What Is a Good Credit Score to Buy a House?

A 500 to 620 credit score is enough to buy a house in many cases, but it may not be enough to get the best mortgage rate.

The difference between a 620 and 780 score can mean paying hundreds more each month or not being able to qualify for a home in a slightly higher price range. Here’s what credit score you need for each mortgage type and how your score affects what you can afford.

Key takeaways

| Your goal | Credit score you’ll need |

|---|---|

| Buy a house with FHA financing | 500 to 580 |

| Buy a house with a conventional loan | 620 |

| Get competitive mortgage rates | 680 |

| Get the best rates available | 780 |

What is a good credit score to buy a house?

A 620 credit score is generally considered good enough to buy a house because it qualifies you for most common mortgage loan programs. However, the best credit score for buying a house is usually 780 or higher, since borrowers in that range often receive the lowest mortgage rates and monthly payments.

What is the minimum credit score to buy a house?

There is no true minimum score to buy a home, since most loan programs have the flexibility to go below their listed or typical floors, and will work with borrowers with no credit history. That said, the guideline minimums for each program are:

- Conventional loans: 620

- FHA loans: 500 to 580

- VA loans: 620

- USDA loans: 640

What different credit scores mean for homebuyers

| Credit score | What to expect when buying a house |

|---|---|

| 780+ | You may qualify for the lowest available rates |

| 740-779 | You’ll likely qualify for very good mortgage rates |

| 680-739 | You’ll have competitive rates and loan options |

| 620-679 | You’re eligible for many conventional loans |

| 580-619 | You’ll likely qualify for FHA financing with a low (3.5%) down payment or a VA loan, but rates may be higher |

| 500-579 | You may qualify for an FHA loan with a larger (10%) down payment or a VA loan |

| No credit | You may still be able to qualify for all of the traditional mortgage loan programs — conventional, FHA, VA and USDA — but could have to undergo extra scrutiny, show that you have mortgage reserves or go through manual underwriting. |

Keep in mind that qualification is only part of the equation. Your credit score also affects your interest rate, monthly payment and the amount of house you can afford. Even a small improvement in your score could save you hundreds of dollars each month.

Don’t know your credit score? Get your free score on LendingTree Spring today.

There are several types of credit scoring formulas, but most lenders use the FICO scoring system. The FICO credit score ranges are as follows:

- 300 to 579 (Poor)

- 580 to 669 (Fair)

- 670 to 739 (Good)

- 740 to 799 (Very good)

- 800+ (Exceptional)

The FICO Score is calculated using an algorithm based on your payment history, how you manage credit and the mix of different accounts you have. Learn more about what affects your credit score.

How much a higher credit score can save you

| Credit score | Average mortgage rate | Monthly payment |

|---|---|---|

| 620 | 7.21% | $1,903 |

| 640 | 7.06% | $1,874 |

| 660 | 6.94% | $1,852 |

| 680 | 6.87% | $1,838 |

| 700 | 6.76% | $1,818 |

| 720 | 6.71% | $1,809 |

| 740 | 6.58% | $1,785 |

| 760 | 6.51% | $1,772 |

| 780 | 6.42% | $1,755 |

| 800 | 6.42% | $1,755 |

| 820 | 6.42% | $1,755 |

| 840 | 6.42% | $1,755 |

3 ways a good credit score helps you buy a house

Besides a lower interest rate and monthly payment, there are some added benefits to buying a home with a higher credit score, including:

1. You can get approved with more total debt

Although on paper many lending programs cap your debt-to-income (DTI) ratio at 43% to 45%, a high credit score or other strong financial factors may allow exceptions above 50%. This means you could get approved for a mortgage even with a larger amount of debt.

2. You can reduce mortgage insurance costs

If you can’t quite swing a 20% down payment, you can at least minimize your monthly private mortgage insurance (PMI) costs (on a conventional loan) with a high credit score. PMI is usually part of your monthly payment.

3. You can afford a more expensive home

Your credit score affects both your interest rate and mortgage payment, so it has an impact on how much house you can afford. Try our home affordability calculator to see the difference a few percentage points can make on the home price you can qualify to purchase.

The example in the table below shows these numbers in action as we compare the interest rate, monthly payment and maximum home price you can afford with a higher and lower conventional credit score. The example also assumes you earn $85,000 per year and make a 3% down payment.

| Credit score | Interest rate | Monthly payment* | Maximum home price** |

|---|---|---|---|

| 780 | 6.42% | $3,243 | $395,494 |

| 620 | 7.21% | $3,231 | $371,407 |

**Assumes a maximum 43% DTI ratio.

The bottom line: A lower credit score reduces your homebuying power by $24,087 in this example.

What affects your credit score?

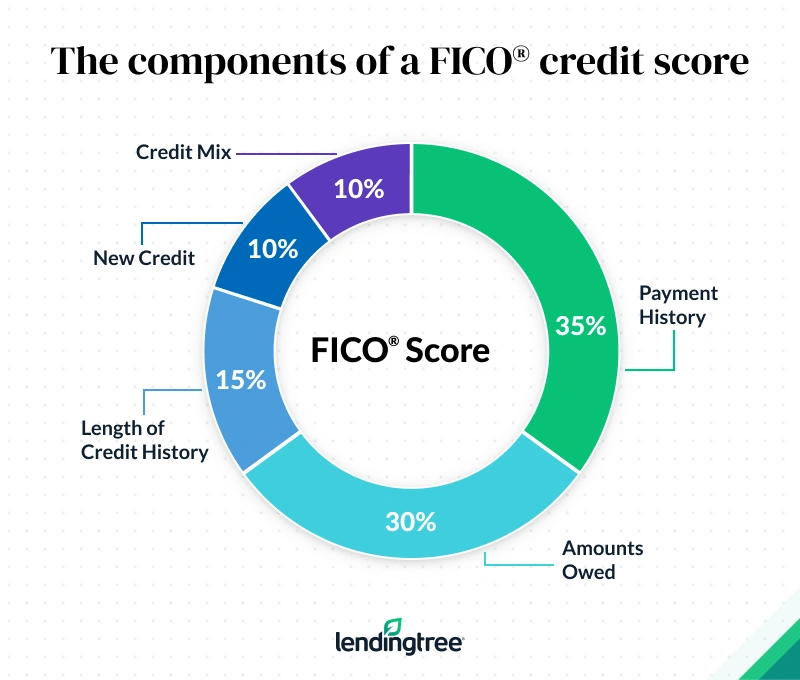

The image below shows the components of your credit score. As you can see, payment history and amounts owed have the biggest impact, followed by length of credit history, new credit and the mix of credit accounts you have.

Learn more about the factors that make up your credit score.

To calculate your score, mortgage lenders typically pull your credit history from all three of the main credit reporting bureaus: Equifax, Experian and TransUnion. Then, they use the middle score to quote you a rate and approve your loan. You can get a free credit report from each credit reporting agency weekly. However, a mortgage credit report, obtained when applying with a lender, will give you a better idea of where you stand as a potential homebuyer.

How to increase your credit score before house hunting

If your eyes are set on homebuying, here are some things you can do now to boost your credit score:

- Shrink your credit card balances. As a general rule, avoid using more than 30% of your total available credit to maximize your score. For example, if you have $2,500 debt out of a $10,000 limit, you’re utilizing 25%.

- Pay your bills on time. Even one recent late payment on a credit card or loan can drastically drop your score.

- Avoid authorized user cards. You’re responsible for charges as a primary cardholder. If an authorized user racks up a large amount of debt on the card and can’t pay it off, your credit score will suffer.

- Don’t cosign on debt. Whether it’s a student loan or a car lease, your credit score could take a hit if a cosigned account is paid late, even if you’re not the primary borrower.

- Don’t open up new credit cards or take out new loans. Limit new credit applications within a year of applying for a mortgage to maximize your credit score and avoid extra scrutiny from your lender.

- Fix errors if you find them. Your credit report may have errors, such as incorrect late payments, that you can fix by filing a dispute with the credit bureaus.

Generally, yes. It’s best to avoid applying for or opening new credit accounts while you’re shopping for a mortgage. A single credit card application will usually have only a small impact on your credit score, but it’s in your best interest to apply for a mortgage with the highest score possible.

It’s especially important not to open a new credit card after you’ve applied for a mortgage. If your score drops or your debt profile changes during underwriting, it could delay your approval, affect your loan terms or even jeopardize your closing.

How to buy a house with bad credit

There are some steps that may help improve your odds of buying a house with a low credit score.

Make a larger down payment

Lenders may be more willing to consider a loan application from a buyer with a poor credit score if you’re making more than the minimum down payment. Consider asking a relative for a gift, and stockpile those tax refunds and bonuses to build your down payment fund.

Pay down your debt

Another way to offset low credit scores is to get rid of as much debt as possible. Mortgage underwriters may look more favorably on an application with a very low DTI ratio, even if your credit history has some bumps in it.

Consider non-QM mortgages

Non-qualified mortgages, more commonly known as non-QM loans, don’t have to meet the stringent federal standards tied to common loan programs. Some non-QM loans even allow you to get a loan one day after completing a bankruptcy or foreclosure, as long as you have a large down payment and can afford a higher interest rate.

View mortgage loan offers from up to 5 lenders in minutes