Best Hawaii Homeowners Insurance for 2026

RLI has Hawaii’s best home insurance, with policies tailored to the state’s unique risks.

Advertising Disclosures

Loading Disclosures…

- The best homeowners insurance company in Hawaii is RLI, with its higher-risk policies and reasonable rates.

- The average homeowners insurance premium in Hawaii is $928 (65% below the national average).

- Climate-related natural disasters have led to more nonrenewals in recent years, but the state does offer an insurer of last resort.

Best homeowners insurance in Hawaii

RLI is the best homeowners insurance company in Hawaii overall. It offers coverage for high-risk homes, which is essential for many in the Aloha State who have been turned down for insurance renewal.

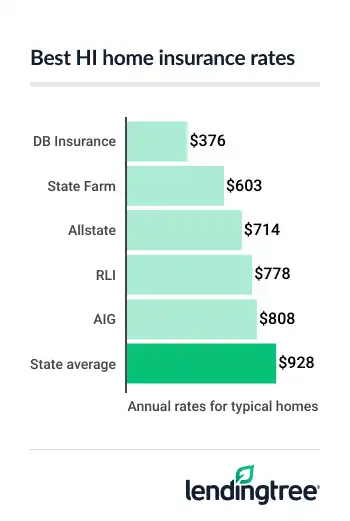

Homeowners who want the cheapest premiums should check DB Insurance, as it has the lowest average rates in the state.

State Farm is the best company in the state for home-auto bundling

Most of the carriers on this list are regional, meaning they are smaller and usually specialize in a limited market. This can be especially important in Hawaii, where coverage needs are unique compared to the mainland.

Best overall homeowners insurance: RLI

Average annual rate: $778

Star rating: N/A

Why we chose it: It’s not always easy finding coverage in Hawaii, but RLI specializes in high-risk policies. Whether you live on the coast or in an older home, RLI may be willing to work with you. It also offers hurricane coverage, even for single-wall construction.

Who it’s best for: Most homeowners in Hawaii, especially those who have been turned down by other carriers due to the unique risks that come with island living.

PROS

- In tune with the coverage needs of Hawaii homeowners

- Policies available for harder-to-insure homes

-

Zero consumer complaints with the National Association of Insurance Commissioners (NAIC)

The NAIC rates companies on confirmed complaints by size. A confirmed complaint is one that leads to a finding of fault.

CONS

- Not the cheapest, on average

- No online quotes or mobile app

Best cheap home insurance: DB Insurance

Average annual rate: $376

Star rating: N/A

Why we chose it: With an average home insurance rate of just $376 a year, DB Insurance is almost 60% lower than the Hawaii state average. On top of that, it has a generous home-and-auto bundling deal, with a 30% discount on each car you insure, plus 10% off your homeowners policy.

Who it’s best for: Hawaii homeowners who are looking for the lowest rates and don’t mind working with a smaller carrier.

PROS

- Lowest average home insurance rates in Hawaii

- Bundling discount applies to both car and home policies

- Smaller, local company for personalized touch

CONS

- Must contact agent for coverage add-on info

- No online quotes or mobile app

- No online customer portal

Best homeowners insurance for bundling: State Farm

Average annual rate: $603

Why we chose it: State Farm is one of the cheapest car insurance companies in Hawaii, but it also offers competitive rates for homeowners insurance. So if you’re looking to switch both your car and home insurance, State Farm should be on your radar.

Who it’s best for: Homeowners who want to switch both their home and auto policies and prefer doing business with a large insurance company.

PROS

- Great for bundling thanks to lower car insurance rates

- Highly rated mobile app and easy-to-use online portal

- Can get a quote online or with a local agent

CONS

-

Separate deductible

for hurricanesYour deductible is your share of repair costs for a covered claim. Your insurance company pays the rest.

- Hurricanes may be excluded altogether

- More consumer complaints than average

Compare home insurance rates and ratings in Hawaii

Every insurance company has its own way of calculating premiums, so quotes can vary wildly between insurers. Comparing home insurance companies can help you find better pricing and coverage.

Below is a comparison, including our own LendingTree ratings, though note that many of the smaller, regional companies are unrated.

| Company | Average annual rate* | LendingTree rating | Complaint rating* | |

|---|---|---|---|---|

| DB Insurance | $376 | N/A | 0.9 | |

| State Farm | $603 | 4/5 | 1.4 | |

| Allstate | $714 | 4/5 | 1.2 | |

| RLI | $778 | N/A | 0.0 | |

| AIG | $808 | N/A | 0.1 | |

| Island Insurance | $812 | N/A | 0.8 | |

| First Insurance Co. of Hawaii | $1,108 | N/A | 2.9 | |

| Ocean Harbor | $2,228 | N/A | 0.7 | |

LendingTree analyzed thousands of quotes from top insurers across Hawaii to identify the best options for homeowners.

Our team evaluated pricing, customer experience, financial reliability and coverage features to determine the top home insurance companies in the state.

See the full methodology.

How much is homeowners insurance in Hawaii?

The average cost of home insurance in Hawaii is $928, or about $77 a month.

Compared to the national average of $2,628, Hawaii home insurance premiums are generally low. But know that your rate will depend a lot on your home’s specs, claims history and other factors.

For example, you’ll likely pay a higher premium for a home with a wood frame compared to one made of block, which better withstands risks like wind and wildfire.

Average home insurance rates by dwelling coverage amount

Insurance premiums depend on the amount of coverage you have. Dwelling is included in standard homeowners insurance policies and pays to repair or rebuild your house and attached structures after a covered loss. You’ll typically see this as “Coverage A” on your quotes and policy paperwork.

Insurance companies use tools to help decide how much dwelling coverage you need. Your dwelling limit should generally be high enough to pay to rebuild your home, based on current construction costs.

Home insurance rates by dwelling coverage

| Company | $300,000 | $400,000 | $550,000 | $750,000 |

|---|---|---|---|---|

| DB Insurance | $278 | $376 | $525 | $720 |

| RLI | $620 | $778 | $1,012 | $1,326 |

| State Farm | $505 | $603 | $751 | $932 |

| State average | $709 | $928 | $1,273 | $1,708 |

Hawaii home insurance rates by city

Where you live within a state also determines how much home insurance costs. Every ZIP code and neighborhood has its own unique risks.

However, Hawaii shares many of the same statewide risk factors, like hurricanes and high construction costs. That means rates vary less widely by location, compared to many other states.

Across all of the cities we analyzed, average home insurance rates were in a tight range of $925 to $931 a year.

| City | Average rate |

|---|---|

| Ahuimanu | $925 |

| Aiea | $925 |

| Ainaloa | $931 |

| Anahola | $931 |

| Camp H M Smith | $925 |

| Captain Cook | $931 |

| Eleele | $931 |

| Ewa Beach | $925 |

| Ewa Gentry | $925 |

| Ewa Villages | $925 |

| Fern Acres | $931 |

| Fort Shafter | $925 |

| Haiku | $931 |

| Haiku-Pauwela | $931 |

| Hakalau | $931 |

| Halaula | $931 |

| Halawa | $925 |

| Haleiwa | $925 |

| Haliimaile | $931 |

| Hana | $931 |

| Hanalei | $931 |

| Hanamaulu | $931 |

| Hanapepe | $931 |

| Hauula | $925 |

| Hawaii National Park | $931 |

| Hawaiian Acres | $931 |

| Hawaiian Beaches | $931 |

| Hawaiian Ocean View | $931 |

| Hawaiian Paradise Park | $931 |

| Hawi | $931 |

| Heeia | $925 |

| Hickam Housing | $925 |

| Hilo | $931 |

| Holualoa | $931 |

| Honalo | $931 |

| Honaunau | $931 |

| Honaunau-Napoopoo | $931 |

| Honokaa | $931 |

| Honolulu | $925 |

| Honomu | $931 |

| Hoolehua | $931 |

| Iroquois Point | $925 |

| JBPHH | $925 |

| Kaaawa | $925 |

| Kaanapali | $931 |

| Kahaluu | $925 |

| Kahaluu-Keauhou | $931 |

| Kahuku | $925 |

| Kahului | $931 |

| Kailua | $928 |

| Kailua Kona | $931 |

| Kalaheo | $931 |

| Kalaoa | $931 |

| Kalaupapa | $931 |

| Kamuela | $931 |

| Kaneohe | $925 |

| Kaneohe Station | $925 |

| Kapaa | $931 |

| Kapaau | $931 |

| Kapalua | $931 |

| Kapolei | $925 |

| Kaumakani | $931 |

| Kaunakakai | $931 |

| Keaau | $931 |

| Kealakekua | $931 |

| Kealia | $931 |

| Keauhou | $931 |

| Kekaha | $931 |

| Keokea | $931 |

| Kihei | $931 |

| Kilauea | $931 |

| Ko Olina | $925 |

| Koloa | $931 |

| Kualapuu | $931 |

| Kula | $931 |

| Kunia | $925 |

| Kurtistown | $931 |

| Lahaina | $931 |

| Laie | $925 |

| Lanai City | $931 |

| Launiupoko | $931 |

| Laupahoehoe | $931 |

| Lawai | $931 |

| Lihue | $931 |

| Maalaea | $931 |

| Mahinahina | $931 |

| Maili | $925 |

| Makaha | $925 |

| Makakilo | $925 |

| Makawao | $931 |

| Makaweli | $931 |

| Maunaloa | $931 |

| Maunawili | $925 |

| MCBH Kaneohe Bay | $925 |

| Mililani | $925 |

| Mililani Mauka | $925 |

| Mililani Town | $925 |

| Mokuleia | $925 |

| Mountain View | $931 |

| Naalehu | $931 |

| Nanakuli | $925 |

| Nanawale Estates | $931 |

| Napili-Honokowai | $931 |

| Ninole | $931 |

| Ocean Pointe | $925 |

| Ocean View | $931 |

| Olinda | $931 |

| Omao | $931 |

| Ookala | $931 |

| Orchidlands Estates | $931 |

| Paauilo | $931 |

| Pahala | $931 |

| Pahoa | $931 |

| Paia | $931 |

| Papaaloa | $931 |

| Papaikou | $931 |

| Pearl City | $925 |

| Pepeekeo | $931 |

| Poipu | $931 |

| Princeville | $931 |

| Puako | $931 |

| Puhi | $931 |

| Pukalani | $931 |

| Punaluu | $925 |

| Pupukea | $925 |

| Puunene | $931 |

| Royal Kunia | $925 |

| Schofield Barracks | $925 |

| Tripler Army Medical Center | $925 |

| Volcano | $931 |

| Wahiawa | $925 |

| Waialua | $925 |

| Waianae | $925 |

| Waihee-Waiehu | $931 |

| Waikane | $925 |

| Waikapu | $931 |

| Waikele | $925 |

| Waikoloa | $931 |

| Waikoloa Village | $931 |

| Wailea | $931 |

| Wailua | $931 |

| Wailua Homesteads | $931 |

| Wailuku | $931 |

| Waimalu | $925 |

| Waimanalo | $925 |

| Waimanalo Beach | $925 |

| Waimea | $931 |

| Wainaku | $931 |

| Wainiha | $931 |

| Waipahu | $925 |

| Waipio | $925 |

| Waipio Acres | $925 |

| Wake Island | $925 |

| West Loch Estate | $925 |

| Wheeler AFB | $925 |

| Wheeler Army Airfield | $925 |

| Whitmore Village | $925 |

Current state of homeowners insurance in Hawaii

Hawaii may have cheaper-than-average homeowners insurance premiums, but there is trouble in paradise. Catastrophes like the Maui wildfire, along with ballooning construction costs, have led to instability.

Two insurers have recently stopped doing business in Hawaii: UPC, which announced in the summer of 2023 that it would be leaving the state, and DTRIC, which followed in the fall of 2025. Others have started to place restrictions on hurricane coverage or are excluding it altogether.

What to do if your insurer won’t renew you

-

Start by shopping the private market

Compare quotes from the best home insurance companies, and not just with big national names. Hawaii has many regional insurers, so consider working with an independent agent or using a marketplace like LendingTree to compare multiple companies at once. -

If needed, consider coverage through the HPIA

The Hawaii Property Insurance Association (HPIA) is the state’s insurer of last resort for homeowners who can’t find coverage on the private market. Premiums tend to be high, and the coverage is basic, but something is better than nothing when you have mortgage requirements to meet. Speak to a Hawaii-licensed agent for more info.

How to compare homeowners insurance in Hawaii

When comparing options, don’t just look at rates, but also consider:

- Coverage limits and add-ons: Make sure limits and the type of coverage included are the same across quotes. One quote may seem lower than another simply because it provides less protection.

- Deductibles: Some companies require a separate deductible for hurricane damage. This can make coverage cheaper, but it may increase your out-of-pocket cost when filing a claim.

- Exclusions: Some insurers may exclude hurricane coverage. Unless you have no choice, choose a quote that doesn’t have this exclusion. Hawaii-specific carriers may be more likely to include this coverage, knowing how important it is when living on the islands.

And if you own one or more vehicles, consider bundling your home and auto insurance. Many insurance companies offer big discounts for this.

How LendingTree helps you find the right policy

Shopping for home insurance isn’t always straightforward, especially when availability and pricing can vary widely. LendingTree makes it easier by helping you explore options from multiple insurers so you can find coverage that fits your home, location and budget.

How it works

Tell us about your home

Answer a few quick questions about your home, location and coverage needs.

Compare options from insurers

See quotes and typical rates from insurers that offer coverage in your area.

Choose the right policy

Review your options and pick the coverage that fits your needs and budget.

Frequently asked questions

Standard homeowners policies typically cover wildfire damage. But read your quote carefully, especially as wildfires become more common and costly. Some carriers may exclude wildfire coverage or issue it with a separate deductible in high-risk areas.

Standard homeowners insurance can cover some damage caused by a volcanic eruption, but check your policy documents to be sure. Earthquakes and landslides are not covered, even if associated with a volcanic event. For that, you need a policy endorsement or, more commonly, an earthquake policy.

Standard homeowners insurance doesn’t cover flooding. Some companies offer flood endorsements, or you can purchase a separate flood insurance policy.

Methodology

How we chose the best homeowners insurance in Hawaii

The rates shown in this article are based on an analysis of non-binding quotes obtained in February 2026 from Quadrant Information Services for sample homes in every Hawaii ZIP code. Unless otherwise noted, policies include:

- Dwelling coverage: $400,000

- Other structures: $40,000

- Personal property: $200,000

- Loss of use: $80,000

- Personal liability: $100,000

- Guest medical payments: $5,000

- Deductible: $1,000

How we create LendingTree ratings

Our team of insurance experts evaluates insurance companies across several categories, including average rates, discounts, coverage options, third-party customer service ratings and app/website experience. We use this information to create LendingTree ratings, which help us identify and recommend the best insurance companies for consumers.

For third-party customer service ratings, we included NAIC’s Complaint Index scores and financial strength ratings from A.M. Best. NAIC Complaint Index scores show how well companies treat customers over things like claims, while financial strength ratings from A.M. Best reflect the ability to pay out claims.

See our home insurance ratings methodology and full editorial guidelines for further details.