Auto Refinance Rates: What To Expect by Credit Score in July 2026

See refinance APRs by credit score and lenders with competitive starting rates

Advertising Disclosures

Loading Disclosures…

-

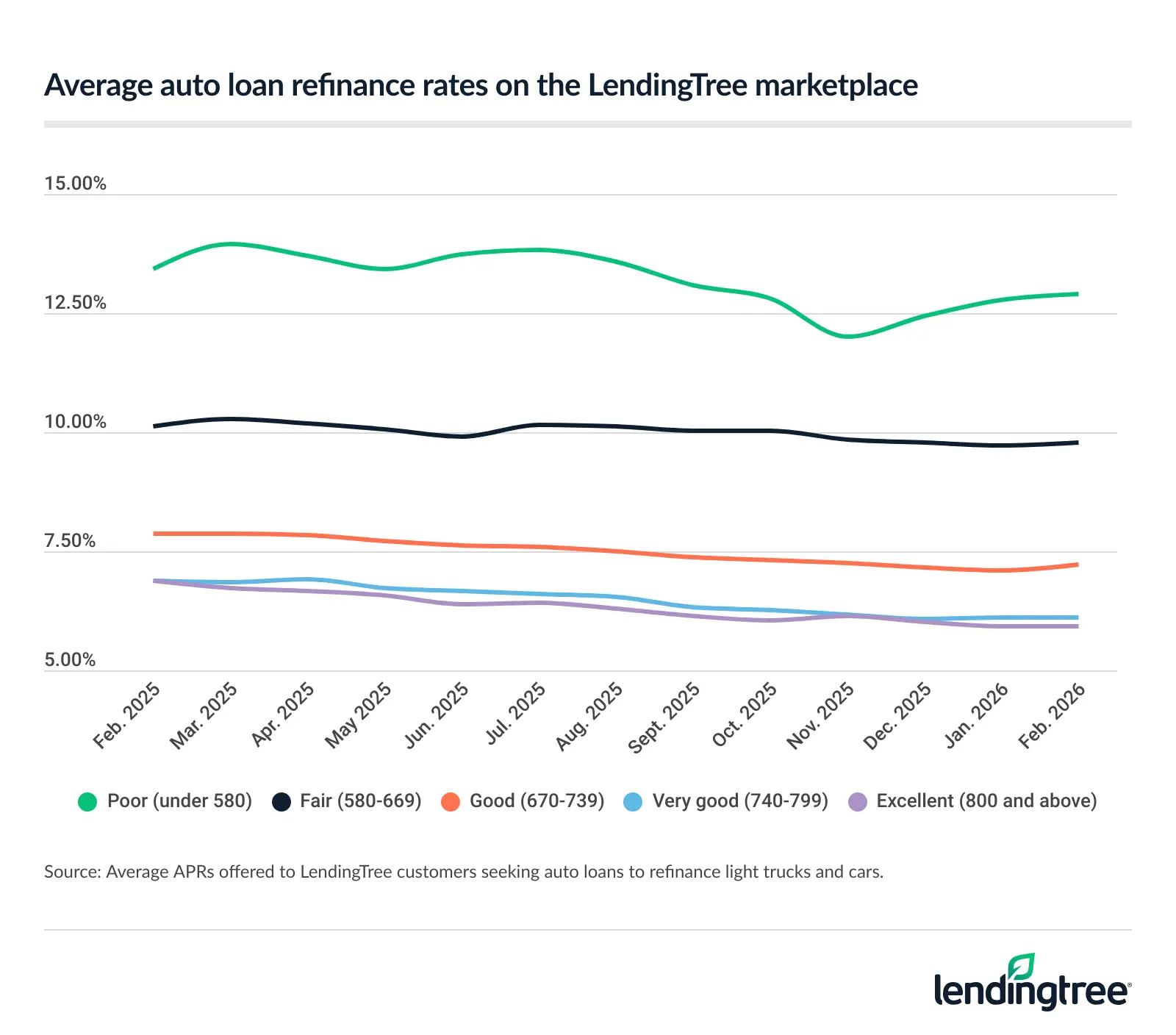

The average auto refinance rate is 7.76%

across all credit scores, according to Q4 2025 LendingTree marketplace data.Based average APRs offered to LendingTree customers seeking auto loans to refinance light trucks and cars.

- Average auto refinance rates are slightly lower than they were around this time last year (7.97% in February 2025 vs. 7.85% in February 2026), based on the latest data.

- In a LendingTree analysis, borrowers who refinanced their auto loans reduced their monthly payments by an average of $142.

What are auto refinance rates right now?

To help you make smarter financial decisions, LendingTree uses anonymized marketplace data to find average rates for auto refinance loans on a quarterly basis.

Q4 2025’s data highlights the wide gap in average annual percentage rates (APRs) offered to borrowers with very good credit versus those with poor credit. Those with scores under 580 (poor credit) pay nearly double the rate compared to borrowers with very good credit (740-799).

| Credit tier | Average APR | Average amount | Average term |

|---|---|---|---|

| Excellent (800 and above) | 6.30% | $33,249 | 67 months |

| Very good (740-799) | 6.48% | $35,892 | 66 months |

| Good (670-739) | 7.50% | $30,196 | 66 months |

| Fair (580-669) | 10.10% | $29,129 | 66 months |

| Poor (under 580) | 13.38% | $27,337 | 67 months |

Tracking auto refinance rates over time, based on LendingTree data

Auto refinance rates have been holding fairly steady, except for borrowers with poor credit (under 580). Bad credit auto refinance rates dropped significantly in Q4 2025 but have since risen.

If you’re waiting for the Fed rate to drop before refinancing, reconsider. No one knows what the future holds, especially in a tumultuous economy. Besides, borrowers typically save more by improving their credit score before refinancing than they do by trying to time the market.

Auto refinance loans with low starting rates

| Lender | Starting APR | Term | Amount | |

|---|---|---|---|---|

|

|

3.50% | 12 to 84 months | Up to $100k | |

|

|

3.89% | 12 to 96 months |

$250 – $50k |

|

|

|

4.49% (with autopay) | 12 to 96 months |

$10k – $150k |

|

|

|

4.49% | 24 to 84 months |

$4k – $100k |

|

|

|

4.29% | 24 to 96 months |

$5k – $150k |

|

|

|

4.49% | 24 to 84 months |

$5k – $125k |

Learn more about how we chose lenders with competitive auto refinance rates.

Auto refinance rates and terms by company

- Starting APR

- 3.50%

- No restrictions on model year or odometer reading

- Can skip a payment when in financial need

- Special financing for recent college and trade school grads, based on eligibility

- Must become a credit union member (but it’s easy to join)

- Skipping a payment isn’t free

- Can’t check rates without impacting credit

Southeast Financial Credit Union (SFCU) offers some of the lowest auto refinance rates around, especially on shorter-term loans. Not only does it offer competitive rates, but SFCU accepts all model years and has no restrictions on vehicle mileage.

This credit union is based in Tennessee, but it does business online nationwide. Like many credit unions, it offers member-friendly benefits like its Skip-a-Payment program. It costs $60 to skip a payment (which SFCU can add to your loan balance), but the fee may be worth it to avoid a missed payment.

You must have a credit score of at least 600 to qualify for an auto loan. You also need to join the credit union before you can borrow.

All SFCU members must open a savings account with a deposit of at least $5. To become a member, you must meet one of the requirements below:

- Make a $5 donation to Autism Tennessee

- Be a current employee or retiree of a Southeast Financial Select Employee Group

- Be related to a current SFCU member

- Live, work, worship or go to school in certain parts of Tennessee, Kentucky or Mississippi

- Starting APR

- 3.89%

- Active duty and retired military can get an APR discount

- 24/7 U.S.-based customer service

- Must be affiliated with the military to become a member

- Have to apply over the phone or at a branch to get the military APR discount

- Checking rates requires a hard credit inquiry

If you qualify to join, Navy Federal Credit Union (NFCU) (NFCU) may be a good option for cheap auto refinance rates. NFCU offers a 0.25% APR discount to active duty and retired military on top of its already competitive APRs. However, be sure to call or stop by a branch if you want to apply for this discount, as it can only be added by a representative.

NFCU has exclusive membership requirements that not everyone meets. If you do qualify for membership, you must agree to a hard credit inquiry to check rates. This could drop your credit score by about five points, according to FICO.

Navy Federal Credit Union (NFCU) doesn’t provide insight into its criteria around what vehicles you can refinance and what credit requirements you’ll need to meet. To become a member, though, you’ll need to fall into one of the following categories:

- Active duty members of the military (regardless of branch)

- Veterans, retirees and annuitants

- Those in the Delayed Entry Program (DEP)

- Department of Defense (DOD) Officer Candidates and ROTC

- DOD Reservists

- DOD civilian personnel

- Immediate family of military members, as well as household members

You’ll need to meet the following requirements:

- Administrative: Provide your Social Security number, home address, credit card or bank account number, and a form of government identification

- Membership: Create a Membership Savings Account and maintain a $5 balance to join and continue membership in the credit union

- Starting APR

- 4.49%

- High ratings from LendingTree users

- Processes the DMV paperwork for you

- Refinances cars up to 20 years old

- No mobile app

Auto Approve is a loan marketplace that connects applicants to partner lenders. It also has loan consultants on staff to guide you through the refinancing process. If you choose an offer, Auto Approve will submit the loan application, handle the DMV paperwork and pay off your old auto loan for you.

Although you can check rates on Auto Approve’s website, it doesn’t have a dedicated mobile app.

To qualify for a car refinance loan with Auto Approve, you’ll need a credit score of at least 600 and your car must be 20 model years old or newer.

To finalize your loan, you must provide:

- Driver’s license

- Valid vehicle registration

- Proof of insurance

- Pay stubs or proof of income

- Starting APR

- 4.49%

- Will pay off your current lender on your behalf

- Free mobile app comes with 24/7 credit monitoring

- No rate discounts

- Customer service not available on weekends

- Not available in all states

Unlike some of the other picks on this list, Happen Bank is a direct lender. That means it funds loans itself rather than connecting you with a partner lender.

With its quick online process and easy-to-use mobile app, Happen Bank simplifies refinancing. If you’re approved, you won’t have to worry about paying off your old car loan — Happen Bank will take care of that for you.

Although it doesn’t offer rate discounts, its starting APRs are low. However, its customer service hours are limited compared to NFCU’s 24/7 availability.

Happen Bank is transparent about its eligibility requirements, which makes it easy to check whether you’re likely to qualify for a refinance. To be eligible, you need to meet the below criteria.

- Credit score: 600+

- Location: Happen Bank doesn’t offer auto refinance loans in Alaska, Hawaii, Maine, New Hampshire, North Dakota, Vermont, West Virginia, Wyoming, Washington, D.C., or the U.S. territories

- Loan requirements: Your current loan must be open for a minimum of one month with at least 24 months of payments left and a balance of $4,000 to $55,000

- Car age: 10 years old or newer

- Mileage: Less than 120,000 miles

- Vehicle restrictions: Refinancing is not available for Chevrolet Express G-Series Van, Aston Martin, Cross Lander, Daewoo, Ferrari, Hummer, Lamborghini, Isuzu, Maserati, Mercury, Nissan Leaf, Oldsmobile, Pontiac, Saab, Saturn and Suzuki

- Starting APR

- 4.29%

- Accepts lower credit scores and monthly incomes

- Consistently top three in customer satisfaction according to LendingTree users

- Pays off old loan for you and transfers title to new lender

- Lackluster mobile app ratings

RefiJet is a loan marketplace that matches borrowers with partner lenders. Some people prefer this option since it allows you to shop with more than one lender at once. RefiJet works with a wide network of lenders that accept credit scores as low as 500, making RefiJet a possibility if you have bad credit.

RefiJet’s mobile app doesn’t have the highest ratings. However, that may not matter, as you can apply through RefiJet’s online portal, and once you’re matched and signed with a lender, you’ll work with the lender rather than with RefiJet.

To qualify for a RefiJet auto refinance loan, you’ll need to meet these requirements:

- Credit score: 500+

- Minimum income: $1,900 single or $2,200 joint; must have a job or verifiable source of income

- Other credit considerations: Recent car payments must have been made on time

- Vehicle restrictions: Must be less than 10 years old, have under 150,000 miles and have at least $5,000 remaining on current loan

- Administrative: Must have a valid driver’s license, full coverage insurance and vehicle registration

- Starting APR

- 4.49%

- Pays off your old auto loan for you

- Assigns you a dedicated loan officer

- Accepts cars up to 20 years old

- No mobile app

- Customer service not available on Sundays

Caribou is a loan marketplace. Instead of funding loans itself, it connects potential borrowers with partner lenders. Although your loan won’t technically be through Caribou, it has dedicated loan officers available to walk you through the process of picking a lender and e-signing your documents.

Caribou is an online-only marketplace, but it doesn’t have a mobile app (although you can communicate with your loan officer via text).

To refinance a car with Caribou, you must meet the requirements below:

- Credit score: 580+

- Residency: Can’t live in Maryland, Nebraska, Nevada or West Virginia

- Minimal annual income: $24,000

- Vehicle restrictions: Car must be 20 years old or newer, cannot have more than 150,000 miles and must have at least $5,000 left on current loan

How much can auto refinancing actually save you?

A LendingTree study found that borrowers save an average of $1,346 in total interest (or $142 a month) by refinancing their auto loan.

How much you can save by refinancing depends on your credit, the car you’re refinancing and other factors that are specific to you. You can get an estimate using an auto refinance calculator. Have your current auto loan information available, and if you aren’t sure what your refinance APR would be, use the data in our quarterly auto refinance rate report.

As a general example, say you have $23,000 left on a 60-month auto loan with 48 months remaining. Your APR is 7% and your monthly payment is about $550. Here’s how refinancing that remaining $23,000 could affect your budget, depending on your refi APR and term.

You may qualify for a lower APR on your auto refinance loan if you’ve improved your credit score since buying your car, if you add a cosigner to your refi loan or simply due to overall market conditions.

Imagine that your credit score was 660 when you financed your car. Because of healthy financial habits, you now have a score of 740 — taking your credit from fair to very good. You qualify for a refi loan at 5% APR, compared to your current 7%. A 2% rate difference would save you $960 in total interest while reducing your monthly payment by $20.

| Current auto loan | Refinance auto loan | |

|---|---|---|

| APR | 7% | 5% |

| Time remaining on loan/new loan term | 48 months | 48 months |

| Monthly payment | $550 | $530 |

| Remaining interest | $3,400 | $2,440 |

| Total interest savings | - | $960 |

Refinancing to a shorter term condenses what you owe into a shorter period of time. This will make your monthly payment go up, but you can pay less interest overall and pay off your car loan faster.

By refinancing your remaining 48 months into a 36-month refinance loan, you’d save $840 in total interest and be out of debt one year sooner. However, your monthly payment would increase by $160 a month.

| Current auto loan | Refinance auto loan | |

|---|---|---|

| APR | 7% | 7% |

| Time remaining on loan/new loan term | 48 months | 36 months |

| Monthly payment | $550 | $710 |

| Remaining interest | $3,400 | $2,560 |

| Total interest savings | - | $840 |

Refinancing to a loan with a longer term usually results in more overall interest — but not always. The increased total interest that normally comes from extending your loan term could be offset if your auto refinance loan has a lower rate.

In the scenario below, you extended your loan term from 48 to 60 months, so you’ll be in debt for one extra year. However, you qualified for an APR of 5% instead of your current APR of 7%. Overall, you end up saving a modest $360 in total interest, but you’re able to lower your monthly payment by $116.

| Current auto loan | Refinance auto loan | |

|---|---|---|

| APR | 7% | 5% |

| Time remaining on loan/new loan term | 48 months | 60 months |

| Monthly payment | $550 | $434 |

| Remaining interest | $3,400 | $3,040 |

| Total interest savings | - | $360 |

Factors that influence your auto refinance rate

There’s more to being a “well-qualified buyer” than a strong credit score. Each lender has its own proprietary method of calculating auto refinance rates. That’s why it’s common to see different lenders offer different rates for the same borrower refinancing the same vehicle.

Some lenders may weigh credit score more heavily, while others may put more emphasis on factors like credit history length, income stability or debt-to-income (DTI) ratio. Other auto refinance rating factors include:

- Loan-to-value ratio (LTV): LTV compares your remaining loan balance to your car’s current market value. Lenders will calculate this for you, but the higher your LTV, the more of your vehicle’s value you’re borrowing. Higher LTVs lead to higher auto refinance rates, and an LTV above 100% means you’re upside down.

- Odometer reading: Lenders prefer not to refinance a vehicle that has a high likelihood of breaking down while the borrower is still making payments. Higher-mileage vehicles typically carry higher rates or may not qualify at all, depending on the lender’s eligibility requirements.

- Current loan balance: The amount you refinance can influence your rate. Lenders tend to charge higher rates on their smallest and largest loans. Smaller loans are often less profitable for the lender and bigger loans can be riskier.

- Loan term: Extending your loan term can result in lower monthly car payments, but longer terms often carry higher APRs and lead to more total interest.

Compare auto refinance rates with LendingTree

You’d shop around for flights. Why not your loan? LendingTree makes it easy. Instead of applying to one lender and hoping for a good rate, you can see multiple lenders compete for your business — so you can choose the best offer.

Tell us what you need

Take two minutes to tell us what you need to refinance. We’ll take care of the rest. It’s free, simple and secure.

Shop your offers

LendingTree users get at least three auto loan refi offers on average, even if they have bad credit. Compare your offers side by side to get the best deal.

Get refinanced

Choose an offer, finalize your loan and you could have the money you need within 24 hours.

Why do millions of Americans trust LendingTree?

25+ years in business. 110+ million Americans served. $260+ billion in funded loans.

Security

Instead of sharing information with multiple lenders, fill out one simple, secure form in five minutes or less.

Savings

We’ll match you with up to five lenders from our network of 300+ lenders who will call to compete for your business.

Support

We provide ongoing support with free credit monitoring, budgeting insights and personalized recommendations to help you.

How we chose lenders with competitive auto refinance rates

We reviewed 30 auto refinance lenders and marketplaces and selected those advertising among the lowest starting APRs as of publication. We also refined our picks to ensure representation was given to credit unions, lenders, loan marketplaces and lending platforms.

According to our systematic rating and review process, the best auto refinance loans come from Southeast Financial Credit Union, Navy Federal Credit Union (NFCU), Auto Approve, Happen Bank, RefiJet and Caribou.

To make our list, lenders must offer auto refinance loans with competitive APRs. From there, we prioritized the following factors:

Accessibility: We chose lenders with auto loans that are available to more people and require fewer conditions. This may include lower credit requirements, wider geographic availability, faster funding and easier and more transparent prequalification, preapproval and application processes.

Rates and terms: We prioritize lenders with more competitive starting fixed rates, fewer fees and greater loan options for repayment terms, amounts and APR discounts.

Repayment experience: For starters, we consider each lender’s reputation and business practices. We also favor lenders that have self-service payment options (such as a mobile app), provide reliable customer service and offer unique perks.

Our editorial team applies the same scoring model and standards to every lender. Lenders cannot pay to influence our ratings. Read more about our editorial guidelines and standards.

Frequently asked questions

According to Q4 2025 marketplace data, the average auto refinance rate is 7.76%

If your quoted APR is higher than the average for your credit tier, consider getting additional quotes.

You can usually refinance a car loan as soon as the title is transferred into your name. This can take 60 to 90 days, in some cases.

Even so, you may want to wait at least six months to a year before refinancing. This will give your credit score some time to stabilize after taking out your car loan and prove to a potential refinance lender that you’re responsible by making on-time payments.

Some lenders refinance upside-down car loans, but a down payment may be required and rates may be high. Lenders might also require that you have excellent credit and an acceptable debt-to-income ratio to make up for the added risk.

A break-even point tells you how long your auto refinance repayment term needs to be in order for refinancing to be worth it.

It generally costs money to refinance your car. Some refinance lenders charge doc fees, and your current lender may charge a prepayment penalty for closing your loan early. Many states also require you to pay a title transfer fee after refinancing. You won’t have to pay these fees out of pocket if you roll them into your new refinance loan, but then they’ll be subject to interest.

To calculate your break-even point, divide your total refinance costs by your monthly savings.

For instance, assume that refinancing will cost $600 in fees but will save you $30 a month. In this case, you need to keep your refinance loan for at least 20 months to be worth it (since $600 / $30 = 20).

Refinancing your auto loan can affect your credit in many ways. Obtaining the loan typically requires a hard credit inquiry. According to FICO, hard credit inquiries usually drop scores down by about five points.

However, as you make on-time payments over time, you should see your credit score recover from this small dip. On-time payments can boost your credit, as payment history makes up 35% of your FICO Score.

Lenders give their starting APRs to only the most qualified borrowers and the lowest-risk loans. Actual rates depend on factors like your credit score, income, existing debt and credit history, along with the car you’re refinancing. The best way to know whether a quote is competitive is to compare multiple offers based on the same loan details.