Cash-Out Refinance: How It Works and When To Do It

A cash-out refinance allows you to swap your current mortgage for a new one and convert some of your home equity to cash at the same time.

When used wisely, a cash-out refinance can be a smart way to make progress toward your financial goals, like consolidating high-interest debt or remodeling your kitchen. We’ll break down when a cash-out refinance makes sense, how much it really costs and what alternatives may work better in today’s rate environment.

- A cash-out refinance involves borrowing more than you currently owe on your existing mortgage.

- Cash-out refinance requirements are stricter than for a traditional mortgage refinance and often come with higher monthly payments. In most cases, you’ll need at least 20% home equity to qualify.

- A cash-out refi can be a better option than a personal loan, since it often has a lower interest rate and doesn’t require an additional monthly payment.

Is a cash-out refinance actually worth it?

A cash-out refinance usually makes the most financial sense when the interest savings or other financial benefits outweigh the additional long-term mortgage costs.

Good fit scenarios:

- You’re consolidating high-interest debt

- You’re funding renovations that increase your home’s value

- You want to replace a HELOC with a more predictable loan option

- You’re lowering your total monthly obligations

Bad fit scenarios:

- You’re using it to fund short-term, non-essential or luxury purchases

- Your current mortgage has a very low interest rate

- You’re close to retirement and need lower monthly costs, housing stability or a nest egg of home equity

How does a cash-out refinance work?

For the most part, a cash-out refinance works like any other home loan.

You shop for a mortgage lender, fill out a loan application and qualify based on your credit score, income and assets. You can use a cash-out refinance payout for whatever you want, including renovating your home, paying off debt and covering higher education costs.

However, there are a few extra considerations:

- You must qualify for a higher loan amount. Because you’re taking out a new loan for more than you currently owe, your lender will need to verify your ability to afford the larger loan amount and higher monthly payment.

- You’ll pay for a home appraisal. Until you complete a refinance home appraisal, your cash-out refi loan amount is just an estimate. If your appraisal comes back lower than expected, you may not qualify to borrow as much home equity as you’d hoped.

- Your lender finalizes your cash-out refinance loan amount. Once your appraisal comes back, the lender calculates your cash-out amount by subtracting your current loan balance from the final loan amount.

- Your old loan is paid off and you receive the rest of the money in cash. Once you review your closing disclosure to confirm the final figures and sign your closing paperwork, your lender will fund your loan. Your old mortgage is paid off, the new mortgage is secured by your home and a wire or check is sent to you.

How much can you borrow with a cash-out refinance?

The amount you can get from a cash-out refinance depends on various factors, the most important of which is your home equity. Lenders calculate your home equity by subtracting your loan balance from your home’s appraised value.

They also limit how much you can cash out by setting loan-to-value (LTV) ratio requirements. Most lenders set an 80% LTV limit, meaning you can borrow up to 80% of your home’s value — minus your outstanding mortgage balance.

Use LendingTree’s cash-out refinance calculator to estimate your monthly payments and the amount of cash you could walk away with. To get started, you’ll need to:

- Enter your home value. A home value estimator can help you get a rough idea of how much your home is worth.

- Put in your current mortgage balance. You can find this on your most recent mortgage statement.

- Add the amount of cash you’d like to take out. If you enter too large an amount, the calculator will let you know.

How to get the best cash-out refinance rates

Cash-out refinance mortgage rates are generally higher than those on regular refinances. Here are four steps you can take to get the best refinance rate:

1. Raise your credit score

Your credit score has a major impact on cash-out refinance rates. Although the minimum requirements are typically lower for FHA loans than conventional loans, your credit score still affects the rate you’ll receive.

Paying off credit card balances and avoiding new credit accounts can help you improve your credit score. The extra effort could save you thousands of dollars in interest charges over a 30-year loan term.

2. Borrow less money

Your LTV ratio, which measures how much you’re borrowing compared to your home’s value, is another factor that impacts your cash-out refinance rate. The higher your LTV ratio, the higher your rate will typically be.

One way to borrow less money is by paying down your mortgage principal with a lump sum before refinancing. This can also help make your mortgage payments more affordable.

3. Make home improvements

The right home improvements could increase your home’s value, lower your LTV ratio and lead to a lower cash-out refinance rate.

Check the Journal of Light Construction’s most recent Cost vs. Value Report to learn which improvements give you the best return on every dollar you invest.

4. Shop around for lender offers

You can save serious money by comparing multiple refinance offers before making your final decision. On average, borrowers can save about $80,000 over the course of a 30-year, fixed-rate mortgage by shopping around, according to LendingTree data.

Collect loan estimates from three to five lenders or use an online comparison site and compare the annual percentage rates (APRs) and interest rates to find your best offer. The best cash-out refinance lenders will offer competitive rates, transparent fee structures and streamlined application processes.

Get started by checking out LendingTree’s list of the best refinance lenders, or enter your info into the rate table below.

Cash-out refinance requirements

| Conventional cash-out refinance | FHA cash-out refinance | VA cash-out refinance | |

|---|---|---|---|

| Maximum LTV ratio | 80% | 80% | 100% |

| Minimum credit score | 660 to 700 | 500 | No minimum (but many lenders require 620) |

| Maximum DTI ratio | 45% (can be exceeded with cash reserves) | 43% | No hard limit, but DTIs above 41% receive additional scrutiny |

| Waiting period | 12 months after closing | 12 months after closing | 210 days (about seven months) after your first monthly payment’s due date |

| Occupancy | Primary residence, second home or investment property | Primary residence only | Primary residence only |

| Loan limits | Total loan amount after refinancing must stay within conforming loan limits | Total loan amount after refinancing must stay within FHA loan limits | No set limit |

While you can get a cash-out refinance with a lower credit score, it’s typically more challenging and comes with higher costs. It’s likely easier for borrowers with bad credit to qualify for government-backed cash-out refinance loans, such as FHA or VA loans, versus conventional loans.

Cash out refinance closing costs

Refinance closing costs typically range from 2% to 5% of your loan amount.

You’ll pay the same types of fees for a cash-out refinance as for a purchase mortgage, including origination, title, appraisal and credit report costs.

You can pay cash-out refinance closing costs out of pocket or request the lender deduct them from your payout. Some companies offer no-closing-cost refinance options if you accept a higher interest rate in exchange for having your lender pay your costs.

Even after you’ve paid your closing costs, each loan program comes with its own ongoing fees:

- Conventional cash-out refinances typically don’t require private mortgage insurance (PMI)

- FHA cash-out refinances come with required FHA mortgage insurance payments regardless of your LTV ratio.

- VA cash-out refinances don’t require mortgage insurance, but you’ll have to pay the VA funding fee of 0.50% to 3.30% of the loan amount.

Cash-out refinance pros and cons

Pros

- Flexibility. You can use the funds for any purpose, including consolidating debt, investing in real estate or starting a business.

- Low interest rates. Mortgages typically have lower interest rates than credit cards, personal loans and home equity loans.

- One monthly payment. Since a cash-out refinance replaces your current mortgage, you won’t have to worry about extra monthly payments like you would with a second mortgage, such as a home equity loan.

Cons

- Minimum 20% equity required. If home values have tumbled in your area or you bought your home with a small down payment, a cash-out refinance may not be possible, at least not right now.

- Loss of equity. Borrowing against your home equity now may mean a smaller profit when you sell your home later.

- Higher payments. In most cases, a higher loan amount will mean a higher monthly mortgage payment for as long as you own your home.

- Closing costs. You’ll need to pay various closing costs to get a cash-out refinance loan, including origination and appraisal fees.

Cash-out refinance alternatives

| A cash-out refinance makes sense if: | A HELOC makes sense if: | A home equity loan makes sense if: |

|---|---|---|

|

|

|

Cash-out refinance vs. HELOC

A home equity line of credit (HELOC) is an alternative way to access cash that’s secured by your home. HELOCs work a lot like a credit card: You use the funds up to a set limit and pay off those charges as you go.

One advantage of HELOCs is that most lenders allow you to borrow up to 85% of your home’s value. Some HELOC lenders will even lend up to 100% — much more than the 80% cap on most cash-out refinances.

See current HELOC rates.

Cash-out refinance vs. home equity loan

Another equity-tapping option is a home equity loan, which provides access to funds secured against a portion of your home’s equity. You’ll receive all the funds at once and repay the loan on a fixed payment schedule. Terms often range from five to 30 years.

Like HELOCs, home equity lenders may set LTV ratio limits up to 100%, though most keep the maximum at 85%.

Explore current home equity loan rates today.

LendingTree’s home equity loan and HELOC calculator can help you estimate how much money you can qualify for based on your home’s value and your outstanding mortgage balance.

Compare rates for a cash-out refinance vs. home equity products

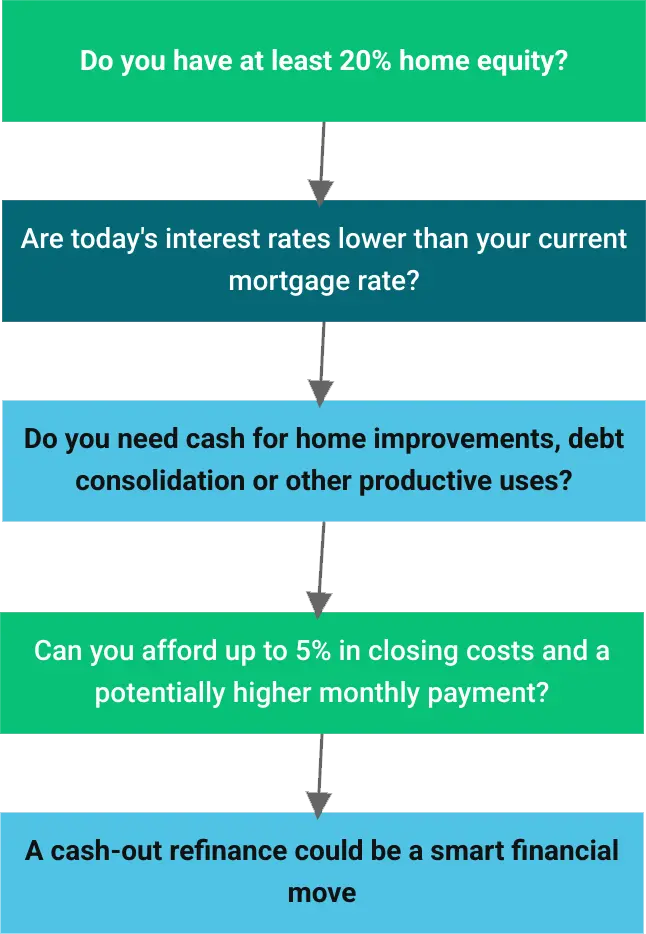

Is a cash-out refinance a good idea?

Whether a cash-out refinance is a good option depends on your financial situation and how you plan to use the funds. Use the flowchart below to find out if a cash-out refi could be the right choice for you.

I took out a cash-out refinance in 2021 to build a fence around my property, buy a shed and make general home improvements. For me, a cash-out refinance was a win-win. I got easy access to the cash I needed and qualified for a lower rate on my mortgage.

Frequently asked questions

How soon you can refinance after buying a house depends on your loan type. While some loans allow you to refinance at any time, others enforce waiting periods, and the waiting periods are often longer for cash-out refinances. For example, you can do a rate-and-term refinance with a conventional loan at any time, while a cash-out refinance requires a 12-month waiting period.

The IRS doesn’t consider cash from a cash-out refinance taxable income. This is because it’s considered a loan, not income.

Yes, if you qualify, you can get a cash-out refinance secured by an investment property. However, you’ll be limited to a lower LTV ratio and should expect a higher interest rate. Lenders limit the LTV ratio for cash-out refinances on investment properties to 70%, and to 75% for second homes.

Cash-out refinance rates are typically higher than traditional refinance rates. This is because lenders consider cash-out refinances to be a riskier mortgage product. However, your specific rate will depend on various factors, including your financial situation and market conditions.

Yes, FHA cash-out refinances are legitimate loan products insured by the Federal Housing Administration (FHA).