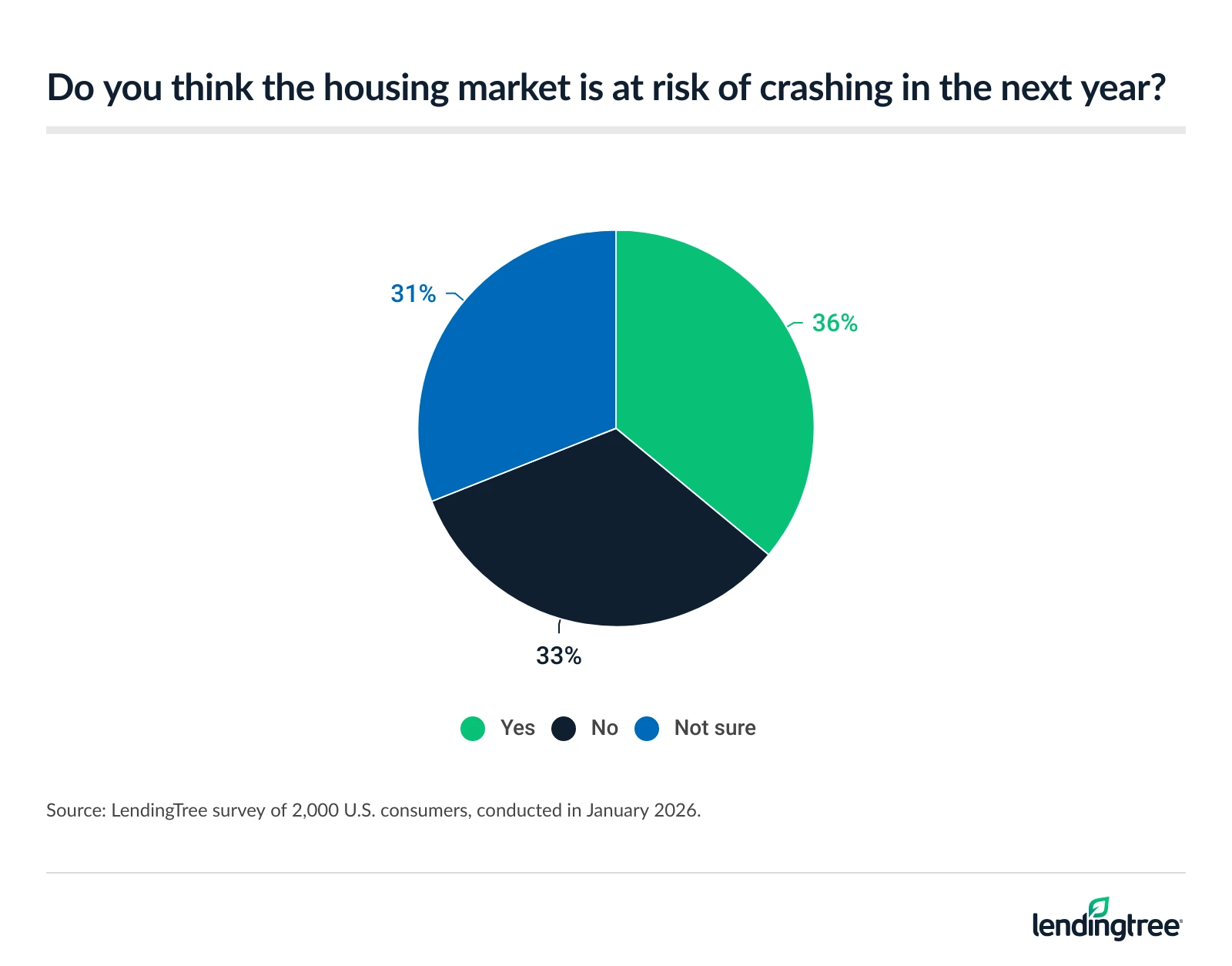

- Nearly a third of Americans are rooting for a housing market crash. 36% of Americans believe the housing market is at risk of crashing in the next year, and 31% say they’re rooting for a crash — including 59% of Gen Zers. Consumers hoping for a crash say they want a downturn to lead to more stability in the future and to lower property taxes on their homes. In fact, 27% of nonhomeowners believe a housing market crash is the only way they could afford to buy a home.

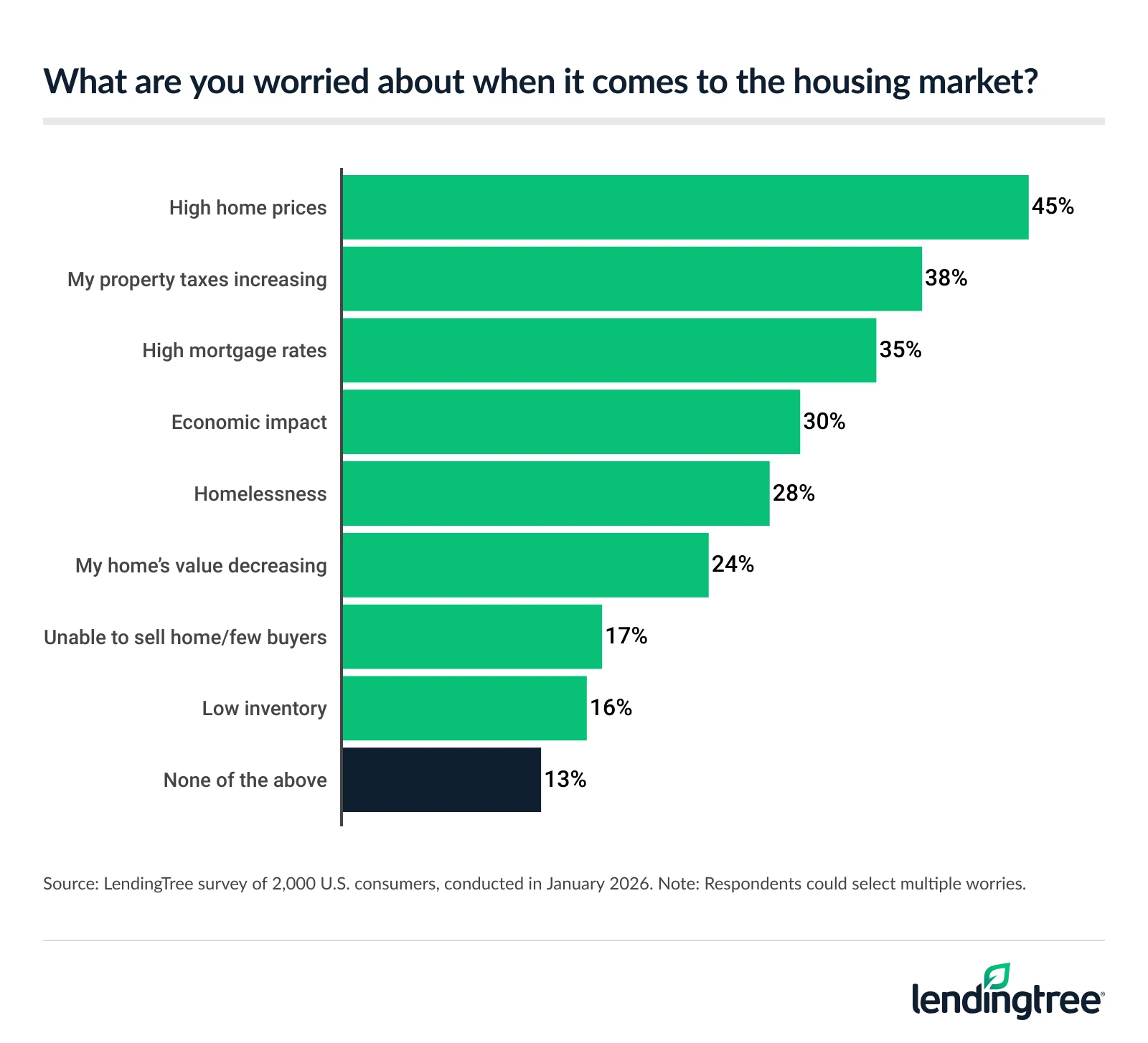

- Americans’ housing market anxieties stretch far and wide. High home prices (45%) and high mortgage rates (35%) are among Americans’ most common worries about the housing market. Other housing market worries include increasing property taxes (38%) and the broader economic impact (30%).

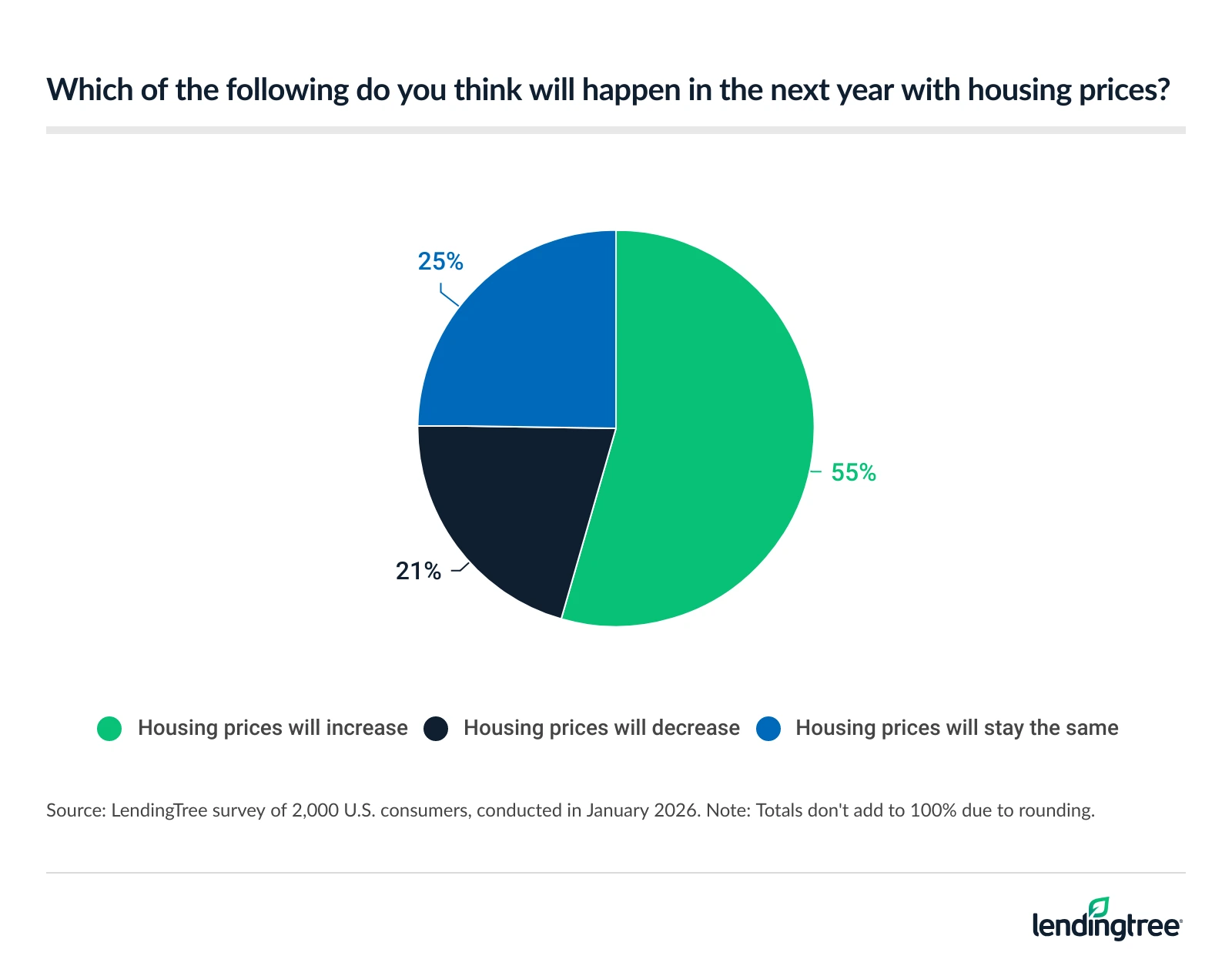

- Optimism is in short supply as Americans look ahead. 52% of Americans don’t believe they’ll ever see mortgage rates as low as they were in 2020-21, while just 20% believe they will. Meanwhile, 55% believe housing prices will increase in the next year — and two-thirds of that group believe prices will rise by at least 5%, including 19% who expect an increase of 10% or more. Lastly, 56% believe President Donald Trump won’t be good for the housing market in 2026.

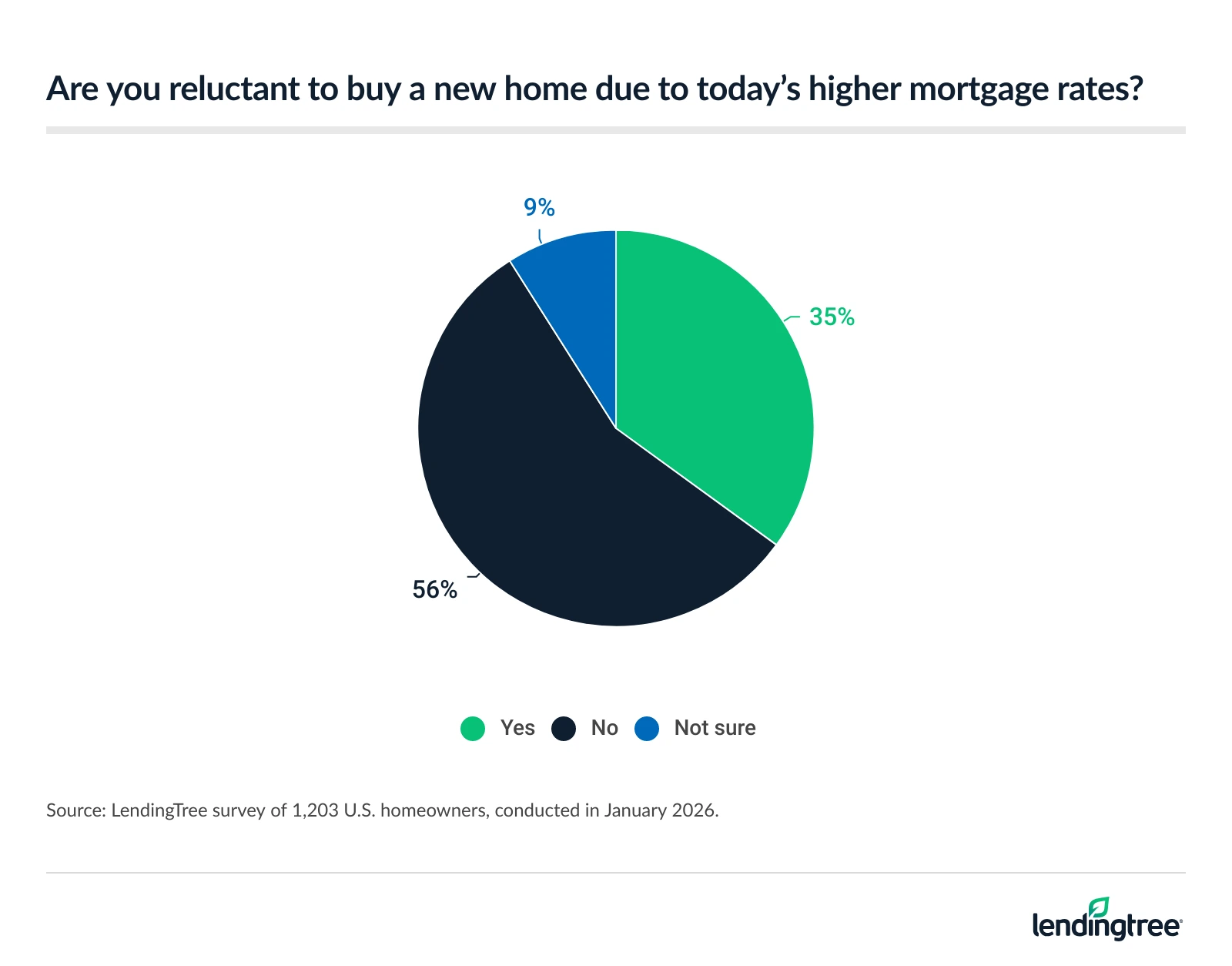

- Many homeowners may already live in the last home they’ll ever buy. 21% of homeowners expect they won’t ever look to buy a home again, while 13% say they don’t think they’ll ever be able to buy another home. 35% of homeowners say they’re reluctant to buy again due to higher mortgage rates, including 62% of Gen Z homeowners. Still, affordability could change minds: 29% of Americans (and 46% of Gen Zers) would consider a 50-year mortgage if it helped them buy a home this year.

Nearly a third of Americans are rooting for a housing market crash

As with seemingly everything these days, Americans are largely split on whether the housing market is at risk of a crash in the next year. While 36% believe it is, 33% say it isn’t and 31% say they aren’t sure. The younger you are and the higher your household income, the more likely you are to believe the market is at risk of crashing.

People don’t just think the housing market is at risk of crashing. Many are actively rooting for it to happen. That’s what 31% of respondents told us, including 59% of Gen Zers ages 18 to 29. A far larger percentage (54%) say they don’t want the market to crash, while another 15% aren’t sure. However, the fact that nearly 1 in 3 Americans wants to see the housing market crash is eye-opening.

Why would these people want that to happen? The most common responses were, in order:

- They think a crash will lead to greater stability in the future

- They think a crash will lower their property tax payments on their current home

- They think a crash will help them buy a home

- They think a crash will help usher in broader economic reform

Separately, 27% of those who don’t currently own a home believe a housing market crash is the only way they could afford to buy a home. Nearly 4 in 10 parents of young kids (39%), 34% of millennials ages 30 to 45 and 32% of men agree with that sentiment.

Americans’ housing market anxieties stretch far and wide

Given how many Americans are rooting for a crash, it should come as no surprise that high home prices (45%) are Americans’ biggest worry about the housing market. Other housing market worries include increasing property taxes (38%), high mortgage rates (35%) and the market’s impact on the economy overall (30%).

High prices are the primary worry for most demographics, though not all. Property taxes are the biggest worry for baby boomers ages 62 to 80 (46%), those earning $100,000 or more annually (44%) and parents with children 18 or older (42%).

Meanwhile, parents of young kids (44%), millennials (42%) and six-figure earners (41%) are the most likely to be worried about high interest rates.

Optimism is in short supply as Americans look ahead

Americans aren’t just worried about today’s housing market. In many cases, they’re downright pessimistic.

For example, 55% of Americans think housing prices will rise in the next year. Two-thirds (66%) of that group believe prices will rise by at least 5%, including 19% who expect them to rise by 10% or more.

At 62%, parents of young kids are the most likely to think that prices will rise in the next year. Younger Americans are more likely than older generations to think that, with 60% of both Gen Zers and millennials saying so, versus 51% of Gen Xers ages 46 to 61 and 47% of boomers.

They’re not just downbeat about housing prices. More than half (52%) of Americans don’t believe they’ll ever see mortgage rates as low as they were in 2020-21, while just 20% believe they will. (The interest rate on a 30-year, fixed-rate mortgage was 2.65% at the start of January 2021. Today, that number is 6.01%.) Also, 56% of Americans believe President Donald Trump won’t be good for the housing market in 2026. There’s a significant gender split when it comes to views of the president’s effect on the housing market: 62% of women say he will not be good for it, while just 50% of men say the same.

Many homeowners may already live in the last home they’ll ever buy

When we asked homeowners, “Do you think you’ll ever be able to buy a home again?” respondents’ answers were generally more optimistic than those to some other questions:

- 50% said yes

- 21% said, “No, I won’t ever look to buy again”

- 13% said, “No, I don’t think I’ll ever be able to buy again”

- 16% weren’t sure

The 21% figure shouldn’t necessarily be seen as entirely pessimistic. It could include a substantial number of people who are in their “forever home” and have no intention of moving, regardless of what happens in the housing market. Given that, these numbers indicate that far more homeowners think they’ll eventually be able to buy a home again than those who feel otherwise.

That doesn’t mean that everything is perfect. More than a third of homeowners (35%) say they’re reluctant to buy a home again because of today’s high interest rates. The younger you are and the higher your income, the more likely you are to say so. Also, male homeowners are much more likely than women to say so (42% of men, versus just 27% of women).

In an attempt to combat housing unaffordability, President Trump last year floated the idea of offering a 50-year mortgage — one that runs far longer than the traditional 30-year mortgage that dominates the American housing market. While the idea was panned by many observers from both parties for being too expensive in the long run and too slow to grow equity, our survey shows that it has some real appeal for consumers. We found that 29% of Americans (and 46% of Gen Zers) would at least consider getting a 50-year mortgage if it would help them buy a home this year.

In moments of uncertainty, control what you can control

No one has a crystal ball to tell them what the next day looks like, much less the next year. While a housing crash seems highly unlikely, there’s still an enormous amount of uncertainty in the economy. That can make you feel helpless and confused about what to do next.

Your best move in uncertain times is to control what you can control and create the best financial foundation for yourself to deal with whatever may come. That’s certainly true when it comes to shopping for a home, too.

Here are a few tips to help you do that:

- Get your credit in order. Life gets really expensive when you have crummy credit, and nowhere does it hit you harder than when you apply for a mortgage. Low credit scores mean higher interest rates, and that means more interest paid over the life of the mortgage. Even a slightly higher rate can cost you tens of thousands of dollars. The sooner you can start working to improve your credit, the better.

- Pay down your high-interest debt. Easier said than done, for sure. However, every dollar that you’re putting toward that credit card debt is a dollar that can’t go toward a down payment or other costs involved in buying a home.

- Start saving now. Yes, even if you’re paying down debts. It’ll take you a little bit longer and cost you a little more to pay off that debt, but it’ll be worth it. The sooner you can start building your home savings fund and let compounding interest work its magic in a high-yield savings account, the better. Don’t go into the process thinking that you have to save enough to make a 20% down payment on a house — that’s too daunting and demotivating. Start small and keep going. A little bit saved consistently over time can grow into a lot.

- Run the numbers to understand what you can afford. Just because someone will loan you a certain amount of money doesn’t mean you need it or can afford to pay it off. (Read that again.) It’s easy to feel flattered when a lender tells you that they’ll give you a huge amount of money to put toward a home, but it’s your job to make sure you understand what you can afford. LendingTree’s mortgage affordability calculator can help.

- Shop around. When banks compete, you win. It’s what we always say here at LendingTree, and it’s as true today as it was when we first said it decades ago. Mortgage offers can vary widely among lenders, and you can even play lenders off of each other to score the best possible rate, especially if you have good credit. However, it will only happen if you take the time to shop around.

Methodology

LendingTree commissioned QuestionPro to conduct an online survey of 2,000 U.S. consumers ages 18 to 80 from Jan. 14 to 17, 2026. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. Researchers reviewed all responses for quality control.

We defined generations as the following ages in 2026:

- Generation Z: 18 to 29

- Millennials: 30 to 45

- Generation X: 46 to 61

- Baby boomers: 62 to 80

View mortgage loan offers from up to 5 lenders in minutes