Dads Are the No. 1 Source of Financial Advice, Survey Reveals

Dad’s had your back since the day you were born. You know you can always count on him — he’s the first one you call when you need help fixing something around the house or when you need a buddy to go to the movies with. As it turns out, he’s probably also your first stop when you’re looking for financial advice.

We commissioned Qualtrics to survey over 1,000 Americans about their dad’s role as a financial model. Our findings show that 43% of those we surveyed said they go to Dad for financial advice, and 56% said their dad helped them develop good money habits growing up.

Millennials in particular tend to lean on dad for financial advice regarding many areas of their lives, from buying a car to saving for retirement and getting a credit card. It turns out dads are MVPs when it comes to guiding their children toward a healthy financial future.

Key findings

- Our survey found that 43% of survey respondents go to their dad when they need financial advice — and 23% would ask their dad about money before consulting a financial advisor (14%).

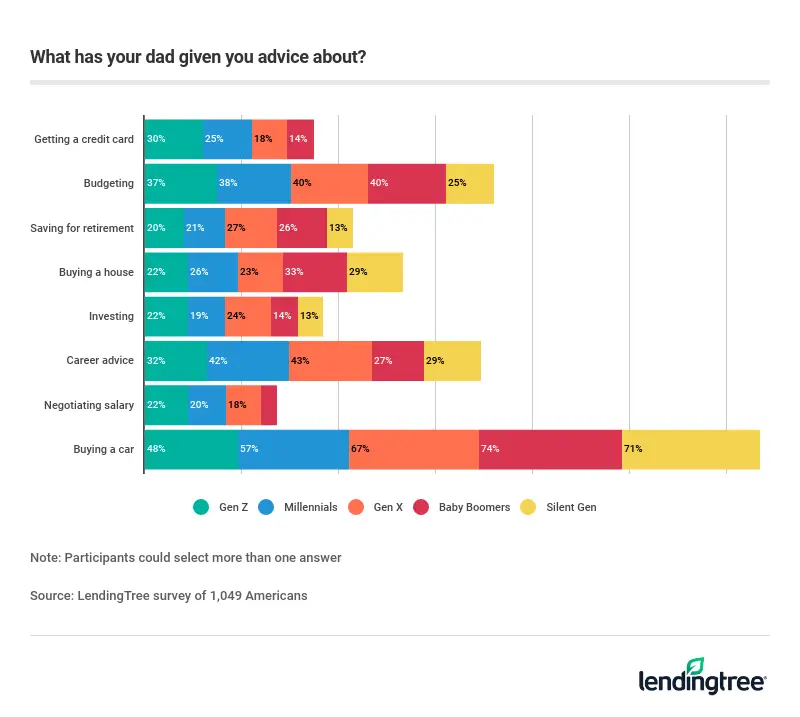

- Buying a car (64%), budgeting (38%) and career advice (37%) are the most common ways dads have helped their children navigate their personal finances. Other ways fathers have advised their children on important money-related subjects include tips on buying a house (27%), retirement savings (23%), getting a credit card (20%), investing (about 19%) and negotiating a salary (almost 16%).

- About half (49%) of respondents consider their father to be their financial role model, and about 56% say their dad helped them develop good money habits growing up.

- Millennials are more likely than any other age group to value their father’s financial advice. Specifically, about 55% of millennials say their dad is their financial role model, compared to the average of 49%. Additionally, 54% of millennials ask their dad for help when they need financial advice, while the average across all age groups is 43%.

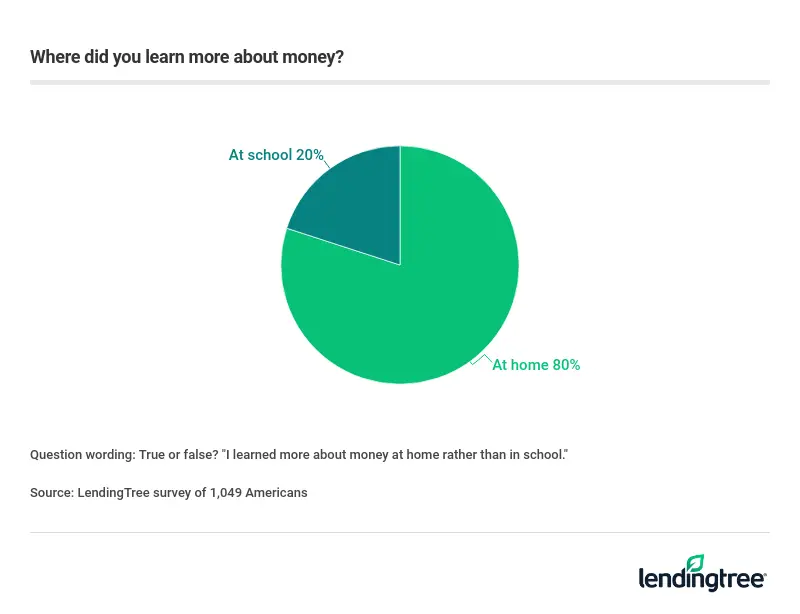

- 80% of Americans say they learned more about personal finance at home than at school, and the same number wish schools taught students more about money.

- More than two-thirds (68%) will use strategies their father taught them when teaching their own children about money.

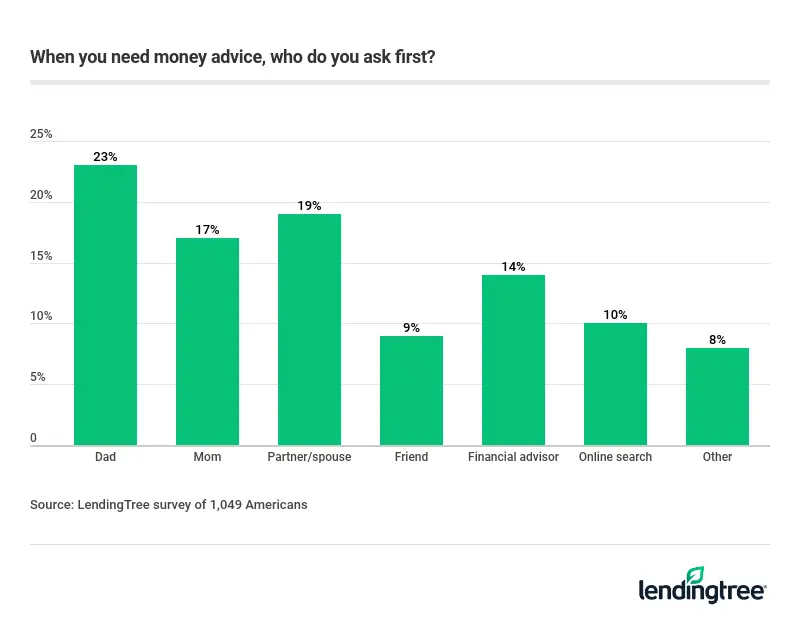

Nearly 1 in 4 Americans go to Dad first for money advice

Money can be a difficult topic to broach for Americans. That may be why about 23% of our survey respondents said they turn to Dad first for financial advice. Even amongst trusted friends, the majority of people aren’t comfortable discussing their finances with non-family members. According to a 2018 report from Acorns, an investment app, 58% of people would rather tell their friends how much they weigh rather than how much money they have saved. And a poll from credit repair service Lexington Law found that 76% of Americans aren’t comfortable asking friends about their salaries. An unwillingness to speak about money outside the home may be why so many people consult their fathers first when they need financial advice — Dad might be one of the only people they’re comfortable having such conversations with.

Of course, Dad isn’t the only person Americans are turning to for help with money. Some survey respondents said they first talk to a partner or spouse (19%) or Mom (17%) for help with money topics. But only 9% said they turn to friends first for financial advice.

Only 14 percent of those we surveyed said they’d turn to a financial advisor for help first. Yet, a 2017 Scottrade study revealed that 61 percent of U.S. investors wish they had access to reliable guidance. But of those who did, trust seems to be the primary issue affecting the relationship. Millennials and Gen Xers were found to be more likely than older generations to express hesitation and cynicism regarding choices their advisors made on their behalf. Our findings indicate that people prefer to consult loved ones they trust, and have a relationship with, over a professional.

Most Americans wish schools taught them about personal finance

Parents are a popular go-to for financial advice and our schools might be to blame for that. We found that 80 percent of those surveyed learned more about money at home than they did at school. This may be problematic, as even the best of parents may not make for the best financial teachers. And family-only financial education can potentially lead to poor financial habits being passed on to children.

The financial habits and planning that worked well for a parent may not serve their child’s money needs, particularly as younger generations are facing crushing amounts of student debt. The average student debt in the United States is $32,731, according to ValuePenguin, which is owned by LendingTree. Younger generations are facing debt that was less conceivable to their parents’ generation. Since 2004 alone, tuition and total student loan debt cost has grown around 302%.

Homegrown financial education is a start but not an ideal end goal for many. The idea of financial education in schools is popular — in fact, 80% of survey respondents wished they’d learned more about personal finance at school. Perhaps the millennials we surveyed particularly desire a more formal financial education because of their debt. They have more debt than those in the Baby Boomer and Gen X generations, according to a LendingTree study that examined debt changes by generation over a three-year period.

How dads’ financial advice changes by generation

If you’re ready to hit the open road, don’t leave dad behind. Buying a car is the No. 1 time all generations turn to dad for advice.

Gen Xers generally have the biggest auto loan burden. That may be why they turn to dad more than the baby boomer generation does when it’s time to buy a car. Baby boomers generally have the second-biggest auto loans across all applicable generations. However, large auto loans are not necessarily a sign of bad financial health: as baby boomers are further along in their careers than younger generations, they may be able to afford to take out larger auto loans for more expensive cars or for family members.

The second-most popular issue to hash out with Dad across all generations is budgeting. As budgeting is a fundamental financial building block, and something you can struggle with during any stage of life, the multi-generational appeal for Dad’s advice is obvious. Budgeting is also a lower-level financial topic that can be learned easier through day-to-day experiences than say investing or buying a home. Both are more complicated financial topics than budgeting.

Meanwhile, 42 percent of Millennials ask their fathers for career advice, compared to 27 percent of Baby Boomers and 32 percent of Gen Zers. Considering the student loan debt crisis is a recent development, it makes sense that millennials’ parents didn’t need to turn to Dad as often for career advice; they were raised in a different economy and job market.

The least-popular problems to seek a father’s council on included negotiating salary, followed by getting a credit card and investment advice.

If your dad was a part of the Silent Generation, you’re in luck — chances are he’s a wealth of financial knowledge. At least if he’s helping contribute to the Silent Generation having the best overall credit scores across all generations. The Silent Generation has had more time to learn healthy financial habits that contribute to their higher credit scores. Plus, time has organically increased their credit scores due to age and more credit building life experiences like buying property or taking out loans; these are experiences that younger generations may not have had yet.

Tackling those big expenses you discussed with Dad

Your dad wants to be there for you for all of your biggest moments — that’s kinda his favorite job. But life’s milestones can come with big costs. Think about the costs associated with going after that college degree or buying your first home or car, for example. But different financial products may help you afford these costs.

Personal loans, also known as a signature loan, are an increasingly popular form of unsecured debt that you can use to pay for almost any expense that you can’t pay for out of pocket. (This differs from secured loans, which are backed by collateral, like your car or house.) Personal loans can also be used to consolidate or refinance debt, so you can repay it at a lower interest rate or with a more favorable term length or fee structure.

But personal loan lenders rely more heavily on your credit score and financial history when determining whether or not to approve you for funds. Your income and debt can also affect your ability to obtain a loan or any interest rates offered to you. That means borrowers with lower credit scores may not qualify — or may only qualify for high rates.

The benefits of a personal loan

There are many benefits to taking out a personal loan, the following are a few to consider.

- Fixed interest rates: These rates won’t change over the life of your personal loan, which makes budgeting for repayment easier.

- Fixed monthly payments: Unlike a credit card, where balances can run up, a personal loan will generally have fixed monthly payments. This means that borrowers will know exactly how long it will take to pay off their loan amount.

- Your credit score may improve: That’s right, the major credit score issuers like FICO reward borrowers who carry a mixture of credit types. You can possibly improve your score by adding a new loan to your report.

- No repossession risk: Because personal loans are generally unsecured, you don’t have to risk collateral to obtain one.

Obtaining a personal loan

The process of obtaining a personal loan isn’t as tricky as it sounds. After gathering all of your financial information and your credit score, you’ll apply to get pre-qualified for a loan. If you accept the quote you’re given during the pre-qualification process, you can move forward with your application or choose to shop around for a better loan deal. After you compare your offers and accept one, you’ll receive your money. You can learn more in our guide about the personal loan application process.

Alternatives to a personal loan

- If a personal loan is not a viable financial product for you, you have other financial options available to you, if there’s a need.

- A credit card can be one option to consider for fast cash flow, especially if you can repay the balance in full by the due date. If you carry a balance, be aware that you can be hit with high interest charges until you pay off your debt. Some credit cards will offer a promotional 0% APR for a specified amount of time that can help you avoid mounting interest fees.

- A salary advance is another option to consider. Some companies have payroll advance programs designed to help employees cover a financial emergency. It’s worth asking your HR department about their policies for paycheck advancement if you find yourself needing to cover an unexpected expense quickly.

- All that said, you should avoid taking out unnecessary debt. Although a healthy payment history is important to building your credit, you shouldn’t take out debt without a clear plan for how you’ll use the funds and repay them. Further, don’t feel rushed to hit life milestones, like buying a car or your first home — do what makes the most sense for your financial situation and needs.

Methodology

LendingTree commissioned Qualtrics to conduct an online survey of 1,049 Americans, with the sample base proportioned to represent the general population. The survey was fielded May 13-15, 2019.

Get personal loan offers from up to 5 lenders in minutes

Recommended Articles

Back-to-School Shopping Defies Inflation: Families Spend Nearly the Same as Before the Pandemic

Delaware, D.C. and Texas Have the Highest Business Bankruptcy Filing Rates in the US

Best Health Insurance Companies in Georgia in 2026

Homebuyer Down Payments by Generation in the 50 Largest US Metros

Best Merchant Cash Advances in July 2026

How To Refinance a Car Loan With Bad Credit

Best Bad Credit Auto Refinance Companies in July 2026

Home Insurance Takes Up Nearly a Fifth of Monthly Housing Costs in Some States

America’s Tourism-Dependent Metros Aren’t Always the Obvious Ones

Personal Bankruptcy Filings Have Risen 47% Since 2022, Marking a Third Straight Annual Increase