Auto Insurance Rates Spike After a DUI, Especially in These States

Driving under the influence — commonly known as DUI — is incredibly dangerous. Even when a crash doesn’t result in severe injuries or fatalities, a DUI conviction can carry major financial consequences that follow drivers for years.

A LendingTree study found auto insurance premiums increase by an average of 74.5% across U.S. states after a DUI, raising average annual rates from $2,130 to $3,716. The financial impact varies significantly by state, with premiums in one state more than tripling after a DUI.

Read on to learn where drivers face the steepest insurance hikes after a DUI, how those added costs compound over time and what steps drivers can take to help manage the financial fallout.

- Auto insurance premiums after a DUI jump by an average of 74.5% across U.S. states. Annual rates climb from $2,130 before a DUI to $3,716 after. North Carolina sees the sharpest increase, with premiums skyrocketing by 284.1% from $1,208 to $4,640, followed by California (136.0%) and Delaware (124.0%).

- A DUI can add thousands of dollars to a driver’s insurance costs over time. Across the U.S. states, premiums after a DUI increase by an average of $132 a month, $1,585 a year and $4,755 over three years.

- California and North Carolina drivers see the biggest dollar increases in insurance premiums after a DUI. Annual costs rise by an average of $3,535 in California and $3,432 in North Carolina, while Delaware ranks third at $3,152. Meanwhile, Mississippi ($378), Maryland ($779) and Wyoming ($810) see the smallest annual increases.

- Drivers at both ends of the age spectrum see some of the biggest premium hikes after a DUI. Typical 20-year-olds pay an average of $2,532 more annually after a DUI, while 80-year-olds pay an average of $2,211 more. Separately, 60-year-olds face the largest percentage increase, with premiums rising 101.1% from $1,491 to $2,999.

Across U.S. states, DUIs send premiums soaring

Driving under the influence can lead to long-lasting financial consequences. Along with court fees, attorney costs and lost wages, drivers also face sharply higher car insurance rates. Across U.S. states, auto insurance premiums rise by an average of 74.5% after a DUI. These findings are based on rates for a 30-year-old male with a clean driving record and good credit driving a 2018 Honda CR-V EX.

Why the dramatic spike? According to Rob Bhatt, LendingTree auto insurance expert and licensed insurance agent, insurance companies are pricing for risk.

“Their data shows that people with a DUI are more likely to have a future car accident than a typical driver,” Bhatt says. “Accidents cost insurance companies money in the form of claims payments. They factor these potential costs into the rates they charge after a DUI.”

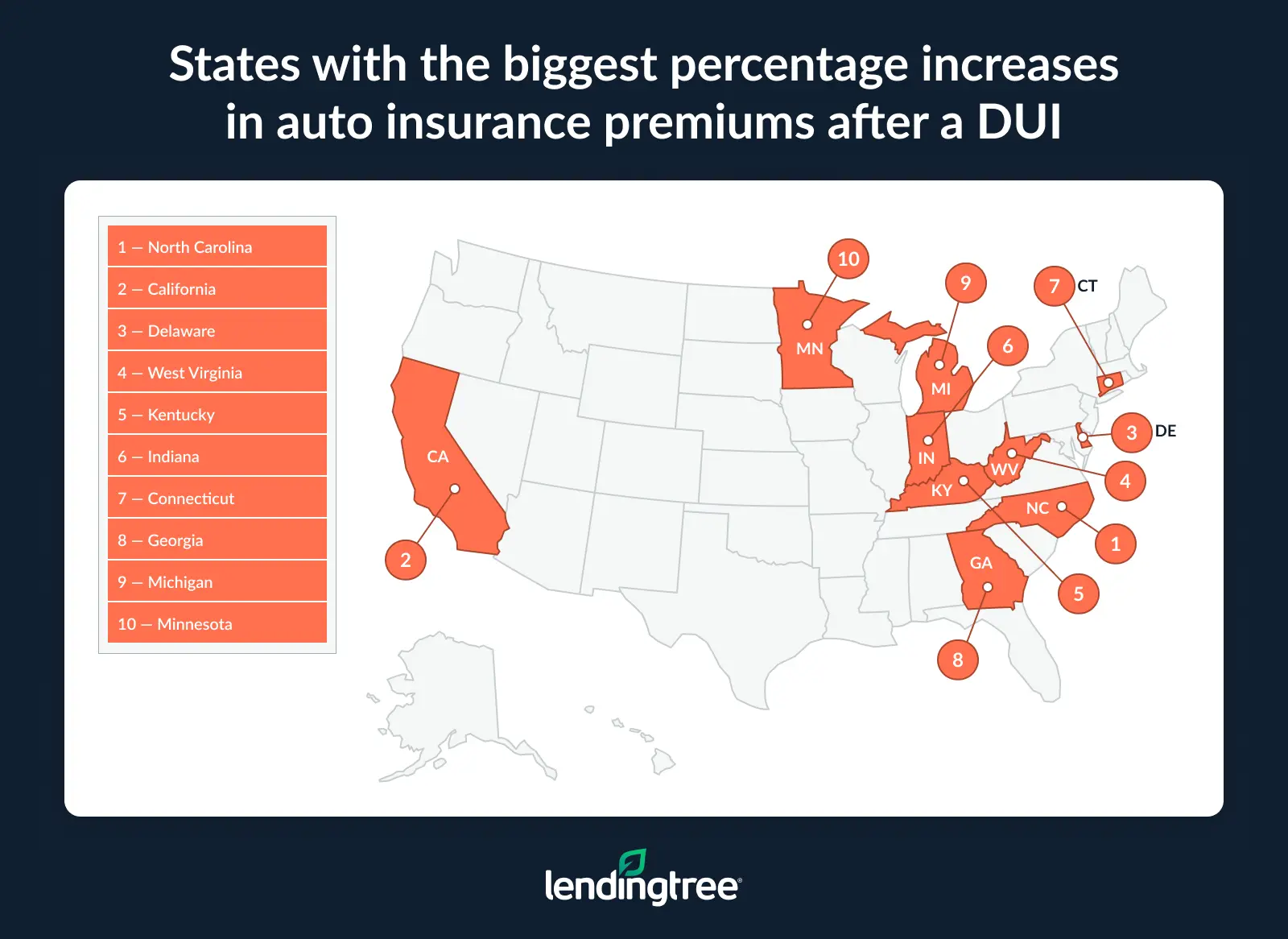

Where you live can play a major role in the financial fallout after a DUI. In North Carolina, for example, drivers see the steepest average percentage increase in their annual car insurance premium of any state in the country. Residents of the Tar Heel State see an average 284.1% increase in their insurance premiums after a DUI — rising from $1,208 to $4,640.

California ranks second, with an average premium increase of 136.0% after a DUI, rising from $2,600 to $6,135. Delaware follows closely behind, with an average 124.0% increase after a DUI, jumping from $2,542 to $5,694.

So, why do DUI insurance penalties vary so dramatically between states? One major factor is how aggressively states penalize DUI offenses. North Carolina, for example, has some of the strictest penalties in the country. The state uses an insurance points system in which those convicted of a DUI are typically issued 12 points, which is one of the highest totals for any traffic violation. Insurance companies use these points to assess risk and adjust premiums accordingly.

By comparison, some states see much smaller percentage spikes in car insurance premiums after a DUI. Mississippi has the lowest average jump at 17.4%, followed by New York at 28.7% and Maryland at 35.4%.

Full rankings: States with the biggest percentage increases in auto insurance premiums after a DUI

| Rank | State | Avg. annual premium before | Avg. annual premium after | % increase |

|---|---|---|---|---|

| 1 | North Carolina | $1,208 | $4,640 | 284.1% |

| 2 | California | $2,600 | $6,135 | 136.0% |

| 3 | Delaware | $2,542 | $5,694 | 124.0% |

| 4 | West Virginia | $1,502 | $3,216 | 114.1% |

| 5 | Kentucky | $2,066 | $4,354 | 110.7% |

| 6 | Indiana | $1,490 | $3,122 | 109.5% |

| 7 | Connecticut | $2,651 | $5,464 | 106.1% |

| 8 | Georgia | $2,489 | $5,079 | 104.1% |

| 9 | Michigan | $2,440 | $4,961 | 103.3% |

| 10 | Minnesota | $1,998 | $4,053 | 102.9% |

| 11 | Hawaii | $1,522 | $3,062 | 101.2% |

| 12 | New Hampshire | $1,335 | $2,608 | 95.4% |

| 13 | Massachusetts | $1,644 | $3,211 | 95.3% |

| 14 | Virginia | $1,605 | $3,118 | 94.3% |

| 15 | Vermont | $1,212 | $2,350 | 93.9% |

| 16 | North Dakota | $1,747 | $3,350 | 91.8% |

| 17 | Illinois | $1,802 | $3,431 | 90.4% |

| 18 | Iowa | $1,801 | $3,400 | 88.8% |

| 19 | Maine | $1,270 | $2,394 | 88.5% |

| 20 | South Carolina | $1,843 | $3,406 | 84.8% |

| 21 | South Dakota | $2,003 | $3,682 | 83.8% |

| 22 | Arizona | $3,586 | $6,560 | 82.9% |

| 23 | Kansas | $1,998 | $3,593 | 79.8% |

| 24 | Idaho | $1,502 | $2,693 | 79.3% |

| 25 | Rhode Island | $3,063 | $5,466 | 78.5% |

| 26 | Ohio | $1,595 | $2,843 | 78.2% |

| 27 | Wyoming | $1,088 | $1,898 | 74.4% |

| 28 | Oregon | $1,830 | $3,116 | 70.3% |

| 29 | Arkansas | $2,721 | $4,561 | 67.6% |

| 30 | New Jersey | $3,214 | $5,368 | 67.0% |

| 31 | Florida | $2,219 | $3,693 | 66.4% |

| 32 | Nebraska | $1,946 | $3,235 | 66.2% |

| 33 | Tennessee | $1,812 | $2,996 | 65.3% |

| 34 | Wisconsin | $1,673 | $2,719 | 62.5% |

| 35 | Texas | $2,170 | $3,520 | 62.2% |

| 36 | Pennsylvania | $1,987 | $3,187 | 60.4% |

| 37 | Colorado | $2,960 | $4,589 | 55.0% |

| 38 | Washington | $2,915 | $4,481 | 53.7% |

| 39 | Alabama | $1,906 | $2,916 | 53.0% |

| 40 | Montana | $2,451 | $3,661 | 49.4% |

| 41 | Alaska | $1,863 | $2,777 | 49.1% |

| 42 | Utah | $2,169 | $3,212 | 48.1% |

| 43 | New Mexico | $2,201 | $3,228 | 46.7% |

| 44 | Missouri | $2,250 | $3,161 | 40.5% |

| 45 | Nevada | $2,674 | $3,751 | 40.3% |

| 46 | Oklahoma | $2,321 | $3,251 | 40.1% |

| 47 | Louisiana | $4,150 | $5,777 | 39.2% |

| 48 | District of Columbia | $2,298 | $3,195 | 39.0% |

| 49 | Maryland | $2,198 | $2,977 | 35.4% |

| 50 | New York | $2,949 | $3,796 | 28.7% |

| 51 | Mississippi | $2,170 | $2,548 | 17.4% |

A DUI costs thousands over time

The long-term financial impact of a DUI becomes even clearer when looking at dollar amounts. Across the U.S. states, premiums after a DUI conviction increase by an average of $132 a month, which adds up to $1,585 a year and $4,755 over three years.

The direct out-of-pocket costs are only part of the financial impact, though. Money spent on higher insurance premiums could otherwise go toward paying down debt, covering major purchases or building long-term savings. For example, investing that $132 a month instead of spending it on higher insurance premiums (assuming a 7% annual return) could grow it to about $5,300 over three years. A one-time investment of the full $4,755 (assuming the same 7% annual return) could grow to about $9,500 over 10 years and more than $38,000 after 30 years.

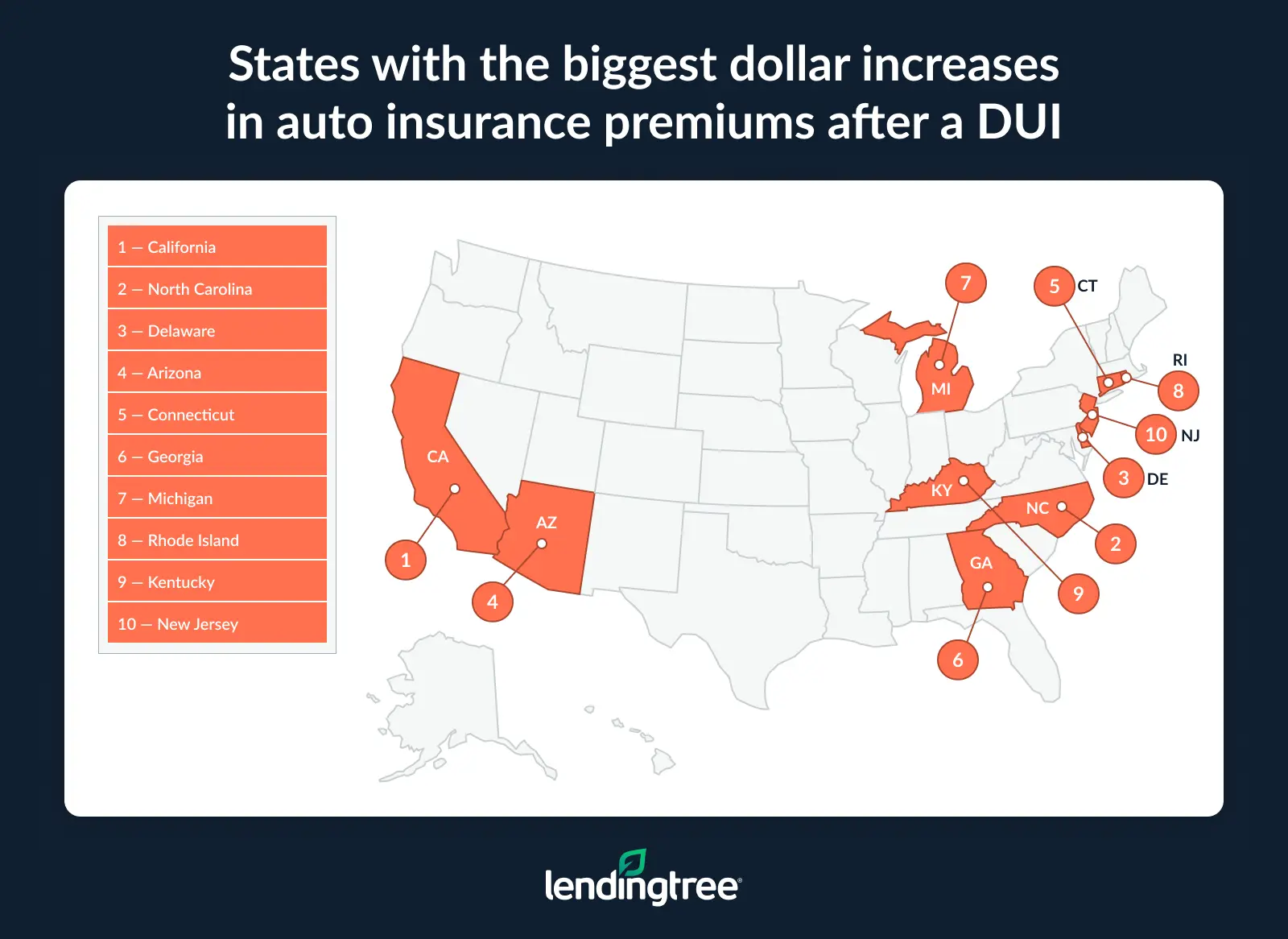

When measured in dollars, DUI-related insurance increases vary significantly by state. In California, drivers see the steepest increase, paying an average of $3,535 a year more after a DUI conviction, followed closely by North Carolina at $3,432. Delaware ranks third at $3,152. On the other end of the spectrum, Mississippi ($378), Maryland ($779) and Wyoming ($810) see the smallest average annual increases.

These added costs, especially in states with the steepest hikes, can place a major strain on household budgets. At a time when many Americans are already grappling with higher living expenses, paying several thousand dollars more each year for car insurance can be financially overwhelming. In some cases, it may force some to take on debt or make other moves that have long-term financial consequences from which it can be difficult to recover.

Full rankings: States with the biggest dollar increases in auto insurance premiums after a DUI

| Rank | State | Monthly increase | Annual increase | 3-year increase |

|---|---|---|---|---|

| 1 | California | $295 | $3,535 | $10,605 |

| 2 | North Carolina | $286 | $3,432 | $10,296 |

| 3 | Delaware | $263 | $3,152 | $9,456 |

| 4 | Arizona | $248 | $2,974 | $8,922 |

| 5 | Connecticut | $234 | $2,813 | $8,439 |

| 6 | Georgia | $216 | $2,590 | $7,770 |

| 7 | Michigan | $210 | $2,521 | $7,563 |

| 8 | Rhode Island | $200 | $2,403 | $7,209 |

| 9 | Kentucky | $191 | $2,288 | $6,864 |

| 10 | New Jersey | $180 | $2,154 | $6,462 |

| 11 | Minnesota | $171 | $2,055 | $6,165 |

| 12 | Arkansas | $153 | $1,840 | $5,520 |

| 13 | West Virginia | $143 | $1,714 | $5,142 |

| 14 | South Dakota | $140 | $1,679 | $5,037 |

| 15 | Indiana | $136 | $1,632 | $4,896 |

| 16 | Colorado | $136 | $1,629 | $4,887 |

| 16 | Illinois | $136 | $1,629 | $4,887 |

| 18 | Louisiana | $136 | $1,627 | $4,881 |

| 19 | North Dakota | $134 | $1,603 | $4,809 |

| 20 | Iowa | $133 | $1,599 | $4,797 |

| 21 | Kansas | $133 | $1,595 | $4,785 |

| 22 | Massachusetts | $131 | $1,567 | $4,701 |

| 23 | Washington | $131 | $1,566 | $4,698 |

| 24 | South Carolina | $130 | $1,563 | $4,689 |

| 25 | Hawaii | $128 | $1,540 | $4,620 |

| 26 | Virginia | $126 | $1,513 | $4,539 |

| 27 | Florida | $123 | $1,474 | $4,422 |

| 28 | Texas | $113 | $1,350 | $4,050 |

| 29 | Nebraska | $107 | $1,289 | $3,867 |

| 30 | Oregon | $107 | $1,286 | $3,858 |

| 31 | New Hampshire | $106 | $1,273 | $3,819 |

| 32 | Ohio | $104 | $1,248 | $3,744 |

| 33 | Montana | $101 | $1,210 | $3,630 |

| 34 | Pennsylvania | $100 | $1,200 | $3,600 |

| 35 | Idaho | $99 | $1,191 | $3,573 |

| 36 | Tennessee | $99 | $1,184 | $3,552 |

| 37 | Vermont | $95 | $1,138 | $3,414 |

| 38 | Maine | $94 | $1,124 | $3,372 |

| 39 | Nevada | $90 | $1,077 | $3,231 |

| 40 | Wisconsin | $87 | $1,046 | $3,138 |

| 41 | Utah | $87 | $1,043 | $3,129 |

| 42 | New Mexico | $86 | $1,027 | $3,081 |

| 43 | Alabama | $84 | $1,010 | $3,030 |

| 44 | Oklahoma | $78 | $930 | $2,790 |

| 45 | Alaska | $76 | $914 | $2,742 |

| 46 | Missouri | $76 | $911 | $2,733 |

| 47 | District of Columbia | $75 | $897 | $2,691 |

| 48 | New York | $71 | $847 | $2,541 |

| 49 | Wyoming | $68 | $810 | $2,430 |

| 50 | Maryland | $65 | $779 | $2,337 |

| 51 | Mississippi | $32 | $378 | $1,134 |

DUIs impact youngest, oldest drivers the hardest

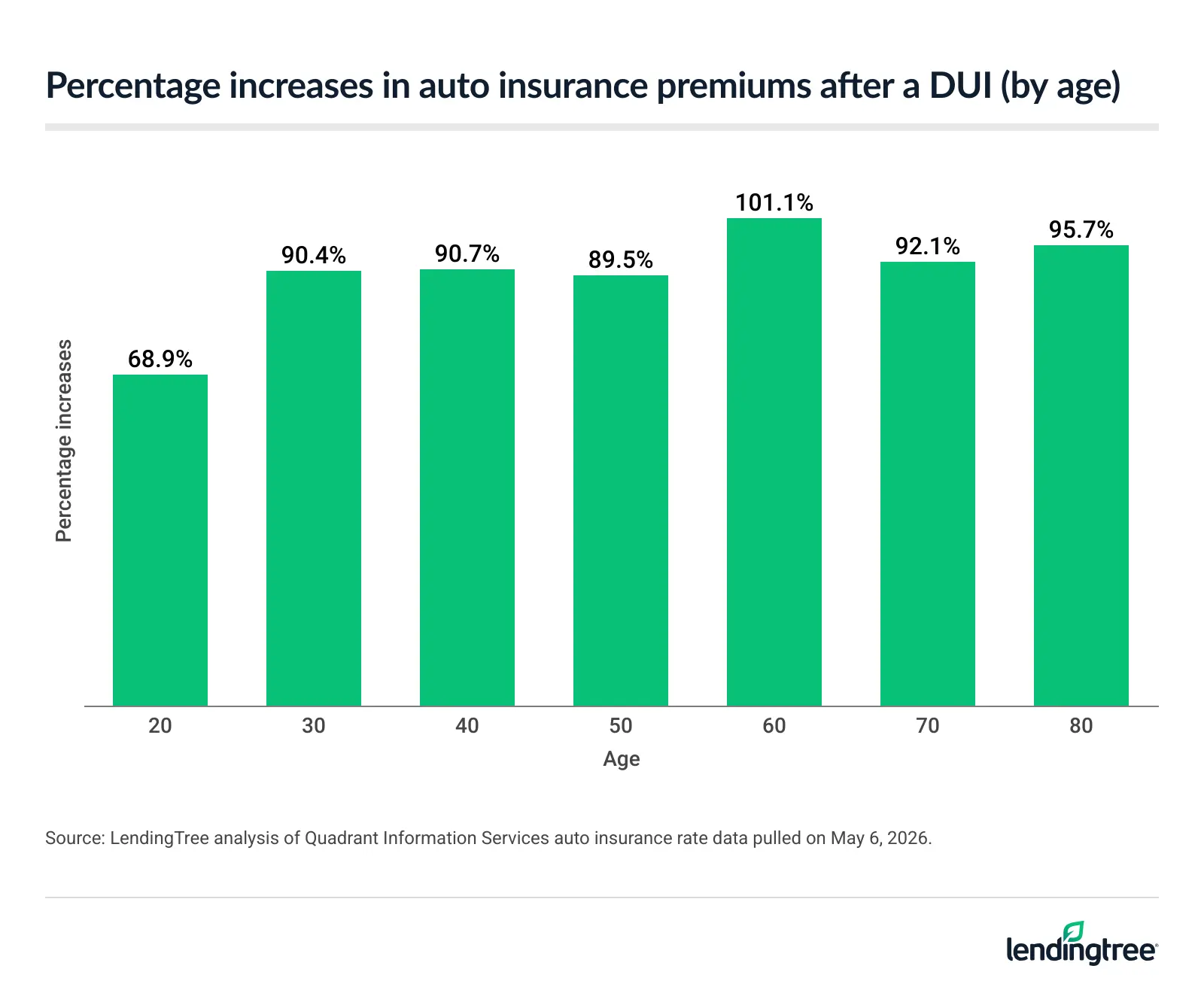

A driver’s age also affects how much car insurance premiums increase after a DUI, with drivers at both ends of the spectrum seeing the steepest increases. Typical 20-year-olds pay an average of $2,532 more annually after a DUI, while 80-year-olds pay an average of $2,211 more.

In between those two ages, annual car insurance premium increases range from $1,427 after a DUI for typical 50-year-olds to $1,629 for typical 30-year-olds.

Change in auto insurance premiums after a DUI by age

| Age | Avg. annual premium before | Avg. annual premium after | % increase | $ difference |

|---|---|---|---|---|

| 20 | $3,673 | $6,205 | 68.9% | $2,532 |

| 30 | $1,802 | $3,431 | 90.4% | $1,629 |

| 40 | $1,696 | $3,234 | 90.7% | $1,538 |

| 50 | $1,595 | $3,022 | 89.5% | $1,427 |

| 60 | $1,491 | $2,999 | 101.1% | $1,508 |

| 70 | $1,725 | $3,314 | 92.1% | $1,589 |

| 80 | $2,310 | $4,521 | 95.7% | $2,211 |

While younger and older drivers see the largest dollar increases, 60-year-olds face the largest percentage jump, with premiums rising 101.1% (from $1,491 to $2,999). In contrast, 20-year-olds see the lowest percentage increase, with premiums rising 68.9% (from $3,673 to $6,205).

Other ages see percentage increases ranging from 95.7% for 80-year-olds to 89.5% for 50-year-olds.

Bhatt says the percentage increase for 60-year-olds is a little surprising, as they’re usually part of an age group that has the lowest crash rates. However, in dollars, it’s much less than the increases for 20- and 80-year-olds.

“This shows that a DUI can have a sharp impact on a driver’s insurance rate at any age,” Bhatt says.

Top expert tips for drivers with a DUI on their record

If you find yourself with a DUI conviction, there’s no way around paying the price. However, there are steps you can take to reduce the long-term financial impact and put yourself in a better position moving forward. Bhatt offers the following tips:

- Look into diversion programs. Consider going through a diversion program to reduce a DUI to a lesser offense. The availability of these programs and their requirements vary by state and sometimes by county, too.

- Compare insurance plans. Shop around to find the most affordable rate you can for DUI car insurance. Some companies have cheaper rates after a DUI than others, so it’s good to compare quotes. Look at both national insurance carriers and smaller regional or local insurers.

- Keep on top of your paperwork requirements. In some cases, you’ll need an SR-22 certificate to reinstate your license. Also known as a Certificate of Financial Responsibility, it proves you have at least the minimum insurance required by law in your state. You’ll typically be notified by the court or by your state’s Department of Motor Vehicles if one is required. If you need an SR-22, make sure to let your insurance company know about it. In most states, your insurance company files the SR-22 certificate for you. If your current insurance company doesn’t offer SR-22 filings, you usually have to switch to a different company that does. Missing deadlines or allowing your coverage to lapse could lead to additional penalties or license suspension.

- Consider public transportation or driving less. If your budget can’t handle the increased cost of car insurance or if you’re unable to secure car insurance altogether, look into local public transportation options. Taking the train or bus may be more affordable than paying sharply higher insurance premiums after a DUI. You may also save money on gas, parking, maintenance and other vehicle-related expenses. Carpooling, rideshare services or working remotely when possible can also help reduce expenses.

- Practice good driving habits. Watch your speed, avoid distractions and follow all traffic laws carefully. Over time, maintaining a clean driving record can help lower your insurance premiums. Many insurers gradually decrease the DUI-related increases after several years if the driver doesn’t have any additional violations or accidents.

Methodology

LendingTree uses insurance rate data from Quadrant Information Services based on publicly sourced insurance company filings. Rates reflect an analysis of hundreds of thousands of car insurance quotes for a typical driver and are intended for comparative purposes only. Your rates may vary based on factors such as location, driving history, age, credit profile and insurer.

Unless otherwise noted, quotes represent a full coverage policy for a 30-year-old male with good credit and a clean driving record who drives a 2018 Honda CR-V EX. Rates were compared before and after the driver was involved in a DUI incident in which they had a blood alcohol concentration (BAC) of 0.08 or more, which is the legal limit for noncommercial drivers 21 and older. Data was collected in May 2026.

We also used the same methodology to analyze how the impact of a DUI varies by driver age before and after the incident occurred.

Minimum liability policies include only the state’s required minimum coverage limits.

Full coverage policies include collision, comprehensive and liability coverage with the following limits and deductibles:

- Bodily injury liability: $50,000 per person and $100,000 per accident

- Property damage liability: $50,000

- Uninsured and underinsured motorist bodily injury: $50,000 per person and $100,000 per accident

- Personal injury protection: Minimum limits, where required by law

- Collision: $500 deductible

- Comprehensive: $500 deductible