Compare Mortgage Refinance Rates Today

June mortgage refinance rates currently average 6.98% for 30-year fixed loans and 6.46% for 15-year fixed loans.

Advertising Disclosures

Loading Disclosures…

Get personalized refinance rates in seconds: The current average rates are a starting point, but your actual rate depends on your credit score, available home equity and location.

Enter a few details below to see real offers from lenders competing for your business.

Current refinance mortgage rates

These averages reflect national trends offered on LendingTree. Your personalized rate may vary based on your credit score, home equity and loan type.

| Loan product | Interest rate | APR |

|---|---|---|

| 30-year fixed rate refinance | 6.98% | 7.20% |

| 15-year fixed rate refinance | 6.46% | 6.93% |

| 10-year fixed rate refinance | 7.15% | 7.77% |

| FHA 30-year fixed rate refinance | 5.79% | 7.20% |

| 30-year 5/1 ARM refinance | 6.30% | 6.37% |

| VA 30-year fixed rate refinance | 6.16% | 6.47% |

| VA 15-year fixed rate refinance | 6.02% | 6.78% |

Average interest rates disclaimer

Mortgage Rate Trends

Rate trend chart

Rate summary

| Loan Type | Avg. APR | 3 Month Diff. |

|---|---|---|

| 30 Year Fixed | 7.16% | 0.30% |

| 15 Year Fixed | 6.72% | 0.52% |

| 5/1 ARM | 6.40% | 0.17% |

Which loan term should you choose?

Choosing the right loan term comes down to a trade-off between monthly payment and total interest.

| Loan term | Monthly payment | Total interest | Best for |

|---|---|---|---|

| Shorter-term refinance (15-year) | Higher | Lower | Paying off your home faster |

| Longer-term refinance (30-year) | Lower | Higher | Keeping payments more affordable |

While shorter-term loans come with higher monthly payments, they can save you tens of thousands in interest over time. However, you should make sure your budget can handle the higher payment before switching to a shorter term. If you’re unsure, you can keep a longer-term loan and make extra payments to pay off your balance faster.

How to compare mortgage refinance rates

Compare offers from at least three to five lenders to find the best deal. Focus on interest rates, APR and closing costs.

- Use a rate-comparison platform. Mortgage rates change daily, so you’ll need quotes from the same day to make a fair comparison. Platforms like LendingTree let you enter your information once and receive multiple competing offers.

- Shop lenders individually. You can contact banks, credit unions or online lenders directly, but this usually means submitting your information multiple times.

Ready to compare? See offers from top lenders in minutes.

The most common mortgage refinance options include conventional and government-backed loans (FHA, VA and USDA).

- Rate-and-term refinance loans. Best for lowering your rate, reducing your monthly payment or changing your loan term.

- Cash-out refinance loans. Lets you borrow more than you owe and take the difference in cash. Typically limited to 80% of your home’s value unless you’re eligible for a VA cash-out refinance.

- Streamline refinance loans. A faster option for FHA, VA or USDA loans that may skip appraisals or income verification. You must already have a government-backed loan.

- Jumbo refinance loans. Required for loans above conforming limits. These loans usually have stricter requirements.

Nearly a third of borrowers who took out a mortgage over the last few years stand to save more than $2,000 annually by refinancing their mortgage.

If you closed on a 30-year fixed-rate mortgage between 2023 and 2025, there’s an opportunity for you to get a lower interest rate and potentially shave $193 off your monthly mortgage payments — adding up to $2,320 in savings each year — according to a recent LendingTree analysis. It pays to shop around.

LendingTree picks for the best refinance lenders

| Lender | User ratings | Best for | |

|---|---|---|---|

|

(1455)

Ratings and reviews are from real consumers who have used the lending partner’s services.

| Overall refinance | ||

| User reviews coming soon | Online refinance | ||

|

(952)

Ratings and reviews are from real consumers who have used the lending partner’s services.

| Rate transparency | ||

|

(56126)

Ratings and reviews are from real consumers who have used the lending partner’s services.

| Loan variety |

Best refinance lender overall: Rate

- Diverse loan options, including hard-to-find specialty loans for physicians or for self-employed borrowers

- Approval in as little as one day

- Brick-and-mortar locations in nearly every state

- Must agree to be contacted in order to get personalized rates

- You may have to attend your closing in person (only in some states)

Available refinance products:

- Conventional cash-out refinance

- FHA refinance

- USDA refinance

- VA cash-out refinance

- VA IRRRL

- FHA 203(k) renovation refinance

- Fannie Mae HomeStyle and Freddie Mac Renovation refinances

- VA renovation refinance

Additional loan products:

- Jumbo loans

- Interest-only mortgages

- Home equity loans

Founded in 2000, Rate (formerly known as Guaranteed Rate) is a mortgage lender specializing in a digital mortgage experience. Consumers can check out refinance rates online, find information about Rate’s loan products, or read articles about mortgage lending and an easy online application process. Rate offers seven different refinance programs, including a wide variety of fixer-upper refinance programs.

You’ll have the best chance of qualifying for a mortgage refinance with Rate if you have a 75% loan-to-value (LTV) ratio or better, according to nationwide data from 2024. That year, 43% of refinance borrowers had a debt-to-income (DTI) ratio under 40%.

Best online refi experience from a traditional bank: Chase

- Offers an on-time closing guarantee

- Relationship discounts for existing customers

- Competitive rates and fees

- Doesn’t disclose income or credit requirements

- Home loan advisors aren’t available in all states

- USDA loans aren’t available

Available refinance products:

- Rate-and-term refinance

- Cash-out refinance

- Cash-in refinance

- Streamline refinance

- No-closing-cost refinance

Additional loan products:

- Conventional mortgage loans

- FHA loans

- VA loans

- Jumbo loans

Founded in 1799, JP Mortgage Chase is one of the oldest financial institutions in the United States. Chase mortgage advisors work with customers in 50 states and the District of Columbia. When it comes to refinancing, Chase provides a combination of online product information, mortgage finance articles and rates updated daily on six different products, earning it the best online mortgage experience award for an institutional bank lender.

You’ll have the best chance of qualifying for a mortgage refinance with Chase if you have a 60% loan-to-value (LTV) ratio or better, according to nationwide data from 2024. That year, about 63% of refinance borrowers had a debt-to-income (DTI) ratio below 40%.

Best for online refi rate transparency: Zillow Home Loans

- A wide selection of purchase and refinance mortgage loans

- Offers online mortgage prequalification with no impact to your credit score

- Available in most states

- Limited rate and fee information on Zillow’s website

- Online loan applications still require speaking with a loan officer

- Not available in New York

Available refinance products:

- Rate-and-term refinance

- Cash-out refinance

- Streamline refinance

Additional loan products:

- Conventional mortgage loans

- FHA loans

- VA loans

- Jumbo loans

- HELOCs

Zillow is probably best known for its home shopping platform, but the company also launched Zillow Home Loans in 2019 to give aspiring homeowners a place to go mortgage shopping as well. Zillow offers a solid menu of refinance types but especially shines when it comes to the amount of online mortgage rate information it offers. Consumers can track rates for conventional, FHA and VA fixed-rate loans and even peruse a number of adjustable-rate mortgage (ARM) rates with initial rates that are fixed for seven years.

You’ll have the best chance of qualifying for a mortgage refinance with Zillow if you have a 72% loan-to-value (LTV) ratio or better, according to nationwide data from 2024. That year, about 59% of refinance borrowers had a debt-to-income (DTI) ratio below 40%.

Best for variety of refi products: Fairway Independent Mortgage

- More loan options than other lenders, including renovation loans and super-jumbo loans

- Brick-and-mortar locations in most states

- Low application denial rates

- Doesn’t publish rates or fees online

- Higher fees than many competitors

- Doesn’t offer home equity loans or HELOCs

Available refinance products:

- Conventional mortgage loans

- FHA loans

- VA loans

- Jumbo loans

- USDA loans

- Fixer-upper loans (including the FHA 203(k) program, Fannie Mae HomeStyle® Renovation loans and VA and USDA renovation loans)

Additional loan products:

- Interest-only mortgages

- Reverse mortgages

- Physician home loans

Fairway Independent Mortgage Corp. has more than 25 years of experience originating loans and currently offers home loans in all 50 states. In addition to most of the standard conventional and government-backed refinance home loans, it also offers refinance loans for borrowers with mortgages currently backed by the U.S. Department of Agriculture (USDA). It also has the widest array of renovation loans of the lenders we reviewed, including a USDA renovation refinance product.

You’ll have the best chance of qualifying for a mortgage refinance with Fairway if you have a 75% loan-to-value (LTV) ratio or better, according to nationwide data from 2024. That year, nearly half (49%) of refinance borrowers had a debt-to-income (DTI) ratio under 40%.

Read more about how we chose our picks for the best refinance lenders.

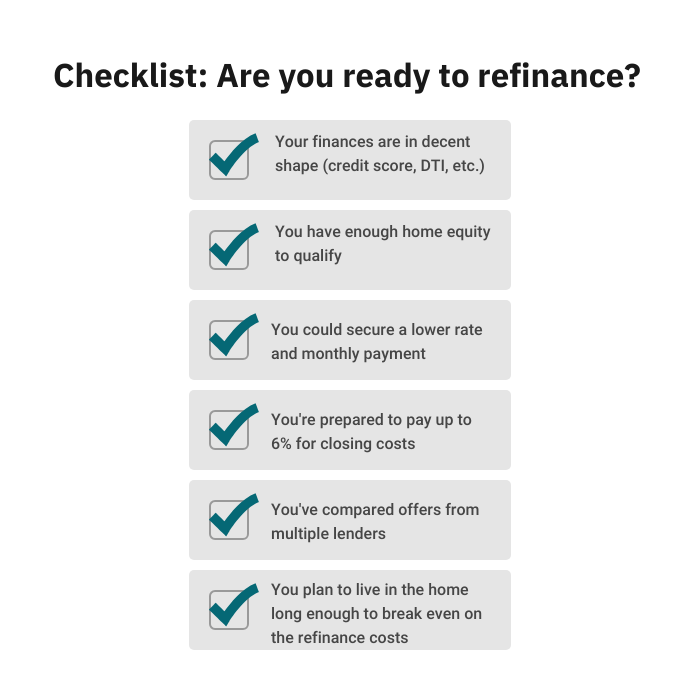

Should you refinance your mortgage right now?

Unless your current mortgage rate is near or above 6.87%, refinancing may not make sense right now. There are a few exceptions that may be worth considering, though:

- You want to switch to a longer loan term to lower your monthly payment (like a 15-year mortgage to a 30-year mortgage)

- You want to access cash through a cash-out refinance

- You need funds for home repairs or renovations (can be an affordable way to manage fixer-upper projects)

- You want to remove mortgage insurance after building enough equity

Refinancing typically comes with closing costs (about 2% to 5% of your loan). To decide if it’s worth it, calculate your break-even point — how long it takes your monthly savings to cover those upfront costs.

If you bought your home a couple of years ago when rates were at their recent peak, it’s possible that today’s rates are low enough to make refinancing worth it. Shopping around and comparing lenders’ rates is key.

Ready to see what you qualify for? Compare offers from multiple lenders in minutes.

How to get the best refinance mortgage rates

-

Shop and compare lenders

Comparing multiple lenders can make a big difference. LendingTree data shows borrowers may save more than $62,000 in interest over the life of a 30-year loan by shopping around. -

Improve your credit

Higher credit scores typically qualify for lower rates. Focus on paying down balances, fixing errors and making on-time payments. -

Consider paying for points

One mortgage point costs 1% of your loan and can lower your rate by about 0.25%. Make sure you’ll break even before paying upfront. (Your break-even point is a measure of how long it takes to recoup your refinance closing costs.) -

Compare APRs and interest rates

Lenders must disclose your annual percentage rate (APR) and your interest rate. A low rate may sound good at first, but if it comes with high fees, it may not actually offer you the best value. The APR reflects the total cost of the loan and is often a better comparison tool. -

Avoid second mortgages if possible

Second mortgages, like a home equity loan or home equity line of credit (HELOC), often have higher rates. A cash-out refinance may offer a lower-cost way to access cash.

See LendingTree’s full guide on how to improve your credit score.

What factors affect my refinance mortgage rate?

While lenders calculate rates differently, these factors have the biggest impact:

Credit score

Higher credit scores typically qualify for lower rates, though you may still be approved with a lower score.

Loan-to-value (LTV) ratio

The less you borrow compared to your home’s value, the lower your risk and often your rate.

Learn more about loan-to-value ratios.

Debt-to-income (DTI) ratio

Lenders compare your monthly debts to your income. A lower DTI ratio (typically 35% or lower) can help you secure better rates.

Learn more about debt-to-income ratios.

Loan term

Longer-term loans (like 30-year mortgages) usually have higher rates than shorter-term loans.

You’ll usually need an appraisal to confirm your home’s value and loan amount. However, some programs, like FHA, VA and USDA streamline refinances, may let you skip it if you qualify.

What if your appraisal comes in low? A low appraisal can affect your refinance, but you may still have options like lowering your loan amount, disputing the appraisal or using a streamline program.

Does a messy house affect your appraisal? Not directly, but appraisers need access to all areas of your home. Keeping your home clean and accessible can help avoid delays.

Mortgage rate news: Are refinance rates going to drop in July?

According to our expert’s mortgage rate predictions, both purchase and refinance rates will remain elevated compared to where they sat before the pandemic.

Here are the U.S. weekly average rates from the Freddie Mac Primary Mortgage Market Survey, as of July 24, 2026:

- 30-year fixed-rate mortgage: 6.58% (↑ 0.03 from last week)

- 15-year fixed-rate mortgage: 5.96% (↑ 0.03 from last week)

At their most recent meeting, the Federal Reserve held the federal funds rate steady. The next Fed meeting is scheduled for July 28 to29.

What this means: Rates may fluctuate week to week, but significant drops are unlikely in the short-term. Many homeowners choose to refinance when they can lower their rate by about 0.50% or more.

Refinance mortgage rates tend to be slightly higher than purchase mortgage rates. However, your quoted rate will depend on your credit score and the refinance type you’re applying for (cash-out vs. rate-and-term).

Frequently asked questions

A good rule of thumb is to wait until you can reduce your current rate by at least 50 basis points. That said, if you need to refinance for other reasons — like removing someone’s name from a mortgage or switching to a fixed-rate mortgage — it can still be worth considering. If you need guidance, reach out to a loan officer or housing counselor.

Refinance rates are usually higher than purchase mortgage rates because lenders view refinancing as a higher risk, especially for cash-out refinances that increase the loan amount.

The table below gives you a quick glance at the refinance requirements for credit score, DTI ratio and LTV ratio for common refinance loan types.

| Loan program | Refinance purpose | Credit score | LTV ratio | DTI ratio |

|---|---|---|---|---|

| Conventional | Rate and term | 620 | 97% | 45% to 50% |

| Cash out | 620 | 80% | 45% to 50% | |

| FHA | Rate and term | 500 to 580 | 97.75% | 43% |

| Cash out | 500 | 80% | 43% | |

| Streamline | N/A | N/A | N/A | |

| VA | Rate and term | No minimum, but lenders typically require 620 | 100% | 41% |

| Cash out | No minimum | 90% | 41% | |

| Streamline | No minimum | N/A | N/A | |

| USDA | Streamline | N/A | N/A | N/A |

Common reasons borrowers are disqualified from refinancing include having a low credit score, unstable income or insufficient home equity.

How we chose our picks for the best refinance lenders

We reviewed more than 40 lenders to determine the overall best refinance lenders. LendingTree reviews and fact-checks our top lender picks annually by gathering loan program and requirement details directly from lenders and analyzing data from the Home Mortgage Disclosure Act (HMDA) government database.

We review five key factors: loan programs offered, digital application availability and ease of use, product and lending information accessibility, in-person branch footprint and LendingTree’s expert star rating.

LendingTree best lender categories

LendingTree experts considered the range of loan programs offered by each individual lender. This ensures the lender offers a variety of options to users for their chosen loan type so customers can choose the best loan for them.

The loan types assessed by LendingTree were:

To be considered as a potential best lender pick by LendingTree experts, the lender must provide users with an online loan application experience that is relatively easy to follow and complete.

This means the lender must provide a user-friendly website and make their customer service contact information easy to find online.

To qualify for “best lender” consideration by LendingTree experts, the lender must provide users with an online experience that helps borrowers make sense of the mortgage lending process.

This means the lender must provide free online learning materials to help homebuyers understand the lender’s offered products, basic loan qualification requirements and high-level rates information.

Lenders must offer mortgages in at least 35 states across the U.S. to be considered a best lender pick. This allows a wider range of users to potentially choose the lender for their home loan, improving accessibility when customers need to contact the lender or get a rate quote.

For lenders to qualify for consideration as a best lender pick, they must have at least a four-star lender review rating from LendingTree experts. This rating indicates that the lender meets most — if not all — of the five criteria considered when assigning ratings. Here is the LendingTree star rating system for this year:

- Publishes rates online (+1 star)

- Offers standard mortgage products (+1 star)

- Includes detailed product info online (+1 star)

- Shares resources about mortgage lending (+1 star)

- Provides an online application (+1 star)

LendingTree mortgage experts’ process for choosing the best lenders

LendingTree gathers data directly from lenders through their websites, disclosures and, in some cases, direct communication with company representatives. Lenders that clearly present product details and terms are viewed more favorably in our evaluation.

The LendingTree editorial team applies consistent criteria to every lender. We also verify and update information periodically. Lenders cannot pay to influence our ratings. Read LendingTree’s editorial guidelines for more information.

Why trust LendingTree’s methodology?

As the lead editor for all purchase, refinance and home equity content, I rely on my 14+ years of personal finance experience to manage a team of staff writers and contributors who create consumer-friendly guides.

Together, our team aims to make LendingTree a reliable and helpful resource for readers as they navigate the complex mortgage lending process.