LendingTree Money Insights: Trusted Advice From Our Experts

Rising gas prices are already changing how Americans spend or save — and many more are bracing to adapt

Published March 24, 2026

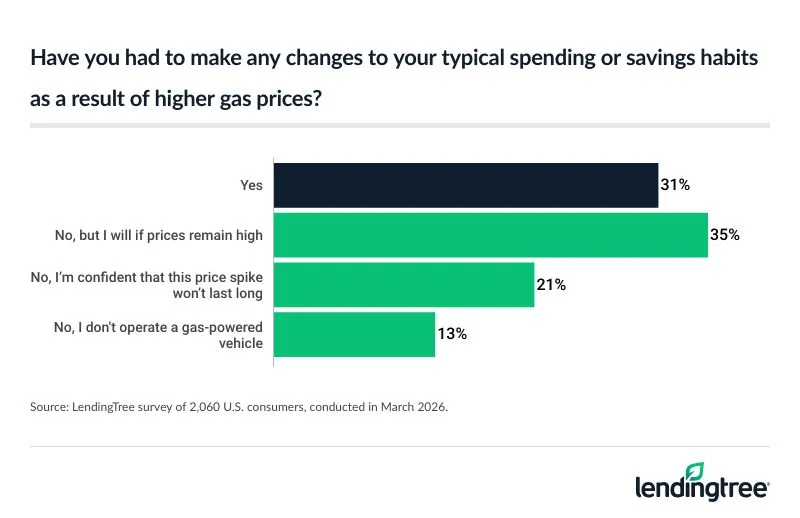

Almost a third of Americans say they’ve made changes to their typical spending or savings habits as a result of higher gas prices, and another 35% say they will do so if prices remain high.

LendingTree surveyed 2,060 consumers, including 1,799 who operate a gas-powered vehicle, about the impact of rising gas prices on their personal finances. Though the conflict with Iran and the ensuing spike in gas prices are less than a month old, our survey — conducted from March 17 to 23 — clearly shows that American families are already feeling the effects.

Here’s what we found.

The conflict began on Feb. 28, 2026. According to AAA, the average price of a regular gallon of gas that week was $2.98. Our survey started fielding less than three weeks later, on March 17, 2026, when the average price of a gallon of regular gas was $3.79. By March 23, 2026, the final day of the survey, gas prices had risen further, reaching $3.96.

Key findings

- Higher gas prices are already spurring Americans to change their behavior. About a third of Americans (31%) have made changes to their spending or savings habits because of higher gas prices, while another 35% say they will if prices remain high. Just 21% say they’re confident the spike won’t last long.

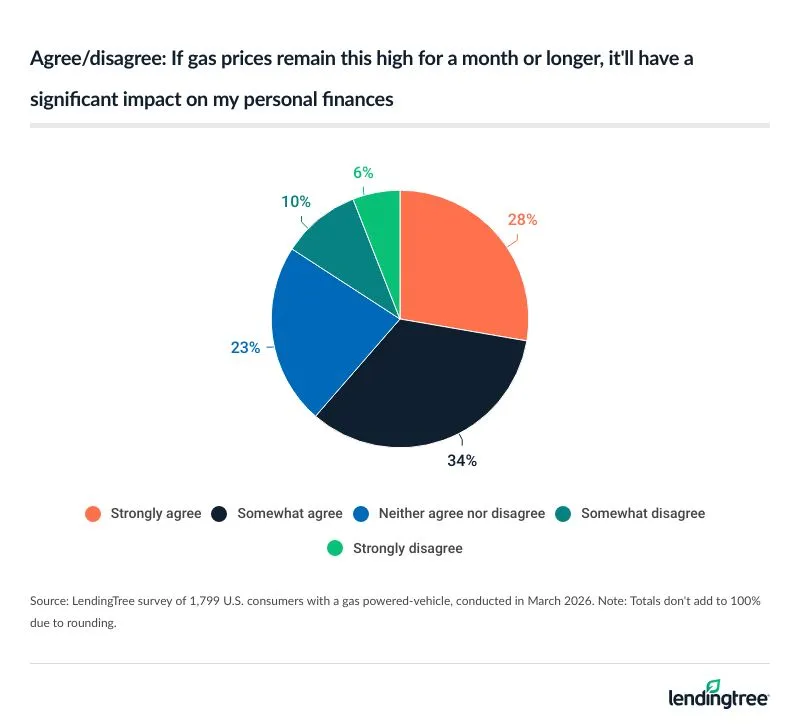

- 62% of Americans with a gas-powered vehicle agree that if gas prices remain high for a month or longer, it’ll have a significant impact on their personal finances. That includes 28% who strongly agree. Parents of young kids (73%) and millennials (71%) are the most likely to agree. The lower your income, the more likely you are to agree.

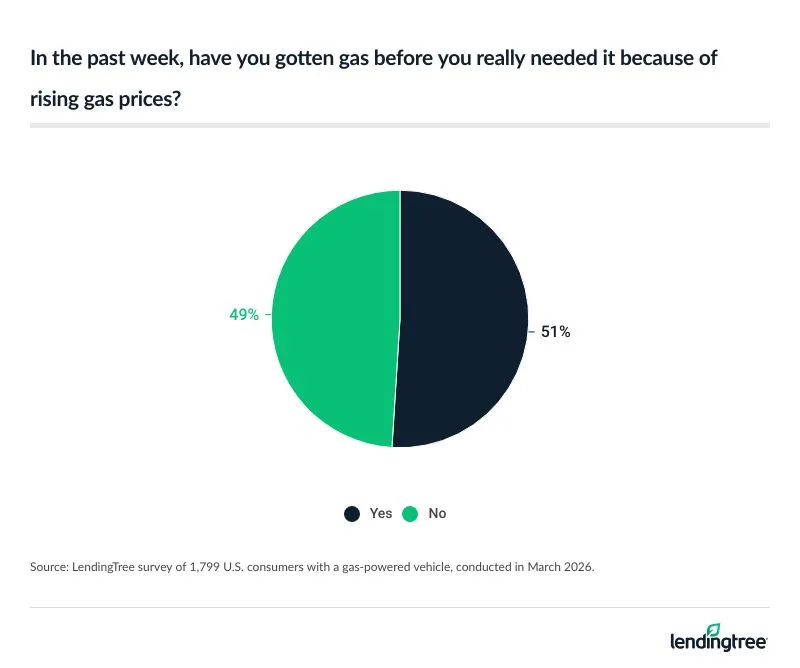

- Americans are trying to get ahead of rising gas prices. At the time of our survey, 51% of consumers with a gas-powered vehicle said they’ve gotten gas in the past week before they needed it because of rising prices. Parents of young kids and Gen Zers are the most likely to have done so.

Higher gas prices are already spurring changes in spending and savings

Nearly 1 in 3 Americans (31%) say they’ve already changed their spending or savings habits because of the gas price spike, while 35% more say they haven’t changed yet but will if prices remain high. Another 21% say they haven’t changed their habits and are confident the spike won’t last long, while 13% don’t operate a gas-powered vehicle.

Parents with kids younger than 18 (46%) and millennials ages 30 to 45 (38%) are most likely to have already changed their spending or savings habits because of high prices. Republicans (35%) are more likely than Democrats (31%) and independents (30%) to say they’ve already made changes.If high gas prices linger, Americans say the impact on their personal finances will be significant

While only about a third of Americans say they’ve already made changes because of rising gas prices, there’s far more agreement on what would happen if high prices linger. More than 6 in 10 (62%) Americans with a gas-powered vehicle agree that if gas prices remain high for a month or longer, this would significantly affect their personal finances. That 62% figure includes 28% who say they strongly agree.

Some highlights:

- Parents of young kids (73%) and millennials (71%) are the most likely to agree

- The lower your income, the more likely you are to agree

- 69% of Democrats agree, compared with 63% of Republicans and 54% of independents

Half of Americans have tried to get ahead of rising gas prices

Having seen gas prices continue to climb, Americans aren’t sitting idly by. At the time of our survey, slightly more than half of Americans (51%) with a gas-powered vehicle said they’ve gotten gas in the past week before they needed it because of rising prices.

Parents of young kids (65%), Gen Zers ages 18 to 29 (61%), six-figure earners (59%), millennials (58%) and Democrats (56%) are the most likely to have done so.

Tips for managing high gas prices

It’s easy to feel powerless as you watch gas prices continue to climb. However, there are things that you can do to help yourself. As mentioned earlier, opting to fill up your tank a little earlier than you might have otherwise can help. Here are a few other possibilities.

- Shop around. This is almost always good advice. We can often be creatures of habit when it comes to filling up our vehicle, but that habit can be costly. Taking the time to compare costs in your area with tools like GasBuddy makes a lot of sense because there can be real price differences. That doesn’t mean you need to drive across town to save a nickel a gallon. It just means that it can be wise to leave your options open.

- Consider a credit card with gas rewards. The right credit card can save you real money at the pump. Depending on your particular driving and spending habits, either a general-purpose card that gives extra rewards for gas purchases or a gas-station-branded card can be a strong choice. However, there’s a big caveat: You should only get a gas-station-branded credit card if you’re confident that you’ll be able to pay your bill in full each month. These cards can have higher-than-normal APRs, some above 30%, so if you carry a balance, any rewards and gas discounts you get will quickly be outweighed by the interest you pay.

- Budget for it. If higher gas prices are hitting you hard, revisit your budget to allow for that extra cost. The best budgets are living, breathing, malleable documents that can be tweaked on an ongoing basis to handle shifting priorities, short-term price spikes and other unexpected events without putting yourself in too deep a hole.

- Share a ride. From carpooling to using public transportation, there are often ways to use your vehicle less than you do today. They may not be ideal solutions, but if gas prices are putting you in a bind, they may certainly be worth considering.

Methodology

LendingTree commissioned QuestionPro to conduct an online survey of 2,060 U.S. consumers ages 18 to 80 on Mar. 17-23, 2026. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. Researchers reviewed all responses for quality control.

We defined generations as the following ages in 2026:

- Generation Z: 18 to 29

- Millennials: 30 to 45

- Generation X: 46 to 61

- Baby boomers: 62 to 80

Matt’s thoughts on March 2026 Fed meeting

Published March 16, 2026

- Anyone hoping for the Federal Reserve to ride in and save them from high interest rates anytime soon is probably going to be disappointed. The Fed is almost certain to leave rates unchanged in March — and again in April — meaning Americans seeking relief will likely have to take matters into their own hands.

- Mortgage rates dipped below 6% briefly, but they’ve climbed again in recent weeks. With global uncertainty, a shaky economic outlook and the Fed’s likely pause on rate cuts, I expect mortgage rates to remain relatively volatile. The good news, however, is that rates have already fallen enough in the past year to make refinancing a real opportunity for many Americans.

-

Credit card rates have fallen for six straight months, but the Fed’s pause on rate cuts could bring that streak to an end. I don’t expect rates to start climbing, though. Credit card rates don’t tend to move much unless forced by the Fed, so I expect that we may see a few months of relative stability in card rates. However, that could all change if the economy takes a turn for the worse.

- Today’s average APR on a new card offer is 23.72%, the lowest since March 2023. That decline is already creating meaningful savings for cardholders. Consider this scenario, with numbers generated using our credit card interest calculator:

- In September 2024, the average new card APR was 24.92%, a record high. At that rate, someone with a $7,000 balance who paid $250 a month would need 42 months and pay $3,594 in interest.

- At today’s 23.72% rate, it would take 41 months and $3,297 in interest. That’s a difference of one month and $297 in interest. That’s a big deal.

- Americans continue to struggle with auto loans, as high prices and high interest rates take a toll. A March 2026 LendingTree analysis found that 1.99% of consumers with recently active auto loans have a default on record. More than 6 in 10 consumers who’ve defaulted on an auto loan have done so on a loan with a term of at least 72 months.

- The rate pause is good news for savers. Rates on certificates of deposit (CDs) and high-yield savings accounts (HYSAs) have fallen from the highs seen a couple of years ago, but rates should stabilize now that the Fed is pausing rate cuts. That makes it a great time to shop for a HYSA if you haven’t before.

- You have more power over rates than you realize — more than a typical Fed rate cut might provide. Shopping around and comparing rates from multiple lenders can save you thousands of dollars on a home or a vehicle, whether you’re buying something new or just refinancing. A 0% balance transfer credit card or a low-interest personal loan can help you dramatically lower how much interest you pay each month. You can even often call your credit card issuer and ask it for a lower rate. It works way more often than you’d imagine.

Below 6%: Why this mortgage milestone matters

Published Feb. 26, 2026

The average rate on a 30-year fixed mortgage fell below 6% for the first time since September 2022, according to Freddie Mac data released on Thursday.

Here’s what LendingTree chief consumer finance analyst Matt Schulz has to say about the decrease.

“This is a big moment. Americans love round numbers, and dropping below the 6% mortgage rate threshold matters psychologically. Now that we’re there, I expect more buyers and homeowners to jump off the sidelines, either to purchase a home or refinance their current loan.

“Yes, rates are still well above the ‘good old days’ of sub-3% mortgages, but they’ve fallen more than a full percentage point since January 2025, and that’s enormous. Even a fraction of a percentage point can mean tens of thousands of dollars over the life of a loan. For homeowners who bought when rates were at their peak, refinancing now could mean meaningful, long-term savings.

“Don’t assume rates will stay below 6%. While the broader trend may be downward, and I think that’ll continue, mortgage rates move constantly based on many factors. We shouldn’t be surprised to see normal volatility push rates back above 6% before they move lower again.

“You have more control over your rate than you think. Simply shopping around can dramatically lower your costs. A June 2025 LendingTree report found that borrowers who compared offers saved an average of $80,024 over the life of a 30-year fixed mortgage. Why? Because the gap between the lowest and highest APR offered on the LendingTree platform was nearly a full percentage point. That’s potentially life-changing money — and proof that shopping around is essential.”

Matt’s thoughts on Q4 2025 New York Fed quarterly debt report

Published Feb. 10, 2026

Here’s what LendingTree chief consumer finance analyst Matt Schulz has to say about the Feb. 10 release of the Federal Reserve Bank of New York’s Quarterly Report on Household Debt and Credit, which is generally considered the gold standard tracker of consumer debt and credit in the U.S.:

- ”Every form of debt the report tracks, except for home equity lines of credit (HELOCs), is at its highest level since the report began in 1999. In the fourth quarter of 2025, overall debt rose for the 22nd straight quarter, and the only time it has fallen since 2014 was in the second quarter of 2020, at the peak of lockdowns during the pandemic.”

- “This debt growth is the K-shaped economy at work. Many Americans are thriving, spending freely and unafraid to take on some debt in pursuit of their goals. Many others are struggling mightily, finding themselves with little choice but to take on more and more debt just to make ends meet. Meanwhile, the overall mountain of debt in America just keeps growing, and there’s little reason to believe it’s going to stop anytime soon.”

- “Credit card debt grew to $1.277 trillion, up 5.5% from last year. Card debt often rises in the fourth quarter, thanks to holiday shopping, leaving people with a big debt mess to clean up at the beginning of the year. This year is no different.”

- “Next quarter’s report on credit card debt will be extremely telling. Card debt usually shrinks in the first quarter, as people focus on paying down their holiday debt. I expect this will happen in 2026 as well. However, given stubborn inflation, high interest rates, a softening job market and other economic uncertainty, that is far from guaranteed. If we don’t see card debt fall next quarter, it will bode very poorly for the rest of 2026.”

- “Mortgage delinquencies continue to rise. Though not high by historical standards, they’re the highest we’ve seen since 2015. That growth is troubling, given that people tend to make mortgage payments their highest priority when it comes to paying bills. If the mortgage bill isn’t getting paid, chances are that other bills may go unpaid as well.”

- “It’s easy to feel hopeless and helpless as you pile on more and more debt. However, you have far more power over your money than you realize. You can use a 0% balance transfer credit card or a debt consolidation loan to tackle credit card debt. You can refinance your home to a lower rate, if possible. You can shop around for better rates and prices when buying your next vehicle. You can even call your credit card issuer and ask for a lower rate on one of your cards. It works way more often than you’d realize, but only if you ask.”

Matt’s thoughts on January 2026 Fed meeting

Published Jan. 26, 2026

Here’s what LendingTree chief consumer finance analyst Matt Schulz — also the author of “Ask Questions, Save Money, Make More: How to Take Control of Your Financial Life” — has to say about the Federal Reserve’s meeting this week, set for Jan. 27-28.

- The Fed is almost certainly hitting pause on rate cuts, which isn’t great news for people dealing with post-holiday debt. Still, rates on several types of loans are at their lowest levels in years and should keep drifting down for a little while longer. That’s a relief at a time when affordability is still a real struggle for many families.

- Mortgage rates keep falling and are now at their lowest point in nearly three years. In the coming months, I expect 30-year, fixed-rate mortgages to dip below 6% for the first time since 2022, which should encourage more people to buy homes or refinance. That said, with today’s unpredictable economy and the way mortgage rates bounce around, I don’t expect sub-6% rates to last for very long.

-

Thanks to earlier Fed cuts, credit card rates are now the lowest they’ve been in almost three years and should continue edging down, at least in the near term.

- The current average rate on a new credit card is 23.79%. That’s the lowest since March 2023 and more than a full percentage point below the record high of 24.92% set in August and September 2024.

- At a 23.79% APR, someone with a $7,000 balance paying $250 a month would pay $3,314 in interest over 41 months before paying it off.

- At 24.92%, that same balance and payment would cost $3,594 in interest over 42 months.

- That’s a difference of one month and $280. Not life-changing, but still meaningful for many households.

- Rates on high-yield savings accounts (HYSAs) are also falling, which isn’t great for savers. Even so, they still pay far more than traditional savings accounts at big banks, and they’re well worth shopping for if you don’t already have one. Even with rates down from their peak, HYSAs remain a strong way to build an emergency fund, save for a down payment or start setting money aside for future expenses. It’s never too early to get started.

Finally, remember that you have more control over your interest rates than you might think. The Fed may not be riding to the rescue anytime soon, but there are still smart moves you can make. A 0% balance transfer card can be a powerful tool for tackling credit card debt. A low-interest personal loan can also help. And don’t underestimate the power of simply calling your card issuer and asking for a lower rate — it works more often than most people expect.

Credit card rate cap proposals usually go nowhere. This one spooked Wall Street.

Published Jan. 12, 2026

Every few years, a politician floats the idea of capping credit card interest rates, generating a lot of headlines before ultimately going nowhere.

This time, however, it feels different.

In a Truth Social post on Friday, President Donald Trump proposed capping credit card interest rates in the U.S. at 10% for one year. (He had previously floated the idea of a permanent cap while on the campaign trail in 2024.) Then, on Sunday, he doubled down, reportedly saying that credit card issuers that don’t cap rates at 10% by Jan. 20 would be “in violation of the law.”

It’s unclear what power the president would have to enact a rate cap of any duration without the help of Congress, and no similar proposal has gained real traction on Capitol Hill in recent years.

However, despite all that, it appears that investors aren’t just shrugging off this proposal the way they have those by politicians on both sides of the aisle over the years. Several credit card issuer stocks were down in early trading on Monday, with many observers attributing the decline to nervousness about a potential credit card rate cap. (Investors may also be reacting to Friday’s news of a federal criminal investigation into Federal Reserve Chair Jerome Powell, but many observers are pointing to the rate cap rather than the Powell case as the primary reason for the dips.)

In years of watching these rate cut proposals come and go, this is the first time I can recall the markets having any significant reaction to one. That tells you that Wall Street is viewing this rate cut proposal differently than the rest, which is noteworthy.

Here are a few key things to know about credit card rate caps.

- When it comes to rate caps, banks have long been adamant that customers should be careful what they wish for. They say that any rate cap would make lenders less likely to extend credit to people with low credit scores because it would be too great a financial risk. They also say it would lead to diminished credit card rewards because credit card issuer profits fuel credit card rewards. The lower the capped rate, the bigger the impact. Some have speculated that at a 10% rate cap, issuers would stop lending to subprime borrowers and that credit card rewards would largely vanish overnight.

- Despite the potential ramifications, rate caps are enormously popular with Americans, and politicians know it. A 2024 LendingTree survey showed that 77% of American credit cardholders support a cap on credit card interest rates. Among those who do, 66% still support a rate cap even if it means reduced rewards, and 60% still support it even if it means restricted access to credit. That’s why we’ve seen big names on both sides of the aisle — from Rep. Alexandria Ocasio-Cortez (D-N.Y.), Sen. Elizabeth Warren (D-Mass.) and Sen. Bernie Sanders (I-Vt.) on the left to Trump and Sen. Josh Hawley (R-Mo.) on the right — propose rate caps. After all, no one’s ever going to get booed at a political rally for attacking credit card companies.

- Credit card rate caps aren’t unheard of in this country. There has been a cap on credit card interest rates for federal credit unions for years. Currently, that cap is set at 18%. However, there has never been a national cap on bank credit cards. There’s no question that it would be a big deal for credit cardholders if it came to pass.

-

The average APR on a new credit card today is 23.79%, nearly two-and-a-half times the maximum rate proposed by Trump. Rates have fallen from a record 24.92% in September 2024 in the wake of cuts by the Federal Reserve, but they’re still sky-high — light-years beyond what the president’s rate cap would allow. Here’s how much interest a cardholder could save by lowering their APR from 23.79% to 10%, using our credit card interest calculator:

- Scenario 1: Typical balance at today’s average APR

- $7,000 balance

- 23.79% APR — the average APR on a new credit card offer in America today

- $250 monthly payment

- 41 months to pay down

- $3,314 in interest

- Scenario 2: Typical balance with a 10% APR

- $7,000 balance

- 10% APR — Trump’s proposed maximum

- $250 monthly payment

- 32 months to pay down

- $1,004 in interest

- The savings: 9 fewer months and $2,310 less in interest

I still think it’s a long shot that any sort of credit card rate cap comes into play. It’s unclear what power the president has to enact a cap, and the opposition is so fierce in the financial services industry that there’s little chance that a cap could pass through Congress — regardless of how popular it might be with Americans.

Still, perhaps the most important thing for credit cardholders to know is this: You have more power over your money than you realize.

You don’t have to wait for a rate cap to lower your card’s interest rates. A 0% balance transfer credit card can help you avoid interest entirely, often for more than a year, and is likely your best tool against card debt. A low-interest personal loan can be great, too. You can even call your credit card issuer and ask it to lower your rate. A 2025 LendingTree survey found that 83% of people who did that in the prior year were successful and the average reduction was about 7.0 percentage points — a substantial cut. I show people how to do this, including word-for-word scripts, in my book, “Ask Questions, Save Money, Make More: How to Take Control of Your Financial Life.” Often, all it takes is a phone call.

Matt’s thoughts on December 2025 Fed meeting

Published Dec. 8, 2025

Here’s what LendingTree chief consumer finance analyst Matt Schulz — author of “Ask Questions, Save Money, Make More: How to Take Control of Your Financial Life” — has to say about this week’s Federal Reserve meeting, set for Dec. 9-10:

- I expect a rate cut of a quarter-point, which would be the third cut of 2025 and the sixth since September 2024. Whether those rate cuts will continue into the new year is anyone’s guess.

- Another Fed rate cut to close an unnervingly uncertain year is good news for borrowers. The accumulated savings from the Fed’s moves are starting to add up to real money.

-

Credit card rates are the lowest they’ve been since April 2023 — and they’re still falling. The reductions could mean hundreds of dollars in savings for debtors. The average APR on a new card offer is 23.96%, still sky-high but well down from last year’s record levels. With a December cut and some card issuers still yet to implement October’s cut, the national average is likely to fall significantly to close 2025 and start 2026. That could lead to $200 to $300 less in interest over the life of a balance than before the Fed started cutting rates in late 2024. Here’s how:

- Before the Fed began cutting rates in late 2024, the average APR on a new card offer was 24.92%. At that rate, someone with a $7,000 balance and $250 monthly payment would take 42 months and $3,594 in interest to pay it off.

- Compare that to today’s average of 23.96% APR. At that rate, it’ll take 41 months and $3,355 in interest to pay off that debt in full — one month and $239 less than it would’ve taken a year ago.

- Drop that APR a quarter-point to 23.71% and the savings go even higher. It’ll still take 41 months, but you’ll only pay $3,295. That’s $299 less than it would’ve cost at the 2024 peak, and that’s real money for those struggling with card debt.

- Mortgage rates continue to hover near the lowest levels in more than a year. While there’s no guarantee that the Fed’s move will push mortgage rates lower, there’s reason to be optimistic that homebuyers could see rates below 6.00% in the next year, even if only briefly. That would likely spur more Americans to refinance their current high-rate mortgages and possibly even to consider shopping for a new home. A LendingTree study from November found that refinancing your home at the lowest rate offered could save some homeowners $50,000 or more over their current mortgage.

- Lower rates stink for savers. Yet another cut means the days of 4.00% or higher returns on high-yield savings accounts may be ending. They’re still worth signing up for, especially compared to traditional savings accounts at megabanks, but these accounts’ record returns are continuing to fade further into memory. Returns continue to shrink on CDs as well, so those in the market should jump in to lock in today’s rates while they can.

- You can maximize your savings by shopping around. There can be significant differences among lenders when it comes to rates and other loan terms. If you don’t take the time to comparison shop, there’s a good chance you’re paying too much. That’s the last thing anyone needs to do today.

Half a century of debt? Here’s what a 50-year mortgage would cost you

Published Nov. 11, 2025

President Donald Trump recently floated the possibility of a 50-year mortgage.

A 50-year mortgage would mean lower monthly payments for homebuyers, which would certainly be appealing for those who feel priced out of the market. However, there are also some very real downsides. In exchange for that lower payment, homeowners would likely face a higher interest rate, pay significantly more interest over the life of the loan and build equity more slowly than they would with shorter-term mortgages.

Breaking down monthly payments, interest paid

A 50-year mortgage would likely come with a higher interest rate than a 30-year mortgage, though it’s impossible to know how much higher. However, even if the 50-year mortgage came with the same APR as the 30-year, the math would look quite different.

Here’s a look at the differences in costs for a 50-year mortgage versus a 30-year mortgage on a $500,000 loan with a 6.10% APR — roughly the average current rate for a 30-year, fixed-rate mortgage today.

Monthly payments and total interest paid on a $500,000 loan with a 6.10% APR

| Loan term | Monthly payment | Total interest paid | % of original balance paid in interest |

|---|---|---|---|

| 50 years | $2,669 | $1,101,430 | 220.29% |

| 30 years | $3,030 | $590,791 | 118.16% |

| 15 years | $4,246 | $264,342 | 52.87% |

With a 50-year mortgage, the amount you’d pay in interest in this example would total more than double the original purchase price of the home — a staggering $1.1 million-plus in interest. With a 30-year mortgage, you’d still pay an enormous amount of interest, but nearly half of what you’d pay on a 50-year mortgage. Not surprisingly, the total interest paid on a 15-year mortgage is far lower, though it comes with a much higher monthly payment.

Here’s what it would look like if you increased the APR to 7.00%, roughly the average rate at the start of 2025.

Monthly payments and total interest paid on a $500,000 loan with a 7.00% APR

| Loan term | Monthly payment | Total interest paid | % of original balance paid in interest |

|---|---|---|---|

| 50 years | $3,008 | $1,305,065 | 261.01% |

| 30 years | $3,326 | $697,544 | 139.51% |

| 15 years | $4,494 | $308,945 | 61.79% |

With this higher APR, the interest you’d pay on a 50-year mortgage would equal more than two-and-a-half times the original balance — more than $1.3 million in total.

Finally, here’s a look at what would happen if rates fell to 4.00%, significantly lower than today’s rates but higher than the record low rates seen at the start of the decade.

Monthly payments and total interest paid on a $500,000 loan with a 4.00% APR

| Loan term | Monthly payment | Total interest paid | % of original balance paid in interest |

|---|---|---|---|

| 50 years | $1,929 | $657,121 | 131.42% |

| 30 years | $2,387 | $359,348 | 71.87% |

| 15 years | $3,698 | $165,719 | 33.14% |

Even with these lower rates, you’d still pay $657,121 in interest over 50 years, well more than the original $500,000 balance.

50-year mortgage would mean slower equity growth

With any mortgage, your early years are spent paying more toward interest than to the original loan balance. That means that the equity in your home tends to grow slowly. That is certainly true with a 30-year mortgage, but it’s even more apparent with a 50-year mortgage.

Here’s what that looks like, using the same $500,000 loan and 6.10% APR as the first example.

Timeline for paying off original loan balance on $500,000 mortgage with 6.10% APR

| 50-year mortgage | 30-year mortgage | |||

|---|---|---|---|---|

| Time | Amount of original balance paid off | % of original balance | Amount of original balance paid off | % of original balance |

| 10 years | $20,989 | 4.20% | $80,459 | 16.09% |

| 20 years | $59,559 | 11.91% | $228,310 | 45.66% |

| 30 years | $130,433 | 26.09% | $500,000 | 100.00% |

| 40 years | $260,673 | 52.13% | Not applicable | Not applicable |

| 50 years | $500,000 | 100.00% | Not applicable | Not applicable |

After 10 years of paying on that 50-year mortgage, you’d have only paid about $21,000 on the original $500,000 balance — just over 4%. Compare that to the 30-year mortgage, with which you would’ve paid more than $80,000, or 16%, of the original balance.

Looking out 20 years, the difference is even more stark. With a 30-year mortgage, you’ve paid about $228,000 — nearly half the original balance. With a 50-year mortgage, you’d have paid off about $60,000, or 12%, of the original balance.

That’s a significant development because home equity can be a powerful asset. A 50-year mortgage means that equity will take far longer to grow. It also creates a real risk because it means that a homeowner could more easily be underwater on a loan — meaning they owe more on the house than the house is worth — in the event of a downturn in the housing market. That’s a troubling spot to be in.

Understand what’s right for you

The future of the 50-year mortgage is unclear. However, there’s plenty that home shoppers can do today to lower their mortgage costs, regardless of what comes of the 50-year mortgage.

One of the most impactful pieces of advice is also the simplest: Shop around. You can compare rates from multiple lenders before you apply for a loan. Recent LendingTree research shows that the savings can be massive:

- November 2025: “Refinancing at the best available rate could save you $50,000 or more over your current mortgage.”

- June 2025: “Borrowers could save an average of $80,024 over the life of a 30-year, fixed-rate mortgage by shopping around.”

Those are substantial savings that can have a real impact on people’s finances, but only if you take action.

Matt’s thoughts on Q3 2025 New York Fed quarterly debt report

Published Nov. 5, 2025

Here’s what LendingTree chief consumer finance analyst Matt Schulz has to say about the Nov. 5 release of the Federal Reserve Bank of New York’s Quarterly Report on Household Debt and Credit, which is generally considered the gold standard tracker of consumer debt and credit in the U.S.:

- “Mortgage debt, auto loan debt, credit card debt, student loan debt and overall debt are all the highest they’ve ever been. That’s troubling. It isn’t uncommon to see debt climb in the third quarter, but these record debt levels are another sign that it might be a tough holiday season for Americans.”

- “Debt will almost certainly continue to rise in the fourth quarter, in part because it almost always does. Holiday shopping is a huge part of that, and this year should be no different. While lower interest rates, thanks to the Fed, should help, there’s little reason to believe debt won’t grow in the coming months before slowing down after the first of the year.”

- “Rising debt in this country is never about one thing. It’s always a mix of confidence and struggle. Some people take on debt because they want to, while others do so because they don’t have any other choice. Both scenarios are taking place all over America today, but I believe that more of the debt growth right now comes from struggle than from confidence.”

- “As Americans’ mountain of debt grows, people need to understand they have far more power over their money than they think they do. They have to be willing to wield it, though. For example, a 0% balance transfer credit card can be a powerful weapon against credit card debt, as can a debt consolidation loan. Refinancing may be a possibility for some homeowners struggling to make payments. Shopping around and getting preapproved for financing can help you keep costs down when buying your next vehicle. Even a simple call to a creditor during a short-term rough patch can make a major difference. Most lenders have hardship programs in which they can temporarily reduce interest rates, waive fees, defer payments and make other tweaks to help you manage things better. These steps can have an impact on your financial life, but only if you pursue them. It can be worth your time to do so.”

Matt’s thoughts on October 2025 Fed meeting

Published Oct. 27, 2025

Here’s what LendingTree chief consumer finance analyst Matt Schulz has to say about this week’s Federal Reserve meeting, set for Oct. 28 and 29:

- Another Federal Reserve rate cut would be good news for Americans wrestling with debt. Yes, this cut will likely be small — it’s widely expected to be 0.25 percentage points — but when combined with the previous one and the promise of more, it’s a reason for cautious optimism for debt-weary Americans.

-

Mortgage rates have fallen to their lowest levels in more than a year. While there’s no guarantee that the downward trend will continue, a rate cut might spur more Americans to consider jumping back into the housing market after sitting on the sidelines.

- Home shoppers need to understand that Fed rate cuts don’t always lead to lower mortgage rates. The Fed is just one factor in determining mortgage rates. But at a minimum, cuts are a reason for potential home shoppers to be hopeful about the future.

-

The average interest rate on a new credit card offer is 24.19%, having fallen for the first time since March in the wake of the Fed’s last cut. That downward trend is only going to accelerate in the next few months, as banks implement the September and (most likely) October rate cuts. Still, even if the Fed steps on the gas in the coming months, credit card rates aren’t going to go from awful to amazing overnight.

- If you have $7,000 in debt on a credit card with a 24.19% APR and pay $250 a month on that card, it’ll take 42 months and $3,411 in interest to pay off that balance.

- Lower that a quarter-point to 23.94% and you’ll need 41 months and owe $3,350 in interest to pay it off. (A savings of one month and $61.)

- Drop it another quarter-point to 23.69% and you’ll need 41 months and owe $3,290 in interest to pay it off. (A savings of one month and $121 from the original calculation.)

-

For savers, it’s likely time to act to lock in today’s high rates. Yields on high-interest savings accounts and certificates of deposit (CDs) are only going to keep dropping. It may be wise to consider a longer-term CD as rates continue to fall.

- If you haven’t shopped around for a high-yield savings account, it’s still worth your time. While yields will be well below the peaks in recent years, they’ll still likely be better than what you’d get from a traditional savings account with a megabank.

- People need to understand that they can have a far bigger impact on their interest rates than the Fed will. By comparing rates from multiple lenders, getting a 0% balance transfer credit card or even calling your lender and asking for a lower rate, you can find significantly bigger reductions than you’re likely to ever get from the Fed.

Federal Reserve cuts rates for first time since December

Published Sept. 17, 2025

The Federal Reserve lowered interest rates by a quarter-point on Sept. 17 — the first time in 2025. This is good news for those struggling with credit card debt, but not so great for savers.

Here’s what you need to know.

Credit card rates are about to fall

When the Fed moves, card interest rates usually follow, meaning Americans should soon see relief on existing balances and new card offers. While any reduction is welcome news, one rate cut is unlikely to have a significant impact, though.

For example, if you owe $7,000 on a credit card with a 24.36% APR — the average APR on new credit card offers, per LendingTree data — and pay $250 a month on that card, it’ll cost you $3,453 in interest and take 42 months to pay off.

Lower the APR by a quarter-point to 24.11% with the same balance and monthly payments, and it’ll cost you $3,391 in interest and take 42 months to pay off. That’s a savings of $62 over the life of the balance, which is significant but isn’t exactly life-changing either.

Rates for home equity lines of credit (HELOCs) are also typically tied to the Fed’s movements, so those should move lower as well after the rate cut.

Impact on other loan rates not as clear

There’s certainly hope that the Fed’s actions will lead to lower rates on mortgages, auto loans, personal loans and other types of loans, but there are no guarantees. That’s because these types of loans’ rates aren’t directly tied to the Fed’s actions the way that credit card and HELOC rates tend to be.

In fact, mortgage rates went up amid the Fed’s rate cuts last fall. However, since mortgage rates have fallen significantly in recent months, there’s reason for optimism that the Fed’s moves will help mortgage rates continue to move lower. Still, that’s far from a sure thing.

Returns on high-yield savings accounts, CDs likely to fall, too

Even though the yields from high-yield savings accounts (HYSAs) and CDs are down from highs a year ago, people have still been able to get substantial returns — often 4.00% or higher — throughout 2025. Now that the Fed has begun lowering rates again, those yields are likely to follow suit.

Still, rates won’t change from excellent to awful overnight. It’s still worth your time to shop for a HYSA if you haven’t already done so. It’s also worth considering buying a longer-term CD — perhaps with a maturity of a year or longer — to lock in rates for a little longer. Just make sure you won’t need to access those funds before maturity hits. Otherwise, the penalty costs could outweigh any extra interest you might’ve earned.

You have more power over your rates than the Fed

No, really. It’s true. Simple moves you make can have a far bigger impact on your interest rates than the Fed will.

- Comparing mortgage offers from multiple lenders can help you secure a lower rate and save you tens of thousands of dollars over the life of the loan.

- Getting a 0% balance transfer credit card can significantly reduce your interest and shorten your payoff time on a transferred balance.

- Consolidating debts with a low-interest personal loan can lower your interest rate and reduce the number of bills you have to pay each month.

- Calling your credit card lender and asking for a lower interest rate can be a big step. A 2025 LendingTree study found that 83% of cardholders who asked for a lower APR on a credit card in the past year got one, and the average reduction was more than 6 percentage points.

You have much more power over your money than you think. While there’s no guarantee these steps will be successful — for example, you may need to have a credit score of 680 or higher to get a 0% balance transfer card — they’re worth the effort.

35% of cardholders wouldn’t cancel if their annual fee jumped $100

Published Sept. 16, 2025

“If your primary credit card’s annual fee rose by $100 without adding any benefits, would you keep it?”

LendingTree asked this question in July to more than 800 Americans with an annual fee credit card, and 35% said yes.

I was stunned. Closing a credit card isn’t something to be done lightly, but the fact that more than 1 in 3 people we asked would willingly absorb a $100 annual fee increase without getting anything new in return blew me away.

High-income earners, millennials ages 29 to 44, Republicans and men are among the most likely to say yes. Here’s a closer look.

- 50% of those making $100,000 or more a year say they’d keep the card, versus no more than 31% among lower-income brackets

- 46% of millennials, versus 39% of Gen Zers ages 18 to 28, 33% of Gen Xers ages 45 to 60 and 10% of baby boomers ages 61 to 79

- 44% of Republicans, versus 35% of Democrats and 28% of independents

- 44% of men, versus 25% of women

We wanted to ask this because sky-high annual fees have been in the news lately. Several major credit card issuers have introduced new high-annual-fee cards or announced plans (or been rumored to do so soon) to hike the annual fee on a current high-annual-fee card. Unlike the hypothetical card in our question, these updated cards are expected to come with at least some new benefits. Still, given that many high-end cards already have annual fees of $500 or higher, any new increases are noteworthy.

There’s risk for card issuers with any annual fee increase. A 2024 LendingTree survey of credit cardholders (including those who don’t have an annual fee card) found that just 9% of cardholders would consider paying an annual fee of $400 or more on a card, including 3% who said they’d be willing to pay $1,000 or more depending on the benefits. Meanwhile, 45% would never pay an annual fee and another 30% would never pay $100 or more for one.

Still, the results of our July survey clearly show that people haven’t hit their ceiling when it comes to credit card annual fees. That means we can expect to continue seeing banks push the envelope in the future.

What to do in case of an annual fee increase

- Ask for a fee waiver or reduction. A separate 2025 LendingTree survey found that a stunning 95% of cardholders who asked to have an annual fee waived or reduced in the past year got their way, though just 39% of those with an annual fee credit card asked. It stands to reason that a bank might be more willing to waive an $89 fee than a $695 fee, but it can’t hurt to ask. That 95% success rate means that it isn’t just people with low annual fees, 800 credit scores and long track records getting their way.

- Downgrade to a no-annual-fee version. This isn’t always possible, but it’s certainly worth asking about. When it comes to your credit, downgrading isn’t seen as closing an account and opening a new one. Instead, it’s seen merely as changing to a different version of the same card.

- If all else fails, it’s likely OK to cancel the card. Generally speaking, when in doubt, you should probably just keep that credit card you’re considering closing. One major exception to that rule is when an annual fee is involved. If a card has an annual fee and you know that you’re not going to use it anymore, you’re likely better off canceling the card. There’s no need to pay that annual fee just to protect your credit.

Credit pro tip: If you cancel the card, consider asking for a credit limit boost on another one of your cards. That new credit can replace the available credit you lost with the newly closed card and minimize the damage the closing did to your credit.