How To Refinance a Car Loan With Bad Credit

Somehow, your bank account dwindles just as the car payment is due. It’s tough keeping up with high car payments, and made worse by high interest rates due to bad credit. You feel stuck in a stressful situation. One way to reduce your financial stress is by refinancing your auto loan. You may be able to get a better interest rate, a lower monthly payment, or a shorter term.

If you have less than excellent credit, you may worry about whether you’ll be approved for a better loan. We’ll walk through the things you need to know to improve your odds of refinancing a car loan with bad credit.

- It’s possible to refinance your car with bad credit or a FICO Score below 580.

- If a lower rate isn’t an option, a longer loan term can still cut your monthly payment.

- You can check your rates without hurting your credit by shopping with LendingTree or by prequalifying on lenders’ websites.

Can you refinance a car loan with bad credit?

Yes, you may be able to refinance your car loan with bad credit. However, you’ll likely have to shop around, and your loan may carry a high annual percentage rate (APR), which includes interest and fees.

Still, depending on your credit score when you first got your car loan, you might qualify for a lower rate, especially if your financial situation has improved.

A LendingTree study found that refinancing your car loan could save you an average of $142 a month and $1,346 over the life of your loan. If you refinance for a shorter loan term, you could save significantly more — $6,291 on average.

Even if you have bad credit, refinancing may be worth it. You might qualify for a lower rate and pay less interest by swapping a longer repayment term for a shorter one. Or, if you’re having trouble keeping up with payments, consider extending your loan term. This will give you a lower monthly payment. However, you’ll pay more interest over the life of your loan.

How bad can your score be to refinance?

There’s no industry minimum standard credit score to be approved to refinance an auto loan, but higher scores are eligible for better rates. OpenRoad Lending refinances car loans for people with credit scores as low as 460. With a score of 600, you’ll be eligible for standard rate offers. At 700 or above, you may be eligible for more attractive rates. Loan options exist; the key is knowing where to find the best option for you.

LendingTree is one of the nation’s longest-standing loan marketplaces, and we understand that you’re more than just your score. We’ll help you find lenders that specialize in what you need.

Will refinancing lower my payment if my rate doesn’t improve?

Qualifying for auto refinancing doesn’t mean that your rate will be lower than what you’re currently paying. Even if you don’t qualify for a lower rate, you can refinance for a longer term, which will lower the monthly payment. However, be aware that you will pay more interest than with a shorter-term loan. Still, it might give you the breathing room you need to keep up with your payments.

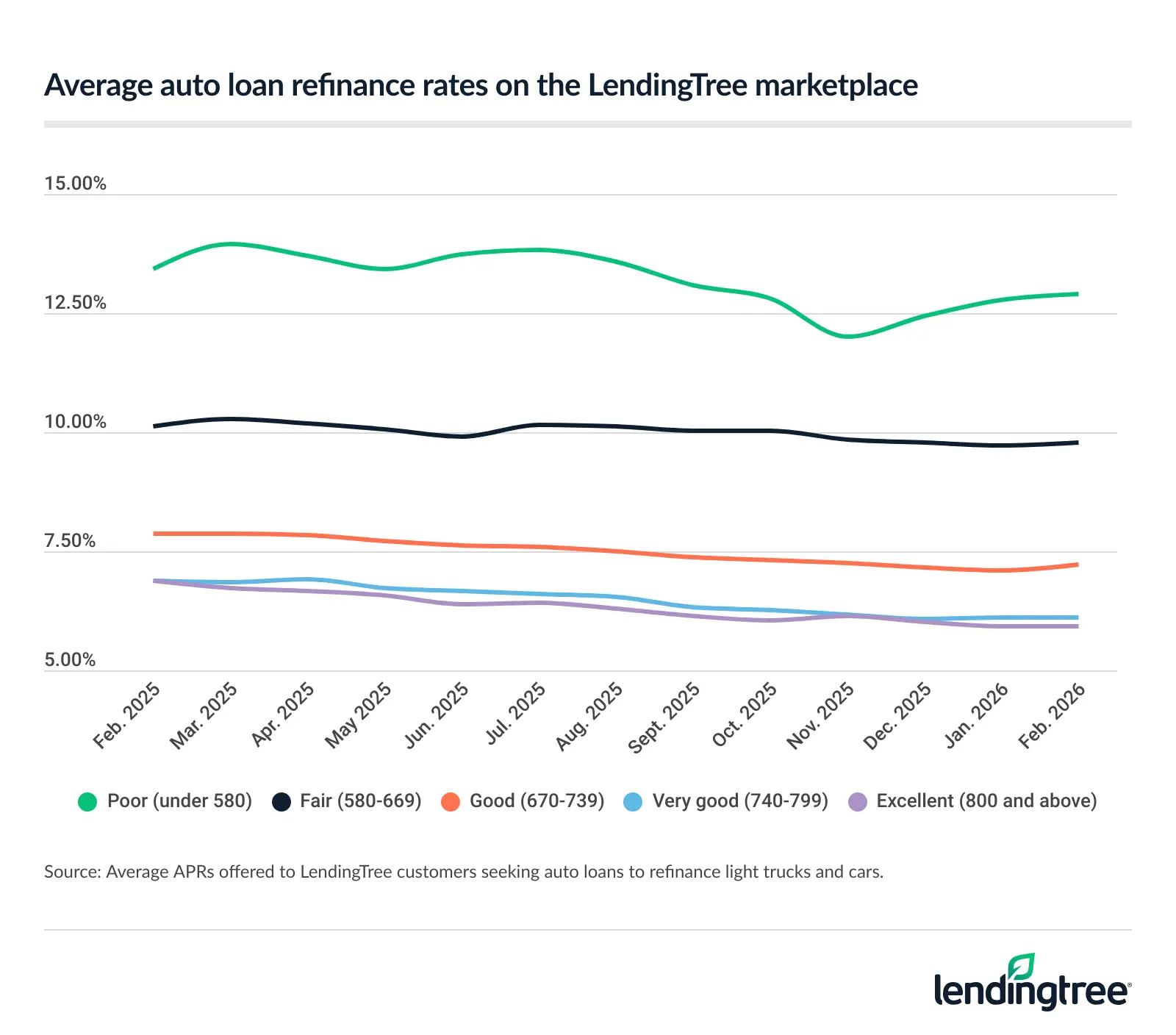

To get an idea of what your rates might look like, compare your current rate with the average offers that LendingTree users received in the third quarter of 2025. If it looks like you qualify for something better, use our auto refinance calculator to see how much you might save.

| Credit tier | Average APR | Average amount | Average term |

|---|---|---|---|

| Excellent (800 and above) | 6.30% | $33,249 | 67 months |

| Very good (740-799) | 6.48% | $35,892 | 66 months |

| Good (670-739) | 7.50% | $30,196 | 66 months |

| Fair (580-669) | 10.10% | $29,129 | 66 months |

| Poor (under 580) | 13.38% | $27,337 | 67 months |

Tracking bad credit car refinancing rates over time

Auto loan refinance rates have been holding fairly steady, though rates for bad credit are trending down on average. But no one truly knows how tariffs and the Fed will impact auto refinancing rates going forward.

Believe it or not, tariffs could improve your odds of approval for auto refinancing. Here’s why:

- Tariffs may cause all car values to rise, either directly or indirectly, through increased material costs. The most noticeable difference will be on certain brand-new cars, if imported.

- Used car demand may go up. More people may opt for a used car to skip tariffs. As the demand for used cars goes up, so does their value.

- A better loan-to-value (LTV) ratio means better approval odds. If your car goes up in value, your loan-to-value (LTV) ratio will go down. This is a good thing for lenders. LTV measures how much you owe compared to how much your car is worth.

Putting it all together, imagine you owe $18,000 on a $16,000 car. This is an LTV of 113%, and LTVs above 100% are a red flag.

After tariffs, your car’s value increases to $18,500, giving you an LTV of 97%. Lenders may be more willing to refinance since you are no longer upside down on your car loan. LTV is a common eligibility requirement for refinancing, regardless of credit score.

How auto refinancing can help, even with bad credit

To illustrate how refinancing a car with bad credit can help, here’s a hypothetical scenario:

Meet John. He has a 500 credit score. When his car broke down, he bought a car at a buy-here, pay-here lot. His loan came with an 18% APR and weekly payments, which were tough to keep up with.

A year later, John refinanced. His new lender offered the same rate (18%) and term, but switched him to monthly payments instead of weekly.

John didn’t save money on interest, but refinancing made his payments easier to manage. More importantly, he’s now with a traditional lender that reports his payments to the credit bureaus. Buy-here, pay-here lenders don’t. This will give him a better chance of refinancing again and getting lower rates in the future.

Should I refinance my car if I have bad credit?

Your credit score isn’t the only thing that matters when it comes to auto refinancing. Even if your credit is bad, it could still be the right time to refinance your car.

Consider refinancing if…

- You’ve improved your credit score: Even if your credit score is low, you might qualify for a better loan if your score is better than it was when you took out your current loan.

- Your car has equity: If your car is worth more than you owe, you have equity. Lenders will be more likely to approve you for refinancing since they face less risk.

- You can’t afford your current payments: Refinancing can reduce your monthly car payment by stretching it out over a longer term. You will likely pay more money in interest over the life of the loan, but refinancing could be worth it if it’s the only way you can afford to keep up with your car payments.

- You can add a cosigner: Having an auto loan cosigner could help you get a better interest rate. Just make sure your cosigner understands they’re agreeing to be 100% responsible for any missed loan payments.

Avoid refinancing if…

- Your credit score has dropped: If your credit score has fallen since you took on your car loan, you probably won’t get a better deal on a refinance.

- Market rates are high: When interest rates rise, borrowing becomes more expensive. If auto refinance rates are higher than when you took out your loan, you’ll have a hard time finding a cheaper refinance option.

- You’re near the end of your loan: Refinancing is less likely to save you money if you have only a year or two of payments left. In fact, it could end up costing you more due to new lender fees and higher interest charges early on. That’s because auto refinance loans are amortized, meaning you pay more interest at the beginning of the term and more principal toward the end. Restarting your loan resets that cycle.

Compare car refinance loans with Lending Tree

You could save an average of $142 a month on your auto loan by refinancing, according to a LendingTree study. LendingTree makes it easy. Instead of applying to just one lender and hoping for a good rate, see multiple lenders compete for your business — so you can choose the best offer.

Tell us what you need

Take two minutes to tell us what you need to refinance. We’ll take care of the rest. It’s free, simple and secure.

Shop your offers

We’ll send you offers from up to five trusted lenders. Compare them to see if you can save money or lower your car payment.

Get refinanced

Choose an offer, finalize your loan and you could have the money you need within 24 hours.

What if I can’t afford my car loan and don’t qualify for refinancing?

It might not feel like it, but you still have options if you can’t afford your car and you can’t get refinanced.

First, call your lender and see if it offers a hardship program. You may be able to extend your existing loan term. This means you’ll likely pay more overall interest but a lower monthly payment. But you won’t have to qualify for a new loan.

If your lender won’t modify your loan, you could:

- Sell your car (but you will need to pay the difference if you owe more than you can sell it for)

- Request a voluntary repossession (this will hurt your credit, but usually less so than if it were involuntary)

- File for bankruptcy (if you also have other debts you can’t afford)

To learn more, read about how to get out of a car loan you can’t afford.

Frequently asked questions

Yes, some lenders offer auto refinancing for credit scores of 500 or lower. These include OpenRoad Lending, Capital One and RefiJet.

However, the interest rates on these loans are usually high, so you may not save money by refinancing. Keep an eye out for predatory lenders that take advantage of people with bad credit.

You can refinance a car loan even if your credit score is near or below 500. But the lower your score, the harder it is to get approved, even with lenders that specialize in bad credit car loans. If you aren’t sure what your score is, check it for free with LendingTree Spring. We’ll also give you personalized tips that can help you improve your credit score.

Lenders have varying car loan eligibility requirements. You could be disqualified due to bad credit or a high debt-to-income ratio (DTI). It’s common for lenders to restrict a car’s age and mileage, and many won’t refinance cars 10 years old or older or with more than 100,000 to 150,000 miles.

Yes, refinancing hurts your credit score because it requires a hard credit hit. This drop will likely be small and temporary as long as you make your car payments on time. In the long run, your credit can actually improve if you stay current on your loan payments.

Before you apply to refinance your car loan, have these documents and information on hand:

- Account number

- 14-day payoff amount for your current loan

- Your financial information (proof of income, employment and residence)

- Lender’s name and contact information

- Vehicle make and model

- Vehicle Identification Number (VIN)

- Exact mileage

- Proof of insurance

Compare Auto Loan Offers