BNPL Tracker: Nearly Half of BNPL Users Have Paid Late in the Past Year, Up for a Second Straight Year

A growing percentage of buy now, pay later (BNPL) users say they’ve paid late on one of these loans in the past year. Now, 47% of BNPL users have done so, up six percentage points from 2025 and 13 percentage points from two years ago.

That’s just one of the troubling findings in LendingTree’s 2026 Buy Now, Pay Later Report. We asked consumers about their behaviors and perspectives regarding these popular loans. Along with increased late payments, we found that more users are buying groceries with these loans and carrying three or more BNPL loans at once, and that more than half of BNPL users say they wouldn’t be able to make ends meet without them.

There’s some good news, however. A separate survey fielded in July 2026 found that BNPL lenders are highly likely to waive a late fee on a BNPL loan if borrowers ask.

Here’s more on what we found.

- Nearly half of buy now, pay later users say they’ve paid late on a BNPL loan in the past year. 47% of users say they’ve paid late in the past year, up from 41% in 2025 and 34% in 2024. (Another 15% say they’ve paid late before, but not in the past year.) However, 72% of late payers say their most recent late payment was no more than a week or so late.

- More than half of BNPL users say they wouldn’t be able to make ends meet without these loans. Among users, 54% agree that they need BNPL loans to make ends meet. Just 25% disagree. Among users most likely to say they need the loans to make ends meet: 62% of parents with kids younger than 18 and 59% of millennials.

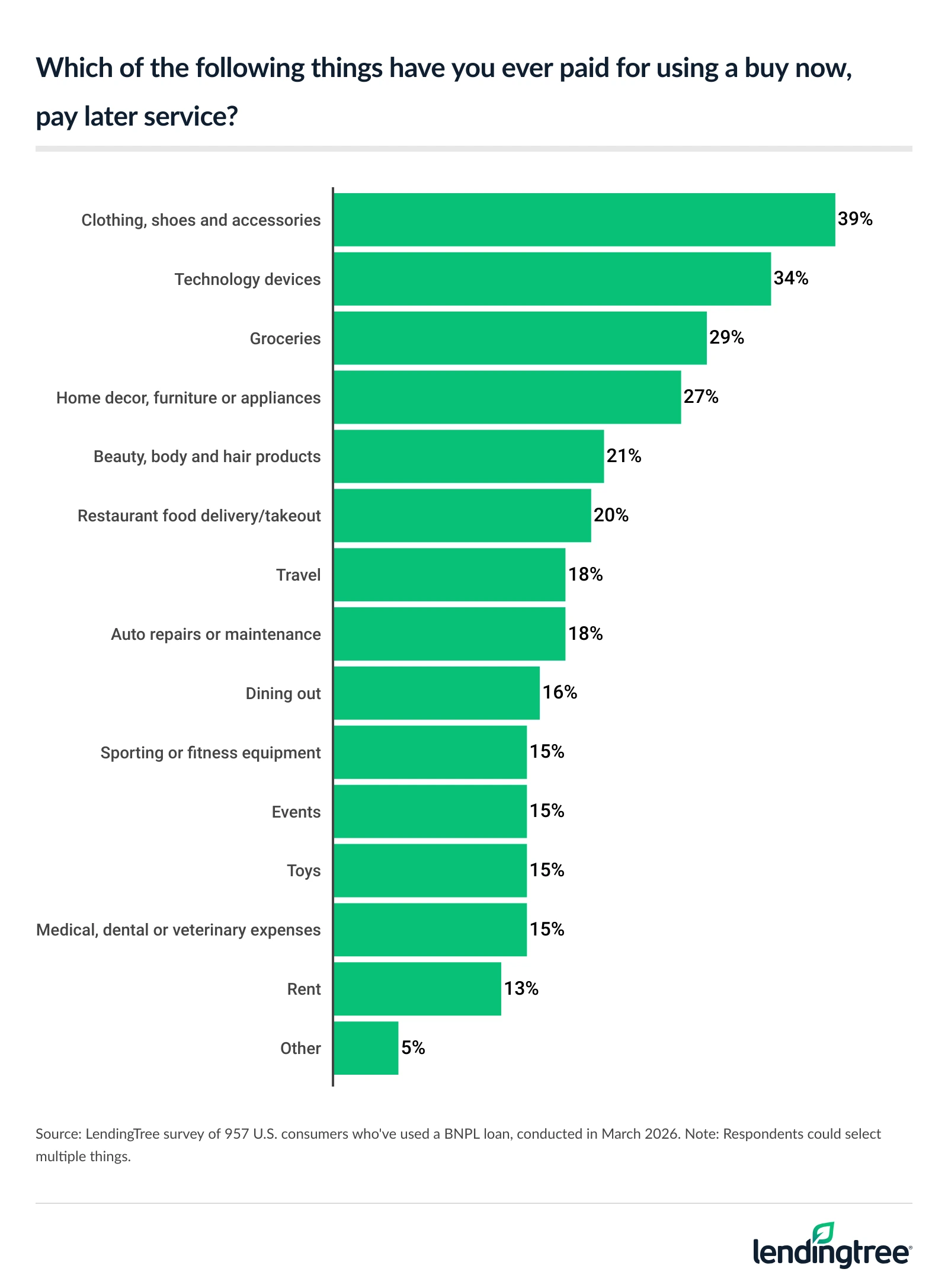

- Twice the rate of users have bought groceries with BNPL than two years ago. 29% of BNPL users say they’ve used the loans for groceries, up from 25% a year ago and 14% two years ago. 38% of Gen Z users have bought groceries with BNPL, as have 34% of users with kids younger than 18 and 33% of users who earn $100,000 or more. Only clothing, shoes and accessories (39%) and tech devices (34%) are more commonly bought via BNPL.

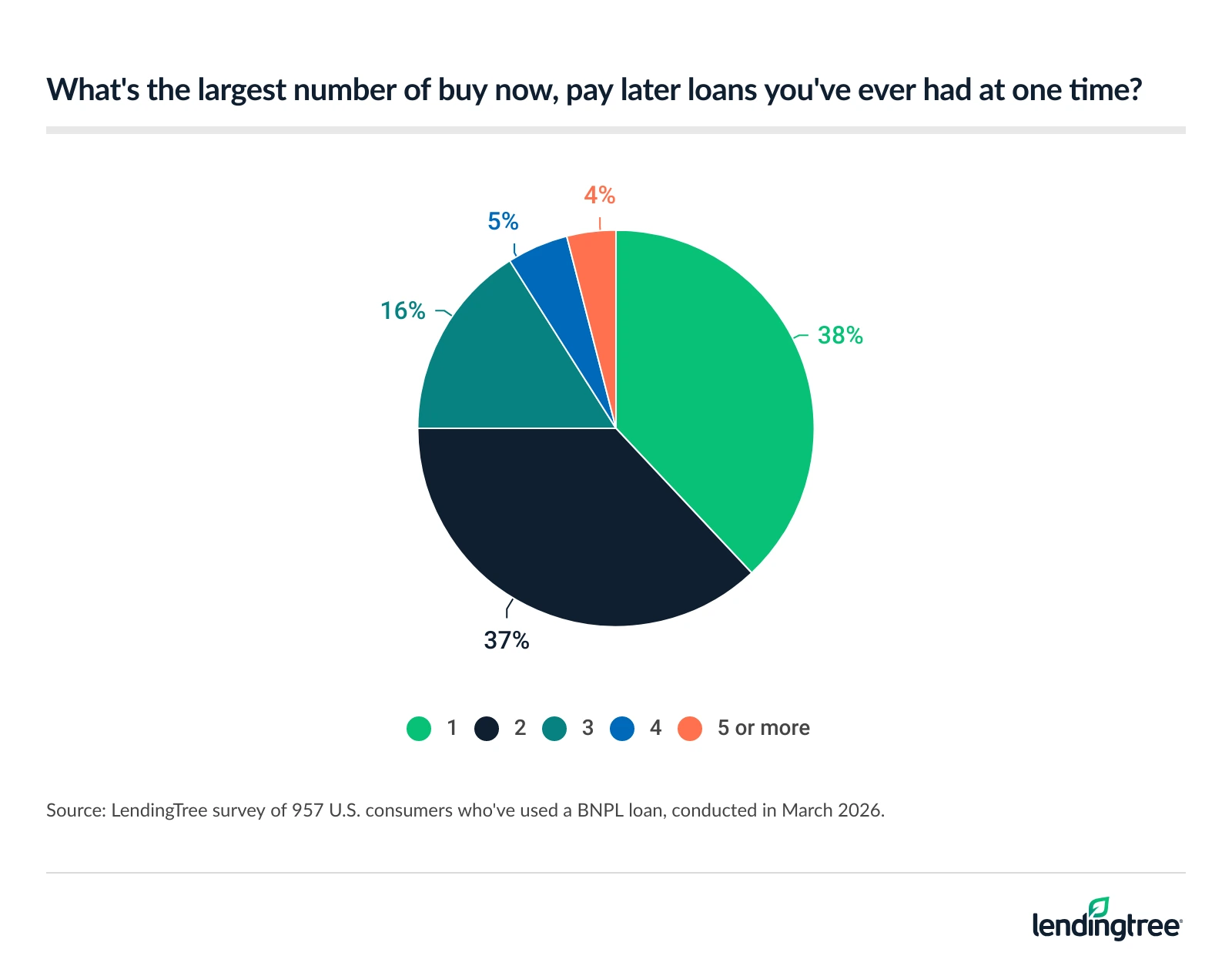

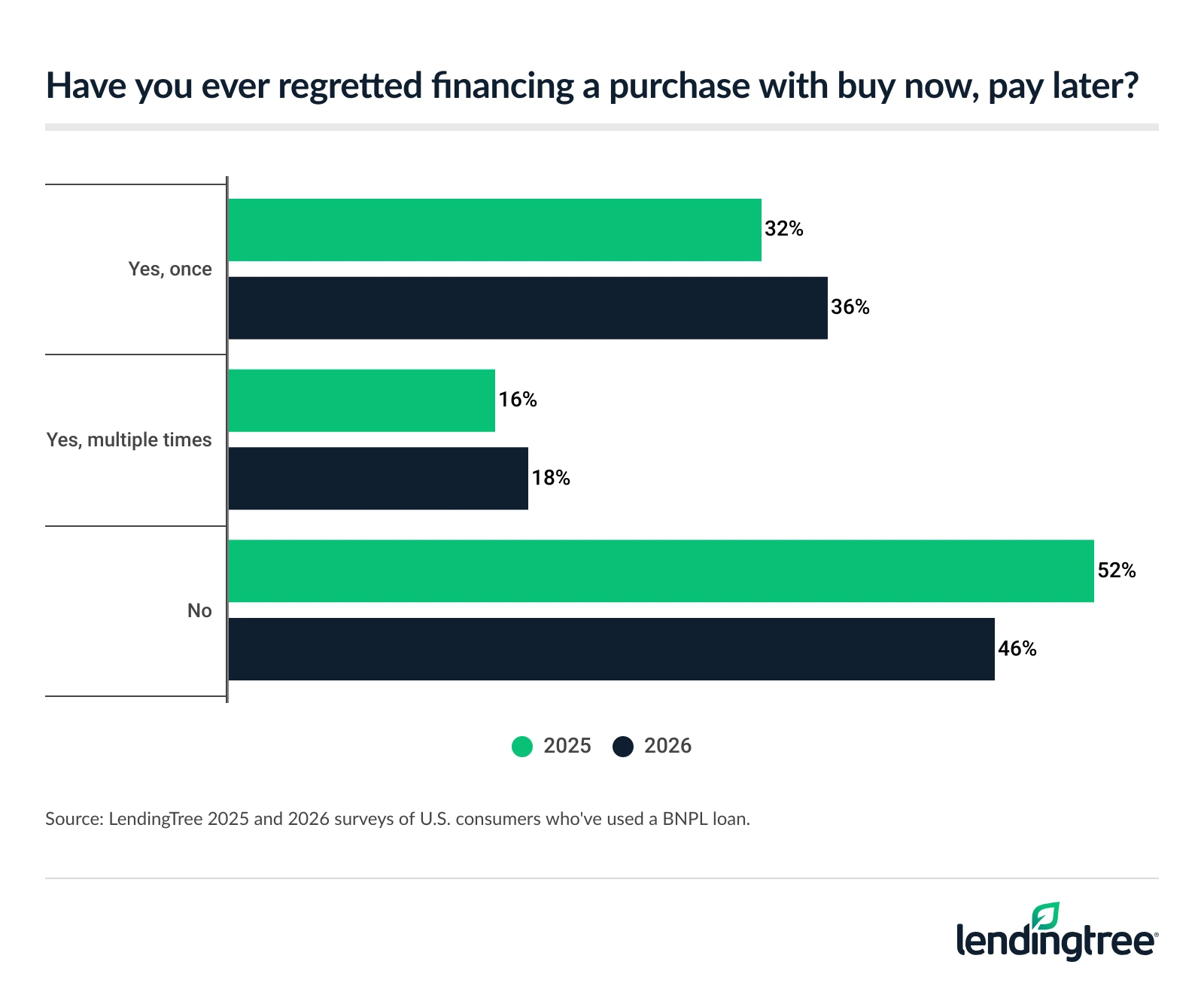

- 1 in 4 BNPL users have had three or more active BNPL loans at one time. That’s up slightly from 23% last year. Gen Zers (29%) and millennials (28%) are among the most likely users to say so. In addition, 68% of BNPL users agree that the loans cause them to overspend, and 54% of BNPL users say they’ve regretted buying with BNPL, including 18% who’ve regretted it multiple times.

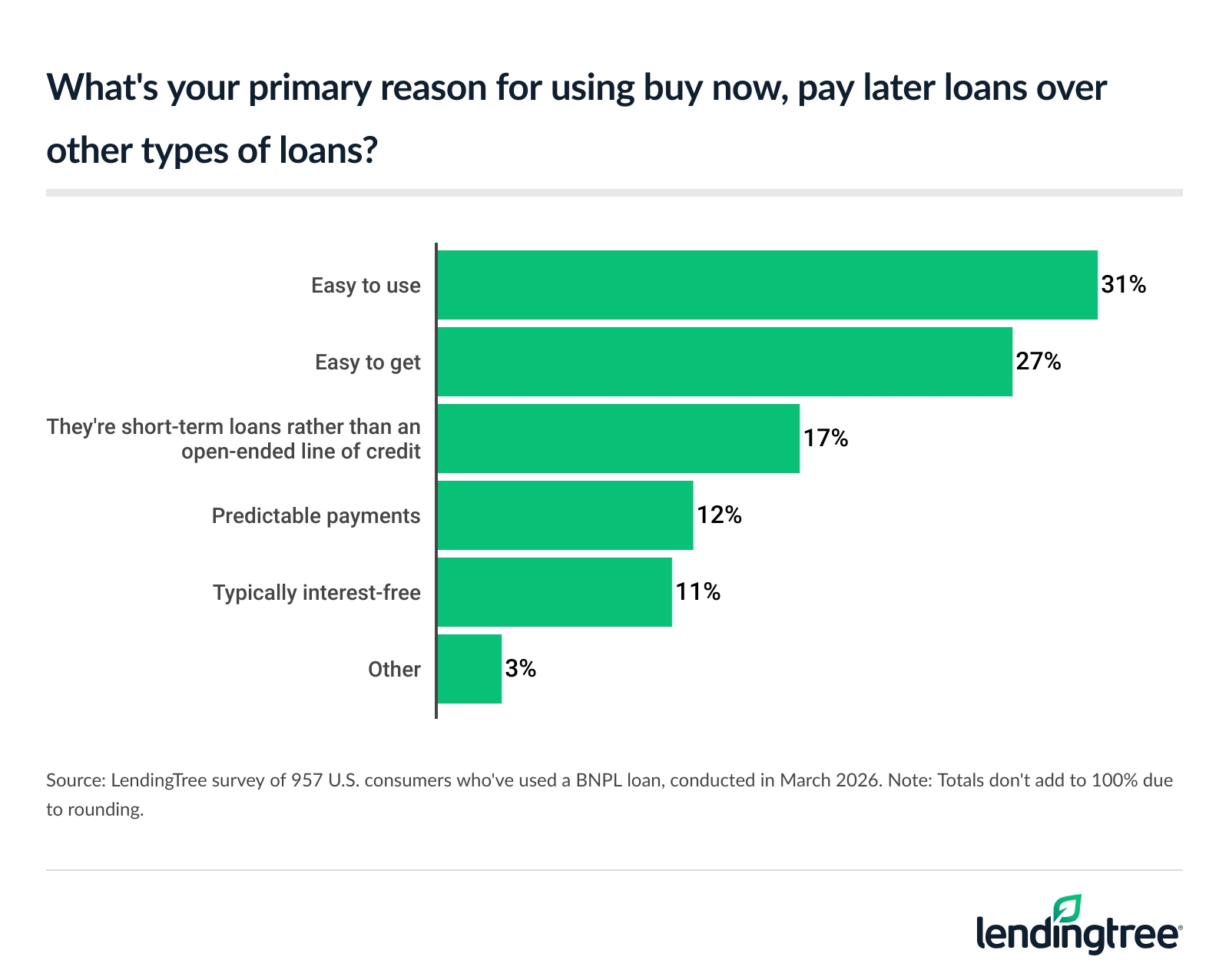

- Convenience matters more than cost to BNPL users. The top reasons given for choosing BNPL over other loans: They’re easy to use (31%) and easy to get (27%). Interestingly, the fact that they’re typically interest-free was the least chosen option. Just 11% say that, behind predictable payments (12%) and the fact that they’re short-term loans rather than an open-ended line of credit (17%).

How many Americans have used a buy now, pay later loan?

Buy now, pay later is everywhere. Nearly half of Americans (47%) say they’ve used a BNPL service, including 10% who have done so six or more times.

Among the demographic highlights:

- Nearly 7 in 10 parents with young kids (69%) have used these loans.

- Men are more likely than women to say they’ve done so (52% versus 42%).

- The younger you are and the more money you make, the more likely you are to say you’ve used one of these loans at least once. For example, 61% of Gen Zers ages 18 to 29 and 59% of those earning $100,000 or more a year say they’ve used one.

LendingTree’s July 2026 BNPL Tracker, which is fielded separately, shows that 37% of Americans are at least considering applying for a BNPL loan this month. That’s down five percentage points from June and far below the record 48% seen in December 2025 at the peak of the holiday shopping season.

Gen Zers and millennials ages 30 to 45 are the most likely age group to at least consider applying for a BNPL loan this month, with 49% of both groups indicating this. Gen Xers ages 46 to 61 are the next most likely (34%) and baby boomers ages 62 to 80 are the least likely to consider one of these loans (19%).

Additionally, 44% of Americans say they expect to apply for a BNPL loan in the next six months, down six points from June.

How many Americans have been late with a payment on a buy now, pay later loan?

A separate survey, also done in March 2026, showed that nearly half (47%) of BNPL users say they’ve paid late on a BNPL loan in the past year, and that percentage is on the rise. In 2025, 41% said they’d paid late in the past year, while 34% said the same in 2024. Another 15% say they’ve paid late before but not in the past year, while just 38% of users say they’ve never paid late.

That’s a high percentage of BNPL users paying late, but it might make sense given consumer confidence levels in our monthly BNPL Tracker. According to July’s BNPL Tracker, 55% of respondents who are at least considering getting a BNPL loan this month say they’re very confident they could pay off that loan without missing a payment. This is down four percentage points from June. Meanwhile, 30% say they’re only somewhat confident, up two percentage points from June.

While that adds up to 85% of people feeling at least some confidence about paying off BNPL loans on time, it still means a significant number of people take out these loans with doubts about whether they’ll be able to pay them back without incident. That’s far from ideal.

There’s some good news here: 72% of late payers say their most recent late payment was no more than a week or so late. That means that most late payers aren’t putting their credit at risk — it generally takes 30 days or longer for a late payment to impact your credit — but they’re setting themselves up to face a late fee.

Not all BNPL lenders assess late fees, but a December 2025 Consumer Financial Protection Bureau (CFPB) report said the average late fee assessed in 2023 was $9.99. The good news, however, is that you have a good chance of getting that fee waived if you ask. Our July BNPL Tracker shows that 90% of those who asked to have a late fee waived on a BNPL loan either got the fee reduced or got it waived entirely.

Why do people choose buy now, pay later loans over other types of loans?

Our March 2026 survey found that convenience is the biggest reason people choose BNPL over other options. Among BNPL users, 31% say their primary reason for using BNPL is that the loans are easy to use, while 27% say they’re easy to get.

Perhaps surprisingly, the fact that BNPL loans are typically interest-free was the least chosen of the options we offered, with just 11% saying that’s the primary reason for using them.

How much do Americans typically spend with a buy now, pay later loan?

According to the December 2025 CFPB report, the average transaction amount for a BNPL loan was $135 in 2023, the most recent year for which data is available.

However, our survey found that most BNPL users don’t stop at just one loan. In fact, 63% of BNPL users say they’ve held multiple BNPL loans at one time, including 25% who’ve held three or more at once.

Younger Americans are more likely to have stacked up three or more BNPL loans simultaneously, with 29% of Gen Z BNPL users and 28% of millennials having done so.

In addition, 68% of BNPL users agree that the loans cause them to overspend. Gen Z BNPL users are among the most likely to agree (83%), as are parents with young kids (77%), six-figure earners (75%) and men (71%).

What do Americans buy most often with a buy now, pay later loan?

Clothing, shoes and accessories (39%) and technology devices (34%) are the items most commonly bought with buy now, pay later, but groceries are moving up the list.

In our most recent survey, 29% of BNPL users say they’ve used BNPL for groceries, up from 25% a year ago and more than double the 14% seen two years ago. That puts groceries in third place on the list of items most commonly bought with BNPL, up one spot from last year.

Nearly 4 in 10 (38%) Gen Z BNPL users have bought groceries with BNPL, making it the second-most-common BNPL purchase in that age group, behind only clothing. Also, 34% of users with kids younger than 18 and 33% of users who earn $100,000 or more have bought groceries with BNPL. Even about 1 in 6 (16%) baby boomers have used BNPL for groceries.

The growth in grocery purchases with BNPL makes sense when you consider that 54% of BNPL users say they wouldn’t be able to make ends meet without BNPL loans, including 26% who strongly agree. Just 25% disagree, including 15% who do so strongly.

Among BNPL users, more than 6 in 10 parents of young kids (62%) say they need the loans to make ends meet, while 59% of millennials and 57% of Gen Zers say the same.

The survey also showed that 13% of BNPL users have used the loans to pay their rent. Also, more than 6 in 10 renters (61%) say they would at least consider “rent now, pay later” services like Esusu and Flex that allow renters to split monthly rent into two payments. Among renters, more than 3 in 4 parents with young kids (76%) would at least consider it, as would 73% of both Gen Zers and millennials. Men who rent are much more likely to consider it than women who rent (66% versus 57%).

Still, BNPL loans aren’t just being used for essentials. Our survey found that 20% of BNPL users have used the loans for restaurant delivery or takeout, 18% for travel, 16% for dining out and 15% for events.

What are the most popular buy now, pay later services?

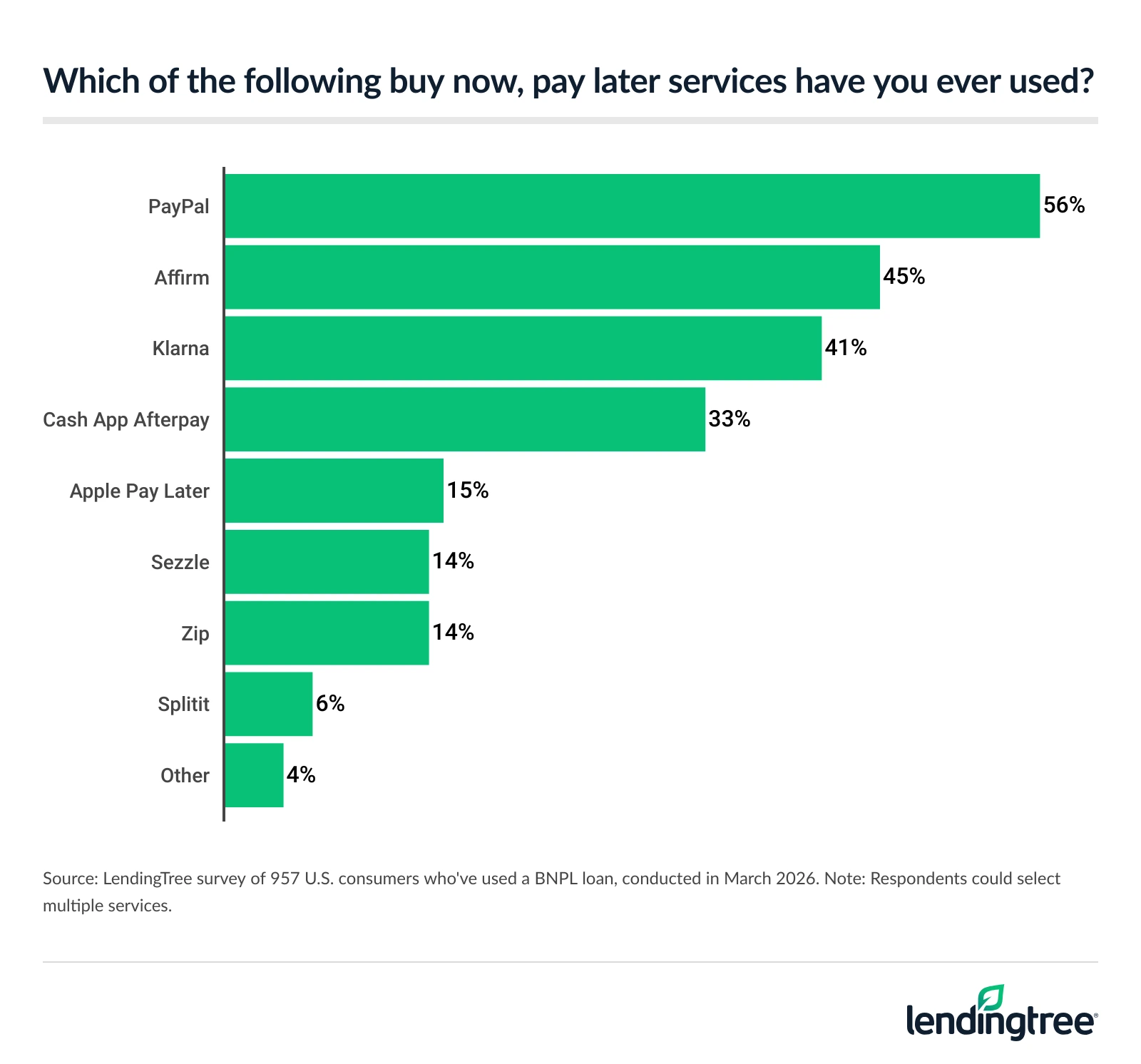

PayPal is the most commonly used BNPL lender, utilized by 56% of BNPL users in our survey. However, three other services — Affirm (45%), Klarna (41%) and Cash App Afterpay (33%) — are also popular. While these companies have been used by at least 33% of BNPL users, no other service tops 15%.

How do I avoid regretting my buy now, pay later purchase?

A growing percentage of BNPL users says they’ve regretted using the loans to make a purchase at least once. More than half (54%) say they’ve regretted a BNPL purchase, including 18% who regretted it more than once. Last year, 48% of BNPL users expressed regret, including 16% who regretted multiple purchases.

Men are more likely than women to express regret (60% versus 47%), and younger Americans are more likely than their older counterparts to do so.

While we all experience buyer’s remorse at times, here are a few things you can do to make it less likely that you’ll feel that way after your next BNPL purchase:

- Stick to one loan at a time. As our survey showed, BNPL’s popularity has exploded in part because it’s easier to get than many other loan types. However, that easy access also makes it dangerous. Getting more than one loan at a time makes managing them more challenging, especially since most of these payments are tied to checking accounts. Having multiple loans means you have to be certain you’ll have enough money in your account to make payments on all those loans when they’re due, typically every two weeks.

- Use a credit card instead if you think you may need to return the item. BNPL loans are notoriously tricky when it comes to returns. Returning an item purchased with a credit card is generally pretty straightforward, but that’s not often the case for BNPL purchases. For example, you may not be able to complete a return until you have paid off the BNPL loan. That could mean potentially waiting weeks — and making more payments — even after you’ve decided to return the product.

- Take your time. Retailers and lenders do an incredible job of making it easy to spend a lot of money in a short period. BNPL services are no exception. However, just because you can borrow the money doesn’t mean you should, and just because you’ve worked with one BNPL lender in the past doesn’t mean they all operate the same way. Before you get your next (or first) BNPL loan, take a moment to make sure you understand the basic rules, including any fees that might be involved. What you don’t know can cost you.

Methodology

LendingTree commissioned QuestionPro to conduct an online survey of 2,049 U.S. consumers ages 18 to 80 on March 3-6, 2026. Separately, for late payment questions, LendingTree commissioned QuestionPro to conduct an online survey of 2,060 U.S. consumers ages 18 to 80 on March 17-23, 2026. Lastly, for the monthly BNPL Tracker questions, LendingTree commissioned QuestionPro to conduct an online survey of 2,000 U.S. consumers ages 18 to 80 on July 2-8, 2026.

For all three surveys, we defined generations as the following ages in 2026:

- Generation Z: 18 to 29

- Millennial: 30 to 45

- Generation X: 46 to 61

- Baby boomer: 62 to 80

The surveys were administered using nonprobability-based samples, and quotas were used to ensure the sample bases represented the overall population. Researchers reviewed all responses for quality control.

Get personal loan offers from up to 5 lenders in minutes

Recommended Articles