Personal Line of Credit Rates From 9% in August 2026

A flexible way to borrow for ongoing expenses, often with lower rates than credit cards

Advertising Disclosures

Loading Disclosures…

| Lender | APR | Term | Amount | See Results |

|---|---|---|---|---|

|

|

9.00% to 10.50% (with autopay) | 12 to 60 months |

$5k – $100k |

|

|

|

12.50% to 18.00% | Up to 144 months | Up to $10,000 | |

|

|

12.50% to 17.00% (with discounts) | Not specified |

$500 – $25k |

|

|

|

Up to 35.99% | 1 to 12 months |

$1k – $8k |

|

|

|

10.75% to 20.75% | 12 to 84 months |

$1k – $25k |

Personal lines of credit at a glance

- APR (with autopay)

- 9.00% to 10.50%

Availability: 12 states

How it works: 5-year draw period; 10-year repayment period

- Low rates

- Offers up to $100,000 — could be ideal for large ongoing projects, like a home remodel

- Hardship program available if you’re having trouble keeping up with payments

- Available in only 12 states (see “How to qualify” below)

- Although the first year is waived, annual fee is high

- Can’t apply online

- Has a 5-year draw period, which means you can borrow for only five years

Fifth Third offers personal lines of credit (PLOCs) with some of the lowest annual percentage rates (APRs) around. It charges an annual fee, but this expense might be worth it depending on the rate you qualify for.

However, Fifth Third personal lines of credit aren’t available for most people — that’s because it does business in only 12 states. And if you do live in an eligible state, you’ll have to apply over the phone or at a branch.

Fifth Third Bank is available only if you live in Ohio (home to its headquarters), Alabama, Florida, Georgia, Illinois, Indiana, Kentucky, Michigan, North Carolina, South Carolina, Tennessee or West Virginia. If you do live in one of these states, you can call Fifth Third at 866-671-5353 or stop into a branch to apply.

- APR

- 12.50% to 18.00%

Availability: Nationwide

How it works: Continuous draw period

- Available in all 50 states

- Can receive advice on how to reach your financial goals through free, one-on-one consultations

- Continuous draw period, so borrowing has no time limit

- Have to become a credit union member first (it’s easy to do online)

- May not work for larger projects (can borrow only Up to $10,000)

On-time payments on a small personal line of credit can help you boost your credit score — First Tech’s lower minimum PLOC amount could be perfect for this. Smaller lines of credit are generally easier to qualify for, and having less available credit can also help you avoid taking on too much debt.

But since First Tech is a credit union, you’ll need to become a member to borrow. To meet First Tech’s requirements, most people will need a membership to the Oregon Computer History Museum or the Financial Fitness Association. First Tech could help you do this, and may even pay for your first year of dues.

You can apply before you become a First Tech member, but you’ll have to join the credit union to accept your PLOC. To qualify, you need to meet one of the requirements below:

- Be related to or live with a current First Tech member

- Work for a company that partners with First Tech

- Work for the state of Oregon

- Live or work in Lane County, Oregon

- Become a member of the Computer History Museum or Financial Fitness Association (First Tech may pay your dues for the first year)

- APR (with discounts)

- 12.50% to 17.00%

Availability: 15 states

How it works: Continuous draw period

- Two rate discounts available (one for established members and one for using autopay with a KeyBank checking account)

- Two financial hardship options to help you get back on track

- Can get help from a person (not AI) via live chat seven days a week

- Available in only 15 states

- Established customers get the best benefits

- Can’t apply online — you’ll have to go to a branch

Put KeyBank on your radar for your PLOC, especially if you’re an established member.

If you have a checking account with at least five transactions in a calendar month, or more than one eligible KeyBank account, you could get a rate discount of 0.75%. KeyBank offers another 0.25% discount for setting up autopay with your KeyBank checking account.

Unfortunately, KeyBank doesn’t issue cards along with its PLOCs; you can only move money online or access it by check or in a branch. Not having a card could make in-person purchases a pain.

You could qualify for a PLOC with lower credit, but KeyBank only gives its best rates to people with 780-plus credit scores. You’ll also need to be at least 18 years old and have a Social Security number.

KeyBank is available only in Alaska, Colorado, Connecticut, Idaho, Indiana, Maine, Massachusetts, Michigan, New York, Ohio, Oregon, Pennsylvania, Utah, Vermont and Washington. Also, you’ll have to apply in person — use KeyBank’s branch locator tool to find one close to you.

- APR

- Up to 35.99%

Availability: 41 states and Washington, D.C.

How it works: Continuous draw period

- May not need perfect credit to qualify

- APR is fixed (most PLOCs are variable), so you won’t have to worry about rates going up

- No fees whatsoever

- High APR makes sense only if you can’t qualify somewhere else

- Due dates generally line up with your payday, so you might have to pay more than once a month

- Can access funds only by transferring them online

- Doesn’t transfer funds on weekends

If you aren’t exactly sure how much money you need to borrow, a PLOC from Pathward could be a good alternative to a bad credit loan. Traditionally, you’ll need at least good credit (670 or higher) to get a personal line of credit — Pathward may be willing to work with lower scores.

Pathward is unique in a few ways. Your due dates usually align with your payday, though that can mean juggling multiple monthly payments if you get paid every two weeks.

Pathward PLOCs have fixed rates, whereas most PLOCs have variable rates. A fixed rate means your rate won’t change; however, a flat 35.99% APR is very high if you have excellent credit.

To get a Pathward PLOC, you’ll need to be the legal age in your state and have a personal checking account, phone number and email address.

Pathward isn’t available in Colorado, Maine, Massachusetts, Nebraska, New Hampshire, New York, Oregon, Rhode Island or West Virginia.

- APR

- 10.75% to 20.75%

Availability: May not be available in all states

How it works: Continuous

- Can access your line of credit with a card (many lenders allow only online transfers)

- Checking rates won’t affect your credit score

- Clear eligibility requirements

- Must be a U.S. Bank customer to qualify

- No autopay discounts

- Charges a 4% fee if you access funds with an ATM

U.S. Bank makes it easy to access your line of credit once you’re a member. Only U.S. Bank members are eligible for PLOCs, but you could open a checking account and then apply.

After you’re a member and approved, you can use a card to access your line of credit. In contrast, many lenders just send out checks — if that (some will allow only online transfers).

Still, using your card could be expensive. If you use it to draw money from an ATM, U.S. Bank charges 4% of the total amount ($10 minimum). This rate is similar to that of a credit card cash advance.

It’s hard to get U.S. Bank’s lowest rates — you’ll need to have a credit score of at least 800. To qualify in general, though, U.S. Bank requires only a 680 score. You’re also required to have a current U.S. Bank checking account.

Why use LendingTree?

$3.2B in funding

In 2025 alone, LendingTree helped find $3.2 billion in funding for people seeking personal loans.

$1,659 in savings

LendingTree users save $1,659 on average just by shopping and comparing rates.

360,000+ loans

In 2025, LendingTree helped find funding for over 360,000 personal loans.

When banks compete, you win

You’d shop around for flights. Why not your loan? LendingTree makes it easy. Fill out one form and get lenders from the country’s largest network to compete for your business.

Tell us what you need

Take two minutes to tell us who you are and how much money you need. It’s free, simple and secure.

Shop your offers

LendingTree users get 11 personal loan offers on average. Compare your offers side by side to get the best deal.

Get your money

Pick a lender and sign your loan paperwork. You could see money in your account in as soon as 24 hours.

What is a personal line of credit?

A personal line of credit (PLOC) is a way to borrow money over and over again, like with a credit card, but with different rates and rules than a credit card. Here’s what you need to know:

- Borrow again and again up to your borrowing limit during your draw period, then pay it back over your repayment period

- Pay interest only on what you borrow, but interest starts adding up as soon as you withdraw money

- Can be harder to find than credit cards and personal loans since fewer lenders offer personal lines of credit

- Typically have lower rates than credit cards, especially for people with good credit

- Often harder to use than credit cards since you typically need to transfer money to your bank account rather than use a physical card to pay vendors directly

- Great for ongoing expenses or projects when you’re not sure how much money you’ll need

Common uses for personal lines of credit

Personal lines of credit are often used for expenses with uncertain or ongoing costs, including:

- Home improvement projects

- Emergency expenses

- Medical bills resulting from a chronic condition

- Bridging the gap if you’re a seasonal or gig worker

- Wedding expenses

- Moving and relocation

- Overdraft protection

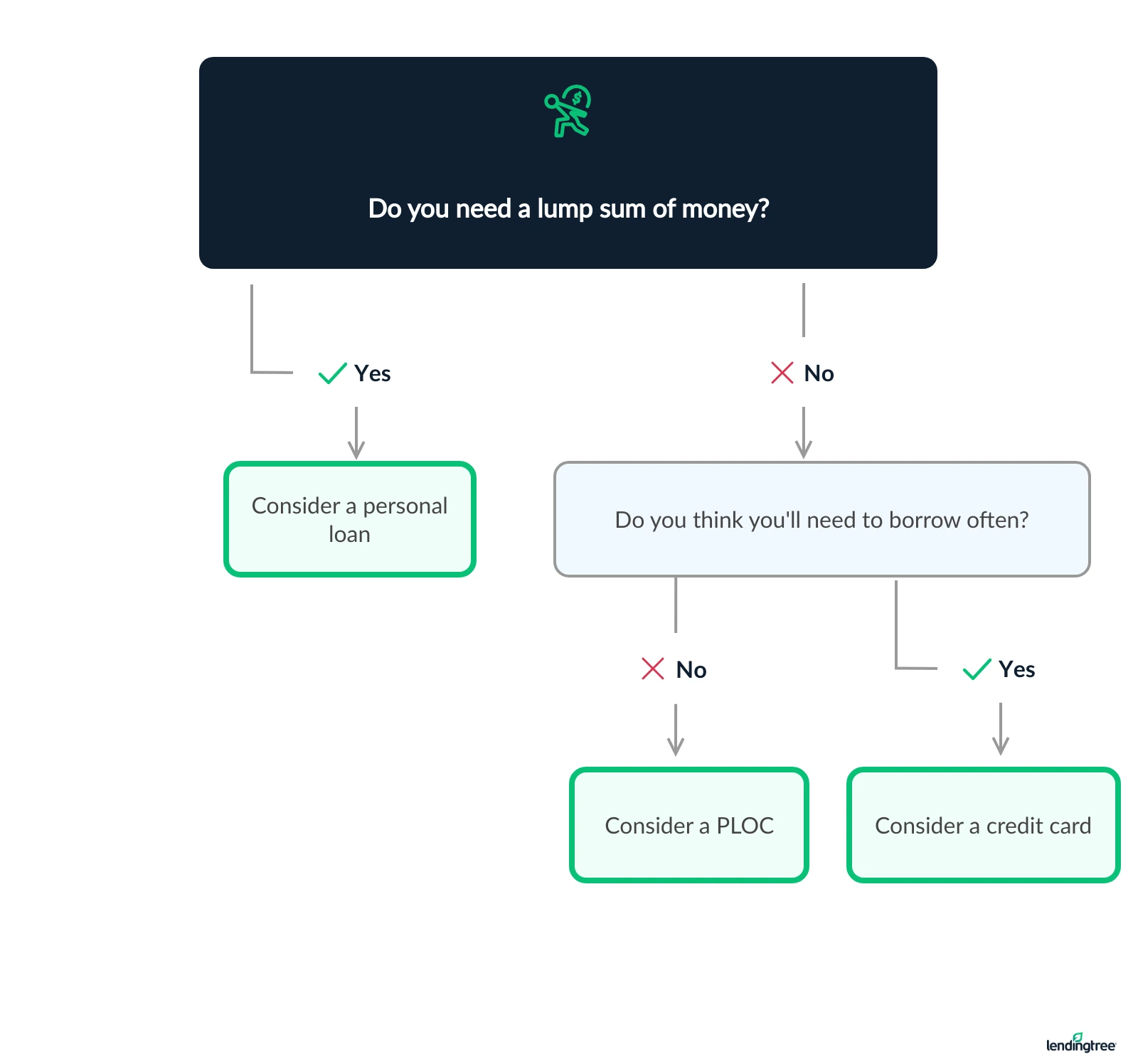

Should you get a personal line of credit?

Since personal lines of credit are less common than credit cards and loans, it can be hard to know when to use one. Here are some signs a PLOC could be a good fit — and when another option may make more sense:

Consider a line of credit

- You want ongoing access to money that you can borrow from again and again

- You’re not sure how much money you’ll need

- You have good or excellent credit

Consider alternatives

- You have fair or bad credit (may only qualify for high rates and fees)

- You can afford to pay back what you borrow within a month (consider a credit card)

- You want predictable payments that won’t change with the market (consider a loan)

Learn more about alternatives to personal lines of credit.

How does a personal line of credit work?

Personal lines of credit can be intimidating. They aren’t very common, and the time periods for borrowing and repaying (called your draw and repayment periods) can vary across lenders.

Generally, there are three ways a personal line of credit can work:

| Type of PLOC | How it works |

|---|---|

| Continuous draw period | Borrow anytime, as long as you have the credit available and your lender hasn’t closed your line of credit |

| Draw period and repayment period | Borrow and make minimum monthly payments during your draw period; pay your outstanding balance during your repayment period |

| Simultaneous repayment period | Borrow and repay at the same time; outstanding balance is due at the end of your PLOC |

When you’re approved for a line of credit, you might not get a card. Not many lenders offer cards for their PLOCs. Instead, you’ll probably get a checkbook and/or access to an online portal so you can transfer funds electronically.

PLOC fast facts

Not every bank offers PLOCs

PLOCs can be hard to find, but some lenders on the LendingTree marketplace do offer them, as do the lenders on this list.

PLOCs usually require good credit

You could get a PLOC with bad credit, but traditional banks and credit unions usually require a 670+ FICO Score.

PLOCs almost always have variable interest rates

Variable interest rates are guided by The Wall Street Journal prime rate, so they go up and down while your line is open.

PLOCs typically have lower rates than credit cards

The average credit card rate over the past couple of years has hovered just above 20%, according to LendingTree’s monthly report. The lowest PLOC rate on this list starts at 9.00% (with autopay), offered by Fifth Third Bank.

PLOCs can have a lot of fees

Compared to personal loans, PLOCs have a lot of fees. You might even get charged for simply using your PLOC.

Making sense of PLOC rates

Since most personal lines of credit have variable rates, your interest rate (and cost of borrowing) may change over time.

You might see personal line of credit rates advertised as Prime + X%. Here’s what that means.

Imagine a lender is offering Prime + 4% to Prime + 22.50%.

1. Find the Wall Street Journal prime rate. Look under “International Rates,” then find the latest prime rate for the U.S. For the sake of this example, say the prime rate is 6.75%.

2. Add the prime rate (6.75% in this example) to both numbers in the range:

6.75% + 4% = 10.75%

6.75% + 22.50% = 29.25%

3. The result is the lender’s rate range. Here, the range would be 10.75% to 29.25%. onal line of credit with bad credit, bu

Personal line of credit pros and cons

PLOCs aren’t as popular as credit cards and personal loans, but they can come in handy for expenses that don’t have a clear price tag. Still, PLOCs have drawbacks you should consider.

PROS

- Tend to have lower rates than credit cards

- Gives you access to a steady stream of money

- You pay interest only on what you borrow

CONS

- Interest starts accruing as soon as you borrow

- You usually need at least good credit to get a PLOC

- Have more fees than other types of loans

- Interest rates usually fluctuate with the market

From the expert: When a PLOC may be the better choice

If you want to consolidate debt or make a major purchase with a fixed price, a personal loan would be preferable.

PLOCs and credit cards are similar, so knowing which to choose is tricky.

If you have excellent credit, you might qualify for lower rates on a PLOC. But if your credit needs work or you want to capitalize on rewards that come with a credit card, the latter may be a better fit.

Alternatives to personal lines of credit

The great thing about personal finance is that it’s personal. If a personal line of credit doesn’t work for you, you may have another option that better fits your needs.

Credit card

Credit cards make more sense for everyday purchases — as long as you pay your balance in full each month.

Why people choose credit cards

- Built-in grace period before interest starts

- Potential cash back and rewards

- Easy to use for everyday purchases

Downsides compared to personal lines of credit

- Higher average interest rates

- Easier to overspend

Personal loan

Personal loans can be a smart choice when you need to borrow a large sum of money one time.

Why people choose personal loans

- Predictable costs and monthly payments

- A lump sum of money can be great for one-time expenses

- Easier to understand and use

Downsides compared to personal lines of credit

- Pay interest on the entire amount you borrow

- Less flexible since you can only borrow once

Learn more about when to choose lines of credit vs. personal loans.

Home equity line of credit (HELOC)

Homeowners considering a PLOC might want to check out a HELOC instead. HELOCs tend to have lower rates — but they’re also riskier.

Why people choose HELOCs

- Typically come with low rates

- Great for home improvement projects

Downsides compared to personal lines of credit

- Uses your home as collateral

- Could lose your home to foreclosure if you can’t make payments

Learn more about how HELOCs work.

Choosing among a personal line of credit, loan and credit card

Choosing among PLOCs, personal loans and credit cards can feel intimidating, but it’s easier when you break it down to what you need. The best option usually depends on whether your expenses are predictable and what kind of credit you have.

If you have excellent credit and can afford to pay your charges off within a year or two, consider getting a 0% intro APR credit card and paying off your charges interest-free in the promotional period.

How lines of credit compare to credit cards and personal loans

| Personal line of credit | Credit card | Personal loan | |

|---|---|---|---|

| Borrowing | ♻️Borrow again and again up to the borrowing limit | ♻️Borrow again and again up to credit limit | 💰Borrow once |

| Interest | Starts immediately; variable APR (rates change with the market) | Grace period before interest charges; variable APR (rates change with the market) | Fixed APR (set rates that don’t change with the market) |

| Flexibility | Medium | High | Low |

| Ease of use | Medium | Easy | Medium |

| Best for | Ongoing and uncertain expenses | Everyday expenses | One-time expenses |

What sets LendingTree content apart

Expert

Our personal loan writers and editors have 32 years of combined editorial experience and 28 years of combined personal finance experience.

Verified

100% of our content is reviewed by certified personal finance professionals and meets compliance and legal standards.

Trustworthy

We put your interests first. We’ll tell you about any loan drawbacks and be clear about when to consider alternatives.

Frequently asked questions

It’s possible to get a personal line of credit with bad credit, but you’ll probably have to look to an online lender. Bad credit PLOCs often come with high rates and fees. NetCredit, for example, offers bad credit PLOCs but charges a 10% fee every time you use your credit line — that’s $100 out of every $1,000 you borrow.

Traditional PLOCs are usually offered by banks, which tend to require at least good credit (670+).

Compared to other types of financing, PLOCs are heavy on fees. Your personal line of credit could include:

- Origination fees. When you open your line of credit, your lender could charge a percentage of your credit line as an origination fee.

- Annual or monthly fees. You may need to pay a maintenance fee every year or month that your line of credit is open.

- Late payment fees. Budget for a possible fee if you pay late.

- Over-limit fees. If you charge past your credit limit, there could be a fee.

- Cash equivalent fees. Some lenders charge when you use your PLOC card to pay for things directly (as opposed to doing an online transfer into your checking account).

- Cash advance ATM fees. You might be able to tap your PLOC using an ATM, but it will probably come with a fee.

- Foreign transaction fees. These can apply to foreign purchases or if you use an ATM overseas to get foreign currency.

- Application fees. These aren’t common and can be a sign of predatory lending.

When you’re comparing offers for personal lines of credit, pay special attention to:

- APRs: Your APR measures the cost of your PLOC, including interest and fees. The higher the APR, the more expensive the PLOC.

- Draw/repayment periods: Many PLOCs have a continuous draw period, which means there’s no end date to your borrowing. However, some lenders have specific draw periods and specific repayment periods. These dictate when you can borrow and when you have to start paying off any remaining balance left on your line.

- Line amounts: Some PLOCs are small; some are big. If you don’t need a lot of money, make sure you meet the lender’s minimum credit line requirement. For big loans, make sure the lender can provide the amount you need.

- Fees: PLOCs have more fees compared to some other types of loans (including personal loans). Ask for a breakdown of fees to make sure the PLOC is actually worth it.

- Ease of use: Does the PLOC come with a card or just checks?

- Customer complaints: The Consumer Financial Protection Bureau maintains a database of complaints against lenders. Before signing a contract, check customer reviews for the lender you’re considering.