Nearly 2 in 5 US Auto Loans Originate Below $25K, but Many Last 6 Years or Longer

Americans continue to face high vehicle prices, putting increasing pressure on household budgets. As a result, many car buyers appear to be scaling back their purchases and focusing on affordability when financing a vehicle.

According to a LendingTree analysis of active auto loans, more than a third (36.1%) of borrowers nationwide originally financed amounts of less than $25,000. Here’s a closer look at where smaller auto loans are most common, which borrowers are most likely to take them out and what consumers should know before committing to long-term auto financing.

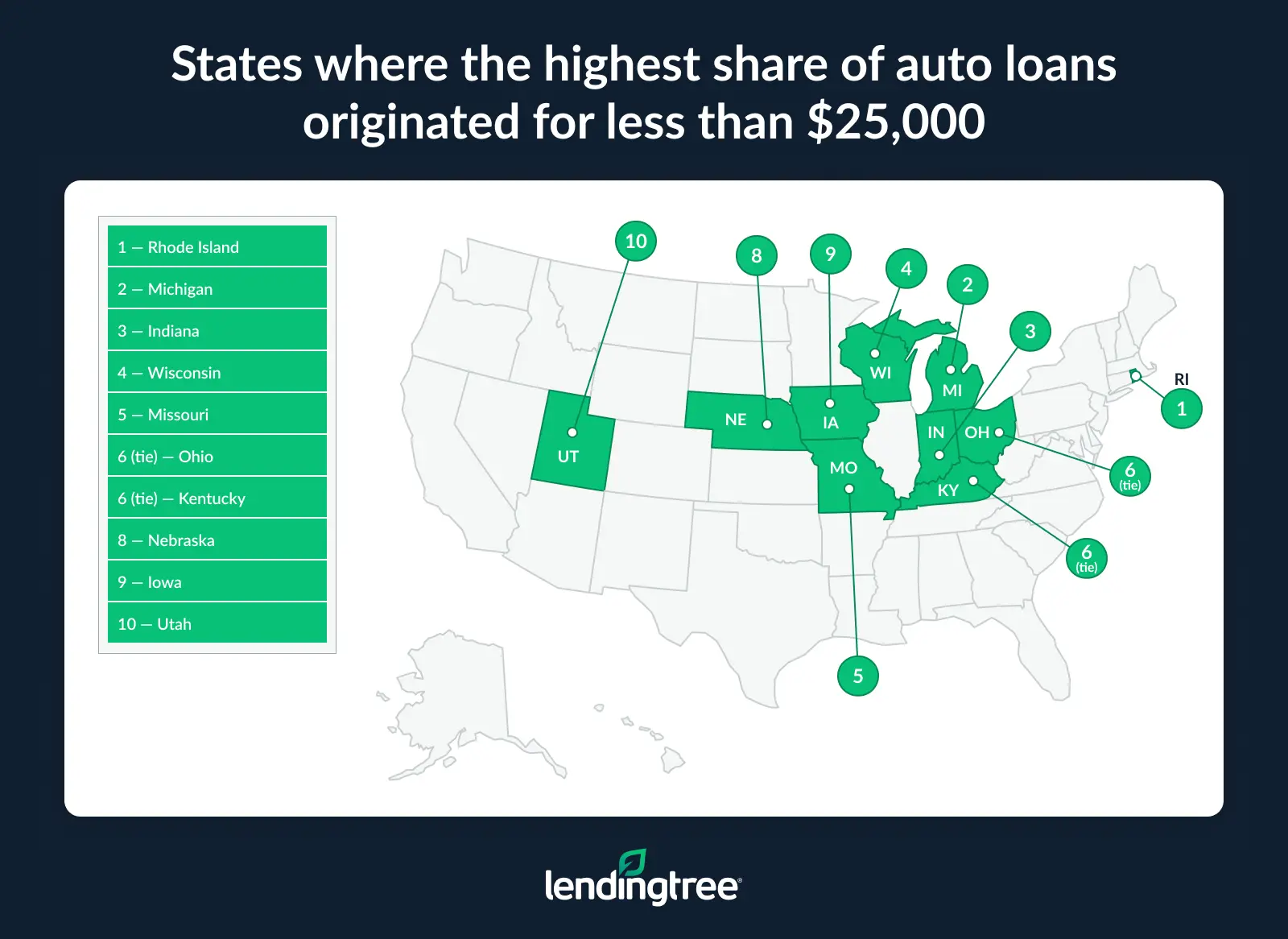

- Nearly 2 in 5 (36.1%) active auto loans nationwide originated for less than $25,000. Rhode Island (45.9%), Michigan (44.5%) and Indiana (44.3%) have the highest shares of loans originated for under $25,000, while Alaska (28.1%), Texas (28.7%) and Hawaii (29.5%) have the lowest.

- Gen Zers with active auto loans are much more likely than older borrowers to originate auto loans under $25,000. Nationally, 51.5% of Gen Z borrowers with active auto loans took out less than $25,000, compared with 36.2% of millennials and 31.4% of Gen X borrowers.

- Borrowers with lower credit scores are more likely to originate loans under $25,000, but they still often seek long repayment terms. Among subprime borrowers with credit scores below 620, 45.6% with active auto loans borrowed less than $25,000, compared with 30.4% of super-prime borrowers with scores of 720 or higher. No matter the credit score, under-$25,000 borrowers take out median loans of at least 60 months.

- Larger auto loans come with significantly higher monthly payments and are more likely to have long repayment terms. Loans of $25,000 or more have median monthly payments of $670, versus $212 for loans under $10,000, while 78.0% of $25,000-plus loans have terms of at least 72 months.

Nearly 2 in 5 auto loans start below $25,000

In an era of strained household budgets, car affordability is a major factor in consumers’ purchasing decisions. Nationwide, 36.1% of active auto loans originally financed amounts of less than $25,000, meaning nearly 2 in 5 borrowers entered the market with relatively modest loan amounts.

The share varies considerably by state. Rhode Island ranks first, with 45.9% of active auto loans originating below $25,000, followed by Michigan (44.5%) and Indiana (44.3%). Meanwhile, Alaska (28.1%), Texas (28.7%) and Hawaii (29.5%) have the smallest shares of active loans in that range.

Matt Schulz — LendingTree chief consumer finance analyst and author of “Ask Questions, Save Money, Make More: How to Take Control of Your Financial Life” — says these figures reflect how many buyers are adjusting their expectations to cope with today’s vehicle costs.

“It’s a clear sign that affordability is driving today’s car-buying decisions,” Schulz says. “Consumers are increasingly prioritizing lower monthly payments and manageable loan sizes over bigger vehicles or premium features. It also reflects how many buyers are turning to used cars and smaller models and making other compromises to make the numbers work in a high-rate, high-price environment.”

Full rankings: States where auto loans under $25K are most common

| Rank | State | % under $25,000 | Median starting balance |

|---|---|---|---|

| 1 | Rhode Island | 45.9% | $26,271 |

| 2 | Michigan | 44.5% | $26,743 |

| 3 | Indiana | 44.3% | $26,930 |

| 4 | Wisconsin | 43.4% | $27,069 |

| 5 | Missouri | 43.1% | $27,427 |

| 6 | Ohio | 42.8% | $27,320 |

| 6 | Kentucky | 42.8% | $27,246 |

| 8 | Nebraska | 42.3% | $27,785 |

| 9 | Iowa | 40.8% | $28,674 |

| 10 | Utah | 40.5% | $28,740 |

| 11 | Connecticut | 40.3% | $27,897 |

| 12 | Oregon | 39.8% | $28,660 |

| 13 | Massachusetts | 39.7% | $28,366 |

| 14 | New Hampshire | 39.6% | $28,264 |

| 15 | South Dakota | 39.5% | $28,233 |

| 16 | South Carolina | 39.2% | $28,677 |

| 16 | Kansas | 39.2% | $28,844 |

| 18 | Vermont | 39.1% | $28,630 |

| 19 | Pennsylvania | 38.8% | $28,244 |

| 20 | Minnesota | 38.7% | $29,096 |

| 21 | Idaho | 38.6% | $29,932 |

| 22 | Oklahoma | 38.1% | $29,333 |

| 22 | District of Columbia | 38.1% | $29,101 |

| 24 | Montana | 38.0% | $29,922 |

| 25 | Maine | 37.8% | $28,489 |

| 26 | Arkansas | 37.7% | $29,835 |

| 27 | Alabama | 37.5% | $29,770 |

| 28 | New Jersey | 37.1% | $29,280 |

| 29 | North Carolina | 37.0% | $29,675 |

| 29 | Colorado | 37.0% | $29,702 |

| 31 | Tennessee | 36.5% | $29,822 |

| 31 | Virginia | 36.5% | $29,900 |

| 33 | Mississippi | 35.7% | $29,866 |

| 33 | North Dakota | 35.7% | $30,467 |

| 35 | West Virginia | 35.4% | $30,279 |

| 35 | Illinois | 35.4% | $29,536 |

| 37 | New York | 35.3% | $29,724 |

| 38 | Delaware | 35.2% | $29,641 |

| 39 | Washington | 33.9% | $31,023 |

| 40 | New Mexico | 33.3% | $31,989 |

| 41 | Nevada | 33.2% | $31,489 |

| 41 | Georgia | 33.2% | $30,879 |

| 43 | Arizona | 33.0% | $30,953 |

| 44 | California | 32.7% | $31,539 |

| 45 | Maryland | 31.8% | $31,924 |

| 46 | Florida | 31.4% | $31,768 |

| 47 | Louisiana | 31.2% | $32,025 |

| 48 | Wyoming | 30.7% | $32,703 |

| 49 | Hawaii | 29.5% | $32,711 |

| 50 | Texas | 28.7% | $33,000 |

| 51 | Alaska | 28.1% | $34,622 |

Young consumers lead the shift toward smaller auto loans

Younger borrowers are far more likely than older ones to finance less expensive vehicles.

More than half (51.5%) of Gen Z consumers (ages 18 to 28 in 2025) with active auto loans originally borrowed less than $25,000. That’s significantly higher than the share among baby boomers ages 61 to 79 (36.4%), millennials ages 29 to 44 (36.2%) and Gen Xers ages 45 to 60 (31.4%).

Gen Z borrowers also have the lowest median starting loan balance ($24,567), the lowest median credit score (649) and the lowest median monthly payment at $493. By comparison, Gen X borrowers have a median starting balance of $31,945 and a median credit score of 700, while baby boomers have the highest median credit score of 756.

Auto loan stats by generation

| Generation | % under $25,000 | Median starting balance | Median monthly payment | Median credit score |

|---|---|---|---|---|

| Gen Z | 51.5% | $24,567 | $493 | 649 |

| Millennial | 36.2% | $29,876 | $564 | 664 |

| Gen X | 31.4% | $31,945 | $582 | 700 |

| Baby boomer | 36.4% | $29,826 | $537 | 756 |

While budget concerns play a key role, Schulz says affordability isn’t the only explanation.

“Gen Zers likely don’t have as easy access to credit as other generations do,” he says. “They’re in the process of building their careers and their credit scores, so they’re a bigger risk for lenders.”

With shorter credit histories and lower average incomes than older borrowers, many Gen Z consumers may find smaller loans to be the most realistic path to vehicle ownership.

Smaller loan amounts are more common among subprime borrowers

Loan size varies significantly by credit profile, with borrowers who have lower credit scores generally taking out smaller auto loans.

Among consumers with subprime credit scores below 620, 45.6% of active auto loans originated for less than $25,000. That share falls steadily as credit scores rise, dropping to 38.5% among near-prime borrowers (620 to 659), 33.4% among prime borrowers (660 to 719) and 30.4% among super-prime borrowers (720 or higher).

The pattern suggests that borrowers with weaker credit may be more likely to shop for lower-cost vehicles, whether because of lender restrictions, affordability concerns or both.

However, smaller loan balances don’t necessarily translate into easier repayment terms.

Among borrowers with under-$25,000 auto loans, repayment terms remain lengthy across nearly every credit tier. The median term is 72 months for subprime and prime borrowers and 71 months for near-prime borrowers. Only super-prime borrowers are likely to pay off smaller loans more quickly, with a median term of 60 months.

Monthly payments also remain substantial despite the smaller loan sizes. Subprime borrowers with loans under $25,000 have a median monthly payment of $417, compared with $381 for near-prime borrowers, $360 for prime borrowers and $348 for super-prime borrowers.

Auto loan stats by credit score tier

| Credit score tier | % under $25K | Median term among under-$25,000 loans | Median monthly payment among under-$25,000 loans |

|---|---|---|---|

| Under 620 (subprime) | 45.6% | 72 months | $417 |

| 620-659 (near-prime) | 38.5% | 71 months | $381 |

| 660-719 (prime) | 33.4% | 72 months | $360 |

| 720 and up (super-prime) | 30.4% | 60 months | $348 |

Schulz says extended loan terms are often one of the few tools available to borrowers with weaker credit who are trying to keep monthly costs manageable.

“Long-term loans remain common among subprime borrowers because they’re often the only way to make monthly payments fit within tight budgets,” he says. “Higher interest rates can dramatically raise payments, so extending the loan term helps ease some of that pressure, at least on a monthly basis.”

The trade-off, however, can be costly.

“Longer terms can make an already expensive loan even more costly over time and increase the odds of borrowers owing more than the car is worth,” Schulz says.

Even when purchasing less expensive vehicles, borrowers with lower credit scores often face a combination of higher interest rates, higher monthly payments and longer repayment periods than consumers with stronger credit profiles.

Longer loan terms create additional financial risks

Borrowers with larger auto loans are much more likely to spend years paying off their vehicles. Among active auto loans, 63.9% were originated for $25,000 or more, and those loans carry a median starting balance of $37,588 and a median monthly payment of $670.

How borrowing burden changes across auto loan bands

| Auto loan bands | % of auto loans | Median starting balance | Median term | Median monthly payment | Median credit score | % with term ≥72 months |

|---|---|---|---|---|---|---|

| Under $10,000 | 3.3% | $7,992 | 48 months | $212 | 651 | 8.5% |

| $10,000 to $14,999 | 7.2% | $12,850 | 60 months | $293 | 658 | 25.3% |

| $15,000 to $19,999 | 11.7% | $17,619 | 69 months | $364 | 664 | 48.9% |

| $20,000 to $24,999 | 14.0% | $22,520 | 72 months | $432 | 674 | 65.4% |

| $25,000+ | 63.9% | $37,588 | 72 months | $670 | 704 | 78.0% |

By comparison, loans under $10,000 make up just 3.3% of active auto loans and have a median monthly payment of $212. As loan sizes rise, payments generally climb: $293 for loans of $10,000 to $14,999, $364 for loans of $15,000 to $19,999 and $432 for loans of $20,000 to $24,999.

Repayment terms also tend to stretch as loan amounts increase. Just 8.5% of loans under $10,000 have terms of at least 72 months, compared with 25.3% of loans from $10,000 to $14,999, 48.9% of loans from $15,000 to $19,999 and 65.4% of loans from $20,000 to $24,999. Among loans of $25,000 or more, that share jumps to 78.0%.

While extending a loan term can reduce the monthly payment, Schulz says consumers should be cautious before committing to six- or seven-year repayment periods.

“They should be quite concerned about taking on longer-term loans, even if they lower the monthly payment,” he says. “Longer terms often mean paying far more in interest over time and increase the risk of being upside down on the loan if the car’s value drops faster than the balance.”

In many situations, he says, a lengthy repayment schedule may indicate that the vehicle is simply too expensive.

“If a 72- or 84-month loan is the only way the payment works, it may be worth considering a less expensive vehicle.”

How to keep your next auto loan affordable

For consumers shopping for a vehicle this year, Schulz recommends focusing on long-term affordability rather than the monthly payment alone.

His top tips include:

- Look beyond the monthly payment. A lower monthly payment can seem appealing, but it often comes at the cost of a longer repayment term. That can add thousands of dollars in interest over the life of the loan and significantly increase the total amount paid for the vehicle.

- Buy less car than you qualify for. Just because a lender approves a certain loan amount doesn’t mean borrowing that much is a good idea. Choosing a less expensive vehicle can help keep monthly payments manageable, provide more room in your budget for other expenses and reduce the risk of becoming upside down on the loan.

- Shop around before making a decision. Comparing loan offers from multiple lenders and improving your credit score before applying can help you secure a lower interest rate. Consumers should also compare vehicle prices across dealerships and sellers. “It isn’t just about financing,” Schulz says. “Shopping around for the actual vehicle itself can lead to big savings, too, and it has never been easier to do.”

Methodology

LendingTree researchers analyzed about 154,000 anonymized credit reports of LendingTree users with active auto loan accounts from Oct. 1 to Dec. 31, 2025.

The analysis included new and used vehicle loans, including individual and joint accounts. For each borrower, researchers selected one representative active auto loan, defined as the active auto tradeline with the largest current balance.

The starting balance was based on the tradeline’s highest reported balance and was used as a proxy for the financed amount. Monthly payments, loan terms and borrower credit scores were analyzed nationally and across borrower segments.

Researchers calculated the share of selected active auto loans with starting balances below $25,000 by state, generation and credit score tier. Loan-size band analyses also examined median starting balances, loan terms, monthly payments and the share of loans with terms of at least 72 months. Credit score tiers were defined as subprime (below 620), near-prime (620 to 659), prime (660 to 719) and super-prime (720 or higher).

We defined generations as follows based on age in 2025:

- Generation Z: 18 to 28

- Millennials: 29 to 44

- Generation X: 45 to 60

- Baby boomers: 61 to 79

Get auto loan offers from up to 5 lenders in minutes