Best Nevada Homeowners Insurance for 2026

State Farm has the overall best home insurance in Nevada, but Farmers may have more discounts

Advertising Disclosures

Loading Disclosures…

- Low rates and helpful coverage options make State Farm Nevada’s best homeowners insurance company.

- Nevada homeowners insurance costs $1,829 a year, on average.

- The cost of Nevada home insurance is up by 27% since 2020.

- Wildfire risks have made it hard to get home insurance in some parts of Nevada.

Best homeowners insurance companies in Nevada

State Farm is Nevada’s best homeowners insurance company for its cheap rates and helpful coverage options.

Country Financial has the best customer service. It has a better complaint rating from the National Association of Insurance Commissioners (NAIC)

Best overall: State Farm

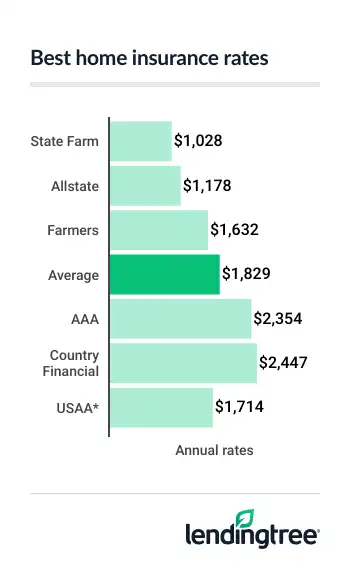

Average annual rate: $1,028

Why we chose it: State Farm has Nevada’s cheapest home insurance and useful coverage options. Its cheap Nevada car insurance makes it affordable to bundle

Who it’s best for: Most Nevada homeowners. In addition to cheap rates, State Farm offers helpful add-ons. These include protections for sewer and drain backups and underground utility lines.

It also offers reasonably priced earthquake coverage. It adds about $30 a month to an insurance quote for a three-bedroom house in Henderson.

PROS

- Cheapest home insurance in Nevada

- Low car insurance rates make it good for bundling

- Useful add-ons let you customize your protections

CONS

- Complaint score is worse than average

Best customer service: Country Financial

Average annual rate: $2,447

Why we chose it: Country Financial’s 0.1 NAIC score means it has one-tenth as many complaints as average. This means it does a good job of coming through when customers need it the most.

Who it’s best for: People who like personal service. When you request an online quote from Country Financial, an agent gets back to you to go over your options. Its Standard policies offer basic coverage, but you can upgrade to Premier for more protection. The company’s discounts for new and renovated homes, among others, can make it more affordable.

PROS

- Better complaint score than most other companies

- Personalized service in most parts of the state

- Flexible coverage options to fit your budget and needs

CONS

- Charges 34% more than state average before discounts

Best discount opportunities: Farmers

Average annual rate: $1,632

Why we chose it: Farmers rates are 11% less than the state average. It can be your cheapest option if you qualify for enough of its discounts.

Who it’s best for: Teachers, firefighters and engineers. Farmers affinity discounts are available to homeowners in these and certain other professions. Current and former military service members can usually get one, too. When you stack this up with other discounts for things like water leak detectors and newer homes, the savings can add up.

PROS

- Charges 11% less than state average

- Several discounts can make it your cheapest option

- NAIC complaint score is better than average

CONS

- High car insurance rates reduce savings when you bundle

Best for military families: USAA

Average annual rate: $1,714

Why we chose it: USAA generally offers affordable insurance to the military community with good customer service.

Who it’s best for: Military service members and their families. USAA extras include electronics coverage that gives your devices more protection than standard home insurance. If you’re on active duty, USAA covers personally owned military gear with no deductible. Its cheap car insurance rates make it good for bundling.

PROS

- Cheap car insurance makes it good for bundling

- Very good NAIC complaint rating

- Electronics coverage gives your devices extra protection

CONS

- Only available to the military community and their families

- Other companies have cheaper home insurance

Compare Nevada home insurance rates and ratings

Each company’s rates vary by customer. It’s good to compare home insurance quotes from a few companies to find the best rate for your situation.

| Company | Annual rate* | LendingTree rating | Complaint rating* | |

|---|---|---|---|---|

| State Farm | $1,028 | 4/5 | 1.4 | |

| Allstate | $1,178 | 4/5 | 1.2 | |

| Farmers | $1,632 | 3.5/5 | 0.7 | |

| AAA | $2,354 | 2/5 | 0.9 | |

| Country Financial | $2,447 | 4/5 | 0.1 | |

| American Family | $2,451 | 4/5 | 0.4 | |

| USAA* | $1,714 | 4/5 | 0.5 | |

LendingTree analyzed home insurance quotes from every Nevada ZIP code to identify the best options for you.

Our team evaluated pricing, customer experience, financial reliability and coverage features to determine the top home insurance companies in your state.

See our full methodology.

How much is homeowners insurance in Nevada?

Home insurance costs an average of $1,829 a year in Nevada, or $152 a month. This is 30% less than the national average of $2,628 a year.

Average home insurance rates by dwelling coverage amount

The actual price you pay depends on things like your location, your home’s features and your credit history. The amount of coverage you need also impacts your rate.

For example, insuring your home for $550,000 bumps your rate up to $2,420 a year. This is 32% higher than the cost of insurance for a $400,000 policy.

You usually have to insure your home at its replacement value

Home insurance rates by dwelling coverage

| Company | $300,000 | $400,000 | $550,000 | $750,000 |

|---|---|---|---|---|

| State Farm | $842 | $1,028 | $1,388 | $1,792 |

| Farmers | $1,271 | $1,632 | $2,390 | $3,017 |

| Country Financial | $1,966 | $2,447 | $3,212 | $4,283 |

| USAA* | $1,452 | $1,714 | $2,072 | $2,554 |

| State average | $1,462 | $1,829 | $2,420 | $3,121 |

Most insurance companies can help you estimate your home’s replacement value. You can help by providing details about your home, including its:

- Age, square footage and number of floors

- Foundation, roof and garage types

- Flooring, countertop and cabinet materials

You can find most of this information by looking up your home on your county assessor’s website. For an older home, let insurance companies know the year your roofing, wiring and plumbing were last updated.

Nevada home insurance rates by city

At $2,216 a year, Winchester has the most expensive home insurance among Nevada’s cities and towns. Winchester is one of two Clark County towns that are home to the Las Vegas Strip. The other is Paradise, which has the second-highest rate, at $1,996 a year.

A variety of risk factors go into your area’s home insurance costs. These include the potential for wildfires, especially in Northern Nevada, as well as the threat of wind and hail damage. High crime rates can also push up an area’s home insurance costs.

About 100 miles north of Reno, Gerlach has the state’s cheapest home insurance, at $1,564 a year. This is 14% less than the state average.

Reno homeowners pay 7% less than the average, at $1,695 a year. In the city of Las Vegas, home insurance costs $1,918 per year, which is 5% higher than average.

| City | Annual rate |

|---|---|

| Alamo | $1,712 |

| Amargosa Valley | $1,825 |

| Austin | $1,772 |

| Baker | $1,706 |

| Battle Mountain | $1,798 |

| Beatty | $1,707 |

| Blue Diamond | $1,789 |

| Boulder City | $1,632 |

| Bunkerville | $1,629 |

| Cal Nev Ari | $1,728 |

| Caliente | $1,701 |

| Carlin | $1,805 |

| Carson City | $1,667 |

| Cold Springs | $1,645 |

| Coyote Springs | $1,767 |

| Crescent Valley | $1,736 |

| Crystal Bay | $1,663 |

| Dayton | $1,649 |

| Deeth | $1,863 |

| Denio | $1,680 |

| Duckwater | $1,733 |

| Dyer | $1,623 |

| East Valley | $1,619 |

| Elko | $1,843 |

| Ely | $1,700 |

| Empire | $1,631 |

| Enterprise | $1,693 |

| Eureka | $1,750 |

| Fallon | $1,612 |

| Fallon Station | $1,587 |

| Fernley | $1,736 |

| Fish Springs | $1,664 |

| Gabbs | $1,642 |

| Gardnerville | $1,656 |

| Gardnerville Ranchos | $1,624 |

| Genoa | $1,629 |

| Gerlach | $1,564 |

| Glenbrook | $1,726 |

| Golconda | $1,636 |

| Golden Valley | $1,632 |

| Goldfield | $1,692 |

| Hawthorne | $1,655 |

| Henderson | $1,743 |

| Hiko | $1,760 |

| Imlay | $1,591 |

| Incline Village | $1,950 |

| Indian Hills | $1,611 |

| Indian Springs | $1,857 |

| Jackpot | $1,836 |

| Jean | $1,713 |

| Johnson Lane | $1,627 |

| Kingsbury | $1,805 |

| Lakeridge | $1,718 |

| Lamoille | $1,867 |

| Las Vegas | $1,918 |

| Laughlin | $1,817 |

| Lemmon Valley | $1,636 |

| Logandale | $1,600 |

| Lovelock | $1,610 |

| Lund | $1,729 |

| Luning | $1,641 |

| Manhattan | $1,673 |

| Mc Dermitt | $1,588 |

| McGill | $1,754 |

| Mercury | $1,666 |

| Mesquite | $1,668 |

| Mina | $1,565 |

| Minden | $1,584 |

| Moapa | $1,659 |

| Moapa Valley | $1,654 |

| Mogul | $1,645 |

| Montello | $1,862 |

| Mountain City | $1,876 |

| Nellis AFB | $1,861 |

| Nixon | $1,568 |

| North Las Vegas | $1,866 |

| Orovada | $1,654 |

| Overton | $1,671 |

| Owyhee | $1,909 |

| Pahrump | $1,759 |

| Panaca | $1,793 |

| Paradise | $1,996 |

| Paradise Valley | $1,590 |

| Pioche | $1,778 |

| Reno | $1,695 |

| Round Hill Village | $1,766 |

| Round Mountain | $1,731 |

| Ruby Valley | $1,900 |

| Ruhenstroth | $1,612 |

| Ruth | $1,717 |

| Sandy Valley | $1,678 |

| Schurz | $1,572 |

| Searchlight | $1,801 |

| Silver City | $1,614 |

| Silver Springs | $1,788 |

| Silverpeak | $1,611 |

| Sloan | $1,780 |

| Smith | $1,715 |

| Spanish Springs | $1,570 |

| Sparks | $1,584 |

| Spring Creek | $1,917 |

| Spring Valley | $1,865 |

| Stagecoach | $1,779 |

| Stateline | $1,801 |

| Summerlin South | $1,612 |

| Sun Valley | $1,669 |

| Sunrise Manor | $1,938 |

| Tonopah | $1,671 |

| Topaz Ranch Estates | $1,743 |

| Tuscarora | $1,755 |

| Valmy | $1,628 |

| Verdi | $1,720 |

| Virginia City | $1,760 |

| Wadsworth | $1,684 |

| Washoe Valley | $1,682 |

| Wellington | $1,735 |

| Wells | $1,851 |

| West Wendover | $1,848 |

| Whitney | $1,843 |

| Winchester | $2,216 |

| Winnemucca | $1,652 |

| Yerington | $1,715 |

| Zephyr Cove | $1,773 |

Current state of homeowners insurance in Nevada

Nevada homeowners insurance has become more expensive and harder to find in recent years. Statewide, the average price of home insurance has gone up by 27% since 2020.

Meanwhile, wildfire risks have made insurance companies reluctant to insure some homes. Nevada does not have an insurer of last resort like California’s FAIR Plan. If standard insurance companies won’t insure you, you may have to get surplus lines insurance.

Surplus lines companies aren’t in the Nevada Insurance Guaranty Association

Home insurance for Nevada’s natural disasters

Wildfires, earthquakes and flash floods are among Nevada’s most significant natural disaster risks. Standard home insurance covers wildfires in Nevada, but a recently approved law allowing wildfire exemptions may someday change this.

Home insurance does not cover earthquakes or floods. However, you can get separate insurance for each of these risks.

Nevada earthquake insurance

Earthquake insurance is widely available across Nevada. Some companies, including State Farm, offer earthquake protection as an add-on to an existing homeowners policy. A few specialty companies also offer stand-alone earthquake insurance.

Most earthquake policies come with high deductibles. For example, the deductible for State Farm’s earthquake coverage is 10% of your dwelling limit. This adds up to $40,000 for a home insured at $400,000.

In this situation, you won’t get any insurance money for an earthquake causing $35,000 in damage. However, if an earthquake levels your home, the policy covers up to $360,000 of your rebuilding costs.

Flood insurance in Nevada

Flood insurance costs an average of $932 a year in Nevada, or $78 a month.

Most flood insurance is purchased through the government-run National Flood Insurance Program (NFIP). It offers up to $250,000 in building coverage for your home and $100,000 in contents coverage for your belongings.

A few private companies also offer flood insurance. Private flood insurance is sometimes cheaper than NFIP policies, and it usually gives you more coverage choices.

Most standard home insurance companies can get you an NFIP quote. Neptune Flood is a good start for private flood insurance quotes.

How to compare homeowners insurance companies in Nevada

Shopping around can help you save money on homeowners insurance. Consider these tips as you compare quotes:

- Be prepared: It’s good to have details about your home handy when you shop. You can find these on your county assessor’s website or in your home’s inspection report.

- Bundle to save: Most insurance companies give you a generous discount for getting home and auto insurance from them. Get quotes for both policies to see each company’s combined rate.

- Check the details: It’s normal for your coverage limits to vary slightly by company. Make sure the details about you and your home are listed accurately in each quote.

- Compare apples to apples: Your deductible and coverage options should match across all quotes.

- Ask about discounts: Most quotes include some discounts, but you don’t want any to get overlooked.

How LendingTree helps you find the right policy

Shopping for home insurance isn’t always straightforward — especially when availability and pricing can vary widely. LendingTree makes it easier by helping you explore options from multiple insurers so you can find coverage that fits your needs and budget.

How it works

Tell us about your home

Answer a few quick questions about your home, location and coverage needs.

Compare options from insurers

See quotes and typical rates from insurers that offer coverage in your area.

Choose the right policy

Review your options and pick the coverage that fits your needs and budget.

Frequently asked questions

Home insurance is not required by law in Nevada, but lenders usually require it for a mortgage. Some homeowners associations (HOAs) also require it.

If you have a mortgage, you need enough insurance to rebuild your home if a disaster strikes. This is known as your home’s replacement value, which should match your policy’s dwelling limit. It’s also good to get enough personal property coverage to replace your possessions.

Homeowners insurance does not cover floods or earthquakes. It usually doesn’t cover sewer and drain backups unless you buy extra protection for them. Standard home insurance only offers limited coverage for jewelry and other valuables. You can usually buy extra coverage for items like this.

Methodology

How we chose the best homeowners insurance in Nevada

The rates shown in this article are based on an analysis of nonbinding quotes obtained in February 2026 from Quadrant Information Services for sample homes in every Nevada ZIP code. Unless otherwise noted, policies include:

- Dwelling coverage: $400,000

- Other structures: $40,000

- Personal property: $200,000

- Loss of use: $80,000

- Personal liability: $100,000

- Guest medical payments: $5,000

- Deductible: $1,000

How we create LendingTree ratings

Our team of insurance experts evaluates insurance companies across several categories, including average rates, discounts, coverage options, third-party customer service ratings and app/website experience. We use this information to create LendingTree ratings, which help us identify and recommend the best insurance companies for consumers.

For third-party customer service ratings, we included the NAIC’s complaint index scores and financial strength ratings from AM Best. NAIC complaint index scores show how well companies treat customers over things like claims, while financial strength ratings from AM Best reflect the ability to pay out claims.

See our home insurance ratings methodology and full editorial guidelines for further details.

*USAA is only available to current and former members of the military and their families.