Buying a Mobile Home: Pros & Cons, Financing and Refinancing Options

A manufactured home (often called a mobile home) is built in a factory and moved to a permanent location instead of being built on-site. It’s typically a more affordable path to homeownership, and all of the most common home loan programs you’re likely familiar with allow for manufactured homes.

The average sales price of a manufactured home is around $163,100 (for a double-wide) as of February 2026 — very affordable when compared to the current median site-built home price of $403,200.

Learn more about how you can finance (or refinance) a mobile home using conventional or government-backed loans.

What is a manufactured home?

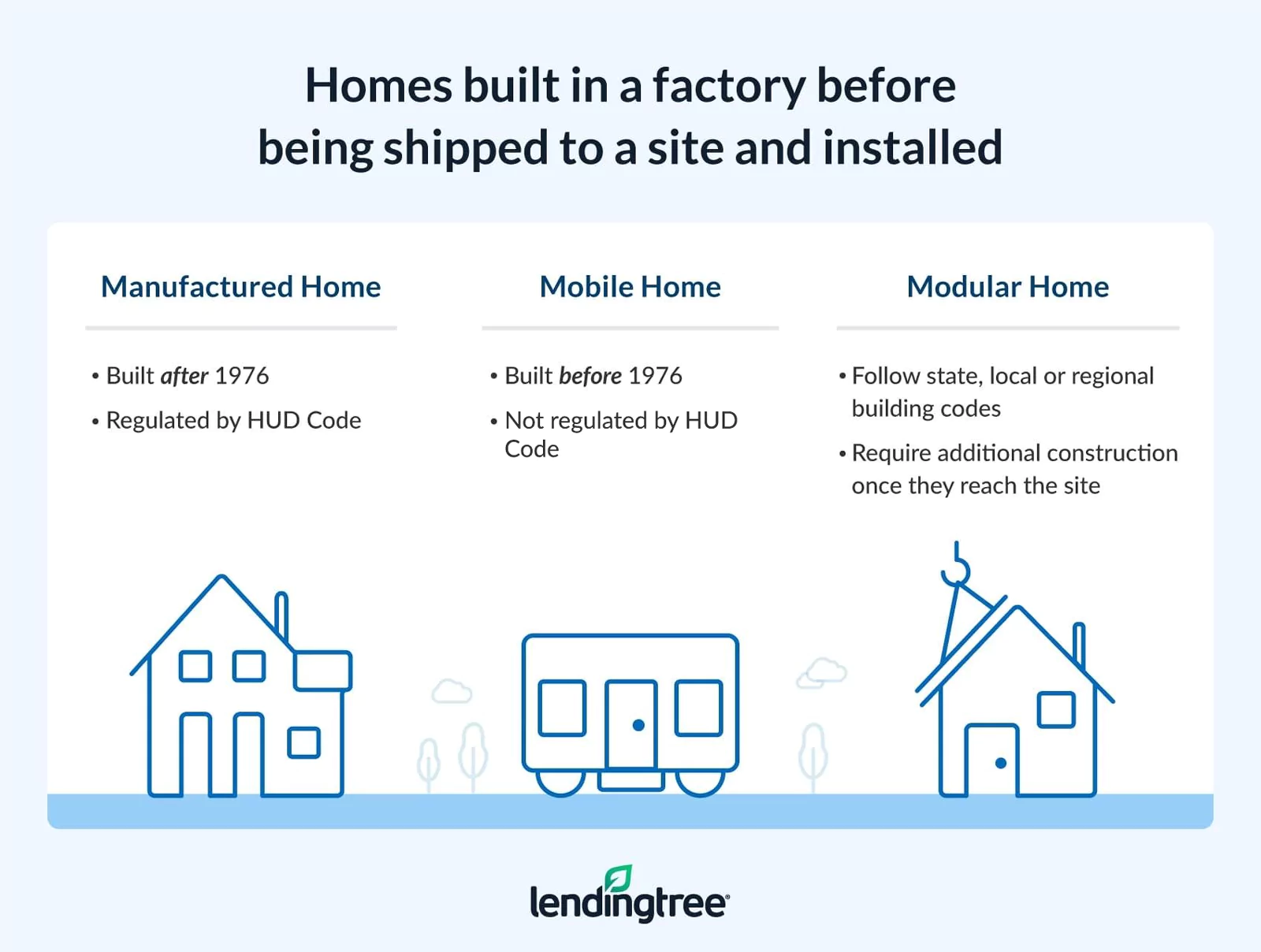

Manufactured homes are constructed in factories according to the safety standards set by the U.S. Department of Housing and Urban Development (HUD). The home is built on a chassis, also called a permanent frame.

Once construction is finished, the manufactured home is taken to a new location in one or more sections. Usually, it’s transported either to a dealer’s lot, a plot of land or a manufactured home park. After the home reaches its permanent location, it’s typically attached to a foundation.

Note the following criteria for manufactured homes:

- They must be at least 320 square feet in size.

- To be considered a manufactured home, they were constructed after June 15, 1976.

- Manufactured homes built since 1976 must contain a certification label (commonly known as a HUD tag) to show that they meet current safety standards set by the HUD code, including body and frame requirements, thermal protection, plumbing, electrical and fire safety.

Manufactured home vs. mobile home

Manufactured homes are often referred to as “mobile homes” but, technically, that term is outdated.

Manufactured homes built before June 15, 1976, are mobile homes; those constructed after that date are manufactured homes. That date signifies when HUD implemented the Manufactured Home Construction and Safety Standards (also known as the “HUD code”), which regulates mobile home construction.

Manufactured home vs. modular home

“Modular home” is another term people often associate with manufactured homes, but these types of structures aren’t identical. Like manufactured homes, modular homes are factory-built and then transported before being finished at the site. However, just as with site-built homes, modular homes follow state, local or regional building codes rather than federal requirements.

How much does buying a manufactured home cost?

The average cost of a single-wide manufactured home was $89,100 in February 2026, the latest available figures. For a double-wide, the average is around $163,100. If you compare that to the $403,200 price tag of an existing single-family, site-built home, manufactured homes are clearly significantly cheaper — but is it just because they tend to be smaller?

The answer is no, because a new manufactured home in the United States is around $84 cheaper per square foot than a site-built home, according to data from the most recent U.S. Census.

However, manufactured home costs vary by location and home size, so expect to find a broad range in prices. Manufactured homes are cheapest in Indiana, Wyoming and Ohio, but most expensive in Washington, California and Arizona, according to a LendingTree analysis.

Pros and cons of buying a manufactured home

Manufactured homes represented about 9% of new single-family residential buildings in 2024, according to data from the U.S. Census Bureau’s most-recent Manufactured Housing Survey. But before you jump into any type of homeownership, it always pays to consider the pros and cons of buying a manufactured home.

Pros

- Affordability. Manufactured homes continue to offer a more affordable option, costing far less per square foot than site-built homes.

- Efficient construction. Because manufactured homes are made in factories, their construction isn’t affected by weather or other factors that might delay site-built homes.

- Multiple financing options. There are a wide range of ways to finance the purchase of a manufactured home. Many options allow you to finance both the land and the home, but it’s also relatively easy to finance or refinance just the manufactured home itself.

- Reasonably safe. Safety concerns around manufactured home parks are largely a myth — crime rates aren’t significantly different in or around these communities when compared to any other residential neighborhood, according to research.

Cons

- Higher interest rates. Borrowers typically encounter higher mortgage rates for manufactured home loans than with other loan types.

- Higher chances of loan denial. Only about 30% of manufactured home loan applications are approved, compared to more than 70% for site-built homes.

- Social stigma. Manufactured housing has come a long way in recent decades, but that doesn’t mean that everyone has gotten the memo. You might receive negative opinions from friends, family or colleagues if you buy a manufactured home.

- Reselling can be difficult. Manufactured homes aren’t easy to resell, and can pose especially expensive challenges if you want to sell only the home while keeping the land. It’ll likely cost thousands of dollars to move a manufactured home to a new site.

Regret may be less common than you think. About three out of four (78%) of manufactured homeowners and residents are satisfied with their homes, according to data from MHInsider magazine’s latest State of the Industry report.

6 types of loans for buying a manufactured home

| Required to be placed on privately owned land? | Minimum down payment | Minimum credit score | Loan limits | |

|---|---|---|---|---|

| Conventional loans | Yes for Fannie Mae programs; No for Freddie Mac programs | 3% to 5% | Traditionally 620 | $832,750 in most of the US but varies by location

The exact limit depends on where the home is located.

|

| FHA loans | No | 3.5% to 10% | 500 to 580 | $43,377 to $193,719

The exact limit depends on the home size and whether you’re purchasing land.

|

| VA loans | Yes | 5% | Commonly 620, but varies by lender | None with full entitlement |

| USDA loans | Yes | 0% | Commonly 640, but varies by lender | None |

| Personal loans | No | 0% | Commonly 580, but varies by lender | Varies by lender |

| Chattel loans | No | 0% | Commonly 575, but varies by lender | Varies by lender |

Conventional loans

Many private lenders offer manufactured home loans, including financing a manufactured home with land. However, in most cases, you’ll have to place the home on a permanent foundation and title it as real estate property to qualify for a manufactured home mortgage. Here are some options for conventional loans on manufactured homes.

- Fannie Mae MH Advantage. To finance a manufactured home, it must be certified as an MH Advantage home. Homes that qualify typically have construction, design and features similar to site-built homes and are located in residential areas. These manufactured homes are built on a permanent chassis, installed on a permanent foundation on land and are titled as real estate. They can be single- or multi-width. Loans can be fixed- or adjustable-rate mortgages.

- Fannie Mae Standard MH. This loan option is for homes that don’t meet the eligibility requirements of the MH Advantage program. However, unless it’s in a co-op or condo project, the borrower must own the land the home is placed on. The manufactured home must be built on a permanent chassis, installed on a permanent foundation on land the borrower owns (with or without a mortgage) and titled as real estate. Loans may be fixed- or adjustable-rate.

- Freddie Mac Manufactured Home Mortgage. These manufactured home mortgages are available in most states. Loan terms include both fixed- and adjustable-rate mortgages. Homes must be on a permanent foundation and can be placed on private property owned by the borrower, in a planned unit development or a condo project.

Government-backed loans

FHA manufactured home loans

You can buy a manufactured home with a loan insured by the Federal Housing Administration (FHA). These loans are available to finance the purchase of a manufactured home only, a lot only or both at once. In addition, you can use an FHA manufactured home loan for a home installed on a leased lot.

These loans do come with loan limits, though, and the loan term can’t exceed 20 years and one month for a single-wide, or 25 years and one month for a double-wide.

VA loans for manufactured homes

Loans backed by the U.S. Department of Veterans Affairs (VA) provide financing options to military service members, veterans and surviving spouses. VA loans for manufactured homes require that the homes be attached to a permanent foundation on land owned by the borrower or a manufactured home and land together. You’ll need a higher down payment than is required for most VA loans — 5% — and a shorter loan term (15 years and one month up to 25 years and one month).

USDA manufactured home loans

Low- to moderate-income homebuyers in rural areas who want to finance a manufactured home, or a home and lot, may qualify for a USDA Single Family Housing Guaranteed Loan. These loans offer flexible qualification requirements, including no minimum down payment and no minimum credit score.

Personal loans for manufactured homes

Depending on the cost of the manufactured home you’re buying, a personal loan may be an option. Personal loans can offer as little as several hundred dollars up to $150,000 or more.

These loans come with fixed rates and terms typically between two and five years (though some could be as long as seven years). However, personal loans typically have higher interest rates than mortgages. Exact personal loan requirements often vary, but most lenders will usually review your credit score, income and other financial details.

Chattel loans

Another way to buy a manufactured home is with a chattel loan. It’s like a mortgage, except it’s meant for high-priced personal property like boats, planes or heavy equipment (“chattel” is another word for “personal property”).

Chattel loans for manufactured homes are common and typically have higher interest rates than mortgages. The loan will be secured by your manufactured home alone; as such, unlike with a traditional mortgage, if you default on the loan, only the home can be repossessed — not the land.

The process of buying a mobile home

Buying a manufactured home entails a different process than purchasing other types of real estate. The exact method will vary by state, so it’s best to research your specific state’s requirements for information on regulations, permits and the process of buying a manufactured home.

Here are six steps you’ll need to take when buying a manufactured home:

1. Decide on the location for your manufactured home

If you’re purchasing land, or placing the manufactured home on property you already own, study the zoning laws and any other guidelines you’ll need to follow.

2. Search for a manufactured home

Work with your manufactured home retailer to customize your manufactured home, unless you’re purchasing a standard model or an existing manufactured home.

3. Secure financing

Work directly with a mortgage lender, broker or your manufactured home retailer to weigh your options for manufactured home loans. Similarly, compare lenders and loan terms if you’re considering a personal loan or chattel loan.

4. Prepare the home site

Your retailer will work closely with you to make sure the site is ready for your home’s installation. This includes securing necessary permits, addressing any issues that affect the installation of the home and preparing utility hookups.

5. Arrange your home’s delivery and installation

Your home is delivered and installed after the land or lot is ready.

6. Sign up for insurance

Before you can move in, you’ll likely need to insure the home and fulfill any other occupancy and maintenance requirements to avoid potential problems or delays.

Can you refinance a manufactured home?

If you own a manufactured home on a permanent foundation, you have three general loan options for refinancing:

- Limited cash-out refinances. A limited cash-out refinance allows you to pay off your current mortgage and roll in your closing costs and the construction fees charged to attach your home to your land. Another perk: You can pocket 1% of the new mortgage balance or $2,000, whichever is less.

- Cash-out refinances. If you’ve owned your manufactured home and land for at least 12 months and it’s a multi-width home, you may be able to borrow more than you currently owe with a new mortgage and pocket the difference. Be aware, though, that in most cases, you can’t borrow as much of your home’s value with a cash-out refinance on a manufactured home as you can with a site-built home.

- Streamline refinances. Manufactured homeowners with a loan backed by the Federal Housing Administration (FHA), U.S. Department of Veterans Affairs (VA) or the U.S. Department of Agriculture (USDA) may qualify for a streamline refinance. These programs usually don’t require income documentation or a home appraisal. Some popular streamline programs include the FHA streamline refinance and the VA interest rate reduction refinance loan (IRRRL).

Pros and cons of a mobile home refinance

Pros

- You could lower your monthly payment. A reduced monthly payment amount can free up space in your budget for other financial goals.

- You could reduce your interest rate. A lower interest rate can save you thousands in interest charges over the long haul.

- You could pay off your loan sooner. Switching to a shorter repayment term can help you more quickly own your home outright.

- You can access cash. You can convert some of your home equity into cash if you choose a cash-out refinance option.

Cons

- You’ll pay closing costs. Refinance closing costs must be paid before you can really start seeing savings.

- You might not break even. If you move or sell the home before your break-even point, the costs of refinancing outweigh your savings.

- You may end up with a higher payment. If you choose a cash-out refinance, your payments could get more expensive since you’re borrowing more than you currently owe.

View mortgage loan offers from up to 5 lenders in minutes