Side Hustles Are Declining — But 61% Say They Can’t Afford Life Without One

Side hustles remain a key financial lifeline for many Americans, but their popularity is beginning to cool.

According to a LendingTree survey of nearly 2,050 U.S. consumers, today’s side hustlers are earning more than ever — $1,242 a month — and often rely on that extra income to keep up with rising costs. But while side hustles help many stay afloat financially, most side hustlers would ultimately prefer the stability of a single, reliable paycheck.

Here’s a closer look at the trends shaping side hustle income and sentiment.

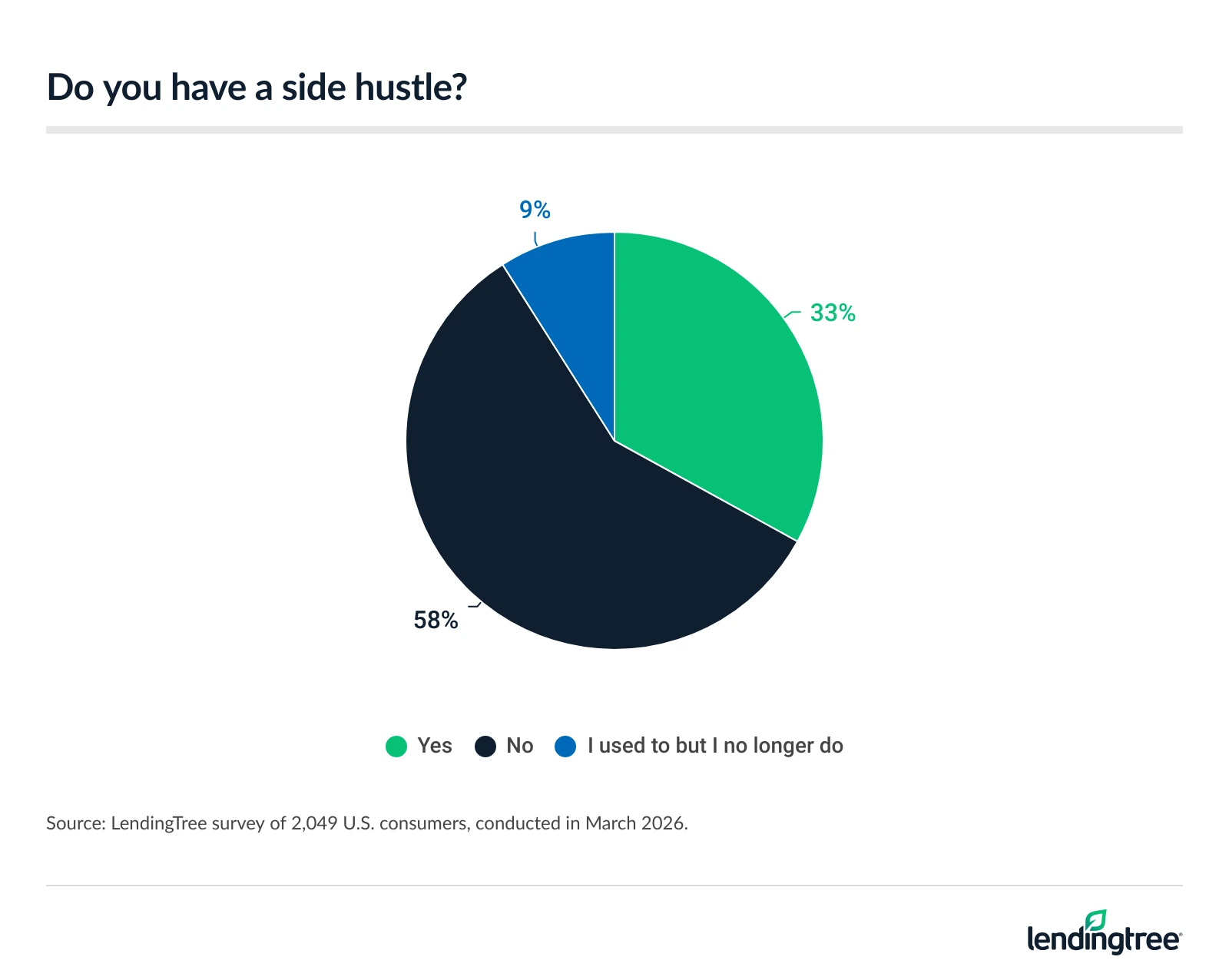

- Side hustlers are on the decline. A third (33%) of Americans have a side hustle, down from 38% last year and 44% in 2022. The most common side hustles are gig and on-demand work (29%), freelance and professional services (26%), and creative, content and media activities (23%). On average, side hustlers earn $1,242 monthly. This is up from $1,215 last year and $473 in 2022.

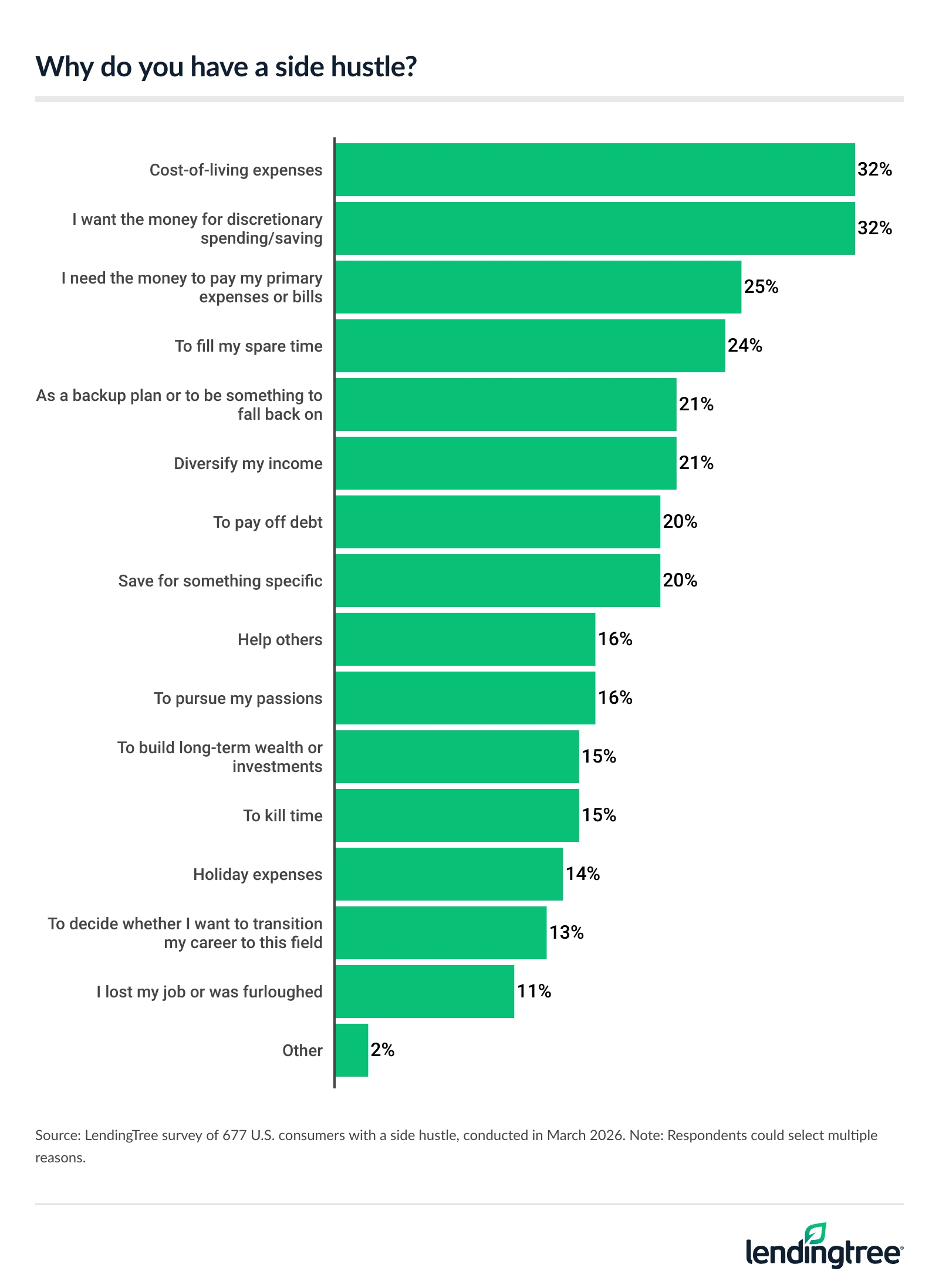

- As costs rise, many are looking for a second income. The most popular reasons for picking up a side hustle are to cover cost-of-living expenses (32%), use it for discretionary spending or saving (32%) and pay for primary expenses or bills (25%). Additionally, respondents cite the current economy (36%) and inflation (31%) as the most common drivers behind starting one.

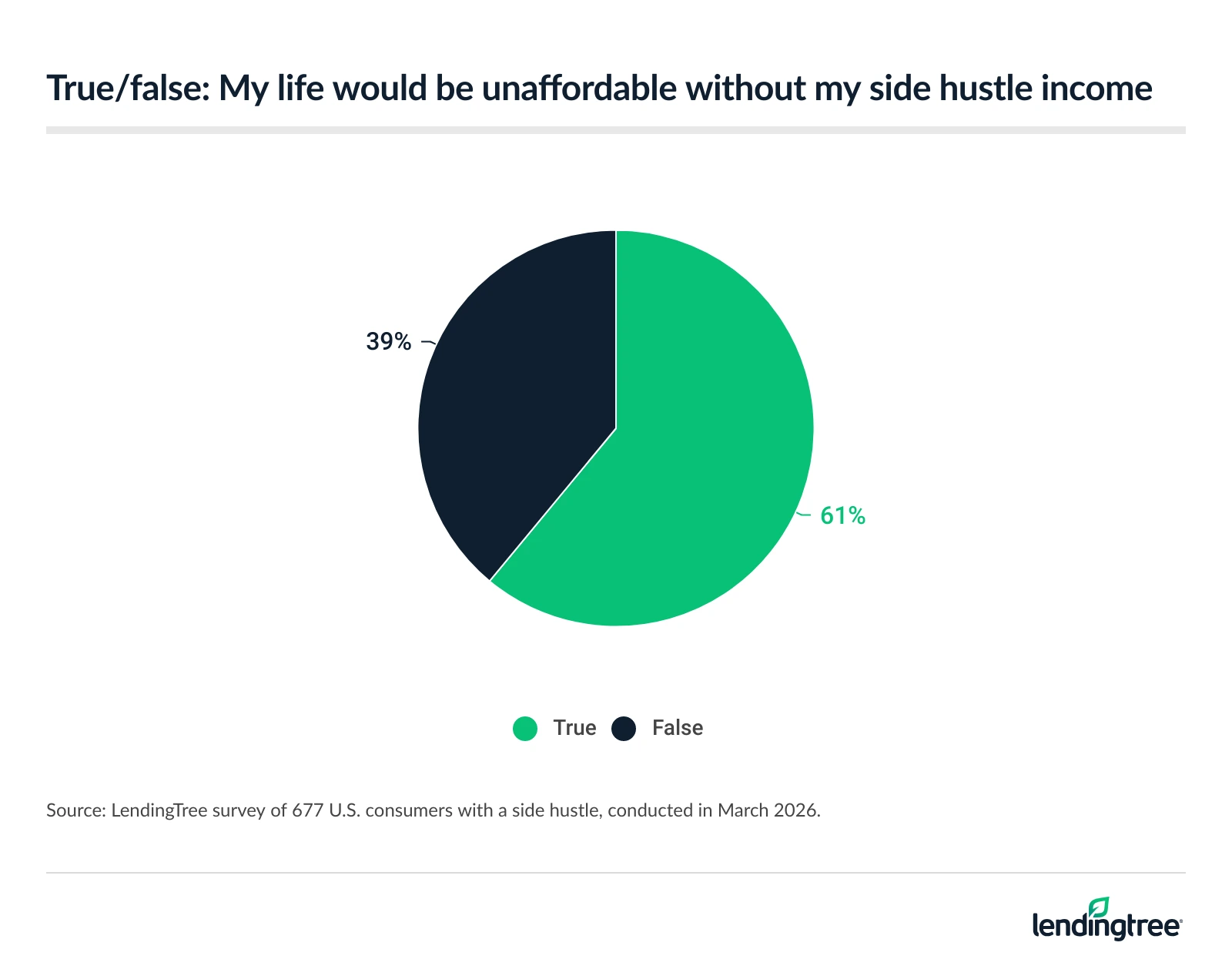

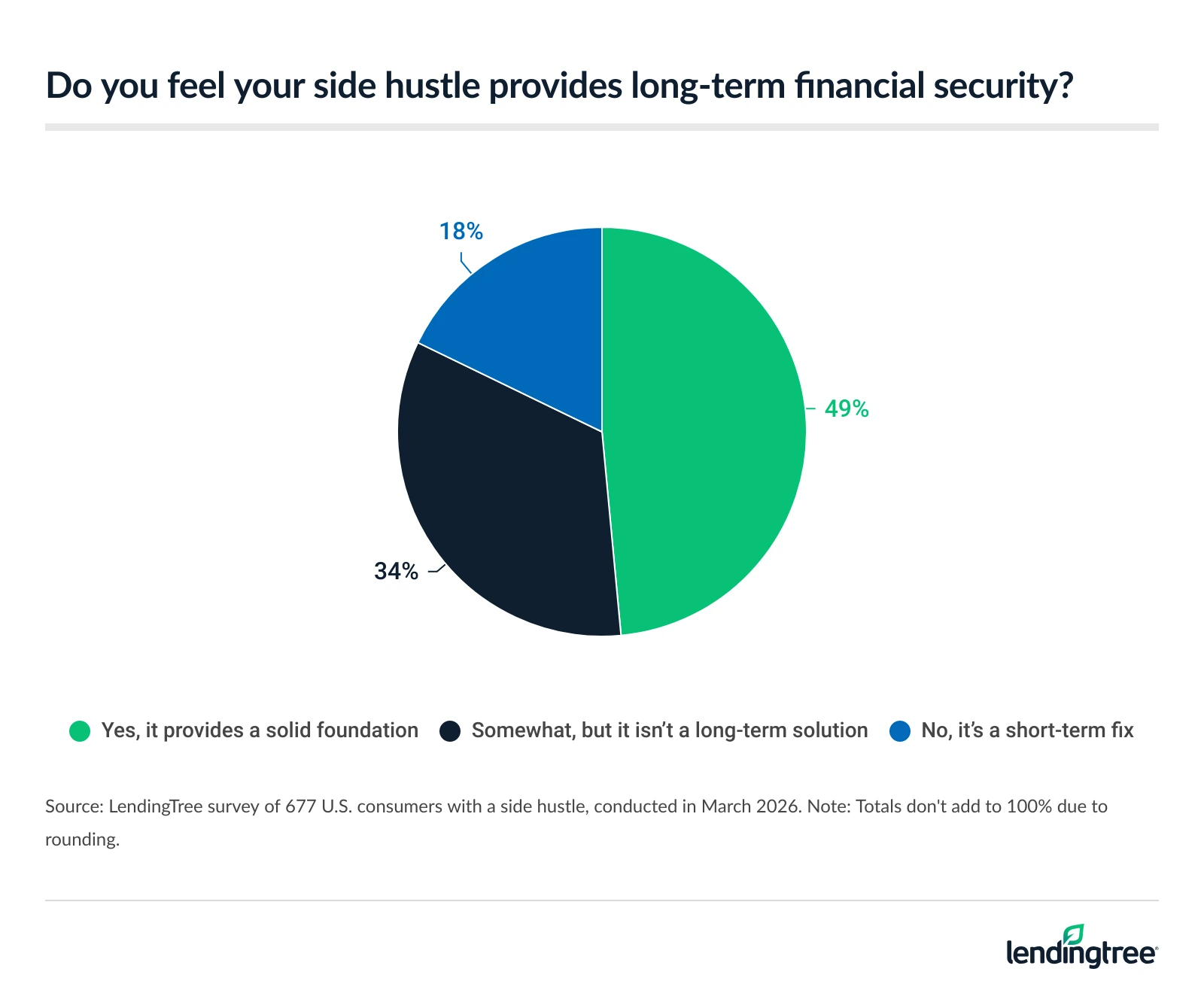

- Side hustles provide a path to financial stability. 61% of side hustlers say their life would be unaffordable without a side hustle income, and 80% say their side hustle improves their quality of life. Additionally, 49% say their side hustle contributes to long-term financial security.

- Still, many would trade side hustles for one steady paycheck. 69% of side hustlers say they’d prefer to have one main source of income if given the opportunity. When asked what they’d cut if their side hustle disappeared tomorrow, 39% said dining out, 37% said shopping, 33% said entertainment and 32% said streaming services.

Fewer Americans have a side hustle

Side hustling is becoming less common. In our 2026 survey, 33% of Americans report having a side hustle, a noticeable drop from 38% last year and 44% in 2022.

This is especially true among younger generations. Among millennials ages 30 to 45, 45% report having a side hustle in 2026, compared with 50% in 2025 and 55% in 2022. Gen Zers ages 18 to 29 experienced an even sharper decline, with 43% side hustling in 2026 — down from 57% in 2025 and 62% in 2022.

When it comes to the most common side hustles, gig and on-demand work (29%) top the list. Here’s the full list, including examples as provided to respondents:

- Gig economy and on-demand work such as food or grocery delivery, ride sharing, babysitting and pet sitting (29%)

- Freelance and professional services such as online freelancing, industry consulting, tutoring or teaching, and fitness instructing (26%)

- Creative, content and media activities such as e-commerce resale, direct sales and multilevel marketing (23%)

- Home improvement and skilled trades such as painting and moving services (21%)

- Home and property services such as house cleaning and landscaping (17%)

- Investing and financial activities such as day trading and rental apartment management (16%)

- Event-based work like DJing, photography and event planning (12%)

- Adult content such as OnlyFans (9%)

- Illicit activities such as illicit substance sales (8%)

Despite fewer people taking on extra work, earnings are on the rise, with side hustlers making an average of $1,242 a month, up slightly from $1,215 last year and significantly higher than $473 in 2022.

Matt Schulz — LendingTree chief consumer finance analyst and author of “Ask Questions, Save Money, Make More: How to Take Control of Your Financial Life” — says declining participation despite rising incomes isn’t necessarily what you’d expect, but it makes sense.

“Yes, it has never been easier or cheaper to start a side hustle, but it still typically costs money to start one,” he says. “Inflation has squeezed budgets, leaving people with less income to devote to starting that small business. High interest rates and tight lending standards have perhaps caused people to think twice about borrowing to fund a business. Also, in this K-shaped economy, while many Americans are struggling and desperately need as much income as they can find, many others are thriving and have less need to have that extra income on the side.”

For many, side hustles require a moderate time commitment. Among side hustlers, 32% dedicate five to 10 hours per week, while 24% spend between 11 and 15 hours. In terms of longevity, 37% have maintained their side hustle for one to two years. Looking ahead, nearly a third (32%) say they expect to always have a side hustle, while 25% — including 35% of Gen Zers — plan to continue until their primary job provides a higher income.

Even as participation declines, interest remains strong. More than half (55%) of Americans say they’re likely to start a side hustle within the next year.

Side hustles cover cost-of-living increases

As everyday expenses continue to climb, many Americans are turning to side hustles for additional income. Among side hustlers, 32% say they take on extra work to keep up with cost-of-living expenses, while another 32% use the money for discretionary spending or saving. Meanwhile, 25% rely on side hustle income to help cover essential bills and primary expenses.

Economic pressures are a major factor behind this trend. Among those with a side hustle, 36% point to the current economic environment as a key reason for starting one, while 31% cite inflation. Additionally, 26% say rising housing costs pushed them to seek out extra income streams. Other reasons for starting a side hustle include:

- Job insecurity or layoffs (20%)

- Rising interest rates (16%)

- Medical debt (15%)

- The COVID-19 pandemic (13%)

- Marriage (12%)

- Birth of a child (10%)

- Stock market dips (9%)

- Divorce (6%)

Still, Schulz cautions against relying on side hustles to combat economic pressures.

“Relying on side hustles can be risky, in large part because of how unpredictable side hustle income can be,” he says. “Even the most successful side hustles will have highs and lows, and that volatility creates real challenges. For example, it’s difficult to have a meaningful budget if you can never be quite sure how much money you’ll bring in during a given month.”

Most rely on side hustles for financial stability

For many Americans, side hustles provide more than just “fun” money. In fact, 61% of side hustlers say their life would be unaffordable without the additional income their side hustle provides — unchanged from last year’s 61%.

Beyond covering immediate expenses, side hustles are also improving overall well-being, with 80% of side hustlers saying their side hustle enhances their quality of life. That’s up from 77% last year. Meanwhile, nearly half (49%) believe it supports their long-term financial security, up from 44% a year ago.

Certain groups are especially likely to say they see long-term benefits. That includes 65% of six-figure earners, 62% of parents with children under 18, 56% of millennials and 53% of Gen Zers. There’s also a notable gender gap, with 58% of men saying their side hustle strengthens their long-term financial security, compared with 36% of women.

Side hustlers would prefer steady income

Even with the financial benefits, many side hustlers would prefer the simplicity of a single steady income. In fact, 69% say they’d choose to rely on one primary source of income if they had the option — up from 65% last year.

Schulz says that’s understandable, particularly as managing your financial life with unpredictable income isn’t easy.

“Millions of Americans do it every month, but that doesn’t make it a walk in the park,” he says. “When you know how much money is coming into your household each month, it makes it far easier to budget for basic costs like food and gas, as well as debt repayment, savings, investments and other long-term goals. When income is inconsistent, it’s harder. You’re forced to hold money back in great months to ensure that you’ll be OK during leaner months, for example. Otherwise, you may be forced to rely on borrowing to help you make ends meet, and that’s not ideal for anyone.”

If that extra income were to disappear, many say they’d scale back on everyday spending. About 4 in 10 (39%) would cut back on dining out (down from 46% last year), 37% would reduce shopping (down from 39% last year) and 33% would spend less on entertainment (also down from 39% last year). Additionally, 32% say they’d cancel or cut back on streaming services.

For most, side hustle income makes up a relatively small portion of their overall earnings. In total, 28% say it accounts for 10% to 24% of their income, while another 28% report it contributes less than 10%.

Earning more and borrowing responsibly with a side hustle: Top expert tips

Side hustles can be a powerful way to boost your income, but making the most of that extra money requires a smart strategy. Whether you’re looking to pay down debt, build savings or set yourself up for long-term success, how you manage your earnings matters just as much as how much you bring in. We offer the following advice:

- Knock down your rates on high-interest debt. “Money that goes toward paying off credit cards and other types of debt is money that can’t go toward building your small business, growing your savings or working toward other financial goals,” Schulz says. “A 0% balance transfer credit card can dramatically reduce the interest you pay on a balance, as well as the payoff time. A low-interest personal loan can, too. You can even call your card issuer and ask it to lower the rate. It works way more often than you realize.”

- Work on improving your credit. “Few things in life are more expensive than crummy credit,” he says. “It can have a massive effect on your personal finances, and it also matters when you’re trying to start a business or a side hustle. Protect your credit by reviewing your credit reports from the three major credit bureaus at least yearly to ensure there are no inaccuracies. Automate as many payments as possible to make sure you’re never late. Always try to pay more than the minimum so you’re never in danger of maxing out a card.”

- Always be saving. “Think you have enough savings?” Schulz says. “I’ve got news for you. You almost certainly don’t. Stashing even just a few dollars away every few weeks in a high-yield savings account can help you widen your financial margin of error, providing peace of mind during those lean months when that side hustle income dips a bit. And, yes, even when you’re paying down debt, you should still put money away. It means it will cost a little more and take a little longer to pay down that debt, but it will all be worth it when your card balance is at $0 and your savings account balance isn’t.”

Methodology

LendingTree commissioned QuestionPro to conduct an online survey of 2,049 U.S. consumers ages 18 to 80 on March 3-6, 2026. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. Researchers reviewed all responses for quality control.

We defined generations as the following ages in 2026:

- Generation Z: 18 to 29

- Millennials: 30 to 45

- Generation X: 46 to 61

- Baby boomers: 62 to 80

Get debt consolidation loan offers from up to 5 lenders in minutes