Personal Bankruptcy Filings Have Risen 47% Since 2022, Marking a Third Straight Annual Increase

Americans are continuing to struggle financially, and the latest bankruptcy data makes that clear.

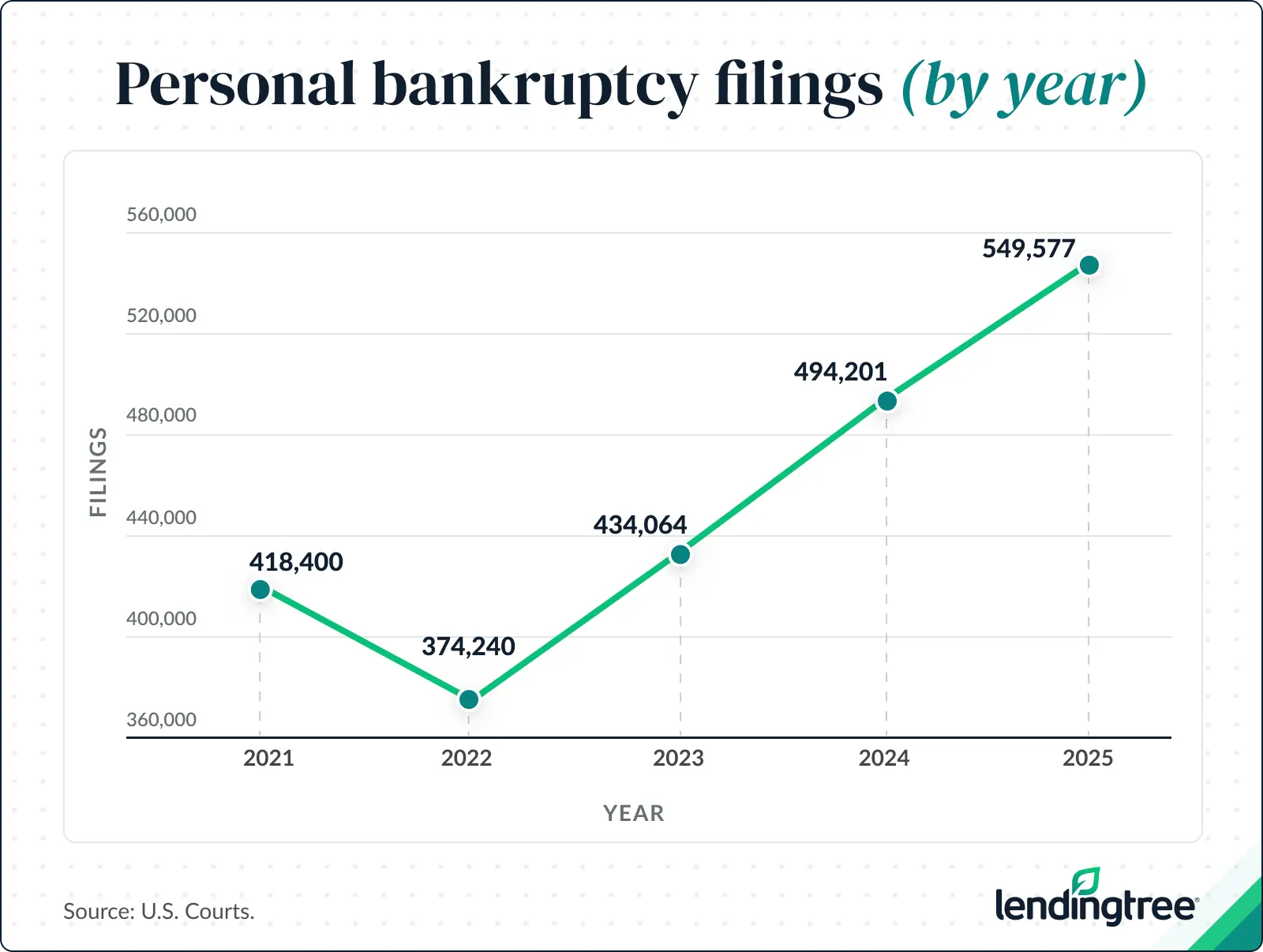

Personal bankruptcy filings rose for the third straight year in 2025, reaching 549,577 filings, up 46.9% from a recent low of 374,240 in 2022.

- Personal bankruptcy filings rose for the third consecutive year in 2025, reaching 549,577 filings. That’s up 46.9% from a recent low of 374,240 filings in 2022. In 2025, Chapter 13 bankruptcies accounted for 37.6% of filings, while Chapter 7 bankruptcies accounted for 62.3%.

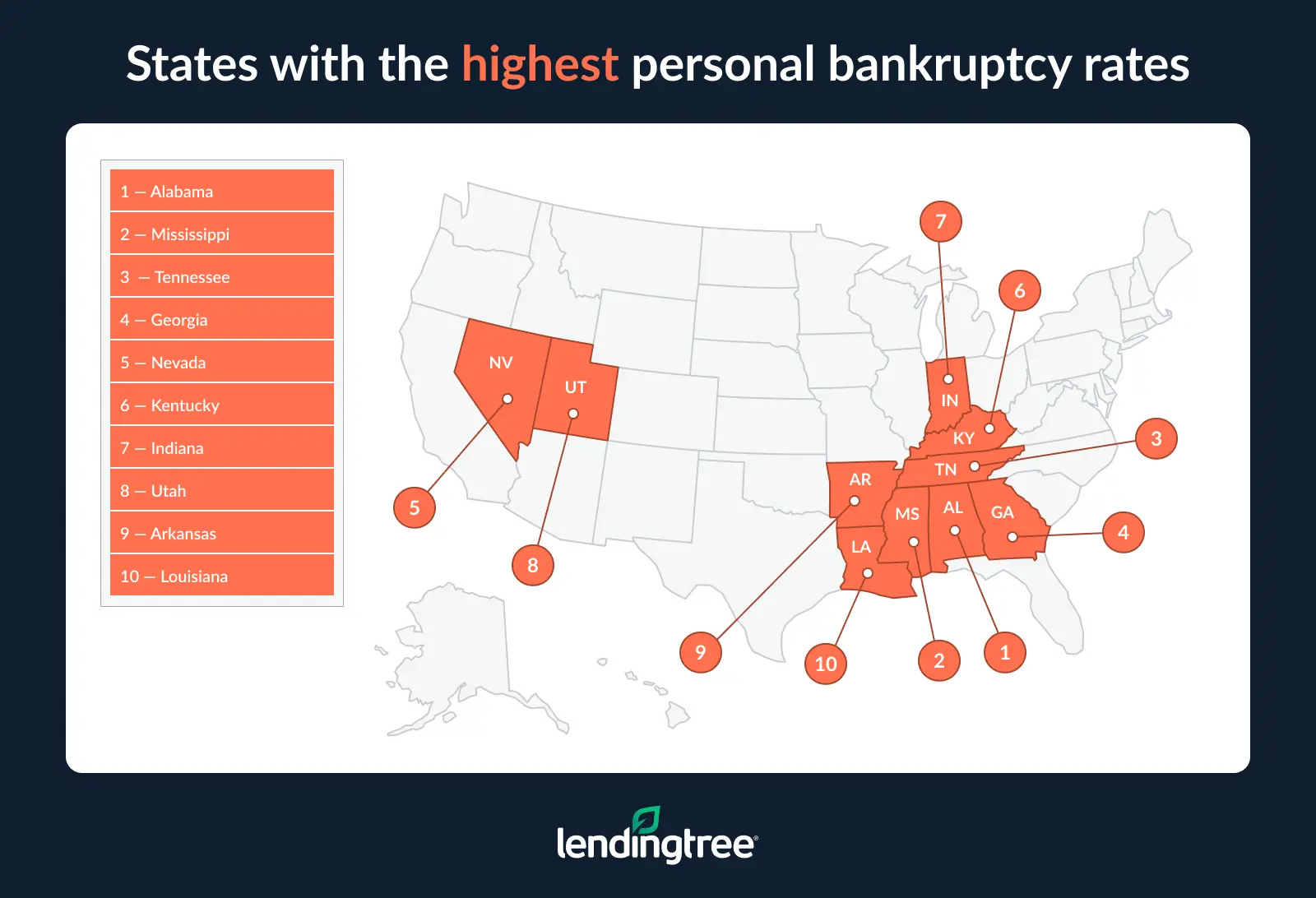

- An average of 1,489 Americans filed for personal bankruptcy each day in 2025. Alabama led the nation with 506.5 filings per 100,000 adults, followed by Mississippi (420.5) and Tennessee (375.3), well above the national rate of 203.5. Meanwhile, Alaska, Maine and Vermont had the lowest rates, with fewer than 50.0 filings per 100,000 adults.

- Personal bankruptcy filings increased in almost every state between 2024 and 2025, rising 11.3% nationwide. Only Maine and New Hampshire had fewer bankruptcies in 2025 than in 2024. The largest increases were in the District of Columbia (40.9%), Oregon (24.4%) and Florida (20.3%).

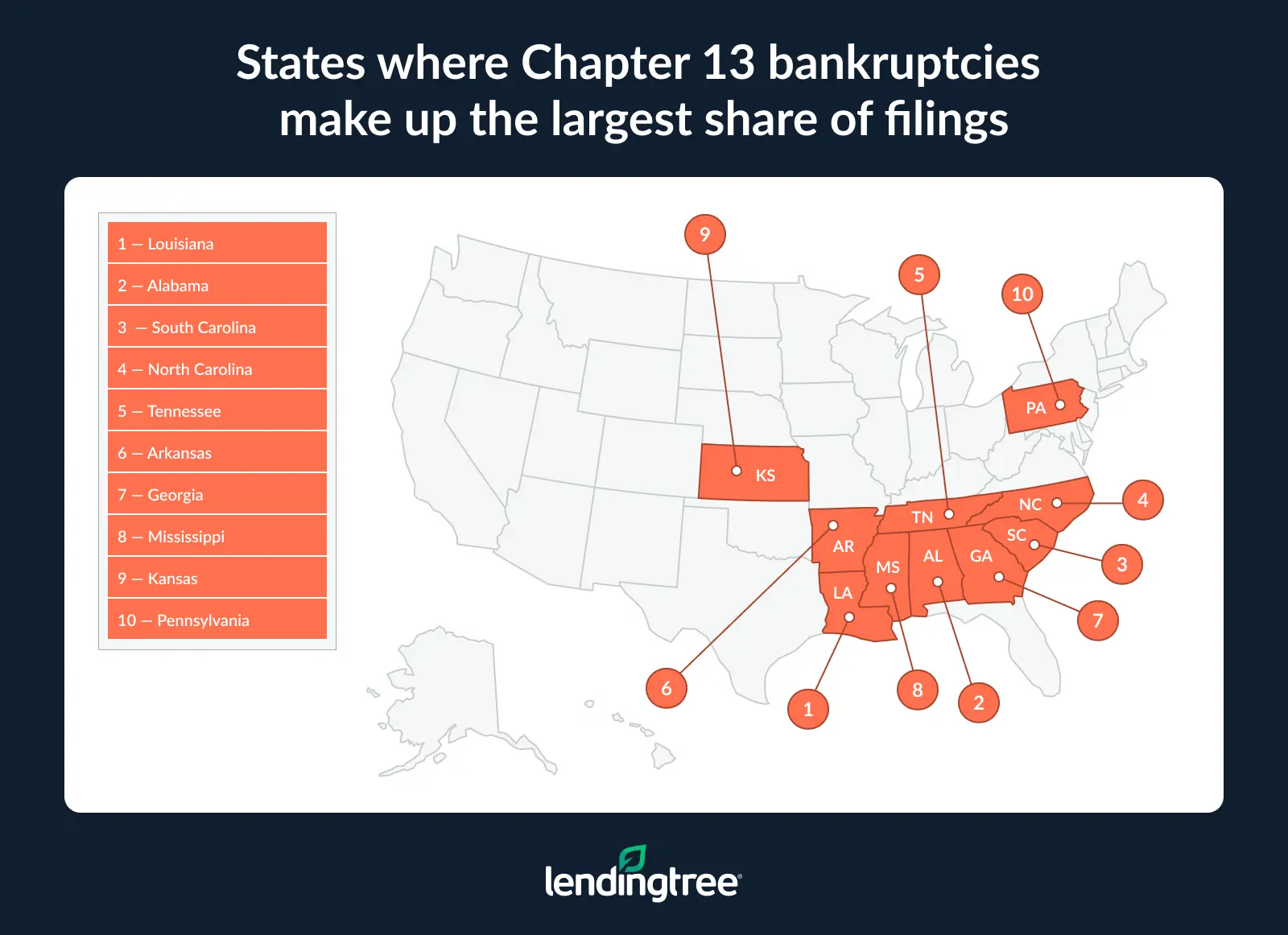

- Chapter 7 bankruptcies grew faster than Chapter 13 bankruptcies between 2024 and 2025. Chapter 7 filings increased 14.9%, compared with a 5.5% increase in Chapter 13 filings. Even so, Chapter 13 remained especially common in the South, accounting for a majority of filings in eight states, led by Louisiana (76.1%), Alabama (71.5%) and South Carolina (66.4%).

In this study, we focused on Chapter 7 and Chapter 13 bankruptcy. The difference between the two is as follows:

- Chapter 7: When an individual faces severe financial hardship, Chapter 7 may provide a path forward. This type of bankruptcy is commonly known as liquidation bankruptcy because it involves converting certain assets into cash. A trustee is appointed to oversee the case, sell any nonexempt property owned by the debtor and distribute the proceeds to creditors.

- Chapter 13: Individuals who earn a steady income but are struggling with overwhelming debt may seek relief through Chapter 13 bankruptcy. Unlike Chapter 7, Chapter 13 focuses on repayment rather than liquidation. Under this chapter, the debtor proposes a repayment plan under which a portion of future earnings is paid to creditors through a bankruptcy trustee. Once the court approves the plan, the debtor receives legal protection from creditors while making payments according to the agreed-upon schedule.

Personal bankruptcy filings rose for the third consecutive year

Personal bankruptcy filings climbed to 549,577 in 2025, marking the third consecutive year of increases. That’s a significant increase from 494,201 in 2024, and it was up 46.9% from a recent low of 374,240 filings in 2022.

In 2025, Chapter 13 bankruptcies accounted for 37.6% of filings, while Chapter 7 bankruptcies made up the majority at 62.3%.

Matt Schulz — LendingTree chief consumer finance analyst and author of “Ask Questions, Save Money, Make More: How to Take Control of Your Financial Life” — says inflation is playing a role.

“Housing, insurance, groceries and healthcare all remain significantly more expensive than they were a few years ago, leading many households to rely on credit cards to bridge the gap. At the same time, higher interest rates have made that debt far more costly to carry, causing balances to grow faster than people can pay them down. Given that combination of rising debt and sky-high interest rates, it’s not surprising that more people are turning to bankruptcy for relief.”

According to the American Bankruptcy Institute (ABI), bankruptcies may also be up because Americans’ financial margin for error has shrunk dramatically. With household debt rising, borrowing costs remaining elevated and economic uncertainty lingering, bankruptcy filings have continued to move closer to prepandemic levels.

An average of 1,489 Americans filed for personal bankruptcy each day in 2025

On average, 1,489 Americans filed for personal bankruptcy each day in 2025.

Alabama led all states, with 506.5 filings per 100,000 adults in 2025. Fellow Southern states Mississippi (420.5) and Tennessee (375.3) followed — all well above the national rate of 203.5.

On the other end of the spectrum, Alaska (36.9), Maine (46.2) and Vermont (47.5) had the lowest rates, with fewer than 50.0 filings per 100,000 adults.

Lower incomes, higher medical debt burdens and state-specific collection laws may help explain why many Southern states have relatively high bankruptcy rates. By contrast, low-filing states such as Alaska, Maine and Vermont generally have smaller populations and stronger income profiles, which may reduce the need for bankruptcy protection.

Meanwhile, California had the most filings, at 51,364, followed by Florida (42,289) and Texas (33,979). Together, the three states accounted for 23.5% of all filings nationwide — largely due to their high populations.

Full rankings: States with the highest/lowest personal bankruptcy rates (2025)

| Rank | State | Bankruptcy filings | Rate per 100,000 adults |

|---|---|---|---|

| 1 | Alabama | 20,388 | 506.5 |

| 2 | Mississippi | 9,549 | 420.5 |

| 3 | Tennessee | 21,209 | 375.3 |

| 4 | Georgia | 30,517 | 352.8 |

| 5 | Nevada | 9,047 | 350.7 |

| 6 | Kentucky | 12,009 | 336.6 |

| 7 | Indiana | 17,951 | 335.8 |

| 8 | Utah | 7,764 | 302.0 |

| 9 | Arkansas | 6,738 | 281.9 |

| 10 | Louisiana | 9,825 | 277.9 |

| 11 | Ohio | 25,634 | 275.2 |

| 12 | Michigan | 21,958 | 273.2 |

| 13 | Illinois | 25,549 | 255.0 |

| 14 | Maryland | 12,047 | 246.1 |

| 15 | Oregon | 7,949 | 230.6 |

| 16 | Oklahoma | 7,131 | 227.7 |

| 17 | Virginia | 15,600 | 224.9 |

| 18 | Florida | 42,289 | 224.0 |

| 19 | Minnesota | 9,958 | 221.2 |

| 20 | Missouri | 10,383 | 212.8 |

| 21 | Wisconsin | 9,952 | 210.5 |

| 22 | Arizona | 12,465 | 207.9 |

| 23 | Delaware | 1,519 | 181.2 |

| 24 | New Jersey | 13,370 | 179.3 |

| 25 | Kansas | 4,043 | 177.0 |

| 26 | Nebraska | 2,699 | 176.9 |

| 27 | Colorado | 8,141 | 171.4 |

| 28 | California | 51,364 | 165.6 |

| 29 | Idaho | 2,381 | 155.2 |

| 30 | Texas | 33,979 | 143.8 |

| 31 | Washington | 9,015 | 143.0 |

| 32 | Iowa | 3,590 | 142.8 |

| 33 | New York | 21,072 | 132.6 |

| 34 | Pennsylvania | 13,373 | 127.9 |

| 35 | Connecticut | 3,562 | 120.8 |

| 36 | West Virginia | 1,703 | 119.7 |

| 37 | South Carolina | 5,064 | 117.0 |

| 38 | Wyoming | 536 | 115.9 |

| 39 | Rhode Island | 1,027 | 113.0 |

| 40 | North Carolina | 9,449 | 108.7 |

| 41 | Hawaii | 1,146 | 99.4 |

| 42 | North Dakota | 592 | 95.7 |

| 43 | New Mexico | 1,587 | 94.1 |

| 44 | South Dakota | 641 | 90.6 |

| 45 | District of Columbia | 503 | 87.9 |

| 46 | Montana | 780 | 86.0 |

| 47 | Massachusetts | 4,759 | 82.3 |

| 48 | New Hampshire | 847 | 73.0 |

| 49 | Vermont | 255 | 47.5 |

| 50 | Maine | 536 | 46.2 |

| 51 | Alaska | 209 | 36.9 |

Personal bankruptcy filings increased in almost every state between 2024 and 2025

Filings rose 11.3% nationally between 2024 and 2025, with nearly every state seeing an increase. Only Maine (down 5.6%) and New Hampshire (down 4.6%) had fewer bankruptcies in 2025 than in 2024.

The largest increase was in the District of Columbia (40.9%), where bankruptcies rose from 357 in 2024 to 503 in 2025. Oregon (24.4%) and Florida (20.3%) rounded out the top three.

Despite the increase in filings, Schulz says consumers shouldn’t assume a bankruptcy filing results in permanent financial damage.

“One of the biggest misconceptions is that bankruptcy permanently ruins your financial life,” Schulz says. “It’s a really big deal, but the effect on your credit doesn’t last forever. In fact, its impact fades over time. Many filers are surprised to find that it can provide a pathway to rebuilding because it eliminates or restructures overwhelming debt. Another myth is that you’ll lose everything you own, but in reality many people are able to keep key assets thanks to bankruptcy exemptions. Consumers should expect the process to involve detailed financial disclosures, court oversight and some short-term challenges, but also the possibility of meaningful financial relief and a fresh start.”

Full rankings: States where bankruptcy filings increased the most

| Rank | State | Bankruptcy filings, 2024 | Bankruptcy filings, 2025 | % change |

|---|---|---|---|---|

| 1 | District of Columbia | 357 | 503 | 40.9% |

| 2 | Oregon | 6,391 | 7,949 | 24.4% |

| 3 | Florida | 35,161 | 42,289 | 20.3% |

| 4 | Texas | 28,344 | 33,979 | 19.9% |

| 5 | Minnesota | 8,365 | 9,958 | 19.0% |

| 6 | New Mexico | 1,358 | 1,587 | 16.9% |

| 7 | Iowa | 3,079 | 3,590 | 16.6% |

| 8 | Delaware | 1,305 | 1,519 | 16.4% |

| 9 | North Dakota | 509 | 592 | 16.3% |

| 9 | Utah | 6,678 | 7,764 | 16.3% |

| 11 | Idaho | 2,054 | 2,381 | 15.9% |

| 12 | California | 44,646 | 51,364 | 15.0% |

| 13 | Alaska | 182 | 209 | 14.8% |

| 14 | Arizona | 10,901 | 12,465 | 14.3% |

| 15 | Nevada | 8,035 | 9,047 | 12.6% |

| 16 | South Carolina | 4,513 | 5,064 | 12.2% |

| 17 | Maryland | 10,745 | 12,047 | 12.1% |

| 18 | Montana | 698 | 780 | 11.7% |

| 19 | Colorado | 7,296 | 8,141 | 11.6% |

| 19 | Oklahoma | 6,388 | 7,131 | 11.6% |

| 19 | Indiana | 16,086 | 17,951 | 11.6% |

| 22 | North Carolina | 8,482 | 9,449 | 11.4% |

| 23 | Nebraska | 2,429 | 2,699 | 11.1% |

| 24 | Pennsylvania | 12,049 | 13,373 | 11.0% |

| 25 | Georgia | 27,528 | 30,517 | 10.9% |

| 26 | West Virginia | 1,537 | 1,703 | 10.8% |

| 26 | Rhode Island | 927 | 1,027 | 10.8% |

| 28 | Connecticut | 3,223 | 3,562 | 10.5% |

| 29 | Washington | 8,165 | 9,015 | 10.4% |

| 29 | Virginia | 14,125 | 15,600 | 10.4% |

| 31 | Wyoming | 488 | 536 | 9.8% |

| 32 | Kentucky | 10,952 | 12,009 | 9.7% |

| 33 | Michigan | 20,083 | 21,958 | 9.3% |

| 34 | Missouri | 9,567 | 10,383 | 8.5% |

| 35 | New York | 19,437 | 21,072 | 8.4% |

| 36 | Kansas | 3,736 | 4,043 | 8.2% |

| 37 | Massachusetts | 4,409 | 4,759 | 7.9% |

| 38 | New Jersey | 12,401 | 13,370 | 7.8% |

| 39 | Tennessee | 19,719 | 21,209 | 7.6% |

| 40 | Louisiana | 9,180 | 9,825 | 7.0% |

| 41 | South Dakota | 600 | 641 | 6.8% |

| 42 | Alabama | 19,120 | 20,388 | 6.6% |

| 42 | Mississippi | 8,959 | 9,549 | 6.6% |

| 44 | Vermont | 240 | 255 | 6.3% |

| 45 | Ohio | 24,307 | 25,634 | 5.5% |

| 46 | Wisconsin | 9,539 | 9,952 | 4.3% |

| 47 | Arkansas | 6,469 | 6,738 | 4.2% |

| 48 | Illinois | 25,135 | 25,549 | 1.6% |

| 49 | Hawaii | 1,145 | 1,146 | 0.1% |

| 50 | New Hampshire | 888 | 847 | -4.6% |

| 51 | Maine | 568 | 536 | -5.6% |

Chapter 7 bankruptcies grew faster than Chapter 13

While both Chapter 7 and Chapter 13 filings increased from 2024 to 2025, Chapter 7 filings grew at a noticeably faster clip — up 14.9%, compared with a 5.5% increase in Chapter 13 filings.

Even so, Chapter 13 remained especially prevalent in the South, accounting for a majority of filings in eight states, led by Louisiana (76.1%), Alabama (71.5%) and South Carolina (66.4%).

Schulz says Chapter 7 may be a more attractive option than Chapter 13 for some consumers.

“For many financially stressed households, a clean slate with Chapter 7 makes all the sense in the world,” he says. “A Chapter 13 repayment plan requires steady income and the ability to commit to years of structured payments, which can be difficult when budgets are already stretched thin. Chapter 7 generally offers a faster path to discharging eligible debts, making it appealing for people who don’t see a realistic way to repay what they owe. With credit card balances at record highs and borrowing costs still elevated, more consumers may conclude that a fresh start is more practical than a long-term repayment plan.”

Meanwhile, Idaho was the only state where Chapter 13 filings were in the single digits, at just 7.4%. North Dakota (10.5%) and New Mexico (13.3%) followed.

Full rankings: States where Chapter 13 bankruptcies were most common in 2025

| Rank | State | Chapter 13 share of bankruptcy filings |

|---|---|---|

| 1 | Louisiana | 76.1% |

| 2 | Alabama | 71.5% |

| 3 | South Carolina | 66.4% |

| 4 | North Carolina | 65.6% |

| 5 | Tennessee | 57.6% |

| 6 | Arkansas | 57.3% |

| 7 | Georgia | 55.1% |

| 8 | Mississippi | 54.7% |

| 9 | Kansas | 46.3% |

| 10 | Pennsylvania | 45.7% |

| 11 | Kentucky | 45.6% |

| 12 | Missouri | 44.0% |

| 13 | Indiana | 43.9% |

| 14 | Illinois | 42.9% |

| 15 | Hawaii | 40.6% |

| 16 | Virginia | 40.3% |

| 17 | Texas | 39.5% |

| 18 | New Jersey | 38.0% |

| 19 | Delaware | 37.2% |

| 20 | Maryland | 37.0% |

| 21 | Wisconsin | 35.5% |

| 22 | Utah | 34.9% |

| 23 | Nebraska | 34.6% |

| 24 | New York | 32.8% |

| 25 | Michigan | 32.2% |

| 26 | Massachusetts | 31.8% |

| 27 | New Hampshire | 29.8% |

| 28 | Florida | 29.6% |

| 29 | Alaska | 29.2% |

| 30 | Rhode Island | 26.8% |

| 31 | District of Columbia | 26.0% |

| 32 | Ohio | 23.8% |

| 33 | Minnesota | 23.5% |

| 34 | South Dakota | 22.5% |

| 35 | Vermont | 22.4% |

| 36 | Oregon | 22.3% |

| 37 | Maine | 21.8% |

| 38 | Washington | 20.3% |

| 39 | Colorado | 18.5% |

| 40 | West Virginia | 18.1% |

| 41 | Oklahoma | 18.0% |

| 42 | California | 17.6% |

| 43 | Iowa | 17.3% |

| 44 | Arizona | 16.8% |

| 45 | Montana | 16.5% |

| 46 | Nevada | 16.4% |

| 47 | Connecticut | 15.7% |

| 48 | Wyoming | 15.1% |

| 49 | New Mexico | 13.3% |

| 50 | North Dakota | 10.5% |

| 51 | Idaho | 7.4% |

How to avoid reaching a financial breaking point

When debt starts to feel overwhelming, taking action early can make a significant difference. Understanding your financial situation and exploring available solutions before balances spiral out of control can help you regain stability and avoid more serious consequences.

- Take stock of your financial picture. Start by creating a complete inventory of your debts, including balances, interest rates and monthly payments. Pair that with a detailed review of your household budget to understand where your money is going and identify areas to free up cash for debt repayment.

- Explore repayment strategies while you still have options. If you’re still making progress on paying down debt, tools such as budgeting, debt consolidation or working with a nonprofit credit counselor may help you reduce what you owe more efficiently. Acting before you fall seriously behind on payments can increase your options and improve your chances of avoiding long-term financial damage.

- Recognize when it’s time to seek additional help. Warning signs such as routinely missing payments, using credit to cover basic necessities or watching balances grow despite your best efforts may indicate deeper financial distress. In those situations, speaking with a bankruptcy attorney can help you understand your options and determine whether bankruptcy or another form of debt relief makes sense for your situation.

Methodology

LendingTree researchers analyzed U.S. Courts bankruptcy filing data from 2021 through 2025. The analysis includes only nonbusiness bankruptcy filings across all chapters during the 12-month periods ending Dec. 31 of each year.

To account for differences in state population size, filing rates were calculated per 100,000 adults ages 18 and older using population estimates from the U.S. Census Bureau’s 2024 American Community Survey (ACS) one-year estimates.

Year-over-year changes reflect changes in bankruptcy filings during the 12-month periods ending Dec. 31, 2024, and Dec. 31, 2025.

Get debt consolidation loan offers from up to 5 lenders in minutes