Nearly 80% of Gen Z Homeowners Had Down Payment Help on Their Current Home, and 33% of Them Say They Couldn’t Have Bought Without It

Four in 10 homeowners received financial help with the down payment on their current home, including nearly 80% of Gen Z homeowners, and more than a third of those who got help say they wouldn’t have been able to buy their home when they did without it.

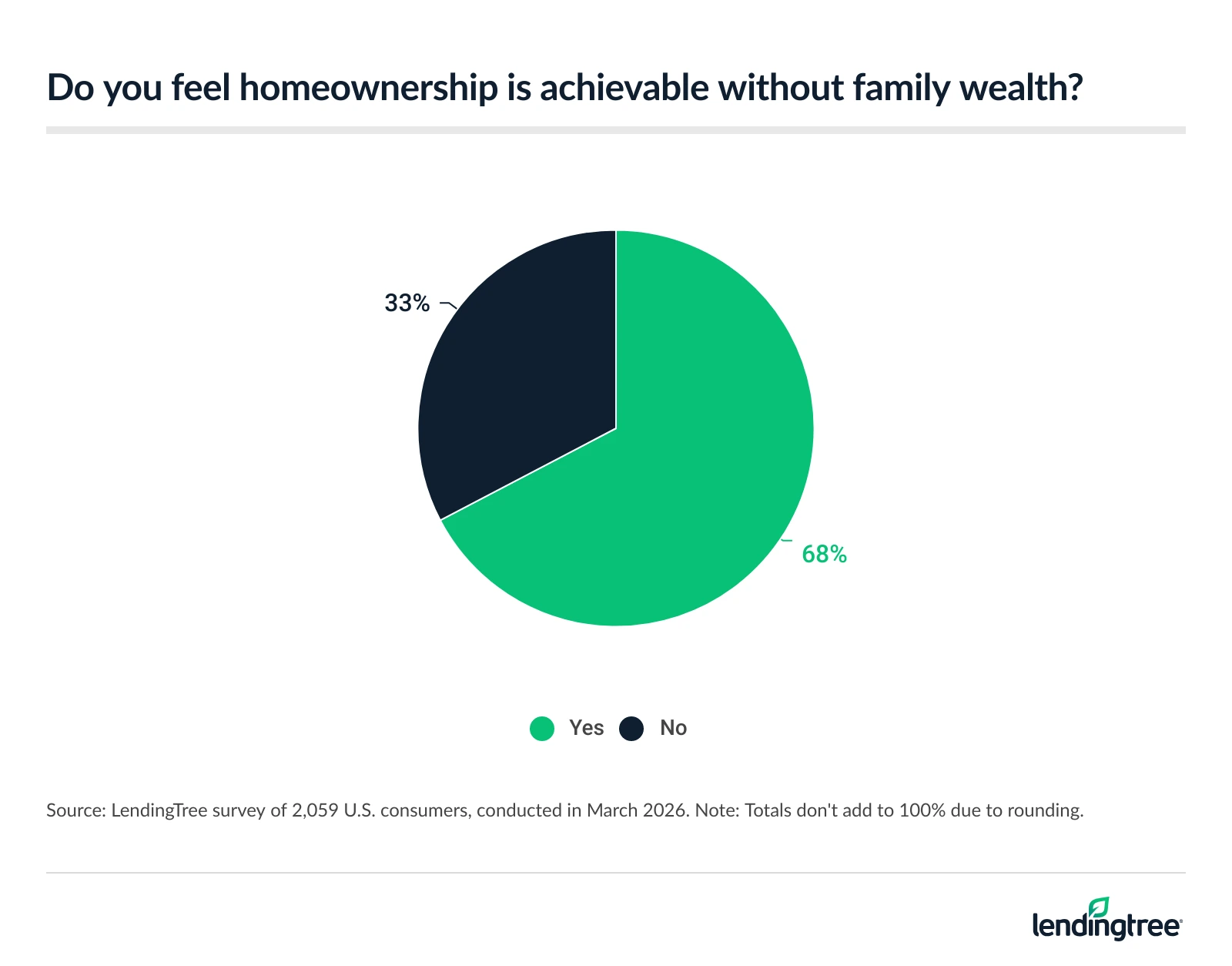

Still, Americans remain optimistic about homebuying, with more than two-thirds saying they feel homeownership is achievable without family wealth.

Here’s more of what we found in LendingTree’s 2026 Mortgage Down Payment Survey.

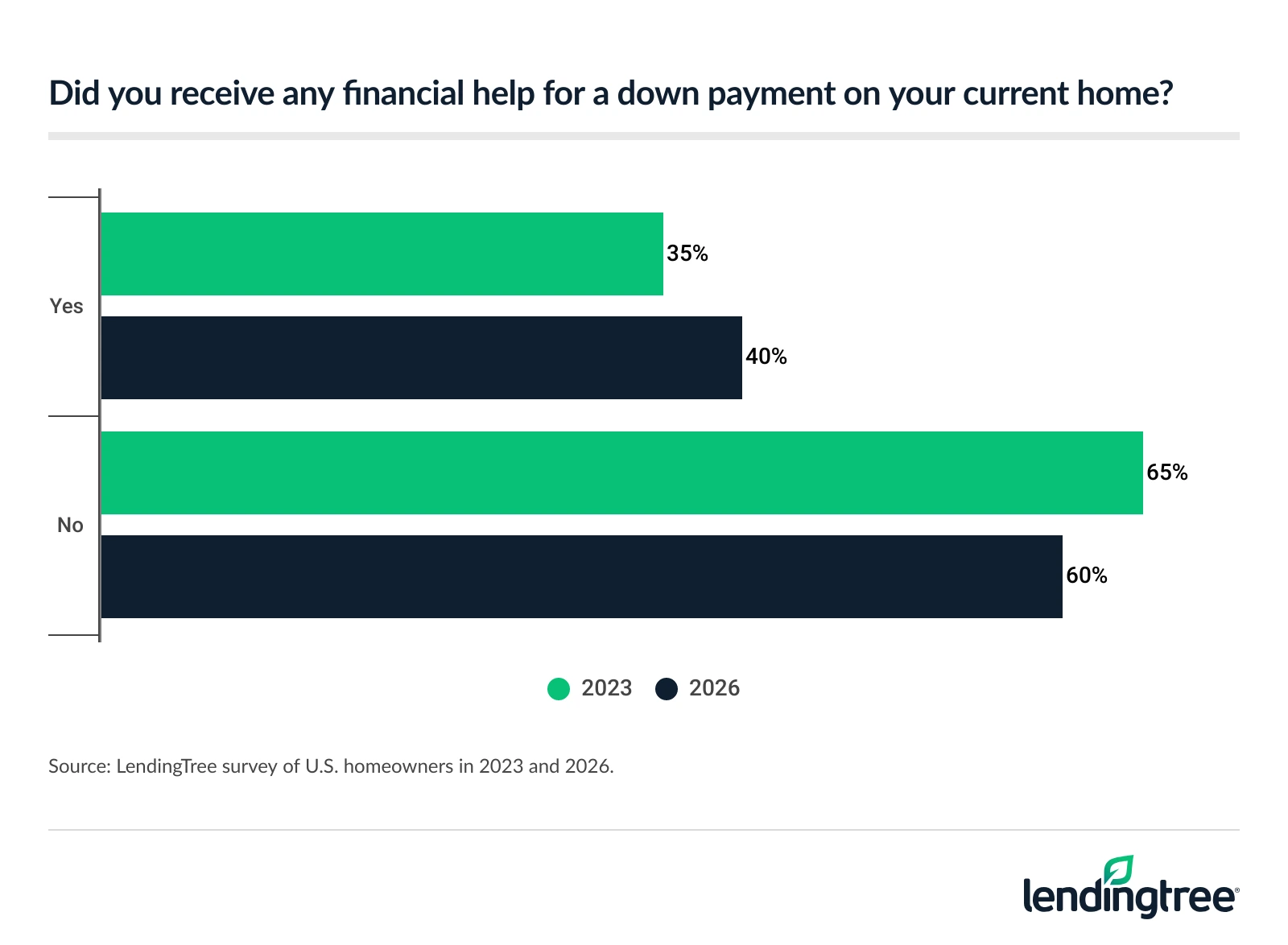

- Down payment help is widespread but highly generational. 40% of homeowners received financial help on their current home, up from 35% in 2023. This figure also rises sharply among Gen Zers (78%) and millennials (56%), compared with just 12% of baby boomers. Among recipients, 46% initially felt grateful, but 21% of Gen Zers felt embarrassed — more than twice the 9% of millennials.

- Family is the primary source of help — especially for younger buyers. 16% of homeowners say their parents helped with their down payment, increasing to 27% among Gen Zers. Additionally, support came from friends or other family (27% of Gen Zers and 19% of millennials) and inheritance or trust funds (24% of Gen Zers and 15% of millennials).

- More than 1 in 3 who received help say they couldn’t have bought their home without it. 35% of those who received down payment assistance on their current home say they couldn’t have bought it when they did without that support, and that figure rises to 44% among women. Assistance helped 43% qualify for a mortgage, 33% reduce their monthly payment and 31% afford a larger down payment.

- Still, the vast majority of Americans remain optimistic about their ability to afford a home. 68% of Americans say they feel homeownership is achievable without family wealth. High-income earners, baby boomers, parents and men are the most likely to agree. However, even 65% of millennials, Gen Xers and women and 61% of Gen Zers agree that you don’t need family riches to buy a house.

Down payment help is widespread but highly generational

The percentage of Americans who received help with the down payment on their current home is growing. In 2023, the rate stood at 35%. Today, it’s 40%.

A deeper dive shows a massive generational gap. We found that 78% of Gen Z (ages 18 to 29) and 56% of millennial (ages 30 to 45) homeowners got financial help with their current home’s down payment, but just 35% of Gen X (ages 46 to 61) and 12% of baby boomer (ages 62 to 80) homeowners did the same.

Perhaps surprisingly, the gap among income levels is far smaller. We found that 43% of homeowners earning less than $30,000 a year got help with their down payment, compared with 42% of those earning $100,000 or more. However, the sample size is significantly smaller in the lower-income bracket, indicating a greater potential margin of error.

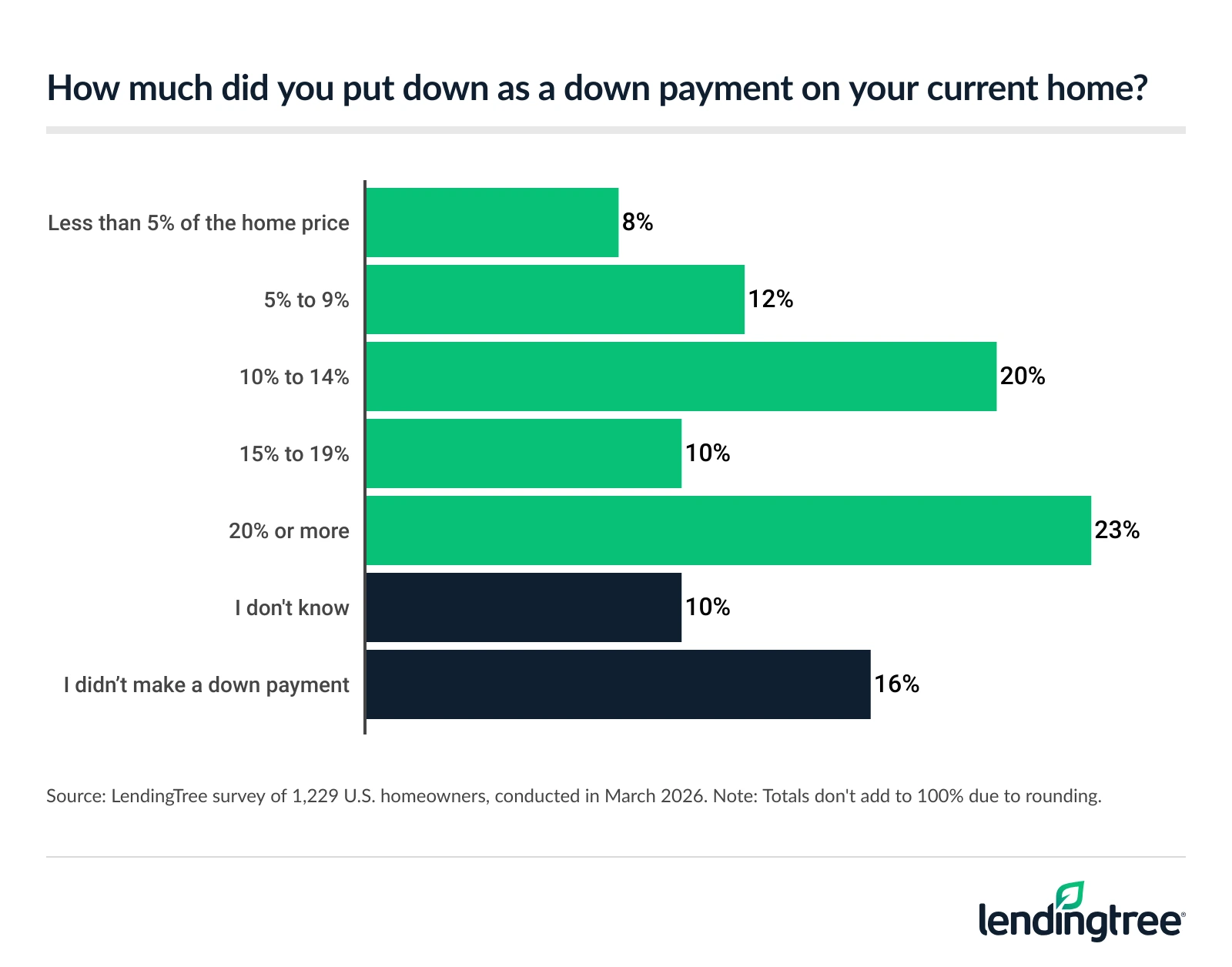

For most homeowners, even financial help isn’t enough to make a down payment of at least 20% — the magic number that allows homeowners to avoid private mortgage insurance (PMI) and dramatically reduce their monthly mortgage costs. Slightly more than half of homebuyers (51%) paid less than 20%, while just 23% paid 20% or more. (Another 10% didn’t know and 16% didn’t make a down payment.)

Family is the primary source of help, especially for younger buyers

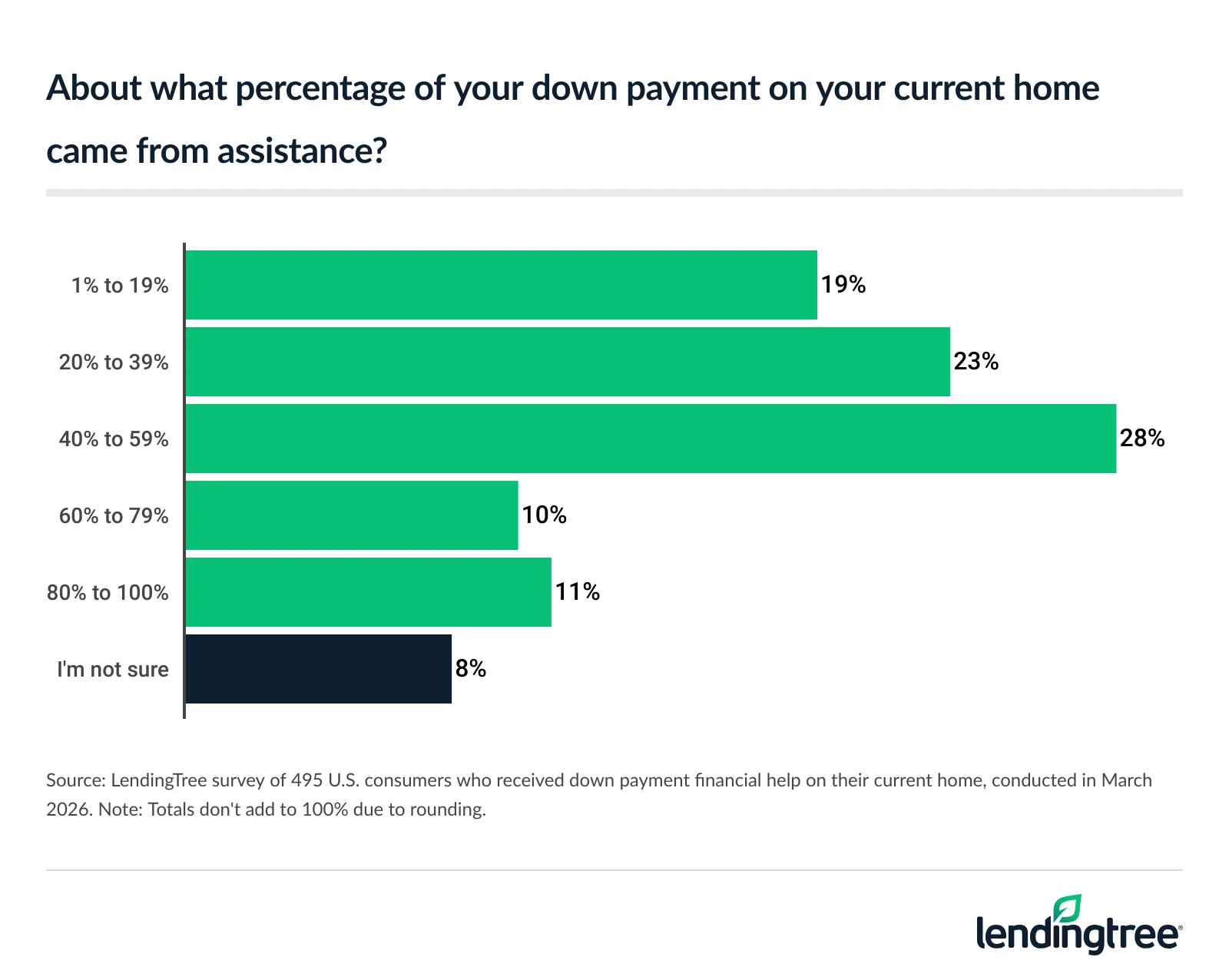

Half of the homeowners who received down payment assistance say that at least 40% of their down payment came from assistance. That includes 22% who say at least 60% of their down payment came from assistance and 11% who say at least 80% did.

The younger you are, the bigger that percentage is likely to be. Data shows that 59% of Gen Zers and 55% of millennials say help covered 40% or more of their down payment, versus just 39% of Gen Xers. (The sample size among baby boomers is too small to be statistically significant.) Also, men are much more likely than women (56% versus 42%) to say that at least 40% of their down payment came from assistance.

The most common source of assistance? The Bank of Mom and Dad. We found that 16% of homeowners say their parents helped with their down payment, which climbs to 27% among Gen Zers, 26% of parents of young kids and 24% of millennials.

That was hardly the only source, however. Others include:

- Friends or other family: 12% (27% of Gen Zers and 19% of millennials say this)

- An inheritance or trust fund: 11% (24% of Gen Zers and 15% of millennials say this)

- Seller concessions: 8%

- A down payment assistance program: 6%

- Employer assistance: 5%

Note: Respondents could select multiple options.

Our respondents report that the down payment assistance was far more likely to be a gift than a loan. Among those who received down payment help with their current home, 48% got it as a gift, 28% got it as a loan and 25% call it a combination of the two.

More than 1 in 3 who received help say they couldn’t have bought their home without it

For many who received down payment assistance on their current home, the extra help wasn’t just nice to have. It was essential.

More than a third (35%) of those who got down payment help on their current home say they couldn’t have bought it when they did without that assistance. Women are much more likely than men to say so (44% versus 29%).

Among those who got down payment assistance, 43% say it helped them qualify for a mortgage, 33% say it helped reduce their monthly payment, 31% say it helped them afford a larger down payment and 30% say it made it possible to purchase a more expensive home.

As impactful as the assistance was, recipients report having mixed emotions about it. Among recipients, 46% say their primary initial feeling was gratitude, while 19% felt relief and 14% felt supported. Still, 11% felt embarrassed, with 21% of Gen Zers saying so.

Still, the vast majority of Americans remain optimistic about their ability to afford a home

We found that nearly half of Americans (46%) expect to help a child or relative buy a home in the future. That number jumps to 75% among parents with young kids, as well as 63% of Gen Zers and 60% of millennials.

However, despite that and the rest of the often-gloomy data in this report, hope springs eternal for most Americans. Nearly 7 in 10 Americans (68%) think homeownership is achievable without family wealth.

Not surprisingly, high-income earners are among the most likely to agree, with 77% of those making $100,000 or more a year and 74% of those earning $50,000 to $99,999 saying so. And 77% of baby boomers, 74% of parents of older kids, 73% of parents of younger kids and 70% of men say so, too. Even 65% of millennials, Gen Xers and women and 61% of Gen Zers agree that you don’t need family riches to buy a house.

Even without family wealth, help is out there

Despite high interest rates and home prices, there’s reason for Americans to feel optimistic about their ability to afford a home without help from a wealthy relative. Perhaps the best reason is that there are many other types of help available to those who seek it, including some we touched on briefly earlier in the report.

- Negotiating with the seller: No, a seller isn’t going to give you down payment money. However, they may offer you a break on closing costs, freeing up some extra funds to be put toward a bigger down payment. Also, when you negotiate a lower overall price on the home, you’re changing the math when it comes to the down payment. You don’t have to be a math wizard to know that 20% of $400,000 is less than 20% of $450,000.

- Down payment assistance programs: These programs often target first-time homebuyers, helping them cover down payments and closing costs. They exist at the local, county, state and federal government levels but could also be available through nonprofits or your employer. You may have to meet certain requirements to qualify for assistance — minimum credit score, maximum income levels and so on — but they’re certainly worth looking into. Googling “down payment assistance programs near me” is a great place to start.

- Unconventional loans: Not everyone will qualify, but if you’re struggling to build a down payment and still want to purchase a home, these options are worth looking into. For example, U.S. Department of Agriculture (USDA) and Veterans Affairs (VA) loans don’t require a down payment but have strict guidelines as to who’ll qualify. Another government-backed loan — a Federal Housing Administration (FHA) loan — does require a minimum down payment of 3.5% but is also designed to cater to first-time homebuyers or borrowers with a low credit score and minimal savings.

Still, it’s important to have realistic expectations entering this process. We all love watching those house-hunter shows on TV and dreaming of the perfect “forever” home, but if you’re a first-time homebuyer, a dream home may not be in the cards for you right now.

The wiser move would be to crunch the numbers using a home affordability calculator to understand what you can afford right now — factoring in price, interest rates, down payments and the whole nine — and adjust your search accordingly. That way, the goal of homeownership can be accomplished, even if it means settling for a little less than your dream home in the process.

Methodology

LendingTree commissioned QuestionPro to conduct an online survey of 2,060 U.S. consumers ages 18 to 80 on March 17-23, 2026. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. Researchers reviewed all responses for quality control.

We defined generations as the following ages in 2026:

- Generation Z: 18 to 29

- Millennials: 30 to 45

- Generation X: 46 to 61

- Baby boomers: 62 to 80

View mortgage loan offers from up to 5 lenders in minutes