66% of Drivers Would Share Driving Data to Lower Insurance Rates

Telematics-based car insurance programs, which track driving behavior to determine premiums, are becoming increasingly mainstream. According to our survey of 2,000 U.S. consumers, drivers aren’t only aware of these programs, but many would willingly share their data if it meant saving money.

Here’s what our survey reveals about how Americans feel about letting their insurer monitor their driving.

- Awareness of telematics-based insurance programs is strong. 78% of drivers are familiar with telematics insurance programs, and 26% are currently enrolled, with participation highest among Gen Z drivers (40%).

- Most drivers would participate if it meant saving money. 66% of drivers say they’d be comfortable sharing driving data with their insurer if it led to lower premiums, and 58% believe their insurance costs would decrease by enrolling in such programs. The most common types of data that drivers would be willing to share include total mileage driven (59%), seat belt usage (56%) and speed (51%).

- Some drivers still express concern about telematics programs. While 51% of drivers at least somewhat trust auto insurance companies to use telematics fairly, 22% say they distrust them. The most common concerns include potential rate increases or reduced discounts (22%), data being shared or sold (20%) and insurers collecting too much information about where they go (16%). Additionally, 32% of drivers would feel uncomfortable with insurers collecting their precise location.

- Most telematics participants report a positive overall experience. 34% of drivers who’ve been enrolled in telematics-based programs say they lowered their insurance costs by more than expected. Additionally, 62% say their experience with insurance telematics was better than they expected.

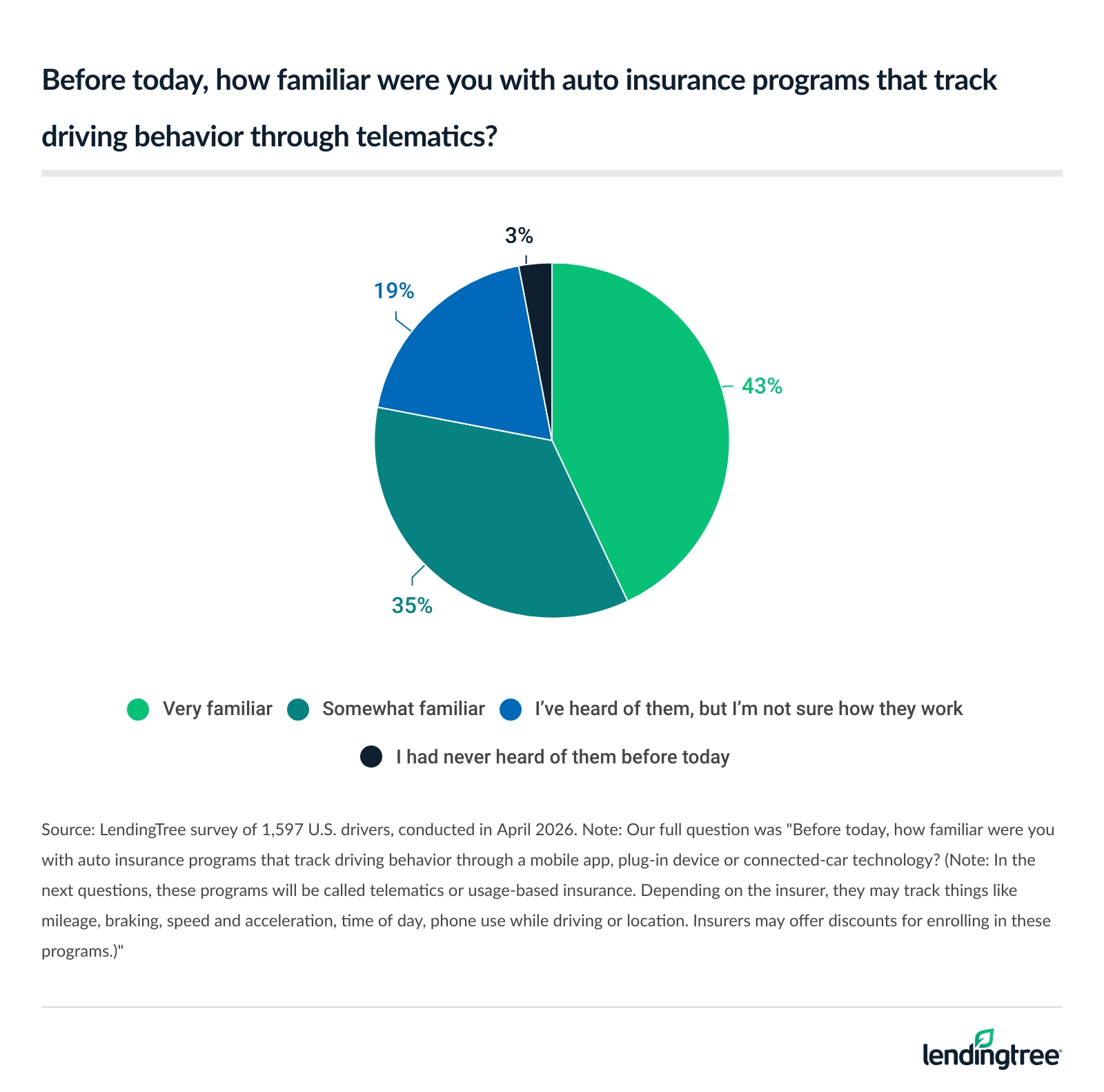

Most drivers know about telematics insurance

In total, 78% of drivers are familiar with telematics insurance programs, while over a quarter (26%) are currently enrolled. Meanwhile, 24% say they’ve never been offered a telematics program but would consider it if they were.

Why hasn’t awareness translated into higher enrollment? According to LendingTree car insurance expert Lindsay Bishop, the gap largely comes down to trust and understanding.

“People may be hesitant to sign up because of concerns about how their data will be used,” she says. “Telematics programs can also have complicated rules, which make people unsure about whether they’ll save money.”

By age group, Gen Z drivers ages 18 to 29 (40%) are the most likely to currently use telematics. That’s followed by millennials ages 30 to 45 (33%). Meanwhile, baby boomers ages 62 to 80 (15%) and Gen Xers ages 46 to 61 (20%) are the least likely.

As for why younger consumers are leading the charge, Bishop points to both comfort and financial incentive. “Younger drivers may be more open to telematics because they’re more comfortable sharing data through apps and connected devices in their daily lives, so telematics doesn’t feel as unfamiliar or intrusive,” she says. “At the same time, younger drivers typically pay higher premiums, so they have more to gain from programs that reward safe driving with discounts.”

Majority of drivers would enroll — if the price was right

Money is the deciding factor for most drivers, as 66% of drivers say they’d be comfortable sharing driving data with their insurer if it led to lower premiums.

And many do believe it would help: Separately, 58% believe their insurance costs would decrease by enrolling in such programs. Drivers would be most willing to share total mileage driven, with 59% being open to it. Seat belt usage (56%) and speed (51%) follow. Other common data points that drivers would share include:

- Time of day driven (49%)

- Crash or air bag-detection data (46%)

- Hard braking or rapid acceleration (41%)

- Phone use while driving (37%)

- Routes or places visited (31%)

- Precise location or GPS data (28%)

As for what discount would seal the deal, 28% of those not currently enrolled say the smallest discount they’d take to consider telematics would be 20% or more, while 25% would take a discount between 10% and 14%.

That said, savings don’t always match expectations. “Many programs offer small upfront discounts of around 10%, with the opportunity to earn larger savings over time,” Bishop says. “But even a 10% sign-up discount could make a telematics program worth it. With the average cost of full coverage car insurance at $208 a month, a 10% savings could mean an extra $250 a year.”

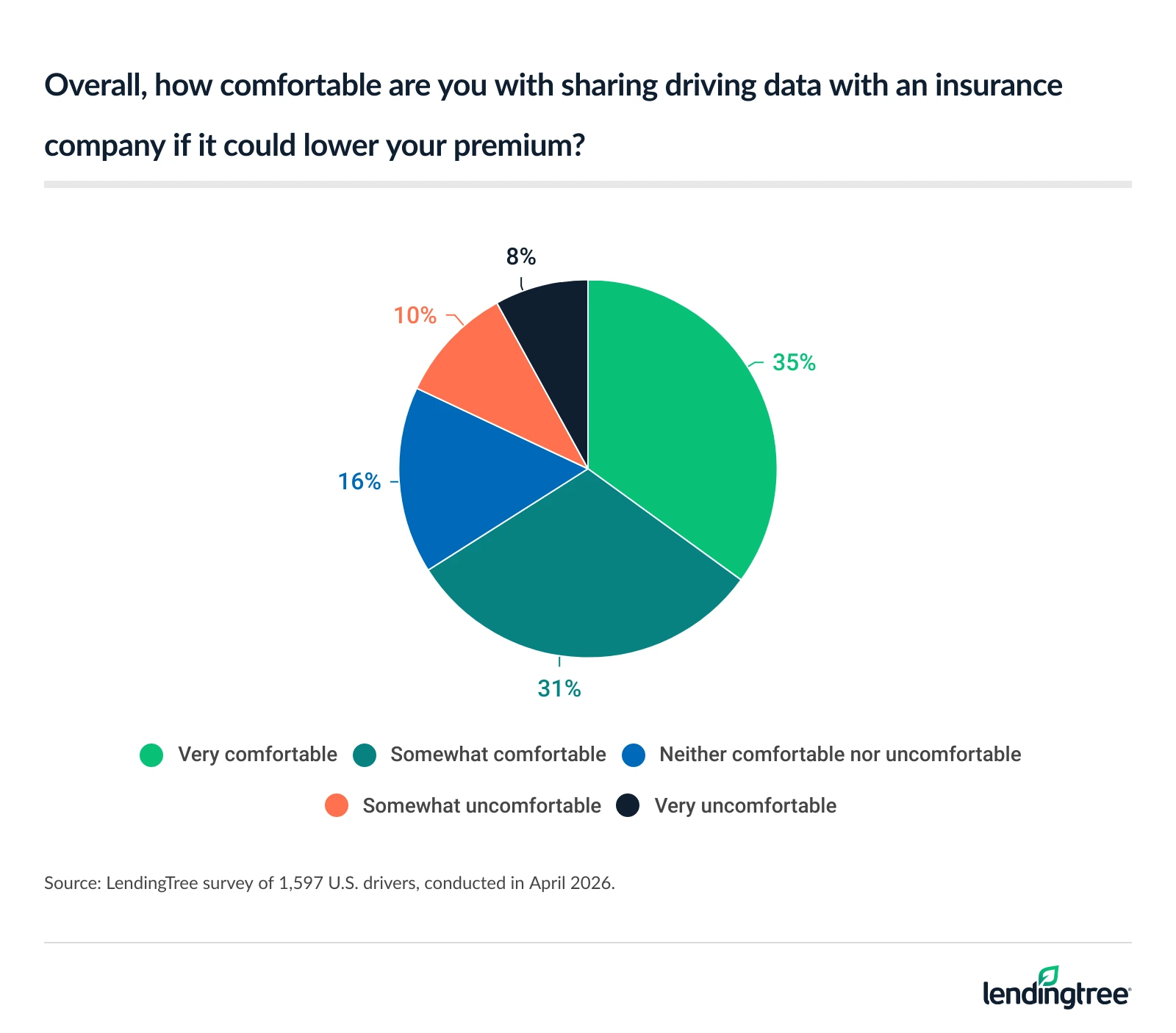

Trust isn’t universal, and privacy concerns are real

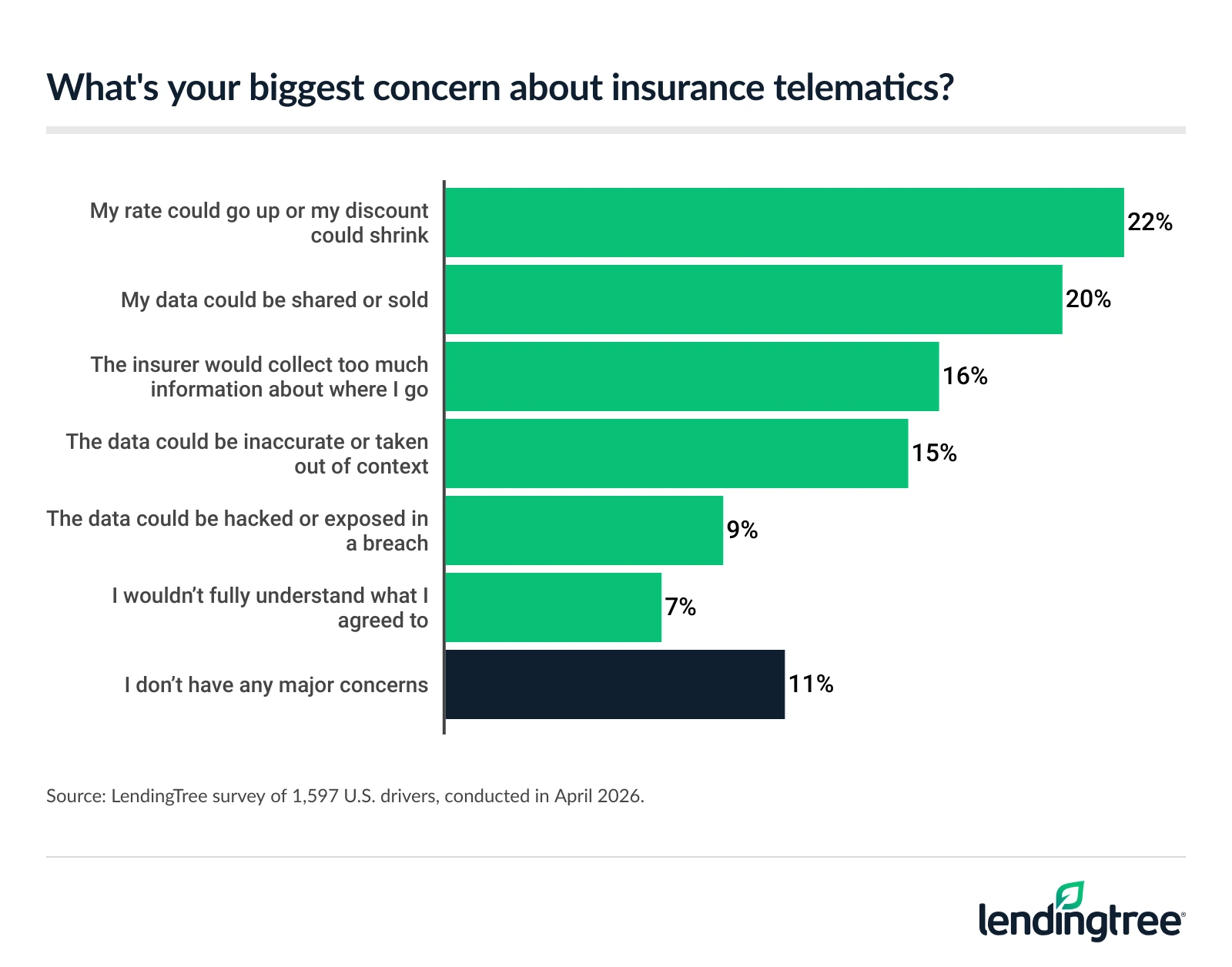

Despite the openness to savings, not everyone is comfortable with telematics. While 51% of drivers at least somewhat trust auto insurance companies to use telematics fairly, a significant 22% say they distrust them.

Most commonly, drivers are concerned about potential rate increases or reduced discounts (22%) as a result of participating. Close behind are concerns about data being shared or sold (20%). Another 16% say they’re nervous about insurers collecting too much information about where they go.

Separately, 32% of drivers would feel uncomfortable with insurers collecting their precise location.

Bishop believes this distrust mostly comes down to uncertainty about how data is being used and who it’s shared with. “Location tracking feels personal, and many drivers aren’t comfortable sharing where they go, even if it means a lower car insurance bill,” she says. “There’s also a transparency issue. Many programs don’t clearly explain how driving behavior translates into a discount. When people don’t fully understand the trade-offs, they’re more likely to sit on the sidelines.”

Transparency could certainly help bridge the gap, as a whopping 61% of drivers would be more willing to enroll in telematics if they could see what telematics data was collected, download it and request deletion after leaving the program.

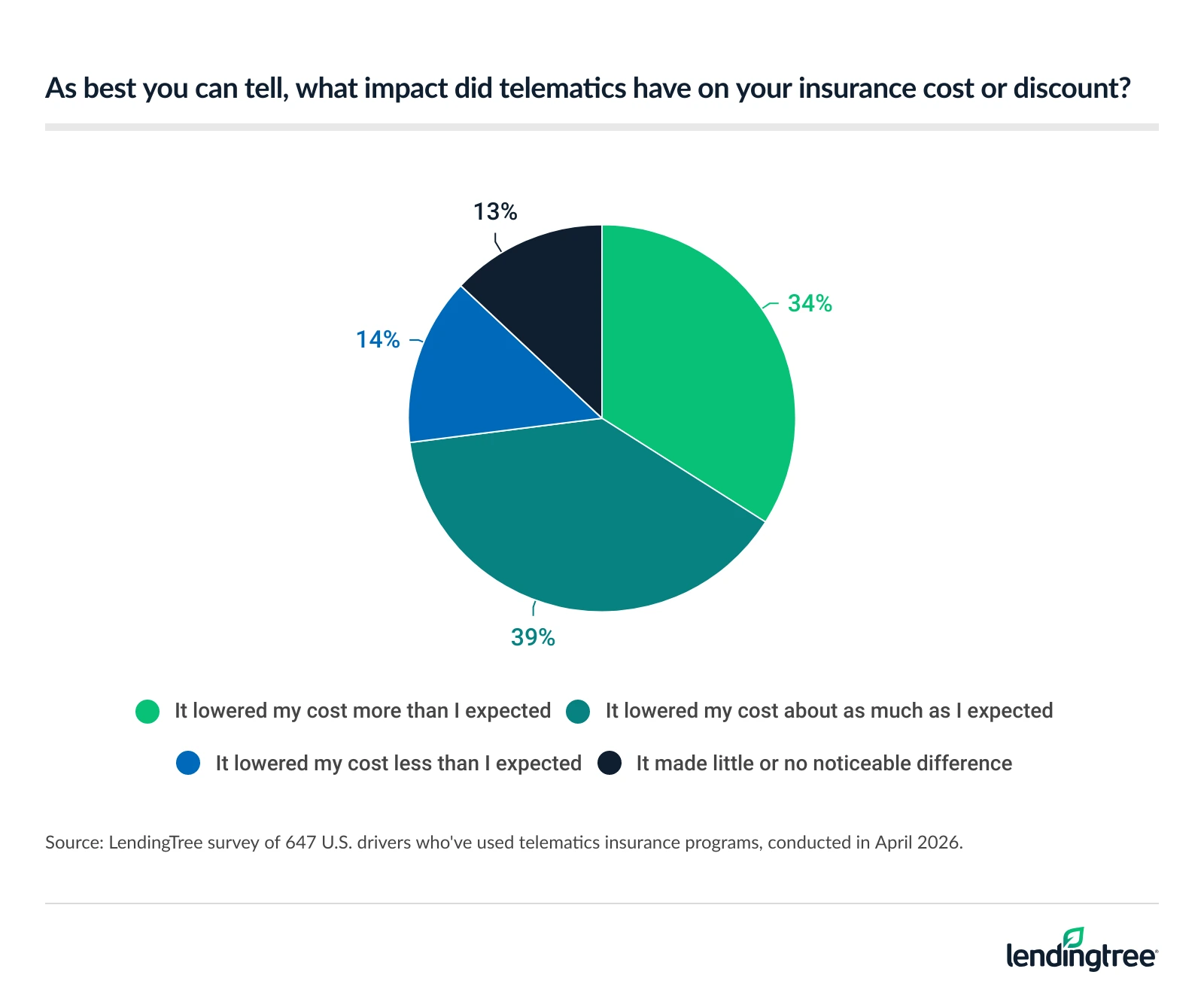

Those already enrolled report better-than-expected results

For those who’ve taken the plunge into telematics, the experience has largely been positive. Among drivers who’ve been enrolled in a telematics program, 34% say they lowered their insurance costs by more than expected.

Meanwhile, 62% say their overall experience with insurance telematics was better than they expected.

Bishop attributes this partly to misconceptions that dissolve once drivers are enrolled. “One of the biggest misconceptions is that your rates will go up if you’re not a ‘perfect’ driver,” she says. “In reality, most programs reward people who mostly show responsible driving habits instead of penalizing people for isolated mistakes.”

Privacy fears also tend to ease with experience. “People often assume insurance companies are closely tracking everything they do,” Bishop says. “But most programs focus on behaviors like speed, hard braking and mileage, which can feel less intrusive than the overall idea of location tracking.”

Enrollment is expected to rise: Among those not currently enrolled in a telematics program, 29% say they’re likely to enroll in one in the next 12 months. That figure rises to 52% among Gen Z drivers.

How to decide if telematics insurance is right for you: Expert tips

Telematics-based insurance goes by a few names: You may see it called usage-based insurance or, for low-mileage drivers, pay-per-mile insurance. Whatever the label, Bishop says the decision of whether to partake comes down to three things: your driving habits, your comfort with data sharing and the potential discount on the table. Here’s a breakdown:

- Honestly assess your driving habits. “If you speed, brake hard or drive late at night, your savings may be limited,” Bishop says. If you’re nervous about your driving habits, consider programs from insurers like State Farm, Nationwide and USAA, all of which won’t raise your rates if you get a bad driving score.

- Look at how the program handles privacy. If you’re concerned about ongoing tracking, companies like Liberty Mutual and Travelers only monitor driving for a limited period, which can feel less intrusive.

- Compare the potential upside. The discount range varies significantly by company. Some insurers, like Allstate and Nationwide, advertise discounts of up to 40%, while others, like Geico, offer closer to 10% — and many still raise rates. “Understanding the ceiling and risk before you enroll is key to deciding whether the trade-offs are worth it to you,” Bishop says.

Methodology

LendingTree commissioned QuestionPro to conduct an online survey of 2,000 U.S. consumers ages 18 to 80 on April 13-17, 2026. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. Researchers reviewed all responses for quality control.

We defined generations as the following ages in 2026:

- Generation Z: 18 to 29

- Millennial: 30 to 45

- Generation X: 46 to 61

- Baby boomer: 62 to 80