How Much Does It Cost to Refinance a Mortgage?

The cost to refinance a mortgage depends on various factors, including your loan size and lender, but you generally won’t pay more than 5% of your total loan amount.

Making sense of these costs can help you decide whether refinancing is worth it, and whether you may want to finance your closing costs.

- Closing costs are usually 2% to 5% of your loan amount. Lenders must list every one of those costs out for you within three business days of your application.

- Just a few closing costs make up more than half of a typical borrower’s closing costs, and of those, origination fees are the most negotiable.

- Some loan programs allow you to roll the closing costs into your loan so you can have no out-of-pocket costs at closing.

How much does it cost to refinance a mortgage?

You’ll typically pay mortgage refinance closing costs ranging from 2% to 5% of your loan amount.

For example, if you refinance a $200,000 mortgage, your total closing costs could fall between $4,000 and $12,000.

The exact amount you’ll pay in refinance closing costs will vary based on:

- Loan size: Larger loans usually have higher total fees, while smaller loans tend to cost more as a percentage of the loan amount

- Lender pricing: Some lenders charge higher origination fees

- Location: Taxes, title fees and recording costs vary by state and county

- Loan type: Government-backed loans include additional upfront fees, but streamline programs may allow you to skip certain costs

If you’re thinking about refinancing your existing mortgage into a new one, it’s important to understand the refinance fees you’ll pay to make it happen.

You’ll see a full breakdown of these costs on your loan estimate, which lenders are required to provide within three business days of your application. Before closing, you’ll receive a closing disclosure with the final numbers at least three business days in advance.

Not all refinance closing costs are worth stressing about or focusing on. In most cases, just a few fees drive the majority of your total cost, while the rest are relatively small or fixed.

Focus on these, which make up over half of most people’s refinance closing costs:

- Origination fees

- Lender title and insurance fees

- Transfer taxes

Comparing these fees across lenders when mortgage shopping can materially change your total costs. You should also know that you can negotiate them — lenders have the power to reduce origination fees if they want to compete for your business.

Don’t stress about these:

- Credit report fees

- Flood certification fees

- Recording fees

- Document prep fees

Typical refinance closing costs with flat fees

Fixed or “flat” refinance fees are the same regardless of your loan amount, so these fees will typically represent a higher percentage of the loan amount for those who take out smaller mortgages. Below are average cost calculations from the Urban Institute using Fannie Mae data.

| Refinance cost | How much? |

|---|---|

| Loan origination fee | $1,545 to $2,258 (roughly 0.5% to 1% of the loan amount) |

| Home appraisal fee | $558 |

| Credit report fee | $80 per applicant |

| Document preparation fee | $102 |

| Title search and lender’s title insurance fee | $1,626 |

| Recording fee | $179 |

| Flood certification fee | $8 |

Application fee

Lenders may charge this fee to start the mortgage application process. The actual fee amount will vary by lender, and some banks require you to pay it up front. Some lenders will waive the fee once the loan process is complete. Most lenders, however, won’t refund the fee if they reject your application.

Loan origination fee

This fee covers the lender’s costs to process and underwrite your loan, which could include expenses like paying a loan officer to help originate the loan or compensating the underwriter for assessing your ability to repay it.

Home appraisal fee

Many lenders order a home appraisal, whether you’re purchasing or refinancing a home. Banks can’t determine how much you can borrow until they know your home’s true market value. In some cases, however, you may not need an appraisal for your refinance.

Credit report fee

It costs money to pull a copy of your credit report and scores, and lenders want to see them before they proceed with your application. Lenders pull several different versions of your credit report, so prices will vary. They often use FICO credit scores.

Don’t know your credit score? Get your free score on LendingTree Spring today.

Document preparation fee

Your lender may charge this fee to create and send the documents you sign at closing.

Title search/insurance fee

You’ll need a new lender’s title insurance policy when you refinance your mortgage. It can pay to haggle over title insurance fees to get the best deal available. That said, know that in some states these fees are more regulated than in others.

Recording fee

When you refinance, you may need to pay recording fees to state or local government agencies to document the transaction. These fees vary based on your location.

Flood certification fee

Your lender charges this fee to check whether your property is in a flood zone. If it is, you may need to purchase flood insurance.

Typical percentage-based refinance closing costs

These fees are based on a percentage of your loan amount, which means that the more you borrow to refinance, the more expensive they’ll be.

| Refinance cost | How much? |

|---|---|

| Mortgage points | 1% of the loan amount per point |

| Mortgage insurance premiums |

|

Mortgage points

Also known as discount points, you can pay mortgage points upfront at closing for a reduced mortgage interest rate. Each point incurs a fee worth 1% of the loan amount and can lower your interest rate by as much as 0.25 percentage points.

Mortgage insurance premiums

If you have 20% equity in your home, you won’t pay any private mortgage insurance (PMI) to cover the risk you might default on a conventional loan.

However, loans backed by the Federal Housing Administration (FHA loans), U.S. Department of Veterans Affairs (VA loans) and U.S. Department of Agriculture (USDA loans) require mortgage insurance, or some type of guarantee fee, regardless of how much equity you have.

| Only paid for with purchases: | Still required in refinances: |

|---|---|

|

|

When is it worth it to refinance?

If you wait long enough, a refinance won’t cost you anything at all — it will fully pay for itself and then begin saving you money.

But you need to be sure you’ll eventually reach that enviable place before you apply for a refinance. To do so, you should calculate your break-even point and make sure that you’ll remain in the mortgage at least to that point.

The calculation is easy: Divide your total refinance closing costs by your estimated monthly savings. The result is the number of months you’d need to stay in your home to recoup the refinance costs.

For example: Let’s say you can save $200 per month with a refinance that costs you $5,000.

When you divide the $5,000 closing costs by the $200 monthly savings, the result is 25.

So, if you stay in your home for at least 25 months — just over two years — the refinance makes sense.

Use LendingTree’s refinance calculator to estimate your break-even point and how much you can save by refinancing.

Reasons to refinance your home

- You’re able to get a lower interest rate: A loan with a lower mortgage rate reduces your monthly mortgage payment and lifetime interest costs. If mortgage rates or your credit history have improved since you took out your existing loan, you could refinance with a lower rate and secure some serious savings.

- You want to change your loan term: You can pay off your mortgage earlier with a shorter term — assuming you can afford the higher monthly payment. Alternatively, you can stretch out your term to get a lower monthly payment.

- You want to convert an ARM to a fixed-rate mortgage: An adjustable-rate mortgage (ARM) is a loan with a low initial fixed rate for the first few years, but changes based on market factors. If rates spike over time, your payments can become unaffordable. Converting your ARM to a fixed-rate loan gives you the stability of a predictable monthly payment.

- You want to tap your home equity: With a cash-out refinance, you’ll take out a new mortgage for a larger amount than you currently owe and pocket the difference in cash to accomplish other financial goals, like making home improvements or covering college costs. Use our cash-out refinance calculator to crunch the numbers and determine whether this option makes sense.

Reasons not to refinance your home

- Your break-even point isn’t advantageous: If your break-even point is several years away, or it’s closer but you have plans to move before it hits, you shouldn’t refinance.

- Your long-term savings aren’t significant: Since refinancing restarts your mortgage term, it can add years to your mortgage payoff date — years during which you’ll also pay additional interest. In some cases, even a lower interest rate can’t overcome this hurdle.

- You can’t pay refinance closing costs: “No-closing-cost” refinance loan programs allow you to roll your closing costs into the loan. However, while it may keep you from spending a chunk of money upfront at closing, it’s not free money — you actually end up paying for it over the life of your loan.

Learn more about when refinancing may make sense or when it could hurt you more than help you: When Should I Refinance My Mortgage?

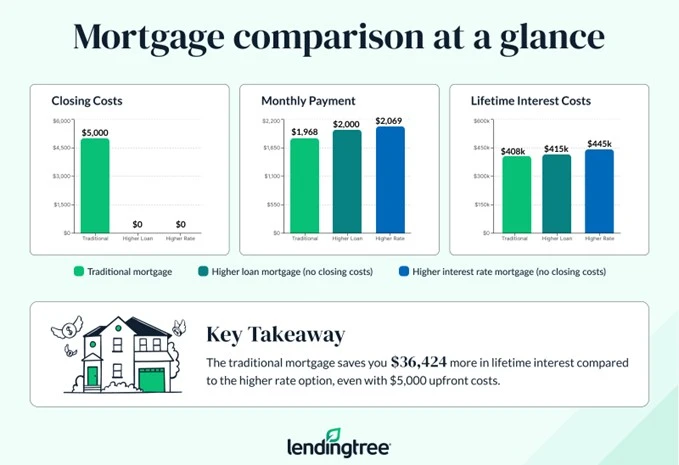

How does a no-closing-cost mortgage work?

If you’re short on cash to refinance your home, a no-closing-cost mortgage allows you to refinance without having to pay thousands out of pocket at closing.

The lender will cover the costs — including origination, title and appraisal fees — but, in exchange, they’ll charge you a higher interest rate or add the closing costs to your loan amount. Just know that you’re not eliminating these costs, you’re paying for them over time through a higher rate or a larger loan balance.

You’ll save money upfront but pay significantly more in interest charges over the life of your loan.

10 ways to reduce refinance closing costs

- Get your credit in the best possible shape: A credit score of at least 780 will typically get you the lowest rate and costs, and may even make the refinance approval process easier. To boost your score, pay your bills on time, shrink your credit card balances, dispute any credit report errors and avoid applying for new credit.

- Shop around with multiple lenders: You won’t know whether you’re getting the best refinance rates possible if you don’t comparison shop. Apply for a loan with three to five lenders and compare their refinance fees.

- Negotiate your refi costs: Don’t be afraid to ask for a better deal. You can negotiate some of the fees associated with refinancing — a lender might reduce or waive some fees, especially application or origination fees.

- Reduce your debt before you refinance: Pay off credit card debt and refinance your auto or student loans before refinancing to avoid paying a higher rate or bringing extra dollars to the closing table.

- Borrow less of your home’s value: Lenders look at your loan-to-value (LTV) ratio when determining your interest rate, and the more you borrow, the riskier they consider the loan. You’ll also avoid mortgage insurance costs if you borrow 80% or less of your home’s value with a conventional loan.

- Avoid cash-out refinances if you can: Converting home equity to cash with a cash-out refinance is a great way to clear out credit card balances or make home improvements. However, since you’re taking out a larger loan, your closing costs may be higher.

- See if you’re eligible for a streamline refinance program: If you currently have an FHA, VA or USDA loan, see if you’re eligible for an FHA streamline, VA interest rate reduction refinance loan (VA IRRRL) or a USDA streamline assist refinance. These programs don’t require an appraisal and charge a lower mortgage insurance fee than regular government refinance programs. Plus, as an added bonus, you won’t need to verify your income.

- Review your loan estimate: Go over your loan estimate with a fine-tooth comb and ask for clarification about any costs that are unclear. You can also shop around for certain services (found on Page 2 of the loan estimate) to find the best deal.

- Try for an appraisal waiver: Ask your lender if you qualify for an appraisal waiver — if so, you could save a couple of hundred dollars on your refi.

- Work with the same title insurance company: You may be able to save money on the lender’s title insurance policy by asking for a reissue rate, which is a discounted policy amount you can get for working with the same title insurance company used for the original loan.

See today’s refinance rates and top lenders on LendingTree.

Frequently asked questions

You can view current refinance rates at LendingTree’s refinance rates page. You may also want to get personalized quotes from multiple lenders.

Though you should expect to pay anywhere from 2% to 5% of your loan amount in closing costs for either a refinance or a purchase, you’ll probably pay less to refinance than you’d pay to close on a comparable purchase loan.

It’s up to your lender whether it wants to offer a no-closing-cost mortgage option; there’s no rule that would prohibit conventional loans from being no-closing-cost loans. Assuming that the loan wouldn’t violate the guidelines set by Fannie Mae and Freddie Mac, a no-closing-cost loan could, in theory, also still be a conforming loan. If the loan violated the rules for a qualified mortgage (QM) loan set under the Truth in Lending Act, it could still be conventional but may be a non-qualified mortgage (Non-QM).