Best Vermont Homeowners Insurance for 2026

State Farm, Vermont Mutual and Allstate have some of the best Vermont home insurance

Advertising Disclosures

Loading Disclosures…

- State Farm has the best overall homeowners insurance in Vermont, offering some of the state’s lowest annual rates along with good coverage options.

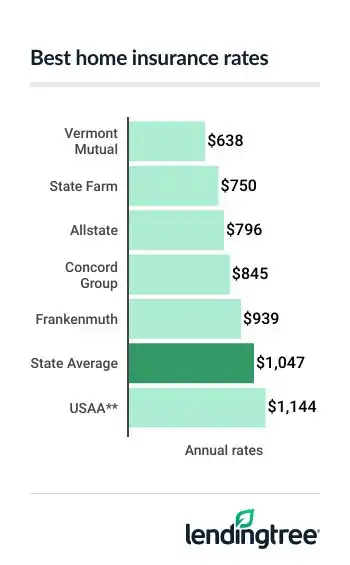

- The average cost of homeowners insurance in Vermont is $1,047 per year, or about $87 per month.

- Home insurance rates in Vermont are some of the lowest in the country and have increased more slowly than in most neighboring states.

Best homeowners insurance in Vermont

The best homeowners insurance companies in Vermont stand out for different reasons, including affordable rates, customer satisfaction and coverage options.

State Farm is the best overall for its low rates and good coverage options. Vermont Mutual is best for people who want a local insurer plus the cheapest rates in the state. Allstate tops the list for discounts, while USAA is best for active-duty service members, veterans and other qualified individuals.

Best overall: State Farm

Average annual rate: $750

Why we chose it: State Farm combines affordable rates with more coverage options than most other companies in the state, making it a solid choice for many Vermont homeowners. In addition to its below-average rates, State Farm’s agent network can make it easier to get personalized guidance when choosing coverage options for your home.

Who it’s best for: Homeowners who want dependable coverage at an affordable price

PROS

- Second-lowest rates in the state

- More coverage options than most competitors

- User-friendly mobile app to help manage policies and claims

CONS

- Gets significantly more customer complaints than average

- Large national company that may not meet certain regional needs

Best for cheap coverage: Vermont Mutual

Average annual rate: $638

Why we chose it: Vermont Mutual has the lowest average homeowners insurance rate among the companies featured in this review. The company also receives very few customer complaints, according to the National Association of Insurance Commissioners (NAIC)

Who it’s best for: Homeowners looking for affordable, reliable coverage from a Vermont-based insurer

PROS

- Lowest average rate in the state

- Deep roots in the local market

- Very few customer complaints

CONS

- Only operates through independent agents

- No online quotes

Best for discounts: Allstate

Average annual rate: $796

Why we chose it: Allstate gives Vermont homeowners several opportunities to lower their already relatively low annual rates. Homeowners may qualify for discounts by bundling policies, installing protective devices and taking advantage of other savings opportunities.

Who it’s best for: Vermont homeowners who want multiple opportunities to save on their insurance premiums

PROS

- Wide variety of discounts

- Lower-than-average annual rates

- Generous discount for bundling home and car coverages

CONS

- Higher-than-average number of customer complaints

- Not the cheapest insurance option in the state

Best for military families: USAA

Average annual rate: $1,144

Why we chose it: USAA offers slightly higher rates than the state average, but their strong customer satisfaction and specialized care for active-duty military members, veterans and their spouses can make the slightly higher price worth it.

Who it’s best for: Active-duty military members, veterans and eligible family members who value affordable coverage and personalized service

PROS

- Fewer customer complaints than expected for an insurer its size

- Active-duty service members get coverage for military equipment and uniforms with no deductible

- Eligibility extends to children of USAA members

CONS

- Coverage is only available to military members, veterans, their spouses and certain eligible others

- Higher-than-average annual rates

Compare home insurance rates and ratings in Vermont

| Company | Average annual rate* | LendingTree rating | NAIC complaint rating* | |

|---|---|---|---|---|

| Vermont Mutual | $638 | 3.5/5 | 0.1 | |

| State Farm | $750 | 4.5/5 | 1.4 | |

| Allstate | $796 | 3/5 | 1.2 | |

| Concord Group | $845 | 4/5 | 0.0 | |

| Frankenmuth | $939 | 4/5 | 0.1 | |

| Travelers | $1,056 | 4.5/5 | 0.7 | |

| Union Mutual | $1,014 | N/A | 0.0 | |

| USAA** | $1,144 | 4/5 | 0.5 | |

Home insurance rates in Vermont can vary significantly between insurers. Comparing quotes from multiple companies may help you find better rates and coverage.

LendingTree analyzed thousands of quotes from top insurers across Vermont to identify the best options for homeowners.

Our team evaluated pricing, customer experience, financial reliability and coverage features to determine the top home insurance companies in the state.

See full methodology.

How much is homeowners insurance in Vermont?

The average cost of home insurance in Vermont is $1,047 per year, or about $87 per month.

Average homeowners insurance rates in Vermont are 60% lower than the national average of $2,628 per year. The state faces fewer large-scale weather disasters than many coastal areas and states prone to wildfires and tornadoes, which helps keep insurance costs lower.

Still, rates can vary significantly based on your home’s location, age and coverage needs. Comparing quotes from multiple insurers may help you find lower rates without sacrificing coverage.

Average home insurance rates by dwelling coverage amount

Home insurance rates for Vermont homeowners typically increase as your dwelling coverage rises.

| Company | $300,000 | $400,000 | $550,000 | $750,000 |

|---|---|---|---|---|

| State Farm | $627 | $750 | $910 | $1,108 |

| Vermont Mutual | $523 | $638 | $827 | $1,117 |

| Allstate | $646 | $796 | $949 | $1,144 |

| USAA** | $915 | $1,144 | $1,454 | $1,839 |

| State average | $821 | $1,047 | $1,344 | $1,714 |

Home insurance rates in Vermont by city

Home insurance rates can vary across Vermont based on factors such as local claim trends, rebuilding costs and housing characteristics. Hinesburg, Huntington and Charlotte have the lowest average home insurance premiums in the state at $941, $942 and $945 per year, respectively.

West Dummerston, East Poultney and Westminster Station have the highest average home insurance rates in Vermont, with each hovering around $1,100 per year. All three are either located along or near rivers, which makes them more susceptible to flash flooding. The increased risk of flood and water damage likely contributes to their higher home insurance rates.

| City | Average rate |

|---|---|

| Adamant | $1,040 |

| Albany | $1,066 |

| Alburgh | $1,053 |

| Arlington | $1,054 |

| Ascutney | $1,091 |

| Averill | $1,100 |

| Bakersfield | $1,047 |

| Barnet | $1,021 |

| Barre | $1,019 |

| Barton | $1,051 |

| Beebe Plain | $1,103 |

| Beecher Falls | $1,060 |

| Bellows Falls | $1,074 |

| Belmont | $1,053 |

| Belvidere Center | $1,062 |

| Bennington | $1,080 |

| Benson | $1,056 |

| Bethel | $1,052 |

| Bomoseen | $1,067 |

| Bondville | $1,068 |

| Bradford | $1,049 |

| Brandon | $1,051 |

| Brattleboro | $1,075 |

| Bridgewater | $1,043 |

| Bridgewater Corners | $1,038 |

| Bridport | $1,053 |

| Bristol | $1,023 |

| Brookfield | $1,057 |

| Brownsville | $1,072 |

| Burlington | $999 |

| Cabot | $1,022 |

| Calais | $1,055 |

| Cambridge | $976 |

| Cambridgeport | $1,079 |

| Canaan | $1,058 |

| Castleton | $1,068 |

| Cavendish | $1,064 |

| Center Rutland | $1,050 |

| Charlotte | $945 |

| Chelsea | $1,052 |

| Chester | $1,057 |

| Chittenden | $1,071 |

| Colchester | $978 |

| Concord | $1,019 |

| Corinth | $1,048 |

| Craftsbury | $1,027 |

| Craftsbury Common | $1,045 |

| Cuttingsville | $1,049 |

| Danby | $1,067 |

| Danville | $1,020 |

| Derby | $1,064 |

| Derby Line | $1,061 |

| Dorset | $1,071 |

| East Arlington | $1,076 |

| East Barre | $1,017 |

| East Berkshire | $1,050 |

| East Burke | $1,033 |

| East Calais | $1,053 |

| East Charleston | $1,057 |

| East Corinth | $1,057 |

| East Dorset | $1,048 |

| East Dover | $1,068 |

| East Fairfield | $1,062 |

| East Hardwick | $1,032 |

| East Haven | $1,033 |

| East Middlebury | $1,038 |

| East Montpelier | $1,044 |

| East Poultney | $1,111 |

| East Randolph | $1,059 |

| East Ryegate | $1,030 |

| East St.Johnsbury | $1,057 |

| East Thetford | $1,062 |

| East Wallingford | $1,061 |

| Eden | $1,074 |

| Eden Mills | $1,070 |

| Enosburg Falls | $1,061 |

| Essex Junction | $964 |

| Fair Haven | $1,056 |

| Fairfax | $1,022 |

| Fairfield | $1,035 |

| Fairlee | $1,051 |

| Ferrisburgh | $1,025 |

| Florence | $1,067 |

| Forest Dale | $1,095 |

| Franklin | $1,031 |

| Gaysville | $1,060 |

| Gilman | $1,022 |

| Glover | $1,031 |

| Grafton | $1,069 |

| Grand Isle | $1,045 |

| Graniteville | $1,019 |

| Granville | $1,064 |

| Greensboro | $1,030 |

| Greensboro Bend | $1,029 |

| Groton | $1,022 |

| Guildhall | $1,034 |

| Hancock | $1,075 |

| Hardwick | $1,027 |

| Hartland | $1,062 |

| Hartland Four Corners | $1,090 |

| Highgate Center | $1,050 |

| Highgate Springs | $1,066 |

| Hinesburg | $941 |

| Huntington | $942 |

| Hyde Park | $1,059 |

| Hydeville | $1,065 |

| Irasburg | $1,065 |

| Island Pond | $1,047 |

| Isle La Motte | $1,042 |

| Jacksonville | $1,077 |

| Jamaica | $1,074 |

| Jeffersonville | $1,064 |

| Jericho | $962 |

| Johnson | $1,060 |

| Jonesville | $1,019 |

| Killington | $1,061 |

| Lake Elmore | $1,029 |

| Londonderry | $1,062 |

| Lowell | $1,074 |

| Lower Waterford | $1,057 |

| Ludlow | $1,050 |

| Lunenburg | $1,020 |

| Lyndon Center | $1,029 |

| Lyndonville | $1,029 |

| Manchester | $1,055 |

| Manchester Center | $1,055 |

| Marshfield | $1,054 |

| Mc Indoe Falls | $1,062 |

| Middlebury | $1,038 |

| Middletown Springs | $1,088 |

| Milton | $977 |

| Montgomery Center | $1,050 |

| Montpelier | $1,035 |

| Moretown | $1,028 |

| Morgan | $1,059 |

| Morrisville | $1,037 |

| Moscow | $1,068 |

| Mount Holly | $1,038 |

| New Haven | $1,019 |

| Newbury | $1,032 |

| Newfane | $1,079 |

| Newport | $1,052 |

| Newport Center | $1,063 |

| North Bennington | $1,073 |

| North Clarendon | $1,057 |

| North Concord | $1,019 |

| North Ferrisburgh | $1,018 |

| North Hartland | $1,040 |

| North Hero | $1,046 |

| North Hyde Park | $1,100 |

| North Montpelier | $1,044 |

| North Pomfret | $1,049 |

| North Pownal | $1,058 |

| North Springfield | $1,068 |

| North Thetford | $1,064 |

| North Troy | $1,057 |

| Northfield | $1,021 |

| Northfield Falls | $1,015 |

| Norton | $1,063 |

| Norwich | $1,067 |

| Orleans | $1,065 |

| Orwell | $1,063 |

| Passumpsic | $1,053 |

| Pawlet | $1,073 |

| Peacham | $1,020 |

| Perkinsville | $1,075 |

| Peru | $1,060 |

| Pittsfield | $1,069 |

| Pittsford | $1,060 |

| Plainfield | $1,047 |

| Plymouth | $1,083 |

| Post Mills | $1,055 |

| Poultney | $1,079 |

| Pownal | $1,073 |

| Proctor | $1,073 |

| Proctorsville | $1,074 |

| Putney | $1,069 |

| Quechee | $1,051 |

| Randolph | $1,056 |

| Randolph Center | $1,051 |

| Reading | $1,057 |

| Readsboro | $1,084 |

| Richford | $1,046 |

| Richmond | $949 |

| Ripton | $1,055 |

| Rochester | $1,066 |

| Roxbury | $1,039 |

| Rutland | $1,084 |

| Salisbury | $1,052 |

| Saxtons River | $1,062 |

| Shaftsbury | $1,089 |

| Sharon | $1,060 |

| Sheffield | $1,061 |

| Shelburne | $964 |

| Sheldon | $1,030 |

| Sheldon Springs | $1,073 |

| Shoreham | $1,057 |

| South Barre | $1,061 |

| South Burlington | $948 |

| South Hero | $1,039 |

| South Londonderry | $1,069 |

| South Newfane | $1,068 |

| South Pomfret | $1,057 |

| South Royalton | $1,046 |

| South Ryegate | $1,040 |

| South Strafford | $1,049 |

| South Woodstock | $1,025 |

| Springfield | $1,069 |

| St. Albans | $1,037 |

| St. Albans Bay | $1,063 |

| St. Johnsbury | $1,007 |

| St. Johnsbury Center | $1,053 |

| Stamford | $1,059 |

| Starksboro | $1,014 |

| Stockbridge | $1,062 |

| Stowe | $1,015 |

| Strafford | $1,055 |

| Sutton | $1,044 |

| Swanton | $1,041 |

| Taftsville | $1,047 |

| Thetford Center | $1,062 |

| Topsham | $1,048 |

| Townshend | $1,038 |

| Troy | $1,055 |

| Tunbridge | $1,051 |

| Underhill | $950 |

| Underhill Center | $1,020 |

| Vergennes | $1,026 |

| Vernon | $1,079 |

| Vershire | $1,053 |

| Waitsfield | $1,013 |

| Wallingford | $1,067 |

| Wardsboro | $1,068 |

| Warren | $1,047 |

| Washington | $1,025 |

| Waterbury | $1,025 |

| Waterbury Center | $1,036 |

| Waterville | $1,058 |

| Websterville | $1,014 |

| Wells | $1,090 |

| Wells River | $1,026 |

| West Brattleboro | $1,075 |

| West Burke | $1,060 |

| West Charleston | $1,066 |

| West Danville | $1,022 |

| West Dover | $1,073 |

| West Dummerston | $1,118 |

| West Fairlee | $1,055 |

| West Halifax | $1,088 |

| West Hartford | $1,047 |

| West Newbury | $1,026 |

| West Pawlet | $1,089 |

| West Rupert | $1,075 |

| West Rutland | $1,079 |

| West Topsham | $1,039 |

| West Townshend | $1,062 |

| West Wardsboro | $1,071 |

| Westfield | $1,054 |

| Westford | $950 |

| Westminster | $1,061 |

| Westminster Station | $1,109 |

| Weston | $1,081 |

| White River Junction | $1,045 |

| Whiting | $1,058 |

| Whitingham | $1,074 |

| Wilder | $1,045 |

| Williamstown | $1,036 |

| Williamsville | $1,069 |

| Williston | $954 |

| Wilmington | $1,068 |

| Windsor | $1,055 |

| Winooski | $945 |

| Wolcott | $1,021 |

| Woodbury | $1,030 |

| Woodstock | $1,033 |

| Worcester | $1,034 |

Current state of homeowners insurance in Vermont

Homeowners insurance remains relatively affordable in Vermont compared with much of the country. The average Vermont home insurance premium increased by only about 19% over the previous five years, well below the national average increase of 48%. Vermont also saw a smaller rate increase than neighboring states like New Hampshire (27%), Massachusetts (28%), Connecticut (38%) and Rhode Island (39%). Maine was the only New England state with a similar increase at about 19%.

The good news is that Vermont’s home insurance increases seem to have slowed. After a 9% increase in 2024, Vermont homeowners only saw a 2.6% increase in 2025.

Vermont’s housing features may help explain some of the state’s lower costs. The average Vermont home is 42 years old and measures about 2,000 square feet. Older homes can come with extra maintenance and repair challenges, but Vermont homes tend to be smaller than those in many other states, which may help keep rebuilding costs more manageable.

Flooding remains a concern for Vermont homeowners, especially during the winter and early spring. In March 2026, the Vermont Department of Environmental Conservation warned that ice jams can cause costly flooding and noted that midwinter floods have become more common in recent years. The agency encouraged residents to understand their flood risk and take steps to protect their homes before severe weather strikes.

How to compare homeowners insurance in Vermont

Since harsh winters can increase the risk of property damage, it’s important to look beyond just price when you compare policies. When reviewing home insurance options in Vermont, consider the following factors:

-

Coverage limits:

Make sure your policy provides enough coverage to rebuild your home after a covered loss. -

Deductibles:

Choosing a higher deductible lowers your premium, but it will increase your out-of-pocket costs if you file a claim, so be sure you can cover that cost should you need to. -

Exclusions:

Standard homeowners insurance policies usually don’t cover flood damage. If your property faces flood risk, you may want to consider separate flood insurance coverage. -

Add-ons:

Consider endorsements or additional coverage for high-value belongings, home businesses or other unique needs.

And if you own one or more vehicles, consider bundling your home and auto insurance. Many insurance companies offer big discounts for this.

How LendingTree helps you find the right policy

Shopping for home insurance isn’t always straightforward — especially when availability and pricing can vary widely. LendingTree makes it easier by helping you explore options from multiple insurers, so you can find coverage that fits your home, location and budget.

How it works

Tell us about your home

Answer a few quick questions about your home, location and coverage needs.

Compare options from insurers

See quotes and typical rates from insurers that offer coverage in your area.

Choose the right policy

Review your options and pick the coverage that fits your needs and budget.

Frequently asked questions

Vermont homeowners pay some of the lowest home insurance premiums in the country. Insurance costs have increased more slowly in Vermont than in most neighboring states, likely due in part to the fact that the state generally faces very few large-scale disasters compared to some other states.

Most homeowners insurance policies don’t cover flood damage. If your home faces a higher flood risk, you may want to consider purchasing a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private insurer.

Heavy snow, ice dams, frozen pipes and ice jams can all lead to expensive home repairs. Carefully reviewing your policy can help you avoid surprises and see where you might need additional protection.

Methodology

How we chose the best homeowners insurance in Vermont

The rates shown in this article are based on an analysis of non-binding quotes obtained in February 2026 from Quadrant Information Services for sample homes in every Vermont ZIP code. Unless otherwise noted, policies include:

- Dwelling coverage: $400,000

- Other structures: $40,000

- Personal property: $200,000

- Loss of use: $80,000

- Personal liability: $100,000

- Guest medical payments: $5,000

- Deductible: $1,000

How we create LendingTree ratings

Our team of insurance experts evaluates insurance companies across several categories, including average rates, discounts, coverage options, third-party customer service ratings and app/website experience. We use this information to create LendingTree ratings, which help us identify and recommend the best insurance companies for consumers.

For third-party customer service ratings, we included NAIC’s Complaint Index scores and financial strength ratings from A.M. Best. NAIC Complaint Index scores show how well companies treat customers over things like claims, while financial strength ratings from A.M. Best reflect the ability to pay out claims.

See our home insurance ratings methodology and full editorial guidelines for further details.

**USAA is only available to current and former members of the military, their spouses, children of USAA members and certain federal employees.