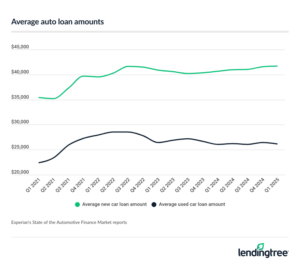

Your car loan rate depends on your credit score, the car you’re buying and the amount of your down payment, among other factors. For comparison’s sake, the average rate for a new car loan was 6.35% as of the fourth quarter of 2024. For used cars, the average was 11.62%.

According to a LendingTree study, improving your credit score from fair (580-669) to very good (740-799) could save you more than $2,316 on your auto loan over time. But improving your credit score isn’t the only way to get a better car loan rate. You could also:

Get preapproved and use it as leverage

Getting preapproved for a car loan before heading to the dealer gives you a lot of power. Preapproval is generally the last step before actually applying for a loan and it’s optional, for the most part. Unlike prequalification, preapproval requires a hard credit hit.

A preapproved car loan will show you — and the dealer — how much you’re approved to spend, and your auto loan rate. The dealer might be motivated to try to get you a cheaper rate in order to sell you a car. Not only that, but you might be able to use your preapproved loan amount to negotiate a better out-the-door price.

If you aren’t comfortable negotiating, bring someone who is

Unless you’re shopping at a dealership that doesn’t allow negotiation (like CarMax), you might as well try to get a little knocked off the purchase price — the worst the dealer can say is no.

If you aren’t comfortable negotiating, get a sales-y friend or family member to come with you to the lot. Having someone bold on your side can also come in handy when you finalize your auto loan. The dealer is probably going to offer you cosmetic packages and warranties. By the end of the day, you’re going to be tired and it might be hard to say no, even if you don’t really want the option the dealer is offering.

Use a comparison service to shop auto loan rates

Applying for car loans is boring at best, and confusing at worst. You also might miss out on super-competitive lenders that aren’t as well known, unless you’re in the industry. Let us do the work for you — LendingTree has the nation’s largest network of lenders, and you only have to fill out one quick form to access it.

Consider a credit union

Credit unions typically offer some of the lowest auto loan rates. The downside is that you have to become a member to borrow. Some credit unions have strict guidelines you have to meet before you can join.

Still, the effort might be worth it depending on the deal you can find. Research credit unions (both brick-and-mortar and online credit unions), see which ones you might be able to join and shop rates.

Don’t wait until you have no choice

If you can, don’t wait until your current car is no longer running before shopping for a different car. When you’re in desperate need of transportation, you could be more likely to take any deal that comes your way — good or bad.

Use a car-buying service

Your current bank or credit union might offer a car-buying service (often through TrueCar). You might qualify for a rate discount if you use it to buy your ride. Car-buying services can also make it easier to compare car deals in your area — prices typically vary from dealer to dealer.

Look for lesser-known promotions and rebates

Most car manufacturers offer their own car loans. This is called captive financing — Ford Motor Credit is one example.

Captive financing can come with perks, including promotions for military and military families, current college students and recent college grads. And if you’re related to someone who works for the company that makes your car, even better — you could qualify for some of the deepest discounts available.

Make a down payment

Not all auto loans require a down payment. Even so, it may be a good idea to make one anyway.

Putting money down takes some of the lender’s risk and transfers it to you. After all, you’ll lose your down payment if the lender repossesses your car. As a result, a down payment can help you secure a better rate.

Pick a short loan term

Cars are getting more expensive, so 84-month car loans are increasingly popular. That’s because longer terms usually mean lower monthly payments. However, longer terms also almost always carry higher rates.

Buy your car during the holidays

If you’re getting captive financing, shop around the holidays and the end of the year. Although they’re harder to find when inflation is high, this is the time of year where you’re most likely to find a 0% APR car deal.

Plan ahead for car insurance“I’ve been a car insurance agent for 15 years and one of the most common mistakes I see car-buyers make is forgetting to budget for their new car insurance premium. Don’t wait until you’re at the dealer to get quotes. It’s hard to shop around in such a high-pressure environment. You also don’t want to get your heart set on a car, only to find out you can’t afford the insurance.”

— Carol Pope, Staff writer