60 Month Loans Personal Loan Review

- APR

- Not specified

- Eligibility and access: 4/5

- Cost to borrow: 1.6/5

- Loan terms and options: 2.5/5

- Repayment support and tools: 1/5

If you don’t qualify for a personal loan from a traditional lender because of your credit, 60 Month Loans could be worth checking out. Here’s what to keep in mind before you apply:

- No hard credit check: 60 Month Loans offers personal loans with no credit check. Instead of pulling your credit report, this lender runs a soft credit inquiry and reviews your bank statements to determine your eligibility.

- Can still qualify if you have less-than-perfect credit: Although it pulls a soft credit report, 60 Month Loans mostly uses your bank statements to determine your eligibility. 60 Month Loans accepts fair and bad credit scores.

- Fast(ish) funding: It typically takes one business day for 60 Month Loans to review your application and bank statements. You could have your money in one to three business days after that.

- Very few tech features: 60 Month Loans doesn’t have a mobile app, and it only accepts automatic payments as a payment method. If you need help, you can’t reach out via chat. Instead, you need to call or email a representative.

- No collateral needed: Loans through 60 Month Loans are unsecured, so you won’t need to put up collateral.

- No prepayment penalties: Unlike some predatory bad credit lenders, 60 Month Loans allows you to pay off your loan early with no penalty.

- Best for bad credit loans (in the 16 states it does business in): It’s not uncommon to find triple-digit interest rates on no-credit-check loans. 60 Month Loans is an exception. Rates vary by state, but even so, they are much lower than you’d find with other no-credit-check lenders.

60 Month Loans pros and cons

60 Month Loans caters to borrowers who wouldn’t otherwise have access to a loan because of their credit scores. Depending on your credit profile, it could be the ideal company. Still, check out its pros and cons below before you commit:

Pros

- Can still qualify with bad credit

- No hard credit hit

- Easy application process

- Could help build credit since monthly payments are reported to the credit bureaus

Cons

- Can likely find lower rates if you have good credit

- Will keep a portion of your loan for itself as an origination fee (Up to 5.00%)

- No small-dollar loans and no big loans, either

- Only available in 16 states

- Can’t add a second person to your loan

If you’ve been turned down for a personal loan because of bad credit, 60 Month Loans could be worth checking out.

Rates are high compared to traditional lenders (and vary by state), but they still generally fall under the 36% threshold that many financial experts consider predatory lending. Plus, your payments are also reported to the credit bureaus, which could help to improve your credit score as you pay off your loan.

On the downside, 60 Month Loans only does business in 16 states, including:

- Alabama

- Arizona

- California

- Delaware

- Georgia

- Idaho

- Iowa

- Missouri

- Montana

- New Mexico

- North Dakota

- Oregon

- South Carolina

- South Dakota

- Utah

- Virgina

There’s also loan size to consider. If you’re looking for a large loan, 60 Month Loans might not meet your needs, as its maximum loan amount tops out at $10,000. At the same time, loans start at $2,600, so if you only need a small bit of money to get you through payday, this lender may not be the best fit.

60 Month Loans requirements

60 Month Loans’ eligibility requirements may be looser than many other lenders, but they’re also a bit vague. 60 Month Loans looks at two main two things when reviewing your application: Your FICO Score (based on a soft-credit check) and three months’ worth of bank statements.

It requires you to have a FICO score of at least 640, but it does not specify what it’s looking for when reviewing your bank statements. Note that you must also be a U.S. resident and at least 18 to borrow.

If 60 Month Loans’ loan options won’t work for your borrowing needs, be sure to shop around for a lender that can help you meet your financial goals and offer you the best-fitting interest rates, terms and amounts for your situation.

How to get a loan with 60 Month Loans

60 Month Loans only offers personal loans online — instead of visiting a brick-and-mortar office, you simply need to complete an application on its website. Follow the steps below to apply:

Fill out an application

To get funding from 60 Month Loans, first you’ll have to fill out an application. Here, you’ll provide basic information, like your name, contact information, Social Security number, driver’s license number (or that of another government ID), employment information and annual income.

Supply bank statements

When you apply, you will also need to provide 60 Month Loans with three months’ worth of bank statements. You can do this by emailing PDF copies of your statements to the lender or through an electronic bank verification process.

Wait for the underwriter to call

After you submit your application and bank statements, an underwriter will call you within one business day to ask additional questions.

Sign your loan documents

If the underwriter approves you, you’ll sign your loan documents electronically. Generally, 60 Month Loans will deposit your funds directly into your bank account as soon as the next business day. It could take up to three business days before you have access to your loan, depending on if your bank puts a hold on the funds.

Begin repayment

About 30 days after you receive your loan, you’ll enter repayment. Your payments will be automatically deducted from your bank account on your due dates (which are shown in your loan agreement).

How 60 Month Loans compares to other personal loan companies

Even if you believe 60 Month Loans aligns with what you want in a personal loan, it never hurts to shop around and compare other lenders. Here’s how 60 Month Loans stacks up against similar personal loan lenders:

| 60 Month Loans | Upstart | Happy Money | |

|---|---|---|---|

| LendingTree’s rating | 2.4/5 | 4.4/5 | 3.7/5 |

| Minimum credit score | 640 | None | 620 |

| APRs | Not specified | 6.20% to 35.99% | 8.95% to 35.99% |

| Loan amounts | $2,600 – $10,000 | $1,000 – $75,000 | $5,000 – $50,000 |

| Repayment terms | 12 to 60 months | 36 or 60 months | 24 to 60 months |

| Origination fee | Up to 5.00% | Varies | 2.00% – 12.00% |

| Funding timeline | May receive funds as soon as the next business day after loan approval | May receive funds as soon as one business day after loan approval | May receive funds as soon as three to six business days after loan approval |

| Bottom line | 60 Month Loans has easy eligibility requirements, but is only available in 16 states and only makes sense if you have bad credit. | Upstart offers loans to those with bad or no credit history, but it is also competitive for borrowers with excellent credit. However, Upstart only offers two repayment terms (36 or 60 months). | Happy Money could be helpful if you’re looking for credit card refinancing, but this is typically the only kind of loan this lender offers. |

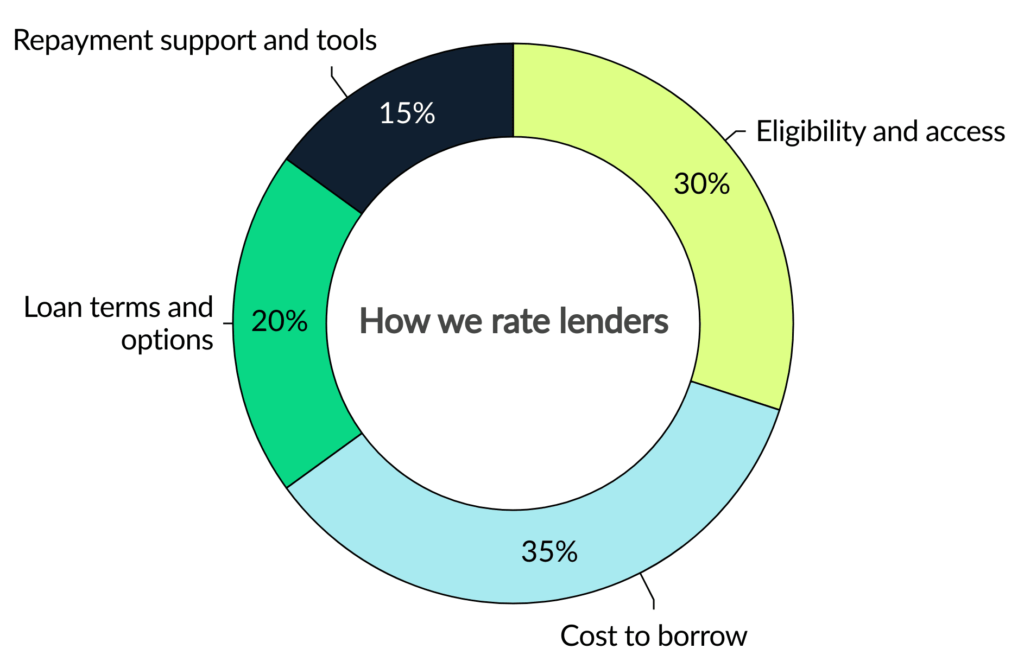

How we rated 60 Month Loans

We evaluate personal loan lenders on more than just interest rates. Our goal is to show how accessible, affordable, transparent and supportive each lender really is.

Our categories

Every lender is scored out of 5 stars, with 5 stars being the highest rating. LendingTree loan experts determine this score using dozens of underlying data points across four weighted categories covering the full borrowing journey.

We assess how easy it is for people to qualify and apply. This includes state availability, soft-credit prequalification, membership requirements, funding speed and whether borrowers with less-than-excellent credit can get a loan.

We evaluate how affordable the loans are based on minimum and maximum APRs, loan fees and rate discounts. Lenders with unclear or potentially predatory costs receive lower scores.

We consider repayment term flexibility, loan amount ranges and whether options like secured loans, joint loans or direct-to-creditor payments are offered — plus whether the lender clearly communicates these options.

We evaluate borrower experience after funding: customer service access, hardship or forbearance programs, payment flexibility and digital tools like mobile apps or credit monitoring.

Our process

We gather data directly from lenders through their websites, disclosures and direct communication with company representatives. Our editorial team verifies and updates information regularly. We value transparency and award less favorable scores when lenders obscure or omit details.

In some cases, our editors may apply a small adjustment (no more than 4% of the overall score) to account for factors not captured by the methodology. This could include J.D. Power customer satisfaction surveys, recent regulatory actions or features that stand out in ways our rubric doesn’t measure directly.

Our editorial team applies the same scoring model and standards to every lender. Lenders cannot pay to influence our ratings.

Frequently asked questions

Yes, 60 Month Loans is a legitimate lender that specializes in no-credit-check loans for people who have fair or bad credit. But just because 60 Month Loans is legitimate doesn’t mean it’s the best one for you — especially if you meet the eligibility requirements for a more traditional lender. Be sure to prequalify for a few personal loans and compare before signing on the dotted line.

Yes, 60 Month Loans is a direct lender. This means the company itself lends you the money itself, rather than sourcing its funds from a partnering bank or other financial institution.

Every lender sets its own personal loan requirements. For instance, some will only lend to people who have excellent credit or bring in a certain annual income, while others will consider bad-credit borrowers as long as they agree to a higher-than-average APR.

In general, you might have a hard time getting a traditional personal loan if your credit score is below 640, or if you have a poor payment history, delinquent debt or insufficient income.

Get personal loan offers from up to 5 lenders in minutes

Recommended Articles