‘Buy Now, Pay Later’ Financing Used for Things Shoppers Can’t Afford

”Buy now, pay later” financing lets shoppers split large purchases into multiple smaller payments, typically through a loan or installment agreement. These products, which are usually advertised at checkout when shopping online, provide a way for consumers to buy things they couldn’t normally afford.

Two in 3 shoppers who’ve used buy now, pay later financing said it’s caused them to spend more than they would have otherwise, a new LendingTree survey of 1,040 Americans found. The survey also revealed that these financing companies have a dedicated base of young consumers, many of whom don’t know how much they’re being charged in interest. Learn more in the breakdown below.

Key findings

- Buy now, pay later services, like Affirm and Klarna, are popular financing tools. About a third of consumers have utilized this type of financing. Among those who’ve made a purchase with buy now, pay later, 62% have done so five or more times and 81% said they’re likely to use it again.

- Having the option to buy now and pay later causes consumers to overspend. Two-thirds of shoppers who have used a buy now, pay later service said they typically buy more than they would if they had to pay for everything upfront, and 47% said they wouldn’t have made their full purchase if they didn’t have the option to finance.

- Most use buy now, pay later for discretionary purchases like clothing and shoes. One in 3 consumers utilizes buy now, pay later financing to purchase things they normally wouldn’t be able to afford. Designer purchases are popular, as 69% who’ve used buy now, pay later financing did so to buy a designer item — a third of these shoppers have done this multiple times.

- Young shoppers frequently use buy now, pay later agreements to finance purchases. They’re much more popular among Gen Zers (59%) and millennials (47%) than they are with Gen Xers (28%) and baby boomers (9%). Young shoppers are also less likely to consider buy now, pay later to be a form of debt.

- Late fees and interest charges are the norm for many buy now, pay later shoppers. More than 7 in 10 consumers who have used buy now, pay later financing were charged fees or interest for missed payments. Nearly a third of shoppers didn’t know what the interest rate and fees would be before agreeing to finance their purchase.

Buy now, pay later is emerging as a popular financing method

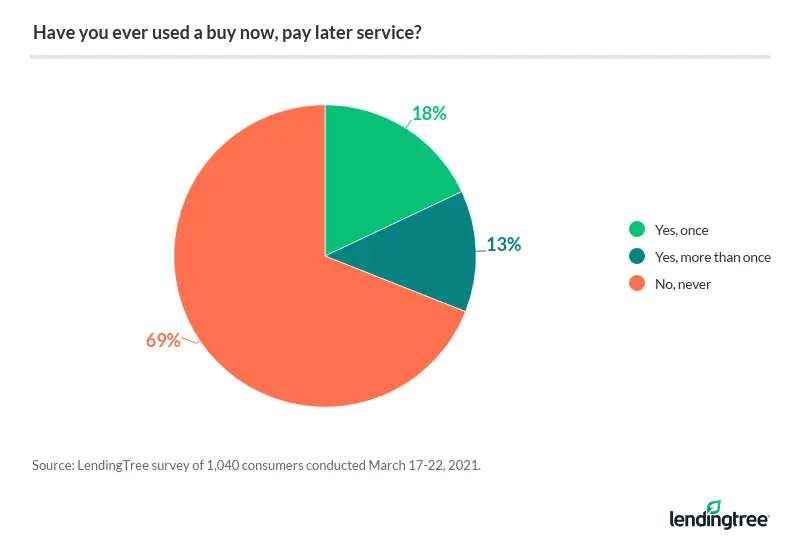

Buy now, pay later services like Affirm offer online shoppers a way to break their purchases into smaller payments, and they’re becoming a popular tool among American consumers. About a third of shoppers (31%) have used a buy now, pay later service. The most commonly used buy now, pay later financing companies among respondents were:

- PayPal (39%)

- Klarna (26%)

- Affirm (25%)

- Cash App Afterpay (25%)

The vast majority (83%) of those who have utilized buy now, pay later financing did so within the past year. That figure includes about 1 in 6 who had used it within a week of taking the survey.

The main reason some (39%) consumers haven’t used buy now, pay later financing is they don’t know what it is. Other respondents said they’d rather just pay for the product upfront without having to worry about making payments (33%), and 19% noted that it seems like a gateway to overspending.

Buy now, pay later financing is emerging as a popular alternative to traditional personal loans and credit cards. Among those who have utilized this financing option, most are frequent customers, as 62% have utilized buy now, pay later financing five or more times. About 4 in 5 (81%) shoppers who have utilized buy now, pay later financing are likely to use this service again.

“The fact that so many folks have used these loans five or more times is amazing,” LendingTree chief consumer finance analyst Matt Schulz said. “It is an incredibly good sign for the future of these products. They certainly seem to be here to stay.”

Many shoppers use buy now, pay later to purchase things they can’t afford

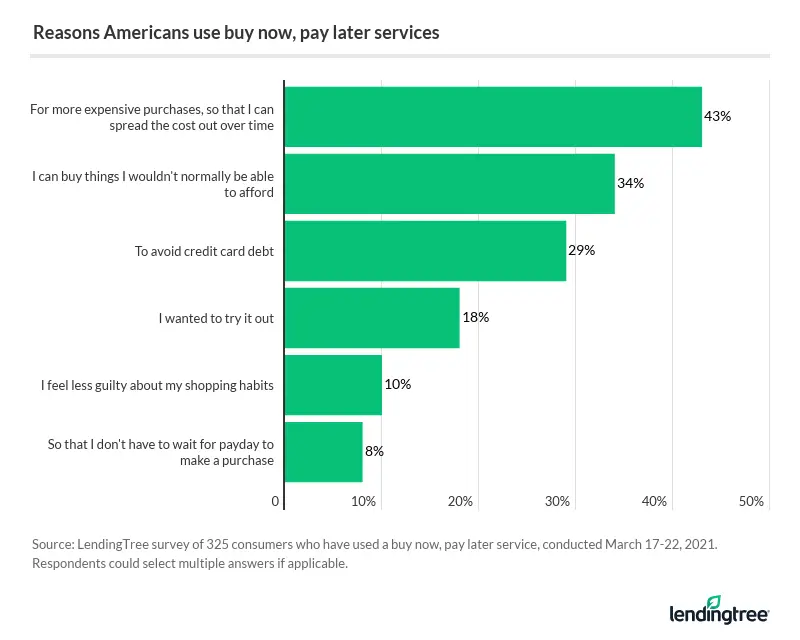

The No. 1 reason shoppers used a buy now, pay later service was to spread out the cost of more expensive purchases over time, but more than a third of consumers utilize buy now, pay later financing to purchase things they normally wouldn’t be able to afford.

Having the option to break up their purchase into smaller payments also leads consumers to overspend. Two-thirds of consumers said they typically spend more using buy now, pay later than they would if they had to front the money at the time of purchase.

Nearly half of shoppers admit they wouldn’t have made their full purchase should buy now, pay later not have been an option. That breaks down to 32% who would have bought fewer items, and 15% who wouldn’t have bought anything at all.

Those impacted by pandemic layoffs or furloughs were four times as likely to use buy now, pay later financing. Six in 10 Americans laid off or furloughed have used buy now, pay later financing, compared with 15% who didn’t experience pandemic-induced income loss. If your income has been affected by the coronavirus pandemic, check out these tips on how to manage your money.

Buy now, pay later gives average shoppers a gateway to luxury spending

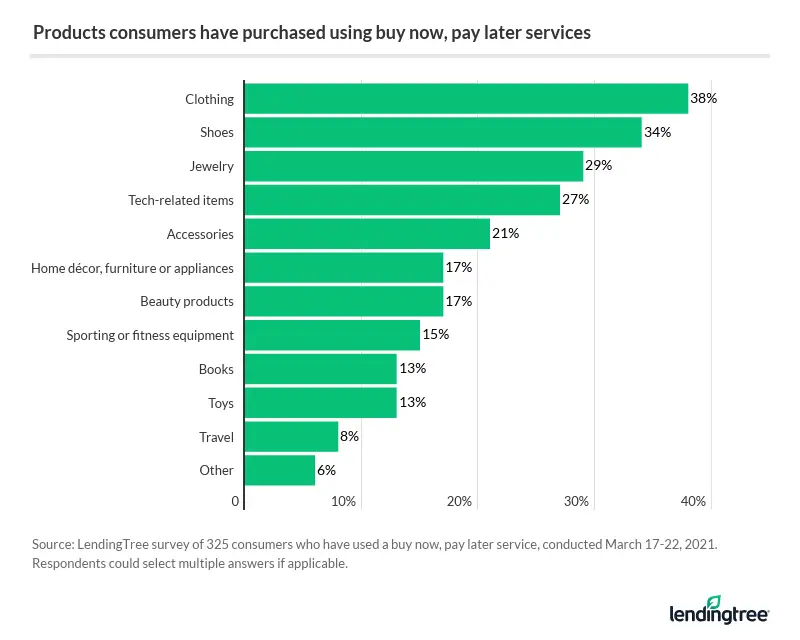

While it’s generally discouraged to take on debt for discretionary purchases, shoppers are using buy now, pay later financing to purchase gratuitous items. Clothing, shoes and jewelry are the top items Americans are most likely to finance using buy now, pay later.

Nearly 70% of those who have used a buy now, pay later service did so to purchase a designer item, such as a Gucci belt or Louis Vuitton handbag. Of that group, about half have even done so multiple times.

Young shoppers are more likely to utilize buy now, pay later

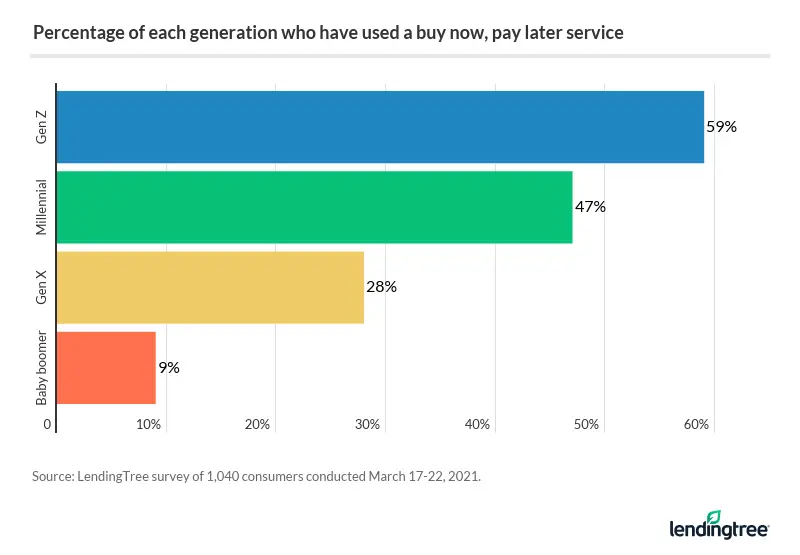

Buy now, pay later is most popular among shoppers 40 and younger. Fifty-nine percent of Gen Z shoppers (ages 18 to 24) have used a buy now, pay later service at least once, compared with 47% of millennials (ages 25 to 40), 28% of Gen X shoppers (ages 41 to 55) and 9% of baby boomers (ages 56 to 75).

The fact that so many younger shoppers flock to buy now, pay later doesn’t come as much of a surprise to Schulz. Gen Z and millennial shoppers are more leery of using credit cards, so they may find the prospect of a finite repayment schedule offered by a loan more alluring.

“We’ve seen that people tend to overspend with these loans, and Gen Z and millennials are likely to have far smaller financial margins for error than Gen X and boomers, so they’re taking a bit more of a risk,” Schulz said.

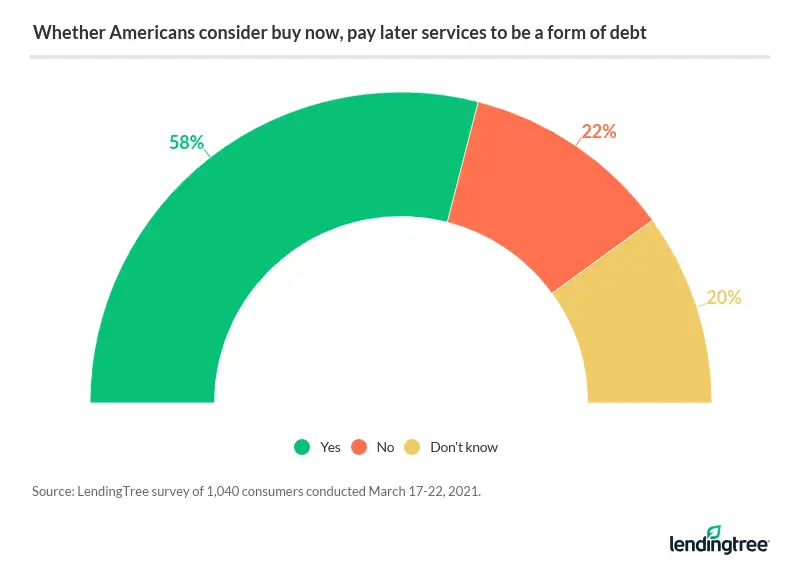

Younger shoppers are also less likely to view buy now, pay later agreements as a form of debt. Just 38% of Gen Z shoppers believe this, versus 53% of millennials, 62% of Gen X shoppers and 68% of baby boomers.

The cost of buy now, pay later financing is often hidden

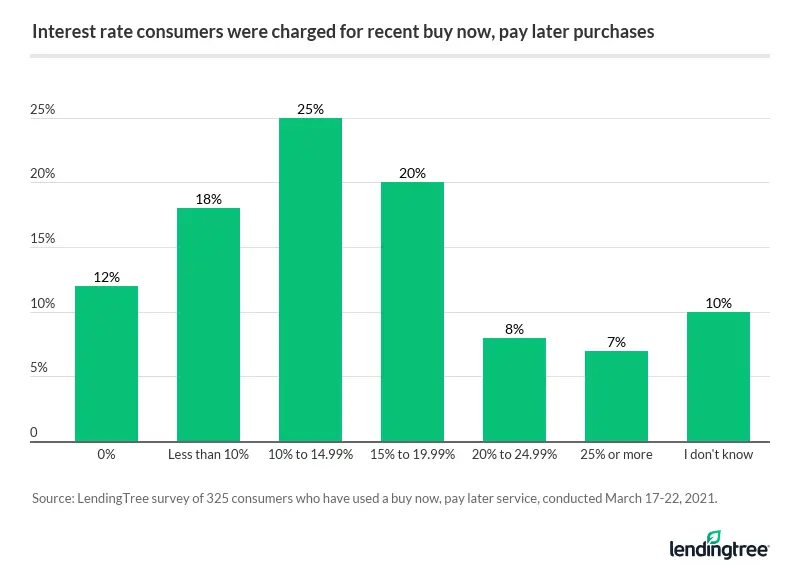

The majority of shoppers who use buy now, pay later financing end up paying for it in some way. About 7 in 10 buy now, pay later users have been charged interest or fees for missed payments:

- 31% were charged a late fee but not interest

- 23% were charged interest but not a late fee

- 18% were charged both interest and a late fee

Many buy now, pay later loans must be repaid every two weeks rather than once a month, which makes it easier to miss payments, according to Schulz.

Thirty-one percent of shoppers who entered a buy now, pay later agreement didn’t know what the interest rate and fees would be before agreeing to finance their purchase. One in 10 still have no idea what interest rate they’re paying.

While many buy now, pay later agreements only let you split your purchase into a few monthly installments, many shoppers are still paying off these loans. One in 7 (14%) buy now, pay later shoppers have owed money to one of those services for over a year. Just 29% said they’ve completed all their payments.

Methodology

LendingTree commissioned Qualtrics to conduct an online survey of 1,040 U.S. consumers from March 17-22, 2021. The survey was administered using a non-probability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2021:

- Generation Z: 18 to 24

- Millennial: 25 to 40

- Generation X: 41 to 55

- Baby boomer: 56 to 75

While the survey also included consumers from the silent generation (defined as those 76 and older), the sample size was too small to include findings related to that group in the generational breakdowns.

Get personal loan offers from up to 5 lenders in minutes

Recommended Articles

Current Investment Property Mortgage Rates: August 2026

Best $100,000 Personal Loans of August 2026

Back-to-School Shopping Defies Inflation: Families Spend Nearly the Same as Before the Pandemic

Delaware, D.C. and Texas Have the Highest Business Bankruptcy Filing Rates in the US

Best Health Insurance Companies in Georgia in 2026

Homebuyer Down Payments by Generation in the 50 Largest US Metros

Best Merchant Cash Advances in August 2026

How To Refinance a Car Loan With Bad Credit

Best Bad Credit Auto Refinance Companies in August 2026

Home Insurance Takes Up Nearly a Fifth of Monthly Housing Costs in Some States