Jumbo vs. Conventional Loans: Which is better for you?

What separates jumbo loans and conventional, conforming loans is simply how much you’re borrowing. Conventional loans let you borrow up to the conforming loan limit, which is $832,750 for a single-family home in most of the U.S. However, if you need to borrow more money, you’ll have to use a jumbo loan.

You can access both conventional and jumbo loans through private lenders, such as banks, or through loan programs backed by government agencies. However, each option comes with its own borrower requirements. We’ll cover how to decide which is right for you when it comes to jumbo versus conventional loans.

- Jumbo loans exist to help borrowers purchase luxury homes or homes in unusually expensive areas.

- Conforming conventional loans come with loan limits that help prevent homebuyers from biting off more than they can chew and potentially losing their homes to foreclosure.

- Jumbo loans usually make more sense only when you need a loan amount that exceeds conforming limits or you can’t qualify for a conforming option.

Jumbo vs. conventional loan: What’s the difference?

A jumbo loan is the largest personal, residential mortgage you can get. A conforming conventional loan is smaller, but comes with built-in guardrails that can help you avoid risk.

What defines whether a loan is jumbo or conforming is simply its amount. The 2026 conforming loan limit for a single-family home in most of the U.S. is $832,750, but rises to $1,249,125 in some high-cost areas. If you need more money, you’ll need a jumbo loan.

| Jumbo loans | vs. | Conventional loans (conforming) |

|---|---|---|

| → Is the largest residential mortgage you can get → Exceeds conforming loan limits → Can be issued by a private financial institution (conventional) or through a government-backed loan program (nonconventional) → Can offer more flexibility in how you qualify, but that means you’ll need to be more mindful of the risks and long-term costs. | → Is the most popular kind of mortgage loan → Must stay within the conforming loan limits → Issued by a private financial institution, like a bank. → Limit lender discretion for “stretch” approvals and come with more safeguards around affordability. |

Looking for more details? Jump down to our section on how lenders define conforming vs. conventional loans.

Is a jumbo loan actually more expensive than a conventional loan?

Jumbo loans usually come with higher mortgage rates and higher upfront costs — typically a 10% to 20% down payment and fees that scale up with the loan amount. This can make them both tough to get into and more expensive overall compared to conforming conventional loans.

Jumbo vs conventional loan rates

Jumbo rates are currently slightly higher than conforming conventional rates. But depending on the housing market, that gap can narrow. Rates for jumbo loans can even undercut conforming (conventional) rates, making a jumbo loan the more affordable choice in some situations.

The exact rate you’ll qualify for depends on your credit profile, loan amount, DTI ratio and more.

To assess the total costs of a given loan option, make sure to look at:

- Both its interest rate and APR

- How much total interest you’ll pay

- Loan fees

- Whether you’re required to pay for mortgage insurance

The best way to ensure you’re getting the best rate possible is through a comparison shop. An online comparison site like LendingTree lets you enter all of your information one time while sourcing loan offers from multiple lenders.

Is a jumbo loan harder to qualify for than a conventional loan?

It’s usually much harder to qualify for a jumbo loan than a conforming conventional loan. If you’re a military borrower taking out a U.S. Department of Veterans Affairs (VA) loan, you’ll get a bit of a break, but a jumbo loan will otherwise take significant amounts of cash, a high income and solid credit.

Jumbo vs. conventional loan minimum requirements

| Jumbo (conventional) | Jumbo (VA) | Conventional (conforming) |

|

|---|---|---|---|

| Credit score | 700 | No minimum set by the VA, but many lenders require at least 620 | Traditionally 620

Fannie Mae and Freddie Mac no longer use a strict 620 credit score minimum Instead, they’ll focus on overall creditworthiness rather than a single credit score threshold.

|

| Down payment | 20% | 0% (for those with full entitlement) | 3% |

| Debt-to-income (DTI) ratio | 45% | 41% | 45% |

| Cash reserves | Six to 24 months’ worth of mortgage payments | Only in special cases involving multiunit rental properties | Two to six months’ worth of mortgage payments. Typically required if your:

|

| Maximum loan amount | No specific limit (varies by lender) | No limit for borrowers with full entitlement; FHFA conforming loan limits with partial entitlement | $832,750 to $1,249,125 depending on location |

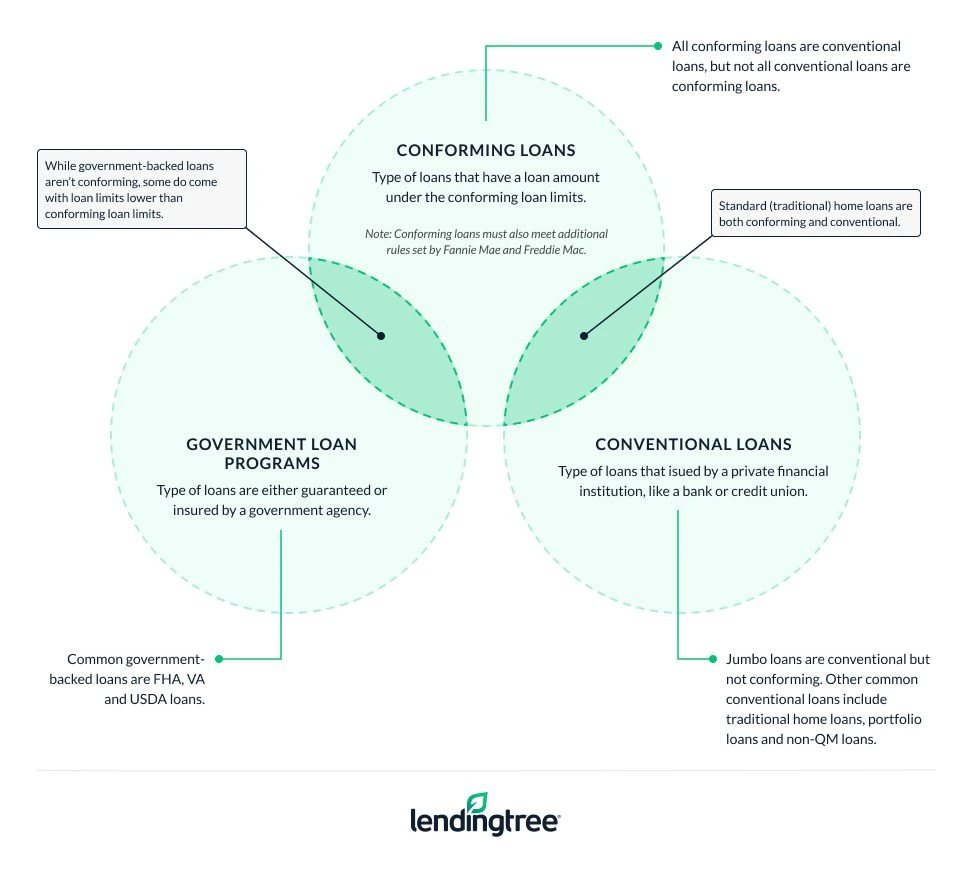

Understanding how lenders define conforming vs. conventional loans

There’s a common saying that can come in handy when navigating loan terminology: All conforming loans are conventional loans, but not all conventional loans are conforming loans.

When people talk about conventional loans, they typically mean conforming conventional loans. But jumbo loans can also be conventional loans — is your head spinning yet?

Here’s the problem: There are two ways of classifying mortgage loans. You can go by loan program (conventional vs government backed) or by loan amount (conforming versus nonconforming). If you remember to keep those approaches to loans separate in your mind, the many labels used to describe loans will be far less confusing.

Jumbo loans can be conventional (not insured or backed by a government agency) or nonconventional (part of a government-backed loan program). However, they’re always nonconforming since they exceed the conforming loan limits.

To see exactly which loan type you’ll need, check the conforming limits in your county.

Loan programs: Conventional loans vs. government-backed

| Conventional loans | vs. | Government-backed loans |

|---|---|---|

| → Not part of a government-backed loan program. → Typically issued by a bank or credit union, though they could also be issued by a private lender → Are typically conforming, which means they meet Fannie Mae and Freddie Mac’s rules, including conforming loan limits — but if they don’t, they’re classified as nonconforming loans. → Examples include: | → Backed by government agencies → Can be conforming or nonconforming → Will need to stay within any loan limits set by the government agency backing the loan → Examples include: |

But, when it comes to jumbo options:

- All conventional jumbo loans are nonconforming, which usually means they’re portfolio loans or non-qualified (QM) loans (or both). These are the loans that often offer greater flexibility in qualification requirements, since they don’t have to abide by either conforming or qualified mortgage rules.

- Only one government-backed jumbo loan program exists: The VA’s, which allows eligible military borrowers with full entitlement to borrow as much as they need with no limit.

No, Fannie Mae and Freddie Mac are government-sponsored enterprises (GSEs), not government agencies. They were created by Congress, but operate as corporations.

It’s important not to think of Fannie and Freddie as government agencies because the loans they back aren’t considered government-backed loans. Learn to associate Fannie and Freddie with conventional lending and you’ll be good to go.

How to decide between jumbo vs conventional options

A jumbo loan may be best if…

- You need a loan amount that exceeds conforming loan limits

- You have a strong income, significant assets or substantial cash reserves

- You’re confident that you can comfortably take on the loan, but have a unique financial situation that means you can’t qualify for a conventional loan.

A conforming conventional loan may be best if…

- Your budgeted loan amount falls within conforming limits

- You want lower upfront costs

- You don’t want to take on the potential risk that comes with a non-QM loan

View mortgage loan offers from up to 5 lenders in minutes

Recommended Articles