Average Credit Card Interest Rate in US Today

The average U.S. credit card interest rate remained at 23.79% in July, marking the second straight month — and third in the past four — that the rate was unchanged.

LendingTree analyzes approximately 220 of the most popular credit cards from more than 50 issuers to track trends in credit card interest rates. The latest findings are published here.

What’s the average interest rate on new credit card offers?

The average APR on a new credit card offer is 23.79%, unchanged from June.

| Category | Min. APR | Max. APR | Avg. | Prior month |

|---|---|---|---|---|

| Avg. APR for all new credit card offers | 20.18% | 27.41% | 23.79% | 23.79% |

| 0% balance transfer credit cards | 17.60% | 26.80% | 22.20% | 22.19% |

| No-annual-fee credit cards | 19.62% | 26.94% | 23.28% | 23.29% |

| Rewards credit cards | 19.90% | 27.54% | 23.72% | 23.72% |

| Cash back credit cards | 20.17% | 27.46% | 23.82% | 23.82% |

| Travel rewards credit cards | 19.43% | 28.01% | 23.72% | 23.71% |

| Airline credit cards | 19.43% | 28.63% | 24.03% | 24.03% |

| Hotel credit cards | 19.39% | 28.39% | 23.89% | 23.86% |

| Low-interest credit cards | 13.30% | 21.31% | 17.31% | 17.31% |

| Grocery rewards credit cards | 19.90% | 27.76% | 23.83% | 23.81% |

| Gas rewards credit cards | 20.50% | 27.51% | 24.00% | 23.98% |

| Dining rewards credit cards | 19.36% | 27.69% | 23.52% | 23.52% |

| Student credit cards | 17.49% | 27.09% | 22.29% | 22.29% |

| Secured credit cards | 26.09% | 26.09% | 26.09% | 26.09% |

This is the second straight month (and third in the past four) that the average has remained unchanged. It marks the first time rates have gone unchanged in back-to-back months since at least 2019, the first year LendingTree began tracking credit card rates monthly.

Why this newfound stability? Historically, most credit card issuers don’t tend to move their rates much unless forced to do so by the Federal Reserve. Unlike mortgage and auto loan rates, most credit card rates are directly tied to the Fed’s rate movements. If the Fed raises or lowers rates by a quarter-point, the interest rates on most U.S. credit cards will move in the same direction by the same amount within a few months. If the Fed sits on its hands, as it has done throughout 2026, credit card rates likely won’t move much. That’s what we’re seeing today.

The Fed held rates steady in January, March, April and June and is widely expected to do the same in July. Some analysts have even suggested that the Fed’s next move later this year, possibly as early as September, could be a rate increase rather than a cut. If that happens, it would be the first rate hike since July 2023.

Unfortunately for those struggling with card debt, that means there’s little reason to expect significant relief in the near term. With the Fed unlikely to cut rates over the next few months, consumers should prepare for borrowing costs to remain elevated for the foreseeable future.

Issuers offer a range of possible rates based on whether you have good or bad credit. The better your credit, the lower the rate you can typically expect. But that’s not guaranteed, as issuers consider various factors when approving you for a new card account.

Borrowers with really good credit currently receive average APR offers of 20.18%, while those with really crummy credit are offered an average APR of 27.41%. That’s a substantial gap.

For example, consider a borrower with a $7,000 balance who makes monthly payments of $250. Using our credit card interest calculator:

- With an APR of 27.41%, the borrower would pay $4,296 in interest and need 45 months to eliminate the balance.

- At a 20.18% APR, interest costs would fall to $2,542 and the balance would be repaid in 38 months.

- That’s a savings of $1,754 in interest and seven months in repayment time. For many households, savings of that magnitude can have a meaningful impact on financial flexibility.

- Balance Payoff in:

- 36 months

- Monthly Payment:

- $198.77

- Principal

- $5,000.00

- Interest

- $2,155.82

This calculator is a self help tool and is not intended to provide financial advice to its users. We cannot guarantee the accuracy of results when applied to a user’s individual factors.

One encouraging sign is that the average FICO Score in the U.S. was 713 in September 2025, according to Experian, compared with 715 in September 2023. That suggests many consumers may be positioned to qualify for lower APR offers. For those who aren’t, borrowing costs can rise quickly.

The type of card you shop for also affects the APR you can expect. For example, we found that cash back cards and 0% balance transfer cards tend to have lower APRs than airline-branded travel rewards cards. (That’s true even when you exclude the 0% offer.) Meanwhile, secured credit cards — which require a deposit to open and are typically held by individuals new to credit or rebuilding their credit — have the highest APRs overall.

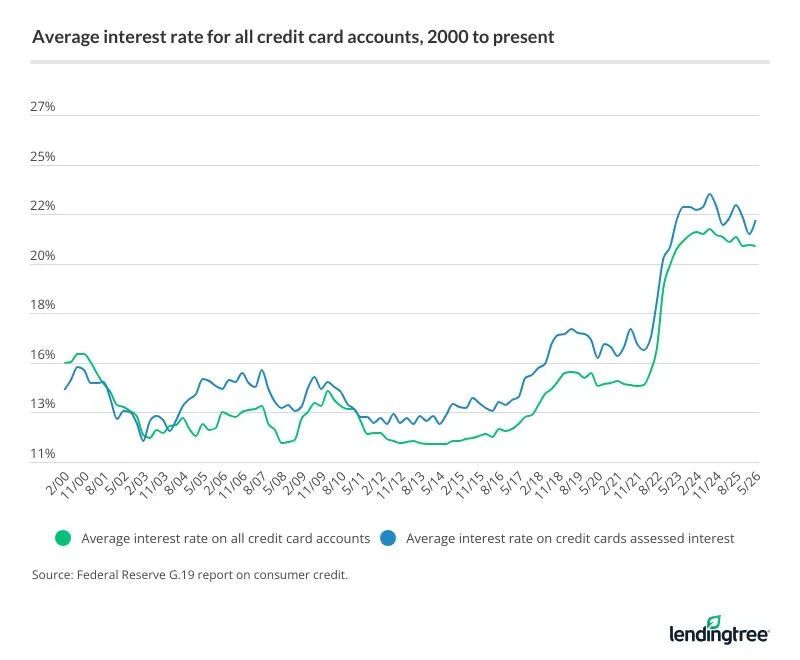

What’s the average interest rate on current credit card accounts?

| Category | Avg. APR |

|---|---|

| All credit card accounts | 20.94% |

| Accounts assessed interest | 22.15% |

Each quarter, the Federal Reserve releases data on credit cards held by U.S. consumers. The report includes the average interest rate on accounts assessed interest — those that carry balances from month to month — as well as the average rate across all credit card accounts.

The distinction between these two measures is important because many cardholders don’t carry balances and therefore never pay interest. The average APR across all accounts was 20.94% in the second quarter of 2026, down slightly from 21.00% in Q1 2026.

Meanwhile, the average APR for accounts accruing interest rose to 22.15% in Q2 2026 from 21.52% in Q1. This measure is particularly significant because it reflects the rates paid by consumers who carry balances and incur interest charges. For cardholders who pay their balances in full each month, APR is largely irrelevant because interest never accrues.

Although both averages remain elevated, they are below their record highs. Both records were set in Q3 2024, when the average APR across all accounts reached 21.76% and the average for accounts accruing interest climbed to 23.37%.

How have credit card interest rates changed over the years?

Credit card interest rates have experienced significant swings over the past decade, largely in response to Federal Reserve policy. Rates generally rose from 2015 through 2019 as the Fed steadily increased its benchmark rate. In 2020, the Fed sharply lowered rates in response to the economic disruption caused by the COVID-19 pandemic. The Fed then reversed course in 2022, implementing seven rate hikes to combat inflation, followed by four additional increases in 2023. Since then, the Fed has cut rates three times in late 2024 and three more times in late 2025.

Before 2015, credit card rates were relatively stable following the implementation of the Credit Card Accountability, Responsibility and Disclosure Act of 2009, commonly known as the Credit CARD Act. Signed into law by President Barack Obama, the legislation introduced sweeping consumer protections, including restrictions on when issuers could raise interest rates, new rules governing payment allocation and limits on certain fees. In the years immediately following the law’s enactment, issuers adjusted pricing and product strategies to offset lost revenue. That transition contributed to a period of rate volatility, during which some cards briefly carried exceptionally high APRs as lenders tested the market’s tolerance for higher borrowing costs.

Over time, the market settled into a period of relative stability, albeit with generally higher credit card interest rates than before the CARD Act. That stability persisted as the economy recovered from the Great Recession and lasted until the Fed resumed raising rates in 2015. Those increases helped drive credit card APRs to the elevated levels seen today.

What can I do if my interest rate is too high?

Although additional Federal Reserve rate cuts remain possible, credit card interest rates are still near record highs as issuers navigate ongoing economic uncertainty, including elevated consumer debt levels and a weakening labor market. As a result, reducing credit card debt remains one of the most effective ways for consumers to improve their financial position. While that can be difficult, paying down balances can lower interest costs and free up cash for emergency savings.

Consumers may also have more influence over their credit card APRs than they realize. Two strategies, in particular, can help reduce borrowing costs.

Get a 0% balance transfer credit card

First, consider a credit card with a 0% introductory APR offer. Many cards provide promotional periods of 12 to 15 months on purchases and balance transfers, while some extend those offers to 18 or even 24 months. For borrowers carrying substantial credit card debt, temporarily eliminating interest charges on a transferred balance can accelerate repayment and reduce overall borrowing costs. Before applying, review any applicable fees, deadlines and restrictions. Qualifying for these offers typically requires good credit — often a score of 680 or higher — as lenders have become more selective amid economic uncertainty. Consumers with strong credit profiles, however, generally have multiple options available.

Ask your issuer for a lower rate

Second, consider asking your issuer for a lower APR. A June 2026 LendingTree survey found that 84% of cardholders who requested an APR reduction were successful, with respondents reporting an average decrease of 6.3 percentage points. Despite those results, only 23% of cardholders said they had asked. One effective approach is to gather competing credit card offers for which you qualify and use them as leverage during negotiations. For example, you might explain that you’ve received an offer with a significantly lower APR and ask whether your current issuer can match it. While approval isn’t guaranteed, issuers are often willing to work with qualified customers. In most cases, however, you’ll need to initiate the conversation, as lenders rarely offer APR reductions proactively.

Methodology: How we evaluated credit card APRs

To calculate average APRs on new credit card offers, LendingTree reviewed the online terms and conditions of approximately 220 credit cards from more than 50 issuers, including banks and credit unions. We collected the standard purchase APR listed for each card on the issuer’s or retailer’s website. Introductory and promotional APRs were excluded from the analysis.

For APRs on existing credit card accounts, we used data from the Federal Reserve’s most recent G.19 Consumer Credit report.