Cheap Car Insurance for Older Cars

- State Farm has the cheapest insurance for most drivers with an older car.

- Older cars are usually cheaper to insure than new ones.

- You can get classic car insurance if your older vehicle is a collectible.

Cheapest car insurance for an older car

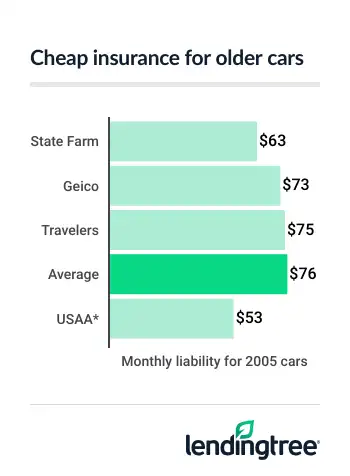

For most drivers, State Farm has the cheapest liability car insurance for older cars at $63 a month. USAA is cheaper at $53 a month, but it’s only available to the military community. Liability-only

Older vehicle auto insurance rates

| Company | Liability only | Full coverage | LendingTree score | |

|---|---|---|---|---|

| State Farm | $63 | $129 | ||

| Geico | $73 | $147 | ||

| Travelers | $75 | $135 | ||

| Farmers | $80 | $155 | ||

| Progressive | $79 | $159 | ||

| AAA | $85 | $173 | ||

| USAA* | $53 | $125 | ||

Insurance companies look at various factors, including your driving record and where you live, when figuring out your insurance rate. Each company weighs these factors differently, so prices will vary by customer. This is why it’s good to compare car insurance quotes from a few companies to find the cheapest rate for you.

Are older cars cheaper to insure?

Older cars usually cost less to insure than newer ones, mostly because they are worth less. Insurance companies will charge less for older cars because it doesn’t cost them as much to repair or replace them. You can also choose to get less insurance coverage, which will cost you less, when the car’s value has dropped low enough.

The average cost of full coverage for a 2005 vehicle is $157 a month before discounts. This is 36% less than the rate for 2025 model year cars and 15% less than the rate for 2015 vehicles.

Car insurance rates by model year

| Model Year | Monthly full coverage |

|---|---|

| 2005 | $157 |

| 2015 | $185 |

| 2025 | $246 |

Do I need full coverage for an older car?

You may not need full coverage for an older car that you own outright. Lenders require collision

The benefits of full coverage start to decline as your vehicle ages and loses value. Collision and comprehensive only cover your vehicle at its estimated resale price. But both also have a deductible, which is subtracted from your insurance payment.

- For example, if you have a car worth $2,000 and a $500 deductible, insurance won’t pay you more than $1,500 for it.

- In general, collision and comprehensive cost $711 a year for older cars. This means you could save about $1,420 over two years if you choose to drop your full coverage.

- The $1,420 you save over two years without full coverage is nearly the same as your insurance payment for a total loss. After three years, you’ll save more than the value of your car. Obviously, these savings may be negated if your car is in an accident or stolen within that time.

How much is my older car worth?

Sources like kbb.com offer good estimates of your car’s value. When to choose to drop full coverage depends on your finances and comfort level with risk.

- If you have money in the bank, it may be worth dropping full coverage once your car’s value drops to $5,000.

- If you’re strapped for cash, full coverage may be worth it for a car worth at least $3,000.

- It’s usually not worth keeping full coverage for a car worth less than, or only slightly more, than your deductible.

What kind of insurance do I need for an older car?

Aside from collision and comprehensive, common auto insurance coverages are the same for older cars. These include:

- Liability

- Uninsured motorist

- Personal injury protection (PIP)/medical payments (MedPay)

Older cars are more likely to break down than newer models. If you don’t already have a roadside assistance plan, you may want to add towing coverage to your insurance.

Liability

Liability is required by law in almost every state. However, your state’s minimum requirements may not provide enough protection. If an accident victim’s expenses are greater than your liability limits, you are responsible for the difference.

Fortunately, it doesn’t cost too much to increase your liability limits. For example, it usually only costs about $20 a month to raise your bodily injury liability

Uninsured motorist

Uninsured motorist covers you and your passengers for injuries caused by a driver with no insurance. About 1 in 7 drivers don’t have auto insurance, according to the Insurance Research Council. Uninsured motorist coverage is required by law in 20 states (plus Washington, D.C.) and optional in most others.

PIP/MedPay

PIP and MedPay both cover injuries to you and your passengers, whether you or another driver caused the accident. PIP also covers lost wages and pays for services you need during your recovery, like help with housecleaning. PIP is required in about a dozen states. PIP and/or MedPay are optional in other states.

Towing and labor

Most car insurance companies offer roadside assistance as a cheap add-on. These plans typically only cover short tows and basic assistance like battery jumps and fuel delivery.

Some insurance company plans reimburse you for roadside assistance after you pay for service. Plans that pay service providers directly are more convenient.

Should I buy classic car insurance for an older car?

Classic car insurance is a good option for an older car that’s become a collector’s item.

A car usually has to be at least 25 years old to qualify for classic car insurance. However, some companies accept younger models. Most classic car insurers also require you to:

- Keep the vehicle in a garage or other enclosed space

- Only drive the car occasionally

- Have a separate car for daily use

Classic car insurance is usually cheaper than standard car insurance. This is mostly because classic cars are not driven very often, which reduces their crash risks.

Standard car insurance only covers a vehicle at its actual cash value, after age and wear. Classic car insurance can cover your collectible vehicle at an agreed-upon higher value, if it qualifies.

Frequently asked questions

No. Older cars are usually cheaper to insure than newer ones.

Most older cars cost insurance companies less to repair or replace than new ones. This usually translates into lower car insurance rates. You can also save more on car insurance by dropping collision and comprehensive, or full coverage, for an older car.

A car typically has to be at least 25 years old to be considered a classic and eligible for classic car insurance. However, the specific age requirements can vary among car clubs and insurance companies. Some classic car insurance companies insure collectible vehicles of any age.

How we got insurance rates for older cars

LendingTree uses insurance rate data from Quadrant Information Services using publicly sourced insurance company filings. Rates are based on an analysis of car insurance quotes for typical drivers in Georgia, Texas and Washington state. Prices are shown for comparative purposes only. Your own rates may be different.

Unless noted otherwise, quotes are for a full-coverage policy for a 30-year-old man with good credit and a clean driving record.

Vehicles

Rates were obtained for the following vehicles from the 2005, 2015 and 2025 model years:

- Chevrolet Equinox

- Ford F-150

- Chevrolet Equinox

- Honda Civic

- Subaru Outback

- Toyota Camry

Coverage limits

Minimum-liability policies provide liability coverage with the state’s required minimum limits.

Full-coverage policies include collision, comprehensive and liability coverage:

- Bodily injury liability: $50,000 per person, $100,000 per accident

- Property damage liability: $50,000

- Uninsured/underinsured motorist bodily injury: $50,000 per person and $100,000 per accident

- Collision: $500 deductible

- Comprehensive: $500 deductible

How we evaluated car insurance companies

Our team of insurance experts rated insurance companies based on several categories. These categories include average rates, discounts, coverage options, third-party customer service ratings and app/website experience. We weighted these categories based on what customers value in an insurance company.

For third-party customer service ratings, we included Complaint Index scores from the National Association of Insurance Commissioners (NAIC) and financial strength ratings from A.M. Best. NAIC Complaint Index scores are used to determine how satisfied customers are with their claims, while financial strength ratings from A.M. Best reflect the ability to pay out claims.

Read our editorial guidelines here.

*USAA is only available to current and former members of the military as well as certain family members.