Consolidating Credit Card Debt Into a Personal Loan Could Save Borrowers $1,750 and Cut Repayment by 6 Months

Struggling with credit card debt? If you have a strong credit score, you could save $1,750 in interest and six months of payoff time by consolidating $10,000 of credit card debt with a low-interest personal loan at the same monthly payment.

That’s the biggest takeaway from LendingTree research on debt consolidation — one of the most powerful tools that people have in their battle against credit card debt. To determine debt consolidation’s impact, we assumed card balances of $5,000 or $10,000, then applied average APRs for personal loan inquiries made on the LendingTree platform and average APRs for new credit card accounts — based on creditworthiness — and calculated the total interest and payoff times under a fixed monthly payment scenario.

What we found should be encouraging to those who feel helpless over credit card debt, especially if you have good credit: You have more power than you think — if you’re willing to act.

That’s an important question because the savings in a debt consolidation analysis are primarily driven by differences in the interest rates involved.

- The personal loan APRs in this report reflect the average APRs offered on 36-month personal loan inquiries on the LendingTree platform in January 2026 for various credit score ranges. They represent offers received, not necessarily funded loans.

- The credit card APRs come from LendingTree’s monthly review of rates and other terms and conditions for more than 200 new credit card offers from more than 50 issuers. For those with credit scores of 680 to 759, we assumed a 23.79% APR — the average APR for all new card offers in January 2026, per our analysis. For those with a 760 or better credit score, we assumed a 20.18% credit card APR — the average minimum APR offered on new card offers, per our January 2026 review. (Note that this reflects the average of advertised minimum APRs, not the average APR consumers ultimately receive.)

- Consolidating $10,000 of credit card debt into a personal loan could save borrowers $1,750. Consumers with a credit score of 760 or higher could save $1,750 by choosing to roll $10,000 of credit card debt into a $10,000 personal loan, even when making the same monthly payment. This is due to the wide variance in the APRs we assumed they’d receive — 13.34% for the personal loan and 20.18% for the credit card.

- Debt consolidation can slash payoff times, too. In the scenario above, borrowers with credit scores of 760 or higher could pay off their debt six months faster. At a fixed monthly payment of $339, it would take 42 months to pay off a $10,000 credit card balance, compared with 36 months for a personal loan based on the assumed APRs and amortization schedule in our analysis. Borrowers with lower credit scores could also benefit, but time savings decrease as interest rates narrow.

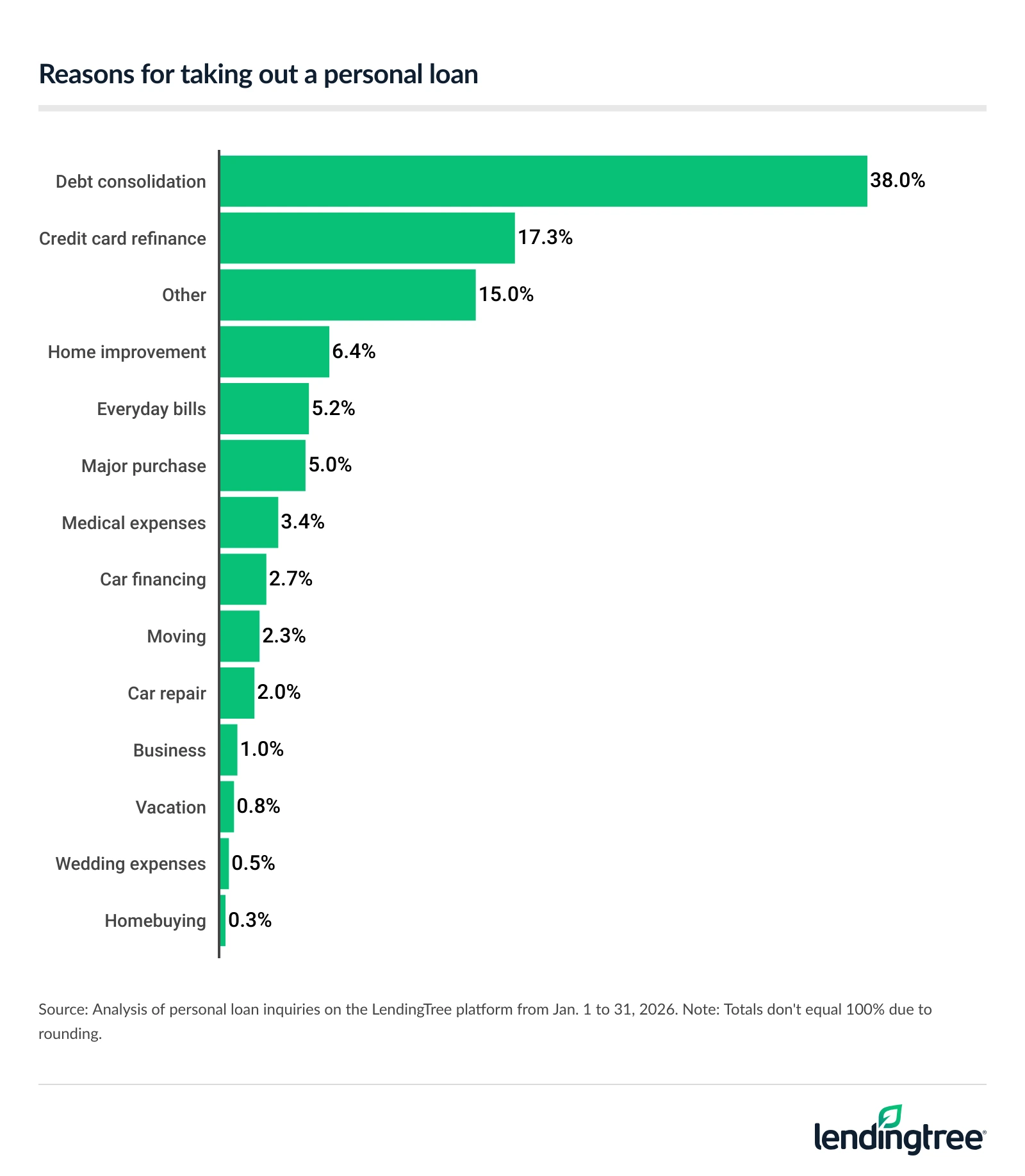

- Debt consolidation and credit card refinancing drive the majority of personal loan inquiries on the LendingTree platform. In January 2026, 38.0% of inquiries were for debt consolidation, while 17.3% were for credit card refinancing — making them the two most common reasons borrowers seek personal loans. In six states, including Alaska, Utah and Washington, at least 20% of inquiries were for credit card refinancing.

How borrowers could save $1,750 (and 6 months of payoff time)

Debt consolidation is as simple as it is powerful: You use a low-interest loan to pay off a higher-interest loan, saving yourself both money and time, assuming you qualify for a lower rate and avoid taking on additional debt.

That’s the basic idea, but how well does it work? That was the goal of LendingTree’s analysis, and there’s good news: It works really well, especially if you have great credit.

If you have a very good or exceptional credit score of 760 or higher, you could save $1,750 by moving $10,000 of credit card debt to a $10,000 personal loan, even when making the same monthly payment. That’s because of the dramatic difference in the APRs someone with that credit score would be likely to receive — 13.34% for the personal loan and 20.18% for the credit card.

Here’s a closer look at the numbers.

Cost of paying off a credit card vs. a personal loan with the same monthly payment: $10,000 balance, 760+ credit score

| Details | Credit card | Personal loan | Difference |

|---|---|---|---|

| Total interest paid | $3,939 | $2,189 | $1,750 |

| Total loan cost | $13,939 | $12,189 | $1,750 |

| Monthly payment | $339 | $339 | $0 |

| APR | 20.18% | 13.34% | 6.84 points |

| Total payoff time (months) | 42 | 36 | 6 |

With debt consolidation, it’s important to remember that you’re not just saving money. You’re also saving time. In the above example, the borrower would pay off their balance six months faster with a consolidation loan. That’s a big deal.

If you cut that balance down to $5,000 with the same monthly payment for both debt types, the savings are smaller but still significant. You’d save $875 with a personal loan over a credit card — and still take six fewer months to pay it off under the same rate and payment assumptions.

Cost of paying off a credit card vs. a personal loan with the same monthly payment: $5,000 balance, 760+ credit score

| Details | Credit card | Personal loan | Difference |

|---|---|---|---|

| Total interest paid | $1,969 | $1,094 | $875 |

| Total loan cost | $6,969 | $6,094 | $875 |

| Monthly payment | $169 | $169 | $0 |

| APR | 20.18% | 13.34% | 6.84 points |

| Total payoff time (months) | 42 | 36 | 6 |

Don’t have excellent credit? You can still save

While the biggest savings are reserved, as you might expect, for those with the best credit, others can definitely still benefit from debt consolidation.

Borrowers with $10,000 in credit card debt and a credit score of 720 to 759 — still good or very good but shy of exceptional — could save $1,708 and pay off their debt five months faster with a debt consolidation loan.

Cost of paying off a credit card vs. a personal loan with the same monthly payment: $10,000 balance, 720-759 credit score

| Details | Credit card | Personal loan | Difference |

|---|---|---|---|

| Total interest paid | $4,671 | $2,963 | $1,708 |

| Total loan cost | $14,671 | $12,963 | $1,708 |

| Monthly payment | $360 | $360 | $0 |

| APR | 23.79% | 17.71% | 6.08 points |

| Total payoff time (months) | 41 | 36 | 5 |

Part of the reason why the savings are smaller is that there is less difference between the APRs that someone at this credit level would expect to get with a personal loan (17.71%) versus a credit card (23.79%). The difference is 6.08 percentage points — a big deal but less than the 6.84 percentage point spread seen at the highest credit level in our analysis.

As with the previous example, when you reduce the initial balance to $5,000, you save less by consolidating your debts, but the savings are still significant. You pay $854 less in interest and pay off the balance in five fewer months with a personal loan than with a credit card.

Cost of paying off a credit card vs. a personal loan with the same monthly payment: $5,000 balance, 720-759 credit score

| Details | Credit card | Personal loan | Difference |

|---|---|---|---|

| Total interest paid | $2,335 | $1,481 | $854 |

| Total loan cost | $7,335 | $6,481 | $854 |

| Monthly payment | $180 | $180 | $0 |

| APR | 23.79% | 17.71% | 6.08 points |

| Total payoff time (months) | 41 | 36 | 5 |

Even those a rung further down the credit ladder can benefit from debt consolidation, our analysis showed. Borrowers with good credit scores of 680 to 719 could save $570 in interest when consolidating $10,000 in credit card debt into a personal loan and pay off their debt two months faster.

Cost of paying off a credit card vs. a personal loan with the same monthly payment: $10,000 balance, 680-719 credit score

| Details | Credit card | Personal loan | Difference |

|---|---|---|---|

| Total interest paid | $4,268 | $3,698 | $570 |

| Total loan cost | $14,268 | $13,698 | $570 |

| Monthly payment | $381 | $381 | $0 |

| APR | 23.79% | 21.73% | 2.06 points |

| Total payoff time (months) | 38 | 36 | 2 |

For those at this level of credit, the gap between the average APR for a personal loan and one for a credit card is significantly smaller than it is for people with better credit. Just 2.06 percentage points separate the average personal loan APR (21.73%) from the average credit card APR (23.79%).

Lower your balance to $5,000 at this credit level, and your potential savings shrink to just $285. That’s not nothing, of course, and any interest rate reduction is welcome, but the savings pale in comparison to those that people at other credit levels might find.

Cost of paying off a credit card vs. a personal loan with the same monthly payment: $5,000 balance, 680-719 credit score

| Details | Credit card | Personal loan | Difference |

|---|---|---|---|

| Total interest paid | $2,134 | $1,849 | $285 |

| Total loan cost | $7,134 | $6,849 | $285 |

| Monthly payment | $190 | $190 | $0 |

| APR | 23.79% | 21.73% | 2.06 points |

| Total payoff time (months) | 38 | 36 | 2 |

These 2 reasons drive the majority of personal loan inquiries on the LendingTree platform

There are countless reasons why people get personal loans. However, when we ask those applying for one on the LendingTree platform what they plan to use the loan for, two reasons stand far above the rest: debt consolidation and credit card refinancing, based on self-reported loan purposes at the time of inquiry.

In January 2026, 38.0% of personal loan inquiries on the LendingTree platform were for debt consolidation, while 17.3% were for credit card refinancing. That means that more than half of all people seeking one of these loans through LendingTree did so for one of those two reasons.

The only other option chosen by more than 10% of applicants was “other” — meaning they applied for a reason other than what we had listed as options. Fifteen percent of applicants made that choice. Meanwhile, home improvement (6.4%), everyday bills (5.2%) and major purchases (5.0%) were next on the list. At the bottom: homebuying (0.3%), wedding expenses (0.5%) and vacations (0.8%).

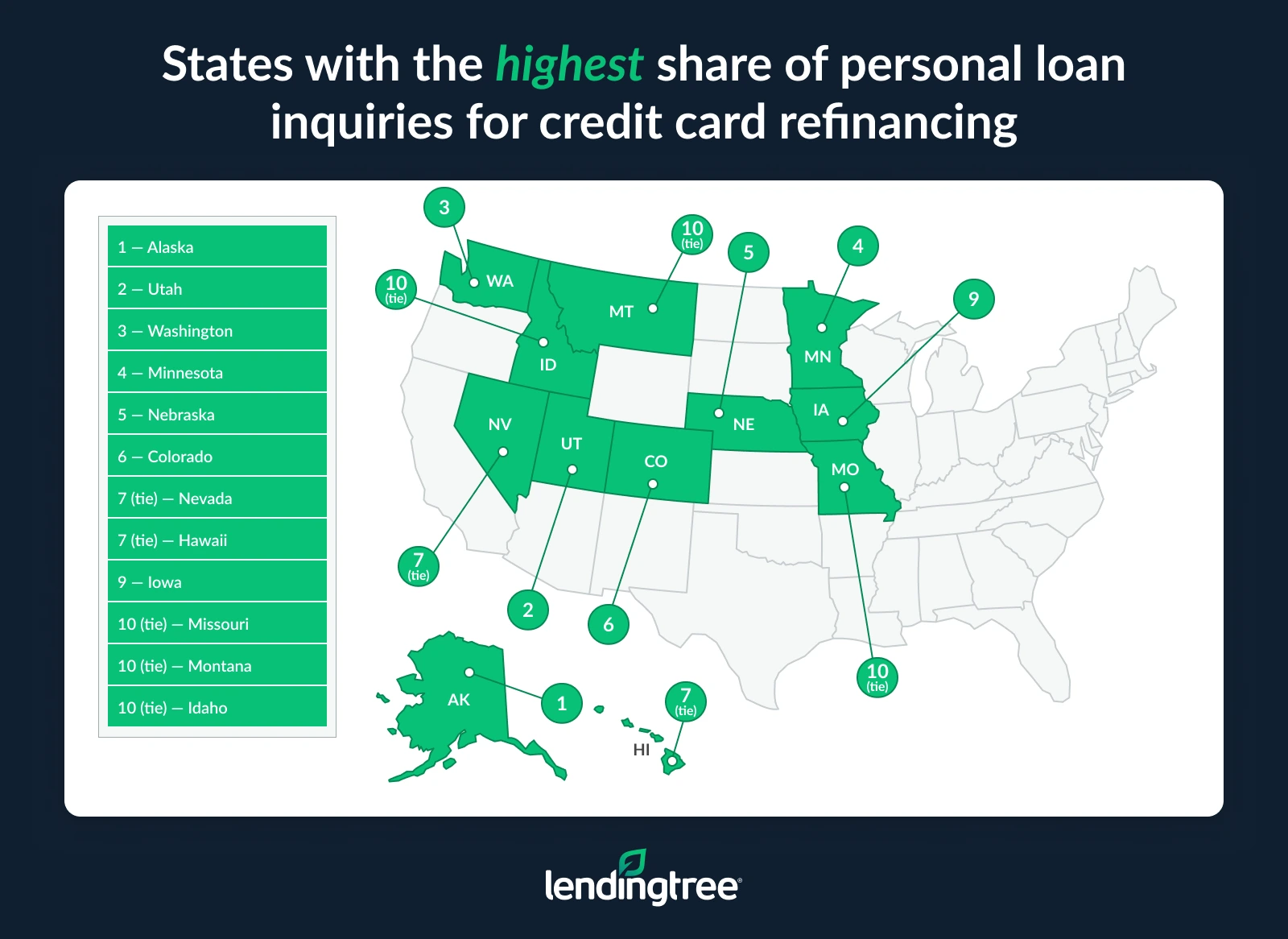

In six states, at least 20% of inquiries were for credit card refinancing. Alaska (23.7%) led the way, with Utah (21.9%) and Washington (21.5%) not far behind. New Hampshire was at the bottom of the list at 11.9%, nearly half the percentage seen in Alaska.

Share of personal loan inquiries for credit card refinancing, by state

| Rank | State | % of personal loan inquiries for credit card refinancing |

|---|---|---|

| 1 | Alaska | 23.7% |

| 2 | Utah | 21.9% |

| 3 | Washington | 21.5% |

| 4 | Minnesota | 20.2% |

| 5 | Nebraska | 20.1% |

| 6 | Colorado | 20.0% |

| 7 | Nevada | 19.9% |

| 7 | Hawaii | 19.9% |

| 9 | Iowa | 19.6% |

| 10 | Missouri | 19.3% |

| 10 | Montana | 19.3% |

| 10 | Idaho | 19.3% |

| 13 | Alabama | 19.0% |

| 14 | Vermont | 18.8% |

| 15 | Connecticut | 18.7% |

| 16 | New Mexico | 18.6% |

| 16 | California | 18.6% |

| 16 | Oregon | 18.6% |

| 19 | Wisconsin | 18.5% |

| 20 | South Dakota | 18.4% |

| 20 | South Carolina | 18.4% |

| 20 | Massachusetts | 18.4% |

| 23 | Wyoming | 18.3% |

| 23 | Louisiana | 18.3% |

| 25 | New Jersey | 18.0% |

| 25 | Oklahoma | 18.0% |

| 25 | Michigan | 18.0% |

| 25 | North Dakota | 18.0% |

| 29 | Maine | 17.9% |

| 30 | Texas | 17.7% |

| 30 | Rhode Island | 17.7% |

| 32 | Florida | 17.6% |

| 33 | Mississippi | 17.5% |

| 34 | Delaware | 17.4% |

| 34 | Kentucky | 17.4% |

| 36 | Kansas | 17.3% |

| 37 | Arizona | 17.2% |

| 37 | Ohio | 17.2% |

| 39 | Maryland | 16.9% |

| 40 | Indiana | 16.3% |

| 41 | Arkansas | 16.2% |

| 41 | New York | 16.2% |

| 43 | Georgia | 15.9% |

| 44 | Tennessee | 15.8% |

| 45 | North Carolina | 15.5% |

| 46 | Pennsylvania | 14.8% |

| 47 | West Virginia | 14.4% |

| 48 | Virginia | 13.6% |

| 49 | Illinois | 12.6% |

| 50 | New Hampshire | 11.9% |

Pros and cons of debt consolidation

Consolidating your debt makes sense if you can score a lower interest rate and avoid fees that outweigh your potential savings. However, it’s still worth considering the advantages and disadvantages before moving forward.

Pros

- Lower interest rates

- One easy-to-manage monthly payment

- Can help repay debt quicker

- Can boost your credit

Cons

- Not everyone qualifies to get a lower rate

- Might come with upfront costs

- Less payment flexibility than with credit cards

- Won’t solve long-term financial problems

Pros of debt consolidation

Lower interest rates

One of the top reasons to consolidate debt is to access a lower interest rate, which can save money in the long run if the new APR is meaningfully lower than your existing rates.

As outlined in our research, borrowers can reduce their total repayment by switching to a low-rate personal loan. However, your new rate will depend on your current balances and credit score. Our debt consolidation calculator can help estimate if the new rate is worth making the switch.

One easy-to-manage monthly payment

Consolidating doesn’t just reduce the interest you pay and the time it takes to pay off your balance. It can also reduce the total number of bills you have to worry about each month, depending on how many loans you consolidate. That can help reduce the risk of forgetting a bill or going into default.

Further, consolidating can provide a simple timeline to becoming debt-free, which can be a motivating factor for many.

Can help repay debt quicker

By securing a lower interest rate, more of your payment can go toward the loan’s principal. This is how borrowers can trim months off their repayment period under a fixed payment schedule.

Can boost your credit

Although applying for new credit requires a hard credit check, making on-time payments on your new loan can help build your credit. Your credit utilization ratio will also improve once you’ve paid off your credit card debt. Also, if you’ve never had a personal loan, getting one can improve your credit mix (the various types of loans that you’ve had), another key factor in credit scoring.

Cons of debt consolidation

Not everyone qualifies to get a lower rate

Debt consolidation only works if you move the debt to a loan with a lower interest rate, and low rates aren’t available to everyone. In general, borrowers with the highest scores get the lowest rates. If your score is less than ideal, a debt consolidation loan for bad credit might help. However, it’s important to ensure your new rate is lower than what you’re currently paying.

Might come with upfront costs

A debt consolidation loan may come with additional fees, which can include the following:

- Origination fee

- Balance transfer fee

- Prepayment penalty

Research before signing on the dotted line to ensure the extra fees are worth it.

Less payment flexibility than with credit cards

Personal loans are installment loans, meaning that you’re expected to pay the same amount each month. That’s different from credit cards, which let you pay whatever you’d like each month, as long as it’s above the minimum required. Personal loans’ predictability is good when budgeting, but it can be a challenge in a short-term rough patch.

In the end, you’ll want to ensure you can afford the new monthly payment before consolidating your debt.

Won’t solve long-term financial problems

Debt consolidation might help fix your immediate financial woes, but it doesn’t prevent you from slipping into the same debt patterns in the future. That often requires being more intentional with your spending, and a well-made budget can help.

You can’t make a meaningful plan to improve your finances if you don’t know how much money is coming in and going out of your household each month. Once you have a handle on that, you can prioritize your spending, making some potentially tough choices to free up more money to put toward your top goals.

This is something that anyone can do on their own. However, if you’d like help, consider credit counseling. Accredited nonprofit credit counselors can help with budgeting, negotiating with creditors and everything in between, and they may offer debt management plans as an alternative to consolidation loans.

Methodology

LendingTree researchers analyzed personal loan inquiries on the LendingTree platform from Jan. 1 to 31, 2026, to calculate average APRs for borrowers across different credit score ranges and to identify the primary reasons consumers seek personal loans.

The credit score ranges researchers examined were:

- 680 to 719 (good)

- 720 to 759 (good to very good)

- 760+ (very good to exceptional)

Researchers assumed borrowers took out either a $5,000 or $10,000 personal loan with a 36-month term. Personal loan APRs reflect average APRs offered on 36-month personal loan inquiries on the LendingTree platform during the examined period. These APRs were used to calculate average monthly payments and total interest paid for each credit score range.

To compare costs, researchers then calculated how long it would take to pay off the same $5,000 or $10,000 balance using a credit card while making the same fixed monthly payment as the personal loan. Credit card APRs are assumed to be 20.18% for borrowers with credit scores of 760 or higher, and 23.79% for those with lower scores, based on LendingTree’s analysis of new credit card offers in January 2026.

All scenarios assume no new charges and that payments are applied consistently until the balance is paid in full.

Get personal loan offers from up to 5 lenders in minutes