Assets, Liabilities, Equity: Balance Sheet 101

Every business balance sheet has three parts: assets, liabilities and equity. Assets are what your business owns, like cash, inventory and equipment. Liabilities are what your business owes, including payables, credit lines and loans. Equity is what’s left over after you subtract liabilities from assets. Essentially, it’s your stake in the business.

These three elements make up the accounting equation: Assets = Liabilities + Equity.

This formula should always balance, which is why the financial statement reporting these figures is called a balance sheet. And your balance sheet helps you gauge your business’s financial health, qualify for financing and file tax returns.

Assets vs. Liabilities vs. Equity

| Assets | Liabilities | Equity |

|---|---|---|

| What you own | What you owe | What’s left after debts |

| Cash | Business loans | Owner investment |

| Equipment | Accounts payable | Retained earnings |

| Increases company resources | Increases obligations | Represents ownership |

Assets: what your business owns

Assets are everything your business owns that has economic value. Lenders consider the strength of your asset base when deciding whether to extend credit.

Your balance sheet might include several different types of assets.

| Category | Definition | Example |

|---|---|---|

| Current | Converts to cash within one year | Checking account balance, accounts receivable, inventory |

| Noncurrent | Takes longer than a year to convert to cash | Manufacturing equipment, buildings |

| Liquid | Converts to cash quickly without losing value | Cash, marketable securities |

| Illiquid | Takes time to sell or loses value in a rushed sale | Real estate, specialized machinery |

| Tangible | Has a physical form you can touch | Vehicles, office furniture |

| Intangible | Has no physical form but still holds value | Patents, trademarks, goodwill |

Most assets fall into more than one category. For example, a company vehicle is noncurrent, illiquid and tangible all at once.

Knowing how to categorize your assets helps you assess how quickly you could raise cash if you needed it.

Depreciation is an accounting method for spreading the cost of an asset over its useful life rather than expensing the entire cost in the year you buy it.

Businesses depreciate assets because it spreads an asset’s cost over the time it’s used to generate revenue, making profits more accurate. It also reflects the reality that most tangible assets lose value as they age and wear down.

Depreciation affects your financial statements and your taxes. On your balance sheet, it lowers an asset’s value over time. On your income statement, it counts as an expense, which reduces profit. On your tax return, it can lower your taxable income.

Liabilities: what your business owes

Liabilities are what your business owes to others. They’re a legitimate, often necessary part of financing business growth.

Few businesses have the cash on hand to cover every purchase, so taking on debt to buy equipment, manage cash flow or expand operations is a normal part of running a company.

| Category | Definition | Example |

|---|---|---|

| Current | Due within one year | Accounts payable, short-term loans, accrued payroll |

| Long-term | Due in more than one year | Mortgages, long-term business loans |

| Contingent | Depends on the outcome of a future event | Pending lawsuit, product warranty claim |

Contingent liabilities typically don’t appear on the balance sheet because their timing and amount are uncertain. Instead, you include an explanation of contingent liabilities in the footnotes of your financial statements.

Accurately tracking your liabilities tells you how much of your business’s future profits and cash flows are already spoken for.

Debt itself isn’t a problem, but certain warning signs are. Watch for:

- Liabilities exceed assets. Your business owes more than it owns, leaving negative equity.

- Negative working capital. Current liabilities exceed current assets, signaling a cash crunch is coming.

- High debt-to-equity (D/E) ratio. You calculate your debt-to-equity ratio by dividing total liabilities by total shareholder equity. A “normal” D/E ratio varies by industry, but a high one indicates you rely heavily on borrowed money rather than owner investment.

- Declining retained earnings. Profits shrink or losses eat into what you’ve built up.

Any of these can signal you’ve taken on more obligations than the business’s financial position can support

Equity: what’s left for the owners

Equity is what remains for you, as the owner, after you subtract liabilities from assets.

Equity = Assets − Liabilities

Theoretically, it’s what you’d have left if you liquidated your business today, using assets to pay off liabilities.

What makes up equity?

Depending on your business structure, your equity accounts might include:

- Paid-in capital. Money you and other owners invested directly in the business in exchange for ownership.

- Retained earnings. Cumulative profits the business keeps rather than distributes to owners.

- Owner’s draws or dividends: Withdrawals that reduce equity when owners take money out of the business.

- Treasury stock. Shares a corporation repurchased from shareholders.

Tracking equity over time shows you whether the business is building real value or just cycling debt.

The book value of your business is what your balance sheet reports: total assets minus total liabilities equals equity. Market value is what your business would actually sell for. There’s usually a big difference between those two numbers, since book value reflects historical costs and accounting rules, while market value reflects earning potential, industry conditions and buyer demand. A business valuation determines the market value of the business.

The accounting equation: Assets = Liabilities + Equity

The accounting equation must stay in balance after every business transaction. This works because of double-entry accounting. Every transaction affects at least two accounts, so the equation never tips out of balance. If one side of the equation increases, either the other side increases, too, or something else on the same side decreases to offset it.

Real-world examples

Here are a few examples to show you how double-entry accounting works.

- Buying equipment with a loan. You purchase $20,000 in equipment financed entirely by a loan. Assets increase by $20,000 (equipment), and liabilities increase by $20,000 (loan payable).

- Investing personal money into the business. You deposit $10,000 of your own cash into the business account to weather a temporary cash shortage. Assets increase by $10,000 (cash), and equity increases by $10,000 (paid-in capital).

- Keeping profits in the business. The business earns $5,000 in net income and you leave it in the company rather than withdrawing it. Assets increase by $5,000 (cash, assuming you collected the profit), and equity increases by $5,000 (retained earnings).

In each case, the transaction affected both sides of the accounting equation, so the balance sheet stays in balance. If it doesn’t balance, you have an error somewhere in your books.

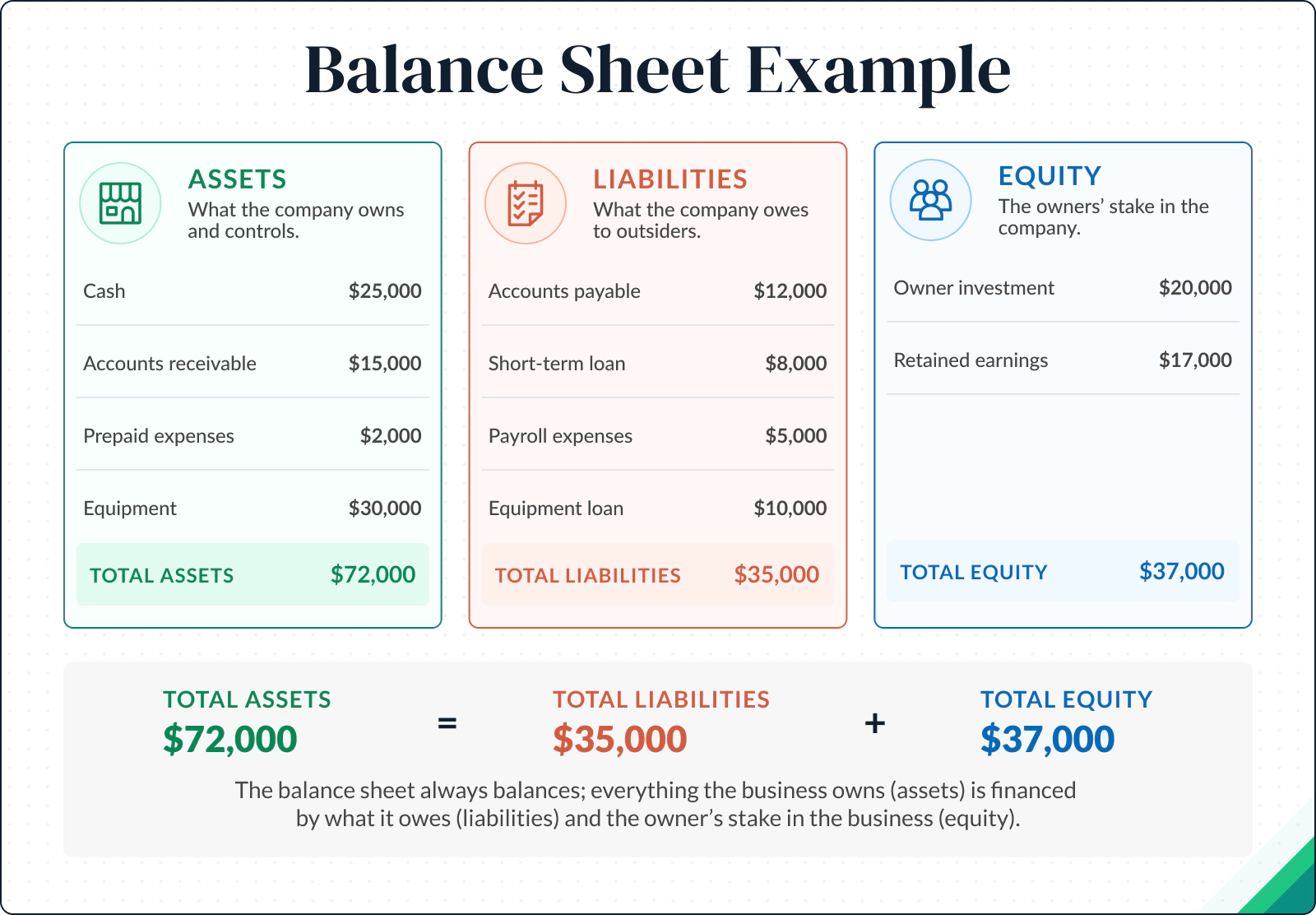

Balance sheet example

Why tracking assets and liabilities matters

Tracking your assets and liabilities affects three essential areas of running your business:

Cash planning and liquidity

Part of managing cash flow depends on knowing which assets you can convert to cash quickly and which liabilities are coming due soon. This visibility lets you time large purchases, plan for loan payments and build a cash buffer before a shortfall hits.

Getting a business loan

When you apply for a business loan, lenders will review your balance sheet carefully. They assess the assets you can use as collateral. They also analyze your liabilities to judge how much additional debt your business can reasonably carry. A healthy, organized and well-documented balance sheet can speed up approval and even improve your loan terms.

Monitoring financial health over time

Comparing your balance sheet across periods helps you monitor your business’s financial health. When you see asset balances growing, manageable liabilities and increasing equity, it’s a sign the business is moving in the right direction. Taking a closer look at declining assets, stagnant equity or growing liabilities helps you identify what’s driving the trend early while there’s still time to make changes.

Key formulas every business owner should know

Tracking a few metrics turns your balance sheet from a static snapshot into a working tool for decision-making. Here are five to know.

- Accounting equation: Assets = Liabilities + Equity. This is the foundation of your balance sheet. What you own equals what you owe plus the business’s book value.

- Owner’s equity: Equity = Assets − Liabilities. This tells you your actual stake in the business after subtracting everything you owe.

- Debt-to-equity ratio: Total Liabilities ÷ Total Equity. This measures how much of your business relies on borrowed money versus owner investment. A high ratio signals heavier reliance on debt.

- Working capital: Current Assets − Current Liabilities. This shows whether you have enough short-term resources to cover your short-term obligations.

- Return on assets: Net Income ÷ Total Assets. This measures how efficiently the business turns its assets into profit.

Frequently asked questions

Assets are everything your business owns, while equity is what remains after subtracting what your business owes from those assets. In other words, equity is your net stake in the business, not the full value of its assets.

Yes. Negative equity occurs when you have more liabilities than assets, and your business owes more than it owns. Negative equity is a sign of financial distress. It makes it difficult to secure financing or attract investors until you rebuild the business asset base or reduce its debt.

Most small businesses should update their balance sheet monthly, alongside their profit and loss statement. If you’re actively seeking financing or closely monitoring cash flow, you may want to review it weekly.

Lenders typically look at your assets for collateral, your debt-to-equity ratio to see how leveraged the business is and your working capital to assess short-term liquidity. You have a better chance of loan approval when your balance sheet shows steady growth and manageable liabilities.

Compare business loan offers